MG - Mistras Group: Trading Cheaply With Scope For Upside

2023-12-26 19:13:34 ET

Summary

- Mistras Group's revenue growth has been mild, despite a strong business model and global scale. Management’s execution has been poor, although the cyclical nature of its clientele has also impacted it.

- The industry is broadly attractive, however, with robust demand, a number of tailwinds (incl. clean energy and increased infrastructure spending), and technological innovation if led.

- MG’s margin development has been underwhelming, although has reasonable scope for improvement through cost rationalization and digitalization.

- Despite the negative undertone, the company has deep expertise, scale, and sufficient scope for margin improvement and growth to imply a change in fortunes is possible.

- MG is undervalued despite its weak financial performance, owing to a strong cash yield and a >100% discount to its peers.

Investment thesis

Our current investment thesis is:

- MG has performed poorly but is not dead-and-buried. There is clear scope for an improvement in financial performance, particularly when considering the increase in infrastructure spending expected.

- There is, however, a clear execution risk that is not mitigated. For this reason, valuation is of utmost importance to compensate. We believe this is the case given the >100% discount to its peers and FCF yield of ~13%.

Company description

Mistras Group ( MG ) is a leading global provider of technology-enabled asset protection solutions. The company specializes in delivering inspection, monitoring, and testing services to ensure the integrity and reliability of critical infrastructure in various industries, including oil and gas, power generation, and aerospace.

Share price

MG’s share price performance has been disappointing, persistently declining, contributing to a loss of over 50%. This is a reflection of its underwhelming financial performance at a time when many of the industries it services have grown well.

