IPSEF - Mirum Pharmaceuticals: In The Spotlight Following Buyout Of Albireo Pharma

Summary

- Albireo, Mirum Pharmaceuticals, Inc.'s only competitor in a billion-dollar market, is being acquired by Ipsen for up to $1.2 billion.

- The biggest value driver of Mirum is Livmarli, currently the only approved life-saving product in a rare pediatric disease market worth $500 million in the U.S. alone.

- Livmarli's sales launch was extremely convincing, generating over $74 million in its first year on the market.

- Further growth potential can be realized in the coming months driven by a global rollout of Livmarli, the indication expansion in PFIC and three important data readouts in late-stage studies.

The new year is off to a rocket start with some exciting news: French pharmaceutical company Ipsen ( IPSEY ) is offering to acquire all outstanding shares of Albireo Pharma ( ALBO ) for a total of $950 million, or $42 per share . An additional $240 million may be due via a contingent value right associated with the approval of Bylvay in Biliary Atresia ((BA)) in the United States. The transaction values and represents the long-term potential of Albireo's lead product, Bylvay. For interested readers: I plan to write a separate Albireo related article on this transaction in the coming days to wrap up my coverage.

This transaction immediately puts Mirum Pharmaceuticals, Inc. ( MIRM ) and its lead candidate Livmarli in the spotlight. Mirum and Albireo are remarkably similar. Both companies have similar pipelines at similar stages of development targeting the identical indications.

I have been following both companies for about two years and have pointed out the undervaluation and long-term potential of both companies. The high premium in the transaction of 104% clearly validates that the market ignored the potential until the very end. However, the market capitalization of Mirum has tripled since my first article and has converged to the validated buyout value of Albireo. This raises the question of Mirum's fair value and its future potential.

In this article, I will not only evaluate the current situation and discuss the developments since my last article , but also propose a possible scenario for Mirum by 2024. For interested readers, I recommend reading not only my older articles on Mirum , but also my articles on Albireo . Many of the articles apply to both companies, for instance the article that gives an overview in adult liver disease .

Business of Mirum Pharmaceuticals

Mirum is a Latin word that means extraordinary, amazing or remarkable. We chose Mirum as our company name because it speaks to the impact we hope we can make for patients and their families. - Homepage

Logo of Mirum Pharmaceuticals (Company Homepage)

{kind=link}

Mirum is a commercially profitable company with a pipeline focused on rare diseases of the liver. The company's value driver is Livmarli, currently the only approved product in Alagille Syndrome, a greater than $500 million U.S. market opportunity. Following approval in Europe , international sales are also expected to gain momentum in the coming months.

However, the team is not only active delivering on the commercial side, but also actively seeks to realize the long-term value of its pipeline . Following positive study results , the company plans to file an sNDA for Livmarli in PFIC in the coming weeks, and is also evaluating Livmarli in a Phase 2b study in BA with top line results expected in the second half of 2023.

In addition to Livmarli, Mirum has another product candidate in the pipeline, Volixibat, to address the severe itching and progressive liver damage associated with cholestatic liver disease in adults. Volixibat has two pivotal data releases coming up in the second half of the year.

Commercial-Stage with Pipeline of Growth Opportunities (Company Presentation)

Recent Developments & Corporate Situation

Since my last article in mid-2022 , Mirum Pharmaceuticals, Inc. has been able to deliver mostly encouraging news. I will first discuss the current financial foundation and then highlight the developments in the pipeline.

Following the capital raise and cash runway extension, Mirum is in an excellent financial position. With low debt, more than $250 million in cash on hand , and growing revenues from global Livmarli sales, Mirum is positioned to advance both international Livmarli sales and the development of its clinical pipeline, and no further dilution is expected.

