SELF - Mining For Small Cap REIT Gems

2023-11-09 07:00:00 ET

Summary

- The stock market is dominated by big tech companies, but there are opportunities for small-cap stocks, particularly in the REIT sector.

- Small-cap REITs were impacted by COVID, and have just started to recover.

- Read about three small-cap comeback REITs that shouldn’t be ignored.

History books are filled with big stories about big people.

Take Alexander the Great, who “overthrew the Persian empire, carried Macedonian arms to India, and laid the foundation for the Hellenistic world of territorial kingdoms,” to quote Britannica .

The History Channel adds how he was:

“… One of history’s greatest military minds who, as king of Macedonia and Persia, established the largest empire the ancient world had ever seen.

By turns charismatic and ruthless, brilliant and power hungry, diplomatic and bloodthirsty, Alexander inspired such loyalty in his men they’d follow him anywhere and, if necessary, die in the process.

Though Alexander the Great died before realizing his dream of united a new realm, his influence on Greek and Asian culture was so profound that it inspired a new historical epoch – the Hellenistic Period.”

Or how about George Washington?

He rallied a ragtag group of Americans to victory over the greatest military force of its time. Despite facing defeat after defeat after setback, he ended up inspiring a new nation into existence anyway with his courage and commitment.

How many other influential people do we learn about before high school’s end, both good and bad?

How about Martin Luther King, Jr. and Winston Churchill, King Tut and Napoleon, Stalin and Mussolini, Queen Elizabeth and Karl Marx, Mark Twain and Aristotle, Muhammad and Genghis Khan, Michelangelo and Mahatma Gandhi, Shakespeare and Plato.

They all easily earned their places in history.

I take no issue with that fact.

Only perhaps we should hear a lot about the little guys too.

An Ode to the Little Guy

It’s impossible to know all the little guys instrumental in every history-changing operation ever.

But that doesn’t mean they didn’t help change the world.

For instance, General Washington sacrificed so much – his finances, his physical safety, and his emotional wellbeing – for what he believed in.

But so did thousands of nameless Continental soldiers.

According to American Battlefield Trust’s website, American Battlefield Trust :

“Throughout the course of the war, an estimated 6,800 Americans were killed in action, 6,100 wounded, and upwards of 20,000 were taken prisoner. Historians believe that at least an additional 17,000 deaths were the result of disease, including about 8,000-12,000 who died while prisoners of war.”

Admittedly, if one of those men hadn’t signed up for duty, it probably wouldn’t have made a difference. The war would have gone and ended the same way, which can’t be said about Washington’s presence.

Still, I do think we need to be more careful about discounting the little guy.

Because sometimes he (or she) really comes through.

I fully realize I may have annoyed one group of readers with that previous example. And I know I’m going to annoy another by bringing up Super Bowl LII.

But other than die-hard Philadelphia fans, nobody thought the Eagles could win.

Did you watch the pre-game coverage?

The NFL presentation featured one Patriot fan after another recounting their favorite Super Bowl victory. And we know they had their pick.

As for the Eagles’ side of the equation… there was a very old man interviewed who said in a trembling voice how he’d waited his whole life to see the Eagles win the Super Bowl.

It was a joke.

Everyone knew the little guy was going down.

Yet the Patriots lost 33-41, allowing that old man to have the last laugh after all.

The Magnificent 7 Tries to Take It All

Now let me point to a stock market example of how easy it is for the little guys to get lost in the crowd.

“It’s a lopsided world. Stock markets are a seesaw with the so-called Magnificent Seven on one side and everything else on the other side.” Apple ( AAPL ), Amazon ( AMZN ), Alphabet ( GOOGL ), Meta Platforms ( META ), Microsoft ( MSFT ), Nvidia ( NVDA ), and Tesla ( TSLA ) “played an outsize role in this year’s stock market rally.”

The S&P 500, it turns out, “has delivered total returns of more than 13% this year.” But remove those seven tech stocks, and “the index is about flat.”

Nobody loves the little guys right now. They’re just not enticing compared to the power of big tech with their AI possibilities. People want to be part of the rally, not lagging behind.

You could say that’s especially evident in real estate investment trusts, or REITs. They’re suffering from very little investor interest this year, as shown by their depreciated share prices.

But is that deserved?

In a few cases, yes.

There always are going to be examples of distressed REITs, especially after an enormously impactful negative event like we had in 2020. We’re still trying to figure out how certain companies can really come back from it.

However, those are just some examples.

They don’t represent the entire sector.

Not even close.

This brings me right back to that Barron’s article.

It goes on to say that the current lopsided market “presents a ‘once in a generation opportunity’ in everything except those companies, says Richard Bernstein Advisors.”

And while he may or may not have been thinking specifically about REITs when he conveyed that image, I definitely am. Let me introduce you to three small-cap comeback stories in the making that really shouldn’t be discounted.

