MG - Mistras Group: Good Q4 2022 Results But Upside Potential Exhausted (Rating Downgrade)

2023-04-11 03:41:16 ET

Summary

- Mistras Group finished 2022 on a strong note as the gross profit margin surpassed 30% in Q4.

- The 2023 guidance looks strong as the expected EBITDA of $70-75 million is close to the $80 million I forecast back in January.

- However, the market valuation of Mistras Group has soared by over 40% since then and the company is trading at an EV/EBITDA ratio of 5.2-5.6x based on the 2023 guidance.

- I wouldn’t be comfortable keeping a position here at above 5x EV/EBITDA and I think that risk-averse investors should avoid this stock.

Introduction

In January, I wrote a bullish article on SA about U.S. advanced asset protection solutions provider Mistras Group (MG) in which I said that annual EBITDA could be back above $80 million over the coming quarters as the company passes on cost increases to its clients.

Well, I think that the Q4 financial results were decent and that the 2023 guidance looks good. That being said, the market valuation has increased by over 40% since my previous article and I think that Mistras Group is starting to look expensive. Let's review.

Overview of the Q4 2022 financial results

In case you haven't read my first article about Mistras Group, here's a short description of the business. The company is involved in the provision of integrated technology-enabled asset protection solutions such as testing, inspection and mechanical services across several industries. The oil and gas sector typically accounts for over half of revenues and Mistras Group deploys technicians at the locations of clients as non-destructive testing ((NDT)) and mechanical services are performed on-site. The company offers oil and gas asset protection solutions to downstream, midstream and upstream operations and it helps its clients identify current and future asset performance as well as actively prevent, mitigate or otherwise address potential issues such as corrosion, cracking, and leaking.

Mistras Group

The majority of revenues from aerospace and defense clients and certain manufacturing customers, in turn, are generated by performing inspections and testing at in-house laboratories. Mistras Group also has an asset protection software platform called OneSuite which offers functions of its software and services brands as integrated apps on a cloud environment. It currently features over 90 integrated applications.

{kind=link}

Mistras Group views energy-related infrastructure and commercial aerospace as its largest market opportunities and it operates in a highly competitive, but fragmented market. The USA and Canada account for the vast majority of revenues. As of December 2022, Mistras Group had around 5,400 employees, of which about 3,600 were located in the USA, and 600 in Canada.

According to a recent report by Think Market Intelligence , the global non-destructive testing and inspection market is expected to reach $19.4 billion by 2030, achieving a compound annual growth rate [CAGR] of 7.62%. The Americas non-destructive testing and inspection market, in turn, is forecast to have a CAGR of 7.64% during the same period and reach $3.71 billion by 2030.

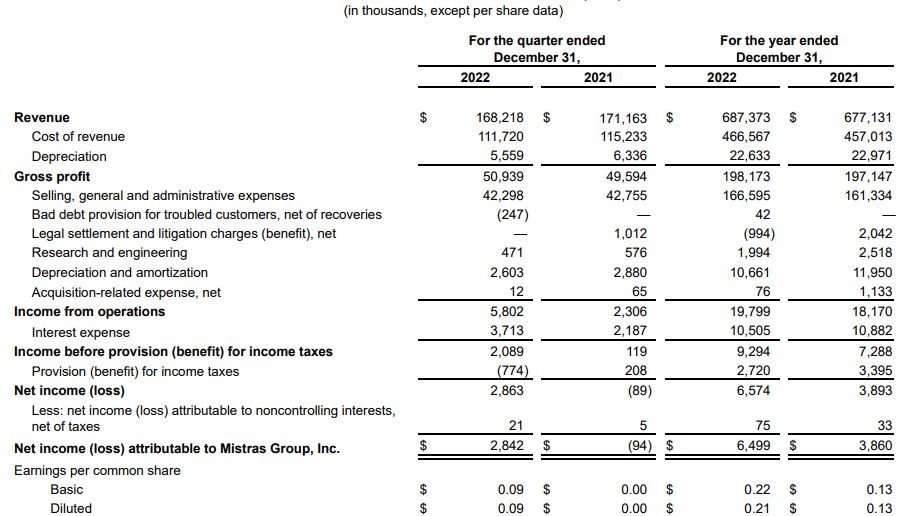

Turning our attention to the Q4 2022 financial results, I was expecting margins to expand significantly as Mistras Group passes on cost inflation to its customers, and the company delivered. Revenues were near the mid point of the recent guidance at $168.2 million while the gross profit margin came in at 30.3%, which represents a 130 basis points improvement compared to a year earlier. The adjusted EBITDA margin, in turn, improved to 9.34% from 8.5% in Q4 2021.