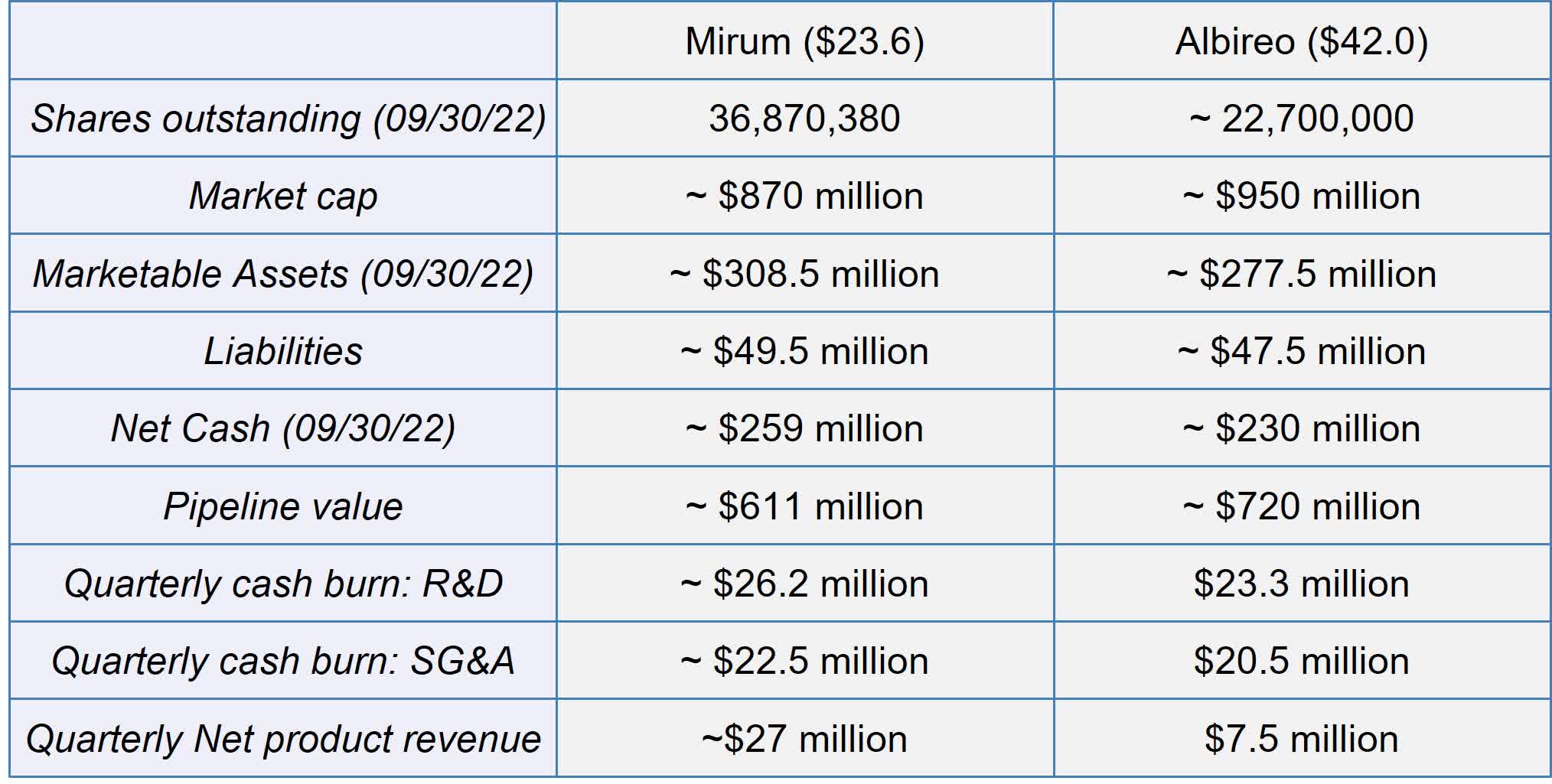

In summary, Mirum Pharmaceuticals, Inc. is well-positioned for the coming months and catalysts. Currently, Mirum has a slightly lower market capitalization than peer Albireo, at around $870 million. The value of Albireo was validated by the buyout of Ipsen. The pipeline itself is valued at about $610 million.

Financial overview of Mirum and peer comparison (Source: Author's Chart with company filings)

{kind=link}

Among the great financial strength, Mirum Pharmaceuticals, Inc. is backed by institutional funds (around 90% of all shares are held by institutional funds).