These David-vs.-Goliath stories are too good not to read about.

CTO Realty ( CTO ) – Market Cap: $383.85 million

Before taking its current name, CTO Realty was known as Consolidated Tomoka Land and for years the company primarily held undeveloped land in Florida and at one time was one of the largest property owners in Daytona Beach.

For well over a decade CTO has been selling off its legacy assets (undeveloped land) and has been reinvesting its capital into income-producing properties across multiple states.

In 2020, the company changed its name to CTO Realty Growth and converted from a regular C-Corp to a real estate investment trust (“REIT”) that same year.

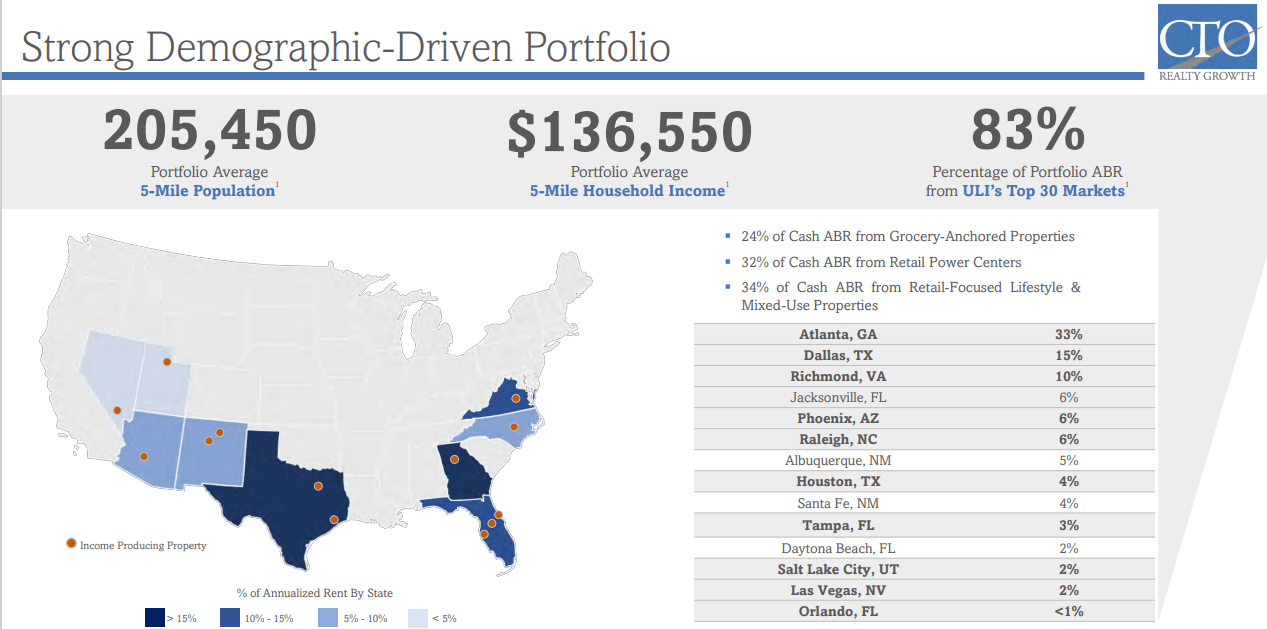

CTO Realty Growth is a shopping center REIT that invests in retail-based, multi-tenanted properties that are anchored by a grocery store or a lifestyle center and are primarily located in Southeast and Southwest regions of the country.