{kind=link}

You see, Mistras Group typically enters into master service agreements that specify an overall framework and contract terms which means that most of its revenues are short term in nature and are thus vulnerable to high inflation. In January, my investment thesis relied on the company having enough pricing power to pass on the cost inflation to its customers which should boost profitability as soon as inflation rates start moderating. During 2022, Mistras Group managed to negotiate price increases with many of its clients, particularly in the oil and gas market. In addition, the company said during its Q4 2022 earnings call that it expects some benefit to both recurring revenue and gross margin for 2023.

Looking at the guidance for this year (page 2 here ), the company forecasts to generate revenues of between $710 and $740 million and adjusted EBITDA between $70 and $75 million based on current market conditions. Considering oil prices have been stable over the past several months, I was expecting higher revenues for 2023, maybe in the region of $800 million. Yet, the EBITDA margin improvement looks compelling, and Mistras Group is thus in striking distance of the $80 million I anticipated back in January.

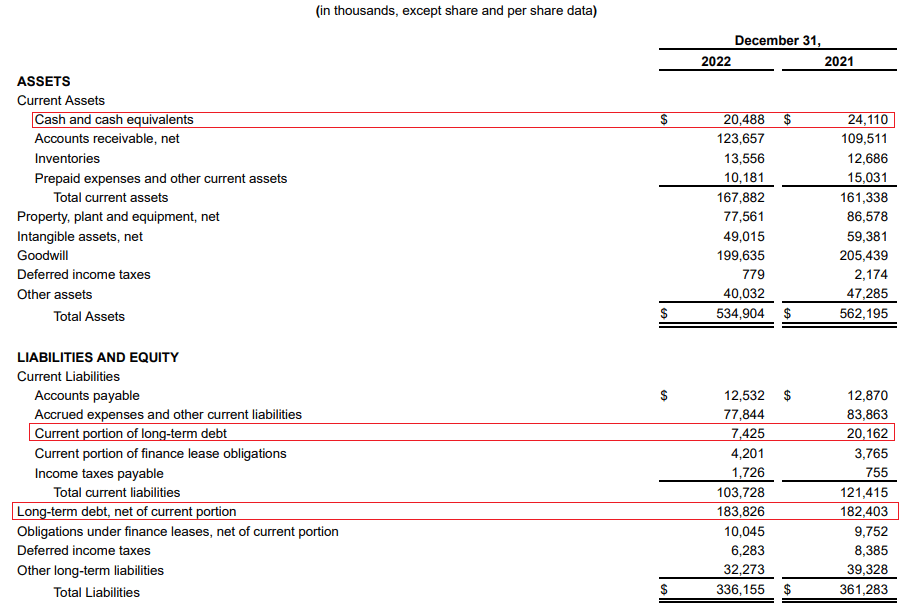

Turning our attention to the balance sheet, the situation looks much better compared to September as net debt declined to $170.8 million from $183.1 million. The leverage ratio is now 3.5x EBITDA, which is the lowest level since the $143 million purchase of Onstream in December 2018. The gross debt of Mistras Group has declined by almost $100 million since the end of 2018. Unless the company makes a major acquisition soon, I expect the net debt and the leverage ratio to improve significantly in 2023 considering the company forecasts free cash flow of between $30 and $33 million during this year.

{kind=link}

Overall, I think that the Q4 2022 financial results were solid and that the balance sheet looks strong. That being said, there doesn't seem to be much upside potential left here as the market valuation of Mistras Group has increased to $222.1 million as of the time of writing. At the moment, the company has an enterprise value of $392.9 million and is trading at an EV/EBITDA ratio of 5.2-5.6x based on the 2023 guidance. There don't seem to be any major potential catalysts for the share price and the company is still heavily reliant on the oil and gas industry which means that the margins are likely to take a hit in a recession. I wouldn't be comfortable keeping a position here above 5x EV/EBITDA.

Investor takeaway

The end of COVID-19 lockdowns and high oil prices helped Mistras Group book its highest EBITDA in a long time in 2022. The company has successfully managed to pass higher costs to customers, and I think that its 2023 revenue and EBITDA guidance seems easily achievable unless the U.S. economy enters a major recession in the coming months. That being said, the market capitalization of the company has soared by over 40% since late January and I think it's currently at a level at which risk-averse investors should avoid this stock.

For further details see:

Mistras Group: Good Q4 2022 Results But Upside Potential Exhausted (Rating Downgrade)