MG - Mistras Group Is On The Road To Recovery

Summary

- The company’s revenues were significantly affected by COVID-19 lockdowns, but they have been growing for 9 quarters now.

- I think annual EBITDA could be back above $80 million over the coming quarters as Mistras Group passes on cost increases to its clients.

- The company recently entered into a new credit facility which boosted its borrowing capacity by $100 million and I expect this to fund organic and non-organic growth.

Introduction

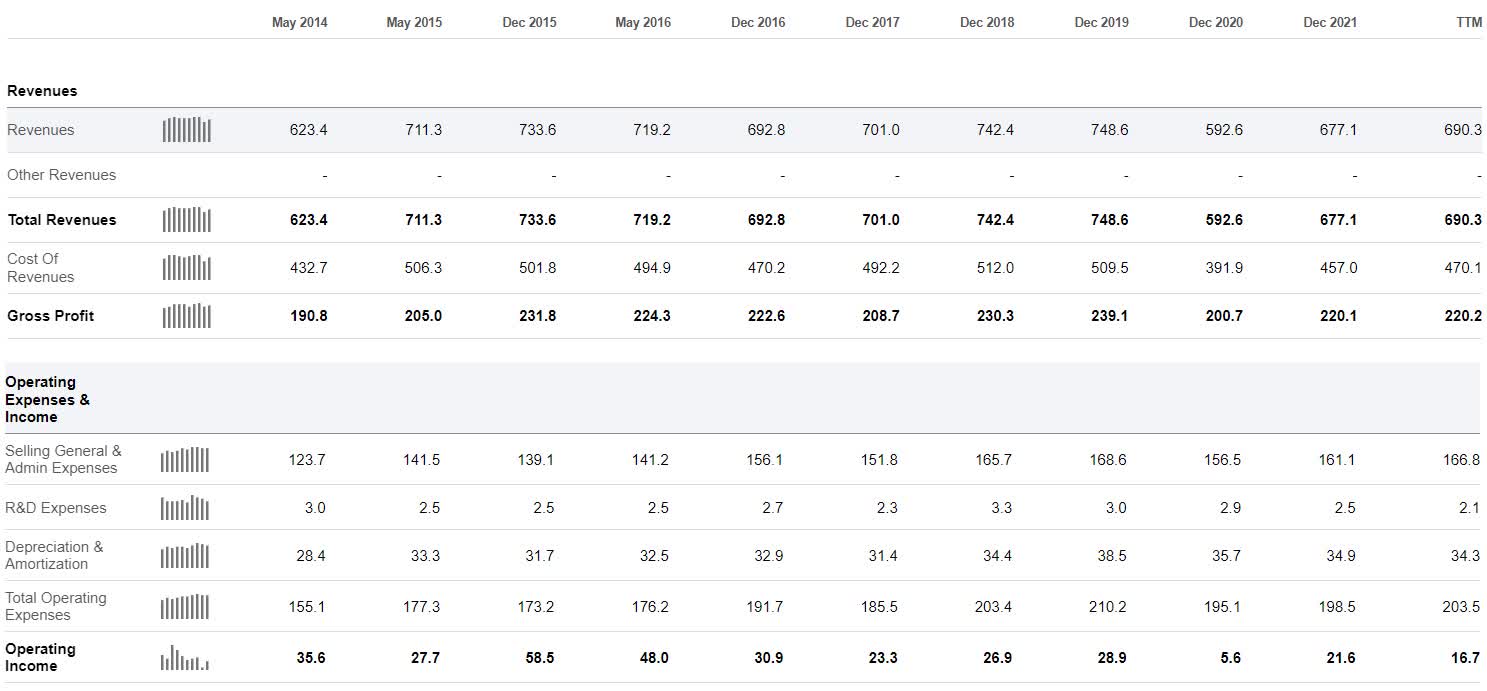

I like to write about companies that lack coverage on SA and today I'm taking a look at Mistras Group ( MG ). It's an advanced asset protection solutions provider which has been through a couple of challenging years, but revenues are growing, and the company should be able to pass on costs increases to customers eventually. The company also recently refinanced its debt. The TTM EBITDA stands at $39.1 million, which I think is a decent achievement in this challenging macroeconomic environment. Let's review.