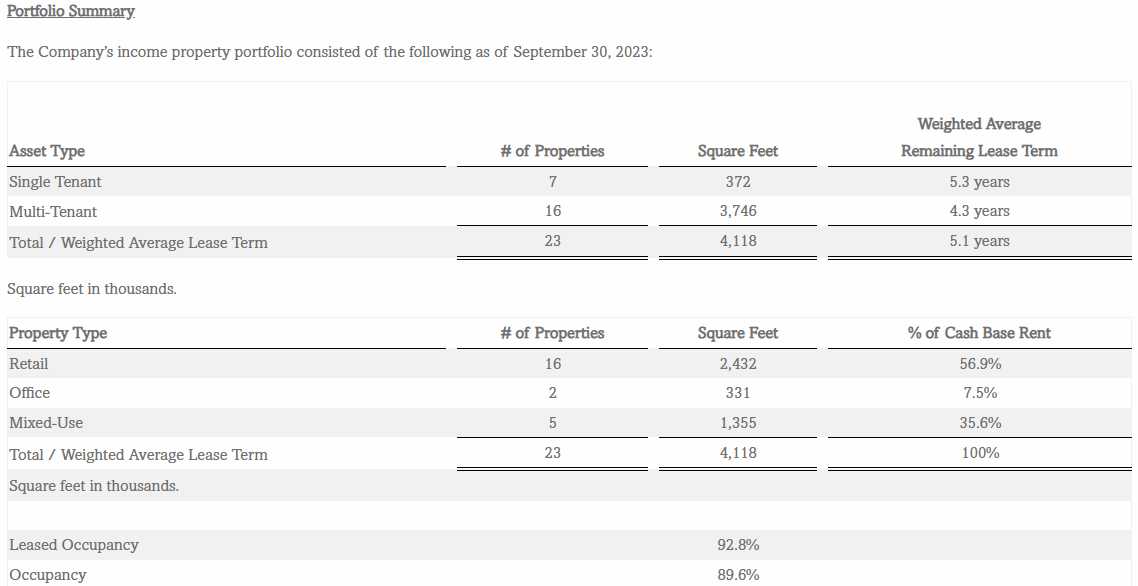

CTO owns or has an ownership interest in 23 properties covering 4.1 million square feet across 14 markets in nine states with a portfolio occupancy of 89.6% as of their most recent update.

In addition to its portfolio of shopping centers, CTO is also the external manager for Alpine Income Property Trust ( PINE ), which is a pure play net lease REIT that invests in single-tenant properties.

CTO has a meaningful stake in PINE with approximately a 15% ownership position and receives management fees and dividend income from the net-lease REIT in addition to the rental income it receives from its portfolio of shopping centers.

{kind=link}

On Oct. 26 CTO released its third quarter operating results and reported total revenues during the third quarter of $28.5 million, compared to $23.1 million in the third quarter of 2022. Core Funds from Operations (“Core FFO”) came in at $10.5 million, or $0.47 per share during the quarter, compared to Core FFO of $8.7 million, or $0.47 per share for the same period in 2022.

Adjusted Funds from Operations (“AFFO”) came in at $10.8 million, or $0.48 per share during quarter compared to $8.9 million, or $0.49 per share in the third quarter of 2022.

The company also provided a current breakdown of its properties, listing 16 retail properties, two office properties, and five mixed-use properties which combined have a weighted average lease term of 5.1 years and a portfolio occupancy of 89.6%.

{kind=link}

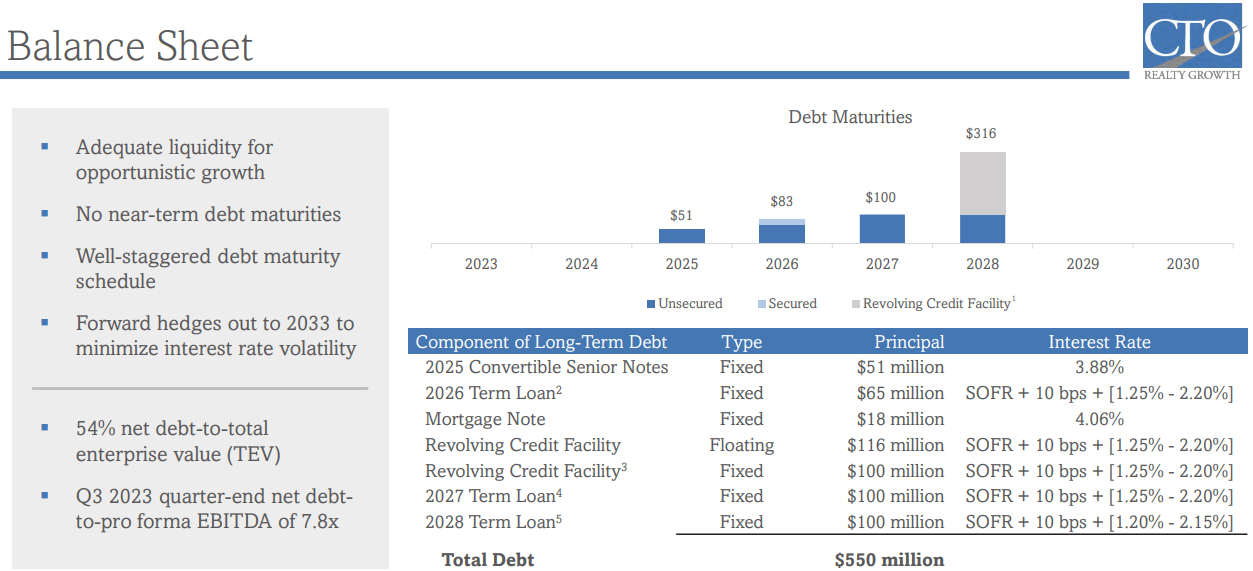

During the earnings release, CTO also highlighted the strength of the balance sheet with a well-staggered debt maturity schedule and no debt maturities until 2025.

They reported a net debt to pro forma EBITDA of 7.8x, a fixed charge coverage ratio of 2.6x, and a net debt to total enterprise value of 54.0%.