Financial analysis

{kind=link}

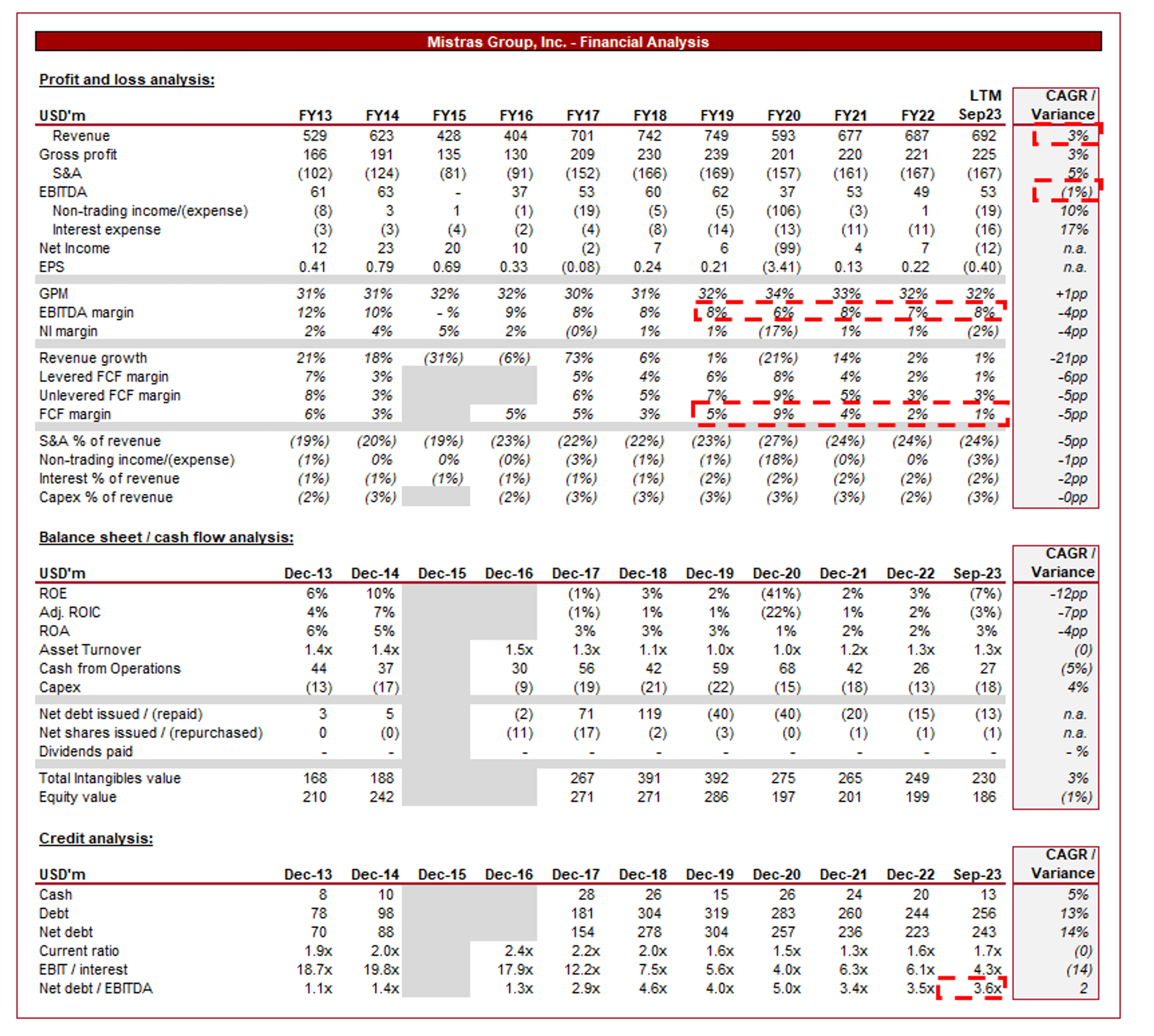

Presented above are MG's financial results.

Revenue & Commercial Factors

MG’s revenue has grown at a mediocre 3% rate during the last decade, while EBITDA has declined (-1%). This is particularly disappointing given Management has supplemented organic growth with M&A.

Business Model

MG specializes in providing NDT services, which involve the examination of materials and components without causing damage. This includes techniques such as ultrasonic testing, radiographic testing, magnetic particle testing, and others. MG supports critical infrastructure businesses, such as those in oil & gas, infrastructure, and aerospace.

The core of MG's business is to help clients ensure the integrity and reliability of their critical assets. Not only is this highly valuable for regulation compliance and monitoring, but it can also support the efficient allocation of capital expenditure over a longer term period.

The company’s competitive advantage stems from:

- Technology: MG employs condition-monitoring technologies to assess the health of assets in real-time. This involves using sensors and data analytics to detect abnormalities and predict potential failures before they occur. Its technology has been built on incremental development over time.

- Value enhancement: Leveraging data from inspections and monitoring across its business and with specific clients, MG offers predictive maintenance solutions. This helps clients optimize maintenance schedules, reduce downtime, and extend the lifespan of their assets. As a specialist in the segment, MG is best placed to offer this.

- Innovation: MG is embracing digitalization by utilizing advanced technologies such as IoT (Internet of Things), AI (Artificial Intelligence), and data analytics. Management is seeking to be proactive, although we note this was initially a delayed response.

- Global Presence: MG operates globally, allowing it to efficiently serve businesses of all sizes.

Although MG has a number of competitive characteristics, we struggle to see the differentiation achieved. The majority of these factors are shared with its peers, while there is a degree of standardization in the results achieved (excluding any breakthrough innovations). This has clearly been a limiting factor for the company’s growth story.