Overview of the business and financials

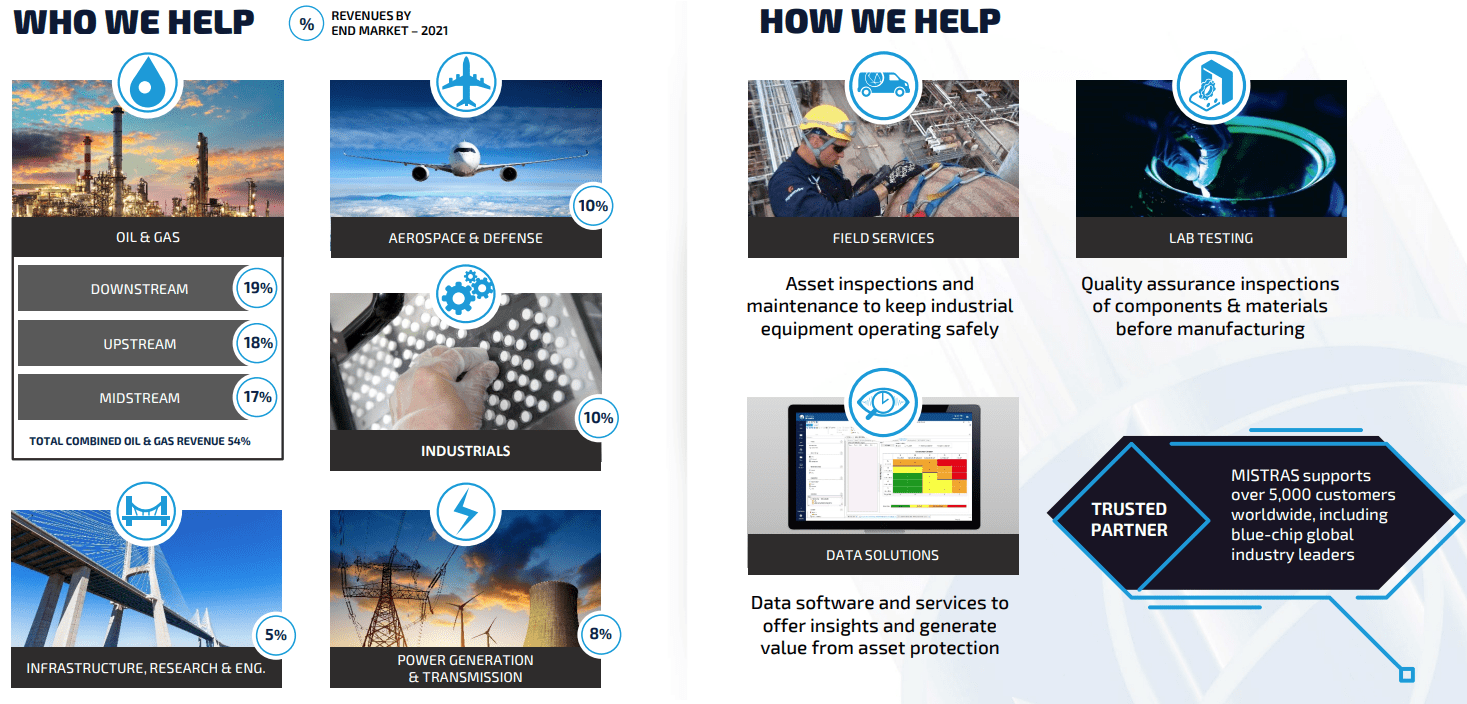

Mistras Group was founded in 1978 and operates in the nondestructive testing (NDT) field, offering a range of testing, inspection and mechanical services across the oil and gas, aerospace, industrial, and public infrastructure industries. The majority of revenues in the oil and gas sectors are generated by deploying technicians at the locations of clients where NDT and mechanical services are performed on-site. In the aerospace industry, in turn, the majority of revenues are generated at various in-house laboratories specializing in chemical cleaning, coating application, painting, and pressure testing solutions. Mistras Group has also developed an asset protection software ecosystem named OneSuite that aims to streamline the management and accessibility of asset integrity data. In addition, the company has a wind blade monitoring tool named Sensoria which can detect damage in real-time and alert operators to blade defects. Mistras Group has a total of 120 locations worldwide and employs about 5,400 people. The majority of the company's revenues come from the USA and Canada.

{kind=link}

According to MarketsandMarkets Research , the global NDT and inspection market is expected to reach $18.5 billion by 2028, achieving a compound annual growth rate ((CAGR)) of 10.1%. Overall, it's a large and highly competitive market, but it's highly fragmented.

{kind=link}

Mistras Group is among the major players in the NDT sector and was generating annual revenues of over $700 million and EBITDA of more than $80 million less than a decade ago. However, revenues decreased in 2017 due to challenges at the company's subsidiary in Germany