{kind=link}

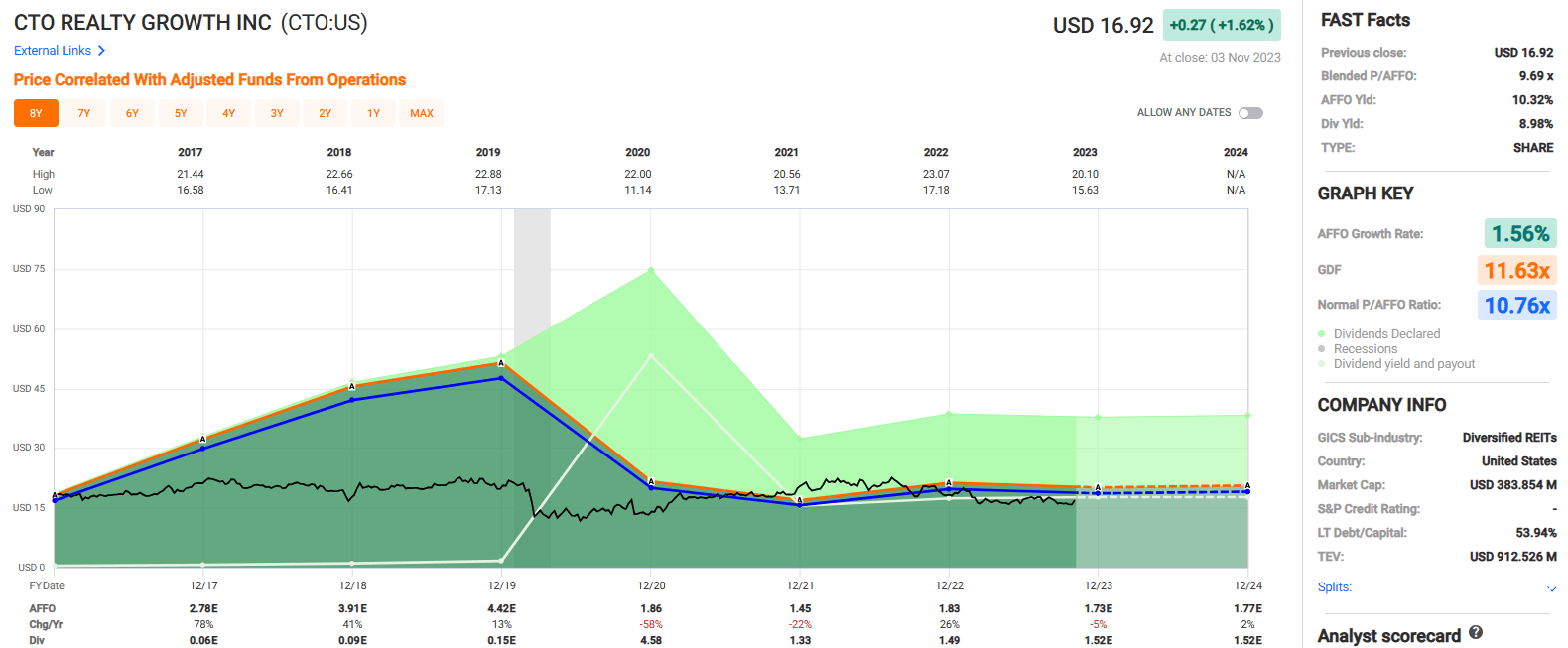

Since CTO only converted to a REIT in 2020 we don’t have many years to review this company as it is currently structured.

After its conversion in 2020, AFFO fell from $1.86 to $1.45 per share in 2021, marking a -22% decline in AFFO, but then increased by 26%, to $1.83 per share the following year.

Analysts expect AFFO to fall by -5% in 2023, but then to grow by 2% in 2024. CTO pays an 8.98% dividend yield with a 2022 year-end AFFO payout ratio of 81.60%, and a projected 2023 AFFO payout ratio of approximately 88%.

Currently the stock is trading at a P/AFFO of 9.69x, which compares favorably to their normal AFFO multiple of 10.76x.

We rate CTO Realty Growth a Strong Buy.