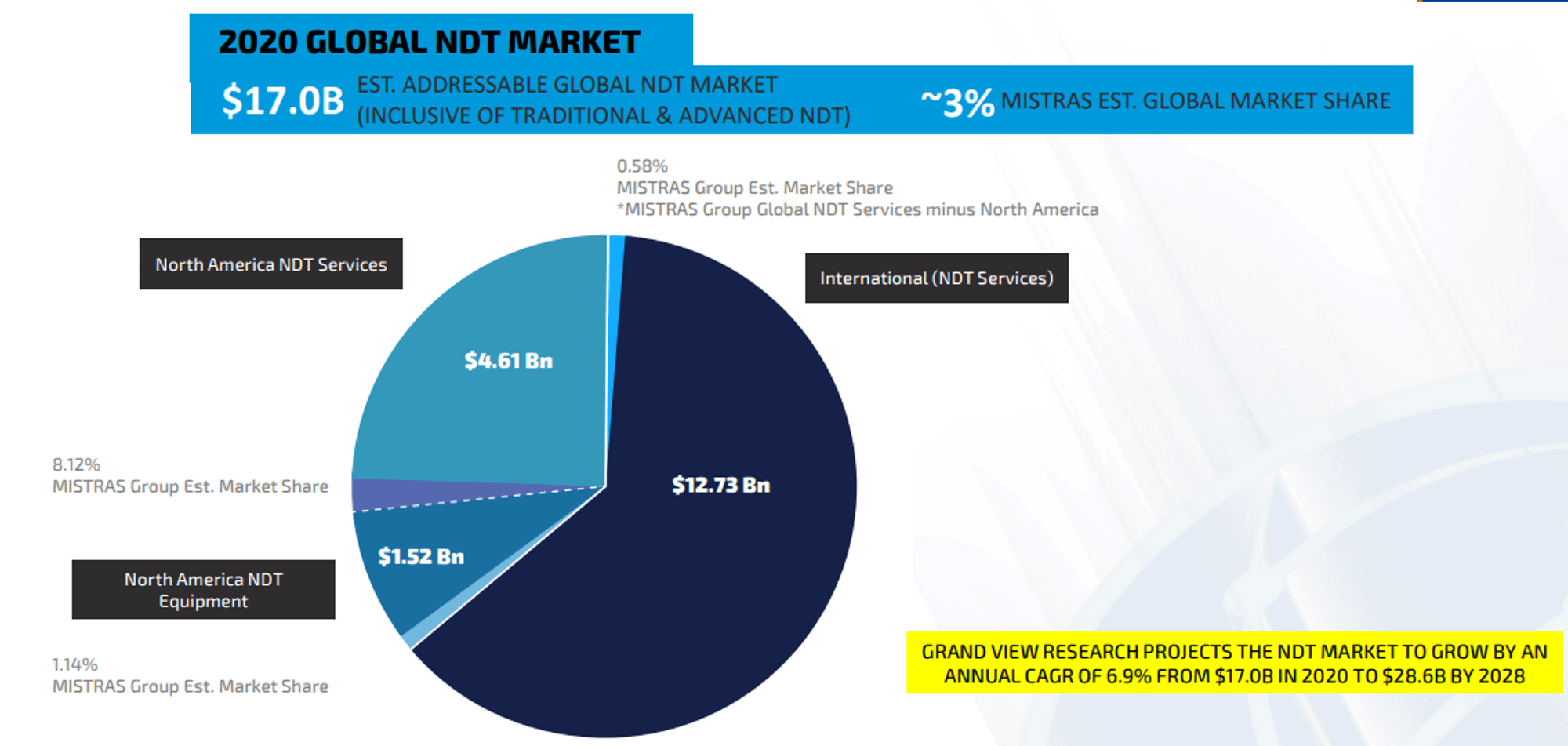

Industry Characteristics and Trends

Industry (MG)

{kind=link}

The NDT segment has a number of key characteristics that are worth highlighting for the purposes of assessing the attractiveness of MG. Namely:

- Robust demand: Although many of the industries it targets are cyclical, spending with MG should remain relatively robust given the importance of its service to the client’s value chain. Reputation and regulatory compliance are critical within these industries and MG is a key player supporting this.

- Dependency on Industrial Sectors: Despite this, MG's growth is closely tied to the performance of industries it serves, such as oil and gas, where economic downturns or fluctuations in demand have shown to negatively impact capex cycles.

- Economic Downturns in Key Industries: Economic downturns inevitably lead to reduced capital expenditure by clients, with its targeted industries in particular being highly susceptible to deep underperformance. Given the long-term nature of capex spending, these downturns impact multi-year spending.

- Competitive Landscape: The industry for NDT and asset protection services is competitive. This has contributed to pricing pressure, particularly as innovation has driven down barriers to entry.

- Technological Disruptions: Rapid advancements in technology, including the emergence of new inspection methods or technologies, can materially impact MG’s service offerings if it is not the one innovating.

- Cyclicality of Capital Expenditure: More broadly, capex spending generally follows cycles, tied to particularly macroeconomic indicators/conditions. We discuss two such examples below.

- Clean Energy - The transition to clean energy promises to bring with it a significant increase in capital expenditure as global infrastructure is modernized to bring global emissions down.

- Increased infrastructure spending: Persistent underspending across many Western nations is contributing to the need for increased spending, coinciding the with development of emerging nations. The US is leading the way with its IIJA bill. **

Overall, we believe the industry exhibits attractive qualities, with scope for lucrative long-term returns. Despite this, MG has been unable to capitalize thus far, implying a high degree of execution risk. The industry’s growth rate is more than double MG’s currently ( Source: Management communications ), implying market share is being lost. We can only attribute this to poor execution.