Backed by financial strength, Mirum continues to drive Livmarli sales. By now, sales are cash-flow positive and contributing to the topline. The fourth quarter of 2022 generated approximately $27 million in sales , ending the fiscal year with product net revenue of $74 million - with further significant room for growth in the U.S. in 2023 and beyond.

In summary, the launch has been very successful, however Mirum is well positioned for a further 50% year-over-year growth in the U.S. in the next fiscal year. Despite the strong market launch, Mirum is still far from having fully penetrated the $500 million market in the U.S. and estimates a current market penetration of just 20% . The low market penetration has two reasons: firstly, patients are reached in waves. Secondly, many patients with the chronic disease visit their doctor only every 6-12 months.

International sales of $5 million contributed to the $27 million in sales in the fourth quarter. In addition to the approval in patients with ALGS two months and older in Europe , Livmarli was approved in Israel . Sales in Germany are expected to start in the coming weeks, as soon as the price has been determined. Additional countries in Western Europe will be approached in clusters throughout the year. In addition, the prospects for market launch are even better than in the U.S. Although the reimbursement pathway in Europe is somewhat limiting, Mirum already has a higher market penetration based on rollover patients from its clinical trials.

The importance of international markets becomes very clear when you look at Albireo's numbers. The international share of quarterly sales there, which consisted mainly of Germany, was almost 40%. In the long term, Albireo expected 40% of all sales from international markets .

In addition to the global launch, the indication expansion of Livmarli in PFIC will play an important role in further strengthening sales towards the end of the year. The study results comprise one of the broadest and most comprehensive data sets with PFIC patients, which is why I expect approval across all PFIC subtypes, similar to Albireo. Albireo has the first-mover advantage in PFIC, but first-year sales in the market have fallen short of expectations, so there's still a lot of potential for Mirum. In addition to the potential in patients with a partial or no response to Bylvay, Mirum has 100 rollover patients from their study, 25 of whom are located in the US . Due to weight-based dosing, Mirum also anticipates that the average price in PFIC will be higher than for ALGS patients .

The acquisition of Albireo by Ipsen should shake up the distribution of power to some extent in the market. Nevertheless, Livmarli and Bylvay will not compete until their expected approvals in the third quarter 2023. In the meantime, the challenge is to penetrate the market as deeply as possible, because the entry barriers for competitors are very high.

Based on the available information, I want to provide a personal revenue forecast for Livmarli and anticipate roughly $130 million in sales in 2023. In the first quarter, I expect a decline in sales due to the build-up of inventory in international markets in the fourth quarter. Nevertheless, I expect steadily increasing patient numbers and sales in the U.S., the ramp-up of international sales in the second quarter and the launch of Livmarli in PFIC in the U.S. in the fourth quarter.

Author's sales forecast for Livmarli (Source: Author's Chart)

{kind=link}

Peer Comparison with Albireo

Due to the high overlap of Mirum to Albireo, I want to do a peer comparison considering the validation done by Ipsen. Ipsen considered Albireo and Bylvay to have advantages over Mirum and Livmarli, particularly in terms of dosing and the progress in its phase 3 study in BA, as BA accounts for 50% of the peak sales revenue. On the other hand, Ipsen has not observed any significant differences in the clinical profile in terms of efficacy and safety.

In addition to the initial 950 million, the deal may be worth nearly 1.2 billion considering the CVR and Bylvay's approval in BA. Nevertheless, I believe that this deal does not reflect the full potential of Albireo, regardless of the fact that the offer represents a premium of almost 100% over the current market price. This claim is also supported by the following question regarding red flags:

Why you are able to get something with peak sales potential of around $800 million for something in the region of $1 billion. Normally, you seem to pay a much higher multiple of potential peak sales. Source: Jo Walton, pharma analyst from Credit Suisse .

Of course, the entire biotech sector was hit hard last year and is at a very low level, but the challenging sales launch and the guidance adjustment last year also contributed to the low multiple. I think I summed it up in my last article on Albireo accurately: "The Commercialization Of Bylvay Is The Key To A Fair Valuation."

This is a major advantage of Mirum Pharmaceuticals, Inc., justifying its higher market capitalization compared to Albireo in the last months. Not only does Mirum address the larger indication, but the sales launch was also compelling, even if it was somewhat slower than originally anticipated.