{kind=link}

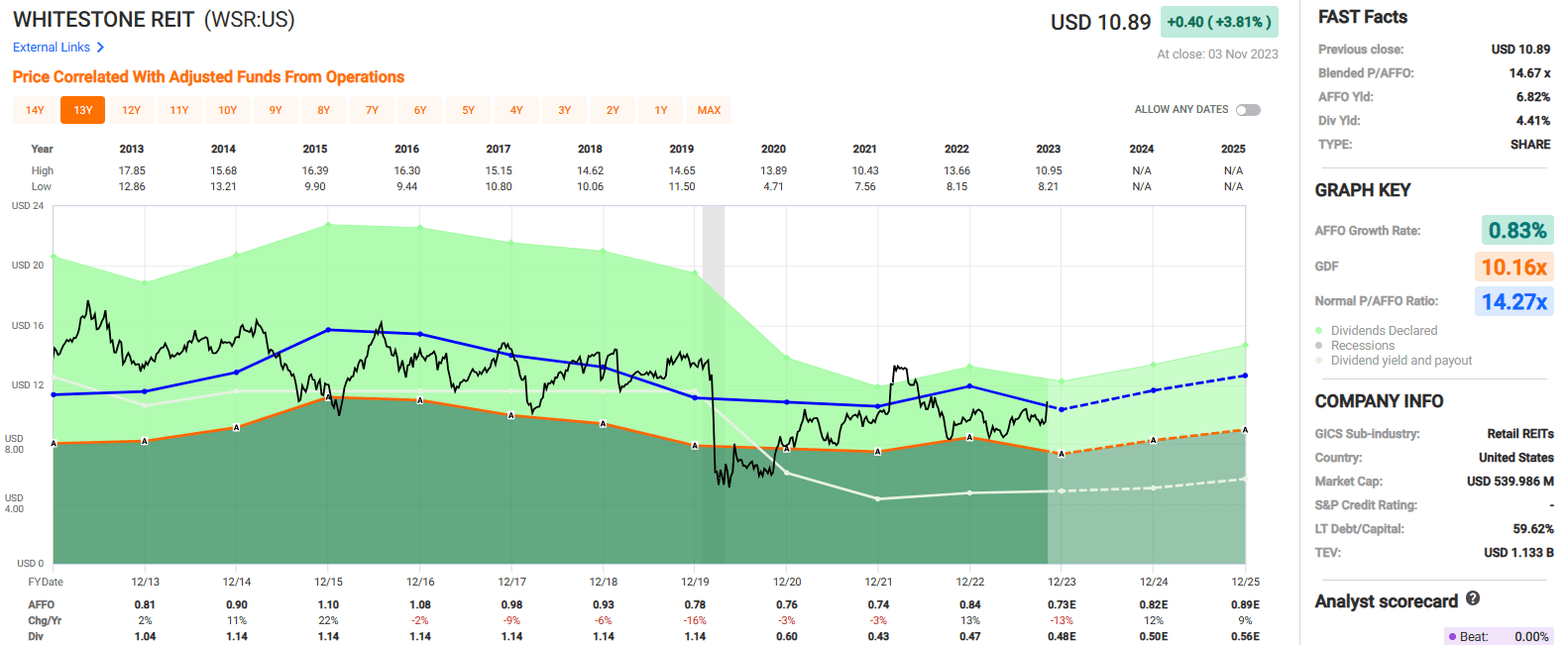

Whitestone REIT ( WSR ) – Market Cap: $539.98 million

Whitestone REIT specializes in the development, acquisition, and ownership of open-air retail shopping centers that are primarily located in the Sunbelt region of the country.

The vast majority of their properties are located in two states, Arizona and Texas, and their largest markets are Phoenix which makes up approximately 42% of their property net operating income (“NOI”), followed by Houston which makes up roughly 25% of their property NOI.

WSR also has a significant presence in the Austin / San Antonio area and the Dallas / Fort Worth area, which make up 15% and 18% of their property NOI, respectively.

WSR looks to acquire properties with tenants that operate in service-oriented industries including grocery stores, restaurants, fitness and educational centers.

Their largest industry is Restaurants & Food Services which contributed roughly 25% to their annualized base rent (“ABR”), followed by Salons which contributed 9%, and Grocery Stores which contributed 8% of their ABR as of their most recent update.

As of the end of the third quarter, WSR owned 56 properties covering around 5.0 million square feet of gross leasable area (“GLA”) that were leased to approximately 1,455 tenants with a portfolio occupancy of 92.7%.

{kind=link}

On Oct. 31 Whitestone REIT released its third quarter operating results and reported total revenues during the quarter of $37.1 million, compared to total revenues of $35.4 million during the third quarter of 2022.

Normalized FFO was reported at $11.7 million, or $0.23 per share compared to Normalized FFO of $12.4 million, or $0.24 per diluted share in the third quarter of 2022. Management attributed the decrease in normalized FFO to higher litigation and interest expenses.

EBITDAre for the quarter came in at $20.4 million, compared to $19.4 million for the same period in 2022 and same-store NOI increased from $22.1 million during the third quarter of 2022, to $23.2 million during the third quarter of 2023, representing a year-over-year same-store NOI growth rate of 4.9%.