Margins

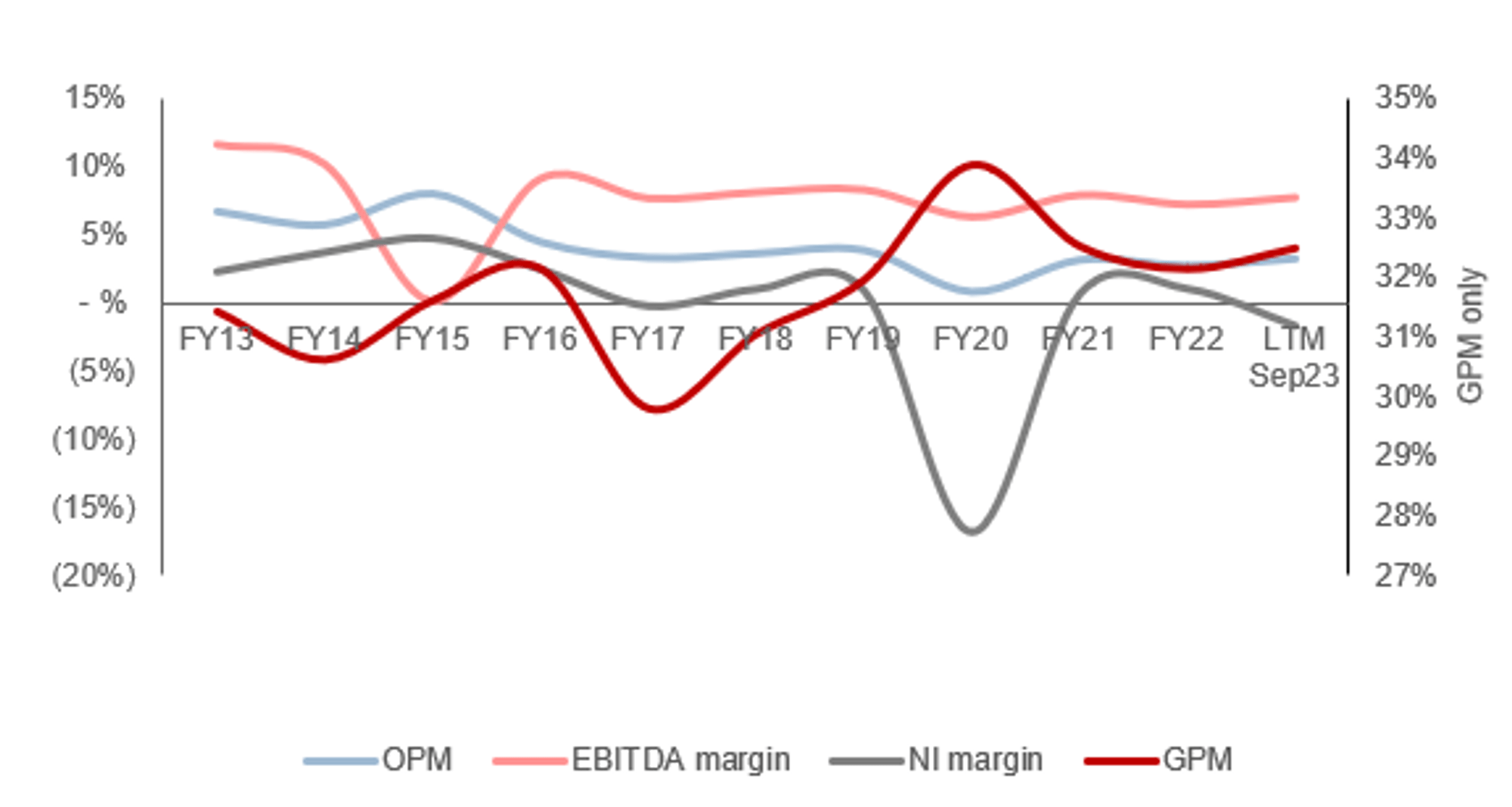

{kind=link}

MG’s margin development has been limited, with EBITDA-M declining from its FY13 levels. This has been predominantly driven by a growing operating cost base, with S&A spending increasing as a % of revenue from 19% in FY13 to 24% in LTM23, while GM% has increased by 1ppt.

This is likely due to a combination of factors. MG has struggled to sufficiently improve pricing over time as market conditions have improved. Further, its investment in operational capabilities to drive an improvement in growth has failed. Finally, although growth is mild, it appears the scope for operating cost leverage is already limited, despite being a <$1b business.

These factors and their respective weightings are concerning, as they limit MG’s future potential upside through an expansion of profitability. As we have discussed, the industry is highly competitive and mature, while MG still appears to be inefficiently executing. We do think this negative trend could be reversed through the digitalization of its service and increased focus on data sales.

Recent performance

MG’s recent performance has been weak, with top-line revenue growth of (1.7)%, 3.9%, (1.7)%, and 0.5%. In conjunction with this, margins have stepped up, returning to its pre-pandemic level.