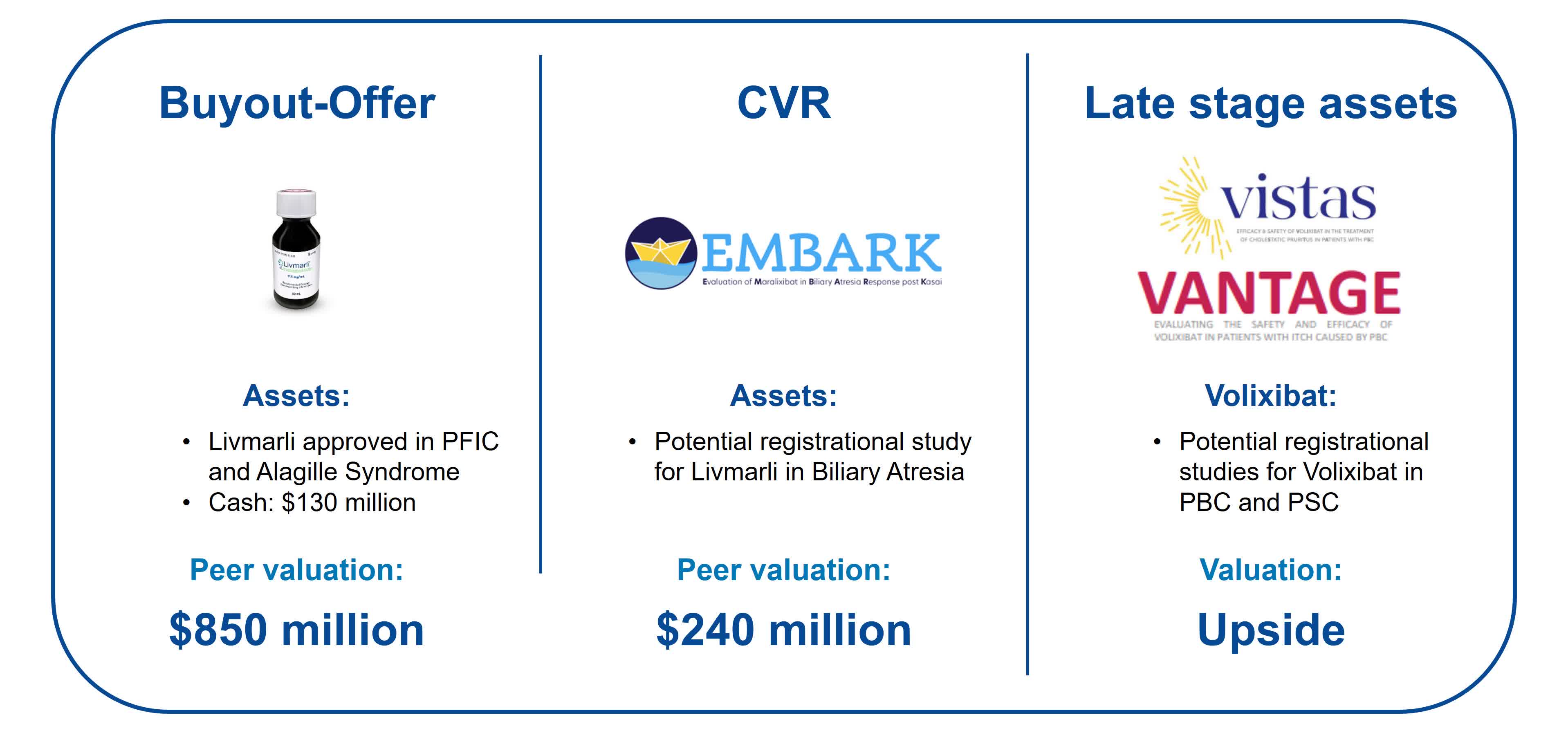

In the following, I would like to highlight the potential for Mirum Pharmaceuticals, Inc. from the Albireo-Ipsen transaction based on three individual pillars. The valuation is based on Mirum as a company at the end of 2023.