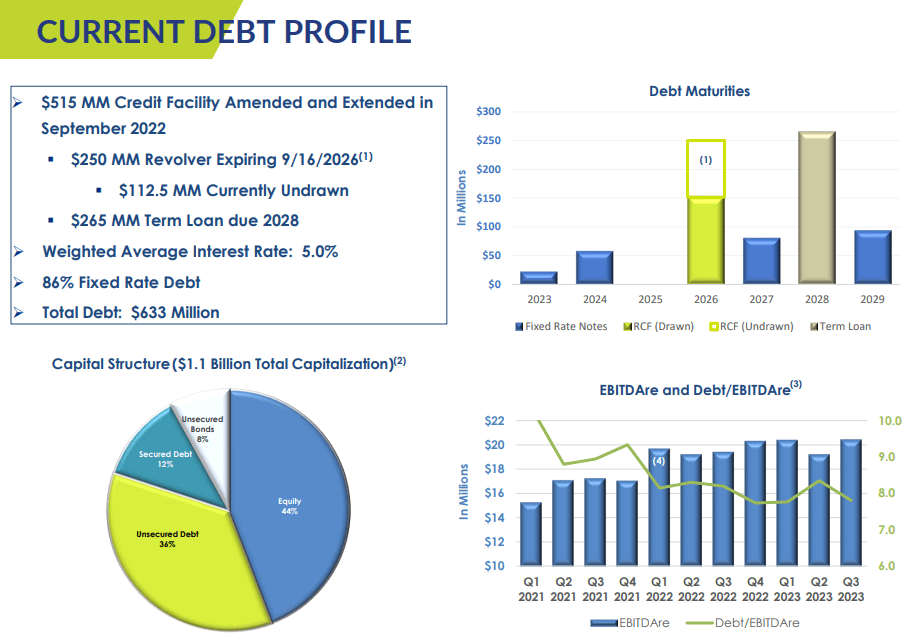

WSR also provided updates on its financial health and reported total debt of $633.2 million, under-appreciated real estate assets of $1.2 billion, and $112.5 million available to them under their revolving credit facility.

WSR has a debt to pro forma EBITDAre of 7.8x and a long-term debt to capital ratio of 59.62%. Additionally, debt has a weighted average interest rate of 5.0% and 86% of their debt is fixed rate.

{kind=link}

Whitestone REIT pays a monthly dividend and has consistently made monthly distributions for more than 15 years, but they have had issues maintaining their dividend in the past.

WSR increased its dividend by approximately 9.0% in 2014 but maintained that same rate from 2015 to 2019. In 2020, they cut their dividend from $1.14 to $0.60 per share, representing a -47.37% dividend cut, and then cut the dividend again by -28.75% in 2021.

It would be easy to attribute the dividend cut in 2020 to the COVID pandemic, but WSR’s AFFO per share only fell -3% in both 2020 and 2021.

The more likely reason for the dividend cuts is the unsustainable AFFO payout ratio the company had from 2011 to 2019 when it was more than 100% each year.

After the dividend cut in 2021, WSR’s AFFO payout ratio improved to 55.99% as of the end of 2022 and is expected to be approximately 66% in 2023.

Currently WSR pays a well-covered dividend yield of 4.41% and trades at a P/AFFO of 14.67x, which is in line with their normal AFFO multiple of 14.27x.

Even with WSR’s troubled past, we view their current dividend as secure given the REIT’s low AFFO payout ratio and analysts’ estimates for AFFO per share to increase by 12% in 2024 and then increase by 9% in 2025.

We rate Whitestone REIT a Spec Buy.

{kind=link}

Global Self Storage ( SELF ) – Market Cap: $50.93

Global Self Storage is an internally managed REIT that acquires, owns, and operates self-storage properties that are leased to both commercial and residential customers.

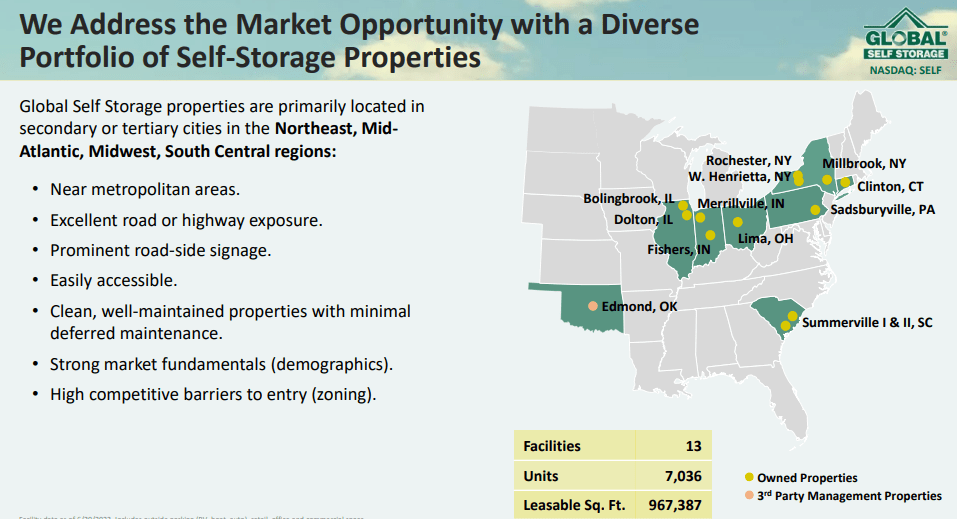

SELF owns and / or manages 13 self-storage properties located in Illinois, New York, Connecticut, Indiana, Ohio, South Carolina, Pennsylvania, and Oklahoma.