Management is currently in the process of delivering “Project Phoenix”, which involves a revitalization of the company’s fortunes via the rationalization of ~15% of its non-billable workforce without any impact on revenue generation. Although this should deliver some margin improvement, we are concerned this will impact sales generation.

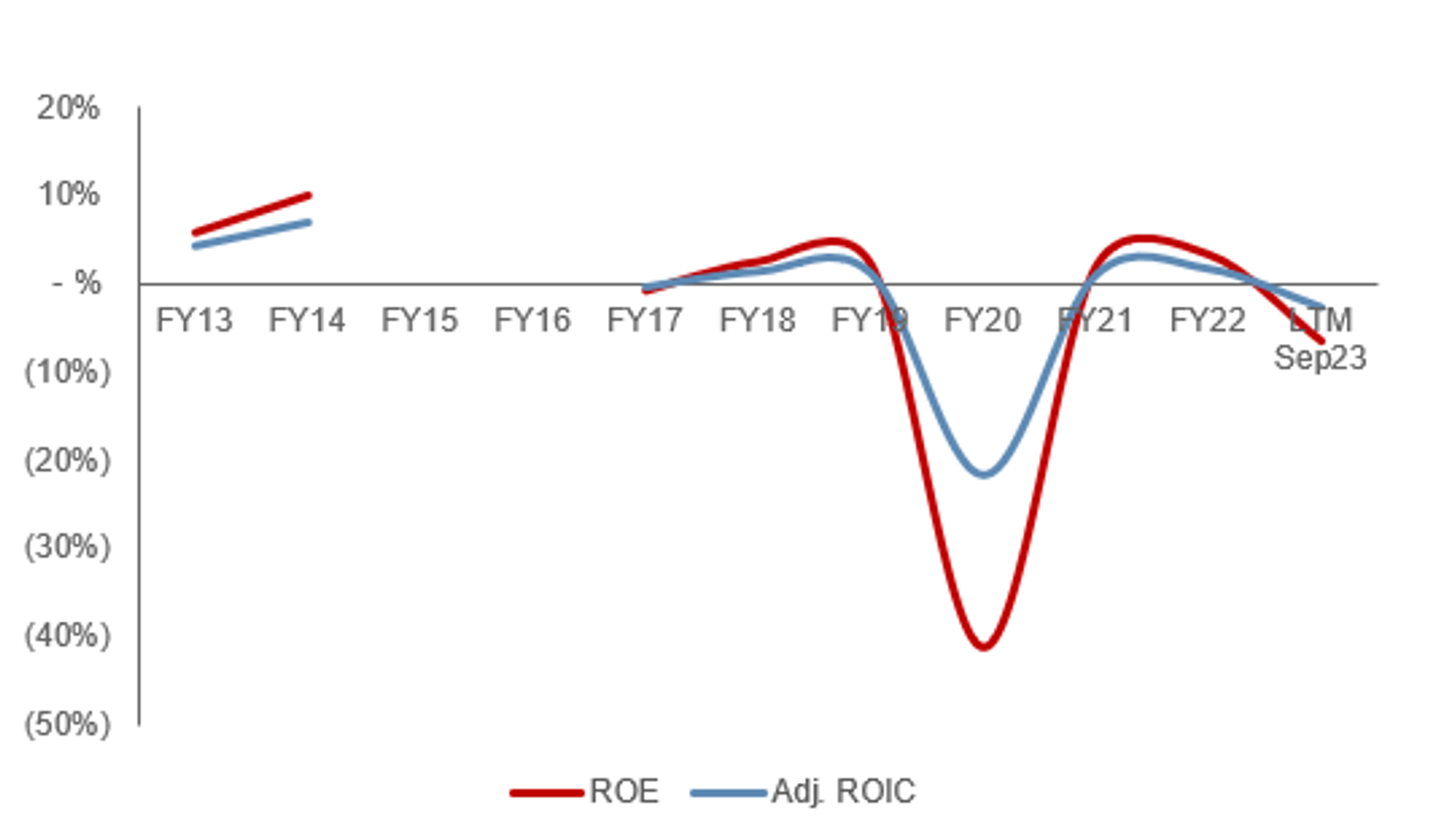

Balance sheet & Cash Flows

MG is moderately financed, with an ND/EBITDA ratio of 3.6x. At this level, the company is maximizing its capital structure without materially threatening its solvency. Management has primarily utilized cash to reinvest within the business, although as the company’s ROE illustrates, development has not been meaningful. The company has been unable to respond to competitive threats, contributing to minimal incremental returns.