while profits shrank significantly due to poor margins on a large contract and lower utilization of technical labor in the UK. In December 2018, Mistras Group bought a competitor named Onstream for $143 million but just as revenues and margins were recovering, the business was put under pressure by COVID-19 lockdowns and now the company is operating in a challenging environment due to cost inflation. The majority of revenues are short-term in nature as Mistras Group enters into master service agreements that specify an overall framework and contract terms. This means that revenues and margins are usually significantly affected by changes in the macroeconomic environment.

{kind=link}

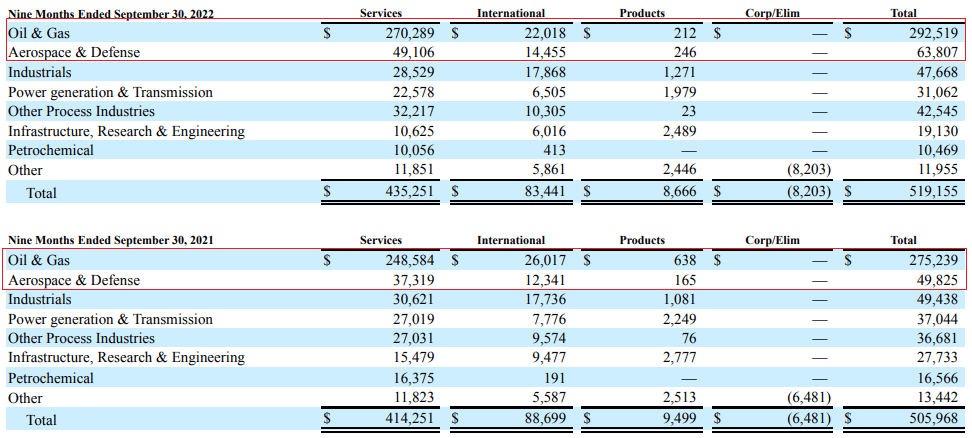

Looking at the financial for the first nine months of 2022, there are a few silver linings. Revenues rose for the 9th consecutive quarter thanks to strong results in the upstream sector due to high production in the USA as well as the aerospace and defense segment due to a recovery in commercial aerospace, growth in private space, and expansion into adjacent services.

{kind=link}

Mistras Group's EBITDA for the first 9 months of the year declined by 11.6% to $22 million due to inflationary pressure on costs but I expect growth to resume in the near future as the company said during its Q3 2022 earnings call that it's implementing price increases. Also, there's a lag between the time Mistras Group boosts its labor rate and the recovery time for the higher billing rate. In addition, the company has a long-term goal of lowering SG&A expenses to about 20% of revenues which translates into a reduction of expenses by $5.9 million per quarter based on the Q3 2022 financial results.