The peer comparison proves that Mirum is attractively valued at current prices (Source: Author's Chart)

{kind=link}

The first pillar represents the core focus of the transaction. Mirum as a company, with the remaining cash on hand and Livmarli, approved in PFIC and ALGS. This pillar is currently valued at $950 million in the transaction.

Since Mirum has only $130 million in net-cash at the end of 2023 according to my calculation, I have corrected the difference in cash in the valuation. However, Mirum is already a commercially profitable company and should be able to generate annualized sales of around $160 million at the end of 2023, which would in fact justify higher multiples.

The second pillar comprises the CVR, which will be payable upon the approval of Bylvay in BA. This element of the deal is valued at just under a further 240 million. In the EMBARK study, Mirum is investigating the efficacy of Livmarli in BA. Given the same mechanism of action, I believe it is very likely that if Bylvay is successful, Livmarli will also be approved.

It is expected that results of the study will be available in the middle of the year. Although the EMBARK trial is only a phase 2b study, Mirum is confident regarding the approval opportunity with positive study results , for example under the FDA's Accelerated Approval Program .

The primary goal of the study is to generate meaningful data and to better understand the impact of Livmarli in patients with BA. Despite the short time frame of only 6 months, there is a good probability of success. Mirum refers to the MARCH-PFIC study in this context: although PFIC is less aggressive and severe than BA, significant positive results were observed within 6 months.

Mirum hopes to redefine the regulatory pathway based on meaningful data from the EMBARK study. To date, the FDA requires a delay in liver transplantation, as reflected in Albireo's BOLD study . However, in practice, monitoring the serum bilirubin level has been established in patients, and physicians use it to evaluate the next steps. By the end of the year, investors may not only have clarity on the likelihood of Livmarli's success in BA, but also an agreement with the FDA on the regulatory pathway to approval.

When we have those results, we'll go back to the agency and talk about the registration plans. Source: Chris Peetz, Q3 Business Update

Compared to Albireo's early pipeline candidates A3907 and A2342, Volixibat is in the regulatory part of the their studies in late 2023 following positive interim results. Although the final results of the studies are not expected until late 2025 , the interim results mark an important milestone in unlocking the full value potential.

As A3907 and A2342 are products in early clinical development, only a low value was attributed to them in the transaction. For this reason, Volixibat represents Mirum's full potential beyond Livmarli.

In summary, Livmarli should be assigned at least the same value as Bylvay based on the compelling sales launch in the larger market opportunity. With positive study results in the EMBARK trial, Mirum's market capitalization should exceed $1 billion, representing a further 20% upside from current prices. This does not yet include Volixibat, whose value can be verified with the help of Ipsen's deal with Genfit ( GNFT ).

Agreement gives Ipsen global rights to develop and commercialize GENFIT’s late-stage asset elafibranor in Primary Biliary Cholangitis. GENFIT receives €120m upfront and is eligible to receive up to €360m in milestone payments as well as tiered double-digit royalties of up to 20%. Source: Press release

Summary

Mirum Pharmaceuticals, Inc. as a company has successfully overcome the challenges of the past months. While this is reflected in the market capitalization, it is not reflected in the share price. Since my first article about Mirum , the Mirum Pharmaceuticals, Inc. market capitalization of about $260 million has almost tripled, while the share price has only increased by 30%. Now that the financing is secured thanks to the company's financial strength and growing product revenue, the future increase in value should be reflected in the share price proportionately.

While Ipsen's deal does in my opinion not reflect the full value and potential of Albireo, it validates Mirum as a company. The peer comparison manifests the valuation, yet Mirum holds all the keys to unlock the full potential. In addition to the global rollout of Livmarli and the indication expansion into PFIC, the market potential in BA, and the progress in the clinical development pipeline, Mirum Pharmaceuticals, Inc. also mentioned the possibility of external growth into other rare diseases.

In addition to the Albireo acquisition, the many milestones in the coming months should keep interest in the stock high. If Mirum Pharmaceuticals, Inc. continues to perform strong operationally, it is likely to be reflected in a higher share price and valuation relative to Albireo.

For further details see:

Mirum Pharmaceuticals: In The Spotlight Following Buyout Of Albireo Pharma