MG - Mistras Group Is Starting To Look Cheap After Recent Selloff (Rating Upgrade)

2023-09-13 02:36:00 ET

Summary

- Mistras Group booked weak Q2 2023 results with revenues down 1.7% while adjusted EBITDA declined by 16.4% to $15.3 million.

- The second half of the year should be good as the adjusted EBITDA guidance for the full year barely changed.

- The EV has decreased below $330 million over the past few days, and I think MG is starting to look undervalued once again.

- In my view, MG should be trading above 5.5x EV/adjusted EBITDA based on the new guidance, which translates into $7.15 per share.

Introduction

In April, I wrote an article on SA about advanced asset protection solutions firm Mistras Group (MG), in which I said that it had managed to pass higher costs to customers but that it was starting to look expensive as it was trading at an EV/EBITDA ratio of 5.2-5.6x based on its 2023 guidance.

On August 2, the company posted underwhelming financial results for Q2 2023 as revenues fell by 1.7% while adjusted EBITDA slumped by 16.4% to $15.3 million. Yet, Mistras Group is optimistic about its financial performance in the second half of 2023 and with the market capitalization of the company recently decreasing to just above $160 million, I feel comfortable upgrading my rating on the stock to speculative buy. Let's review.

Overview of the Q2 2023 financial results

If you aren't familiar with the company or my earlier coverage, here's a brief description of the business. Mistras Group was established in 1978 and is a major player in the non-destructive testing ((NDT)) market with a global share of about 3% (see slide 14 here ). The company focuses on the oil and gas, aerospace, industrial, and public infrastructure industries and it offers testing, inspection and mechanical solutions. The oil and gas sector usually accounts for more than half of its revenues. The vast majority of revenues in this segment are generated by deploying technicians at the locations of clients where NDT and mechanical services are performed on-site. In contrast, the bulk of revenues in the aerospace and defense segment are generated at various in-house laboratories that are focused on chemical cleaning, coating application, painting as well as pressure testing services. Mistras Group also has a wind blade monitoring tool called Sensoria and an asset protection software ecosystem named OneSuite. Overall, Mistras Group has 120 locations worldwide and employs some 5,400 people. North America accounts for over 80% of the company's revenues.

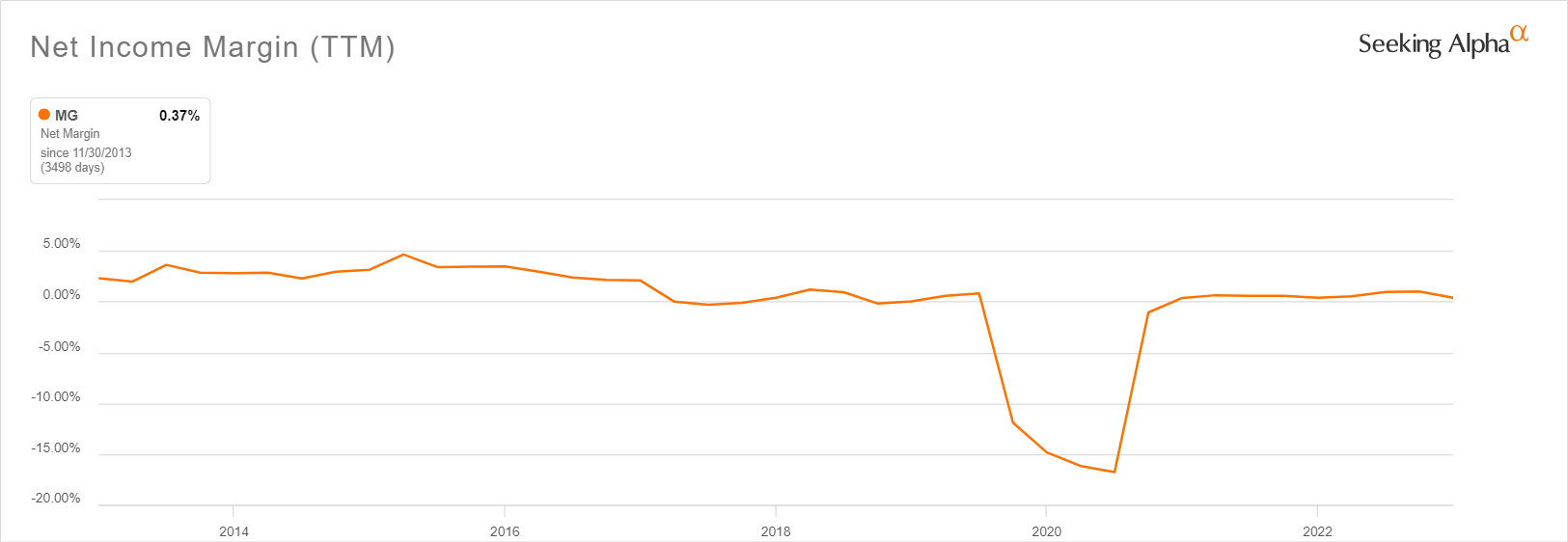

In my view, the key challenge for the business is that most of the revenue is short term in nature as the company enters into master service agreements based on an overall framework and contract terms which leads to margins being significantly affected by cost inflation. In addition, Mistras Group operates in a highly competitive market with thin margins and the net income margin hasn't surpassed the 5% mark over the past decade.