SELF’s portfolio consists of 13 self-storage properties that total 967,387 leasable square feet and contain 7,036 storage units. SELF offers multiple types of storage units including personal storage, business storage, climate-controlled storage, wine storage, and auto, boat and recreational vehicle (“RV”) storage.

SELF has a good mix of property types with 59% of their portfolio consisting of traditional drive-up storage, 33% consisting of climate-controlled storage, and 8% consisting of outdoor storage for cars, boats, and RVs.

SELF targets properties in secondary and tertiary cities primarily in the Mid-West, Northeast, and Mid-Atlantic regions of the country.

They strategically target these markets because they believe there's favorable supply / demand dynamics, where there's less self-storage space available per capita when compared to larger primary markets.

As of their most recent update, SELF’s same-store properties were 91.9% occupied and had an average duration of tenant stay of approximately 3.3 years.

{kind=link}

Tenant leases at SELF’s properties are “month-to-month” leases which can be set monthly, semi-annually, annually, or at any time on a case-by-case basis.

Out of all the property sectors, self-storage typically has the shortest lease duration, which is an advantage in today’s inflationary environment as SELF can re-price its rental rates to keep up with inflation much quicker than other property types with long-term leases.

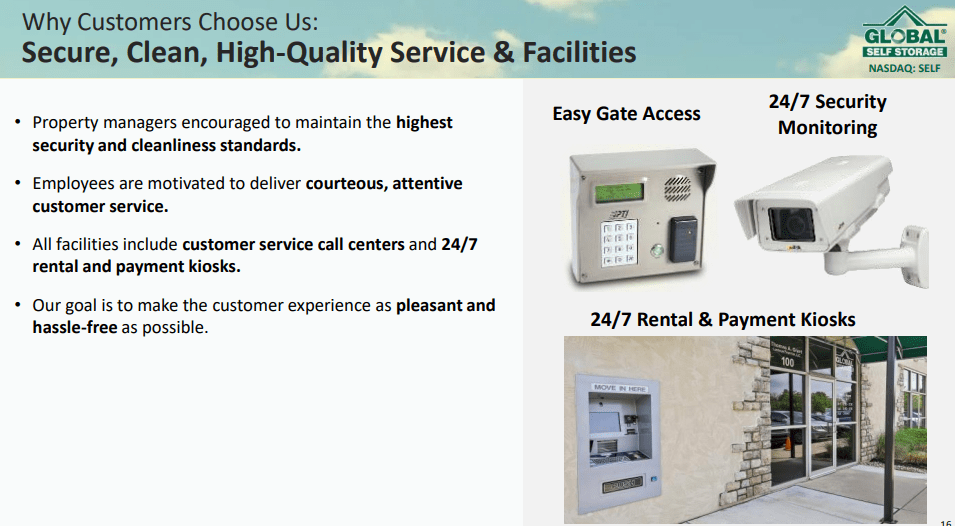

In each of their self-storage properties SELF has a payment and rental kiosk available at all times. Using these kiosks, prospective tenants can rent out a storage unit and current tenants can pay their monthly bill.

Their properties also offer on-site security with gate access codes and around the clock security monitoring. Additionally, all of SELF’s stores have on-site property managers to assist with daily needs and a customer call center to handle inquiries when their store managers are not available.

{kind=link}

Out of all the small cap REITs we’ve looked at, Global Self Storage is by far the smallest with a market capitalization of approximately $50.0 million.

While the company is small, they have a solid balance sheet with $67.3 million in total assets and $17.2 million in total debt for a debt to asset ratio of approximately 25%.

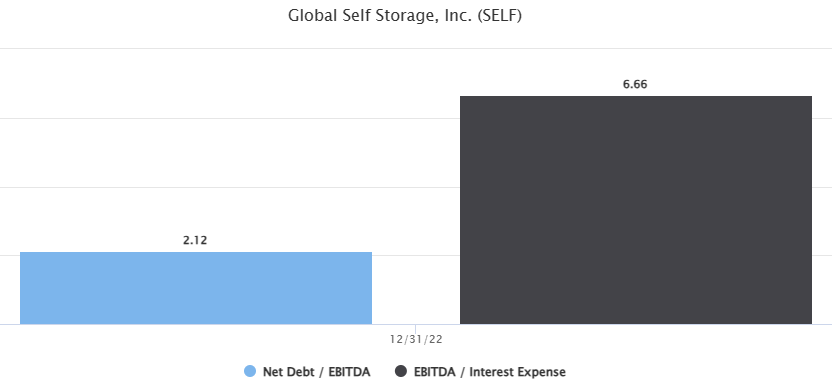

Similarly, their long-term debt to capital ratio is 25.81%, their net debt to EBITDA ratio is 2.12x, and their EBITDA to interest expense ratio is 6.66x as of the end of 2022.