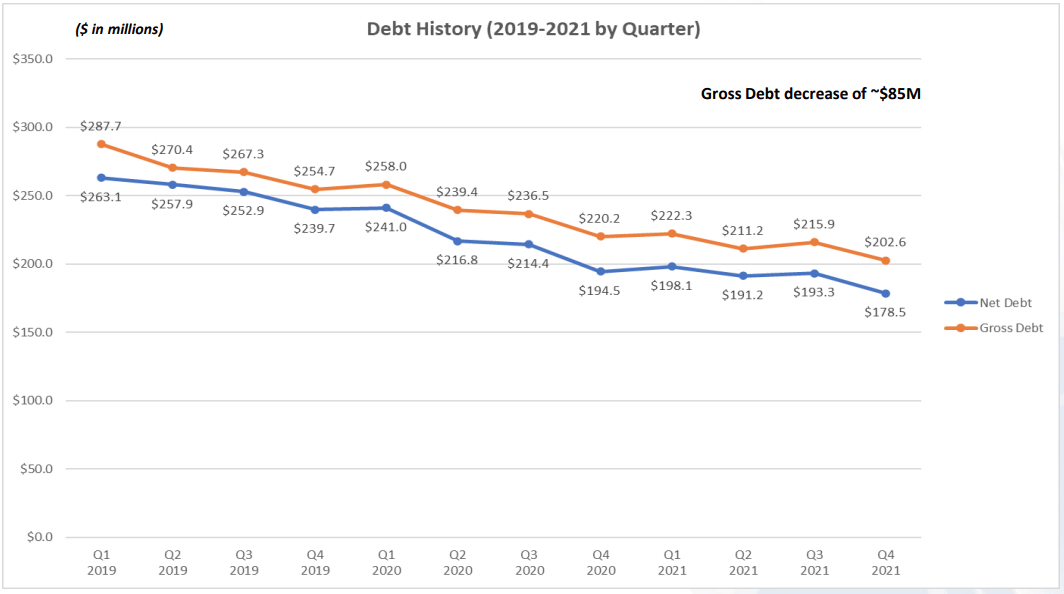

Turning our attention to the balance sheet, net debt increased from $178.5 million to $183.1 million during the first nine months of 2022 but is still about $80 million lower compared to Q1 2019.

{kind=link}

Mistras Group's debt was set to mature in December 2023, but the company announced in August 2022 that it entered into a new credit facility with a syndicate of banks which boosted its borrowing capacity by $100 million to $315 million. The facility matures at the end of July 2027 and will help the company funds growth initiatives in the data (OneSuite) and renewable energy (Sensoria) sectors. In addition, the agreement lowers the effective credit spread by 25 basis points and reduces required quarterly term loan amortization. Considering debt markers have been jumpy lately due to recession fears and rising interest rates, I think that securing a larger credit facility with a maturity in over four years is a significant achievement.

Overall, I think that Mistras Group's revenues are gradually returning to pre-pandemic levels, and I expect them to continue growing in 2023 thanks to higher production levels in the U.S. oil and gas industry, which should boost demand for inspection services. I also expect profitability to improve as the company continues to pass on increased costs to customers while inflation rates decline. In addition, the improved liquidity due to the new credit facility should allow Mistras Group to invest more funds in both organic and non-organic growth.

Looking at the risks for the bull case, I think that there are two major ones. First, another black swan event such as the COVID-19 lockdowns could derail the recovery of Mistras Group. The company is vulnerable to these types of events due to the short-term nature of its contracts. Second, Mistras Group is heavily reliant on the oil and gas industry which means that revenues and margins could decline significantly if oil prices slump.

Investor takeaway

Mistras Group is experiencing strong growth in its primary end markets and has the resources to invest in growth initiatives thanks to a new credit facility. I expect EBITDA to grow significantly over the coming quarters as the company passes on cost increases to its clients and I think they could be back above $80 million in a year or two.

I rate this stock as a speculative buy due to the short-term nature of Mistras Group's contracts.

For further details see:

Mistras Group Is On The Road To Recovery