{kind=link}

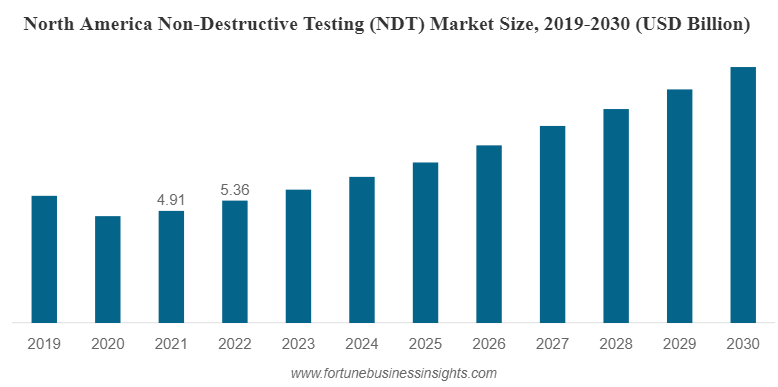

On a positive note, the North American NDT market seems to be poised for rapid growth over the coming years. According to a report from Fortune Business Insights , this market is expected to grow at a compound annual growth rate ((CAGR)) of 11.5% from 2023 to 2030 and reach $33.73 billion. There should ample room for revenue growth over the next several years.

{kind=link}

In addition, I expect the margins of Mistras Group to improve significantly by the end of 2024 thanks to cost-cutting measures. In February, the company announced a change in its leadership and engaged global consulting firm AlixPartners to identify meaningful margin improvement opportunities. Mistras Group refers to this project as Phoenix and the results from the initial phase are encouraging as the company revealed in its Q2 2023 financial report that it expects to realize annualized cost savings of about $6.2 million. Some $5.1 million of those are expected to be made this year. Most of the initial cost-savings are related to overhead functions, mainly in the North American business.