{kind=link}

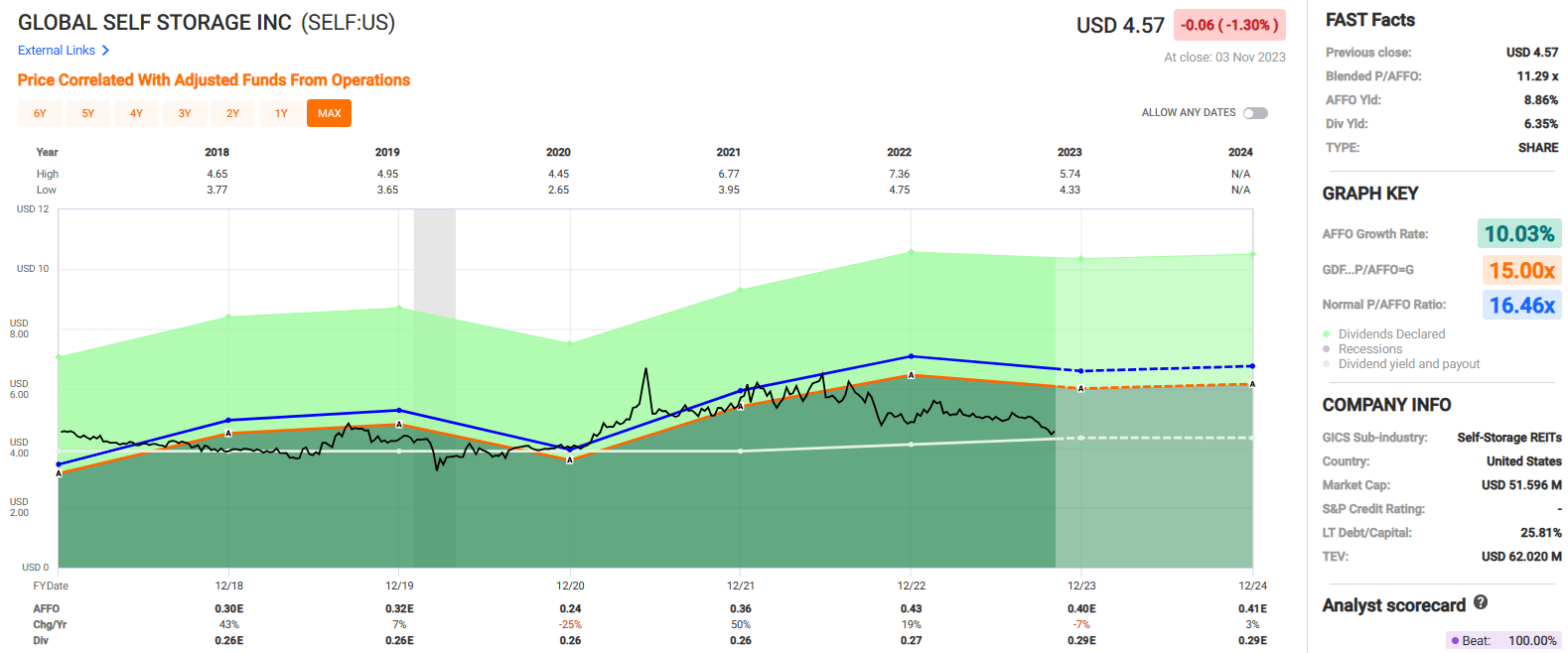

Global Self Storage has delivered a blended average AFFO growth rate of 10.03% and an average dividend growth rate of 1.15% over the last five years. SELF paid a quarterly dividend of $0.065 per share from 2018 through the first half of 2022 and then raised to $0.072 in the third quarter of 2022.

One year later, Global Self Storage declared a 2023 third quarter dividend of $0.0725, which represents an 11.5% increase when compared to the dividend paid during the first half of 2022.

Currently SELF pays a 6.35% dividend yield that's well covered with a 2022 year-end AFFO payout ratio of 63.95% and a 2023 expected AFFO payout ratio of 72.5%. The stock is trading at a P/AFFO of 11.29x, which is a significant discount to their normal AFFO multiple of 16.46x.

We rate Global Self Storage a Spec Buy.

{kind=link}

Screening for Small Cap Gems

From 2016 to 2020 our Small Cap REIT portfolio delivered annual returns of 35%. We closed the portfolio down in early 2020 (due to COVID-19), however, we recently decided to relaunch the small cap strategy given the potential for similar outsized return prospects.

iREIT®

As seen below, we created a new Small Cap Portfolio and we will continue to add new shares monthly, as we attempt to deliver comparable returns as our pre-COVID small cap portfolio did.

iREIT®

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Mining For Small Cap REIT Gems