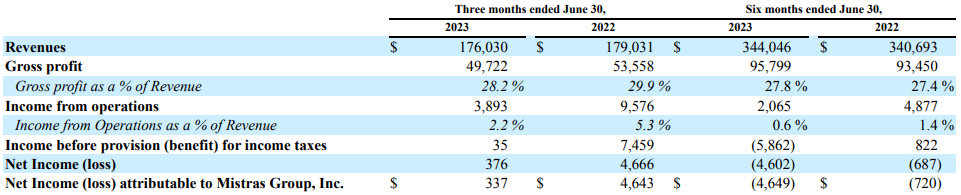

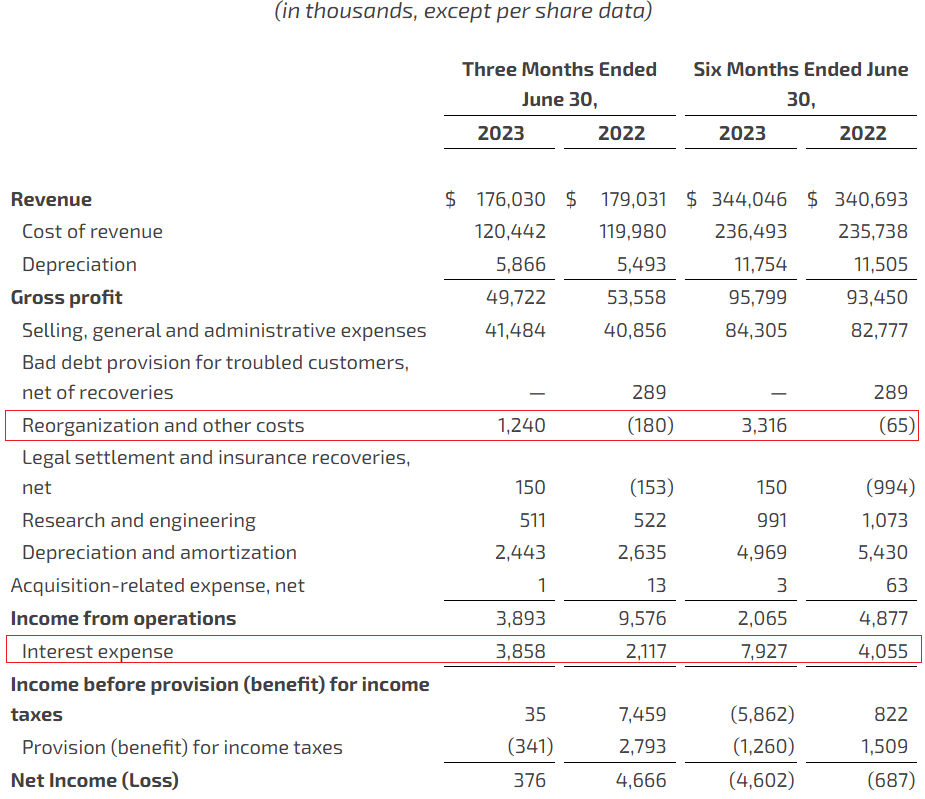

Turning our attention to the Q2 2023 financial results, I think that it was a poor quarter as revenues fell by 1.7% year on year to $176 million and this put pressure on operating margins.

{kind=link}

Looking at the reasons for the lower revenues, there was a decrease in revenues in the aerospace and defense segment due to a delayed defense contract as well as declines in the energy generation industry related to project timing. Also, Mistras Group booked an unfavorable foreign exchange impact of $0.7 million during the quarter. On a positive note, data solutions revenues increased by 11.5% to $18.1 million thanks to strong demand in North America.

Turning our attention to the income statement, operating income was also negatively affected by $1.2 million of reorganization costs due to the cost-saving as well as higher interest expenses due to rising interest rates.

{kind=link}

Following the underwhelming financial results, Mistras Group cut its guidance for 2023 slightly. The company now expects to book revenues of between $700 million and $720 million while adjusted EBITDA is forecast to stand at between $68 million and $71 million. The previous guidance included revenues of between $710 million and $740 million and adjusted EBITDA of between $70 million and $75 million. Overall, I think that such a small decrease in expectations is a positive development as this means that revenue growth should resume in the second part of the year while adjusted EBITDA margins are set to improve compared to the previous guidance. In 2022, the company booked revenues of $687.4 million and adjusted EBITDA of $58.2 million.

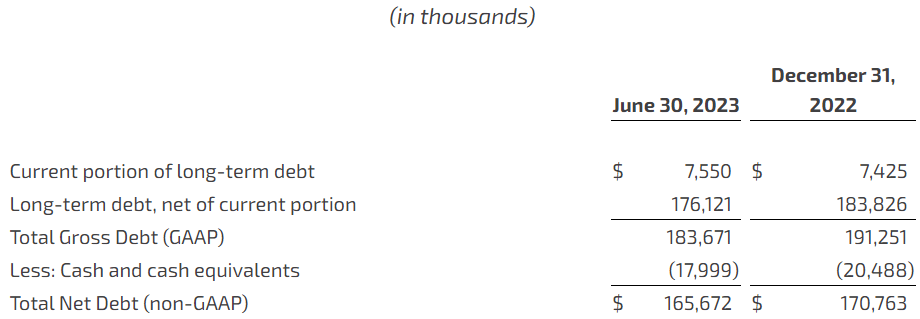

Turning our attention to the balance sheet, I find it encouraging that net debt decreased to $165.7 million in June 2023 from $170.8 million in December 2022. Free cash flow for Q2 2023 was $8 million, bringing the total for the first half of 2023 to $7.7 million.

{kind=link}

Looking at the valuation, the enterprise value stands at $326.9 million as of the time of writing, which is almost 17% lower compared to my April article about the company. Mistas Group is now trading at EV/adjusted EBITDA ratio of 4.7x based on the midpoint of the updated 2023 guidance and I think it should be trading at a ratio of at least 5.5x considering oil and gas prices remain high, which should provide a boost for the business. This translates into $7.15 per share or an upside potential of 34.4%.

Turning our attention to the downside risks, I think there are two major ones. First, the financials of the company could be put under pressure over the coming months if oil and gas prices drop sharply or a black swan event causes costs to rise rapidly. Second, interest expenses have been rising rapidly despite the lower debt load and further rate hikes in the US could offset the effects of the cost-cutting measures, putting the company in the red. Overall, it could be best for risk-averse investors to avoid this stock.

Investor takeaway

Mistras Group struggled from a financial standpoint in Q2 2023, but oil and gas prices remain high and the adjusted EBITDA guidance for the full year barely changed. Cost-cutting measures are progressing well, and I think the company is starting to look cheap based on fundamentals once again. In my view, Mistras Group has a good chance of achieving its updated adjusted EBITDA guidance for 2023. That being said, I'm concerned by the rising interest expenses which is why my rating on the stock is speculative buy.

For further details see:

Mistras Group Is Starting To Look Cheap After Recent Selloff (Rating Upgrade)