{kind=link}

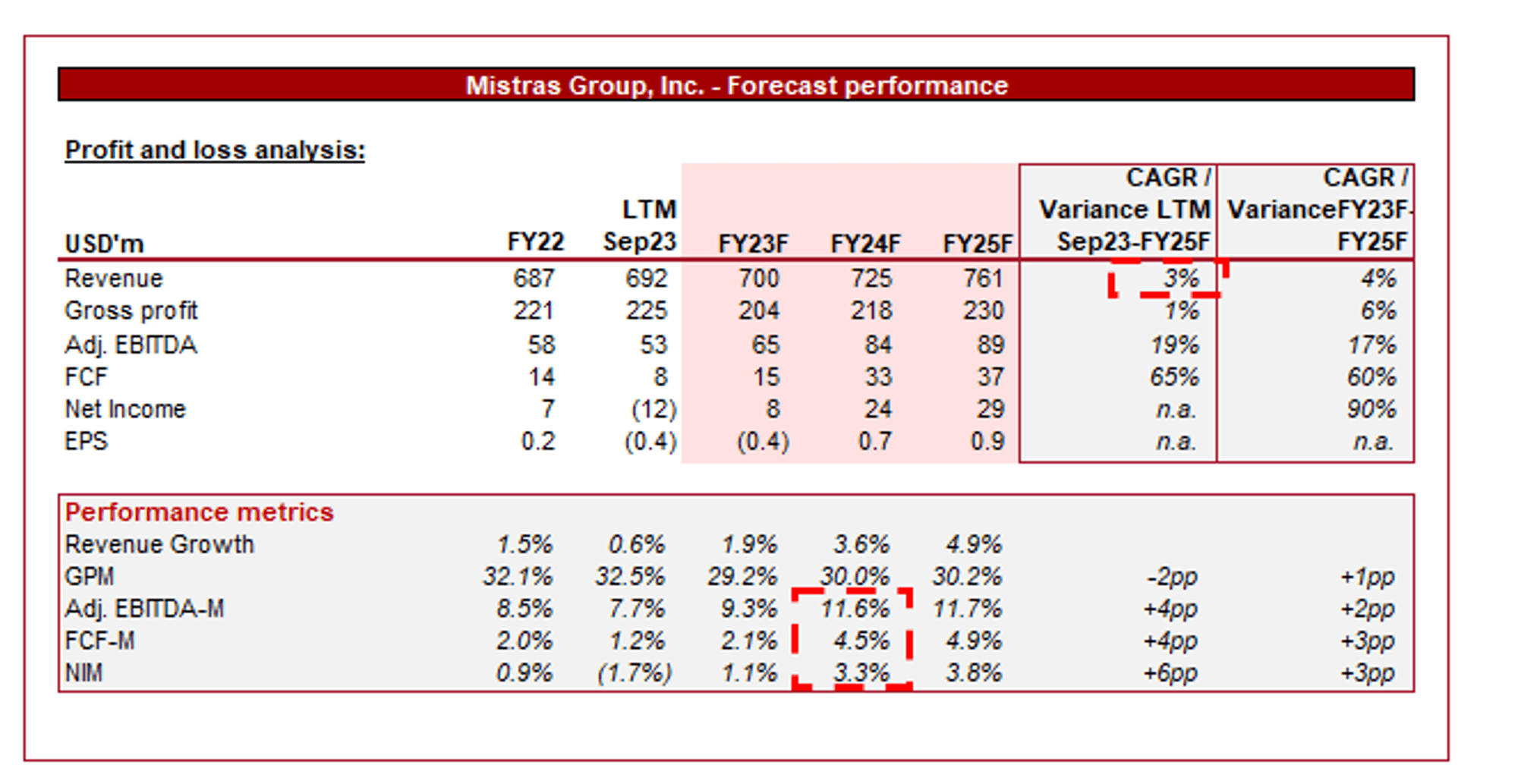

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continuation of its mild growth trajectory, with a CAGR of 3% into FY25F. In conjunction with this, margins are expected to sequentially improve, reaching their decade-high by FY25.

We broadly concur with the revenue assumptions. We have not seen sufficient commercial improvement to suggest the business will experience an acceleration in growth.

We are less convinced by the margin assumptions. Analysts are likely expecting the digitalization of its segment, alongside target-market tailwinds such as the clean transition to drive value. Although we see scope for this, we are currently unconvinced given the limited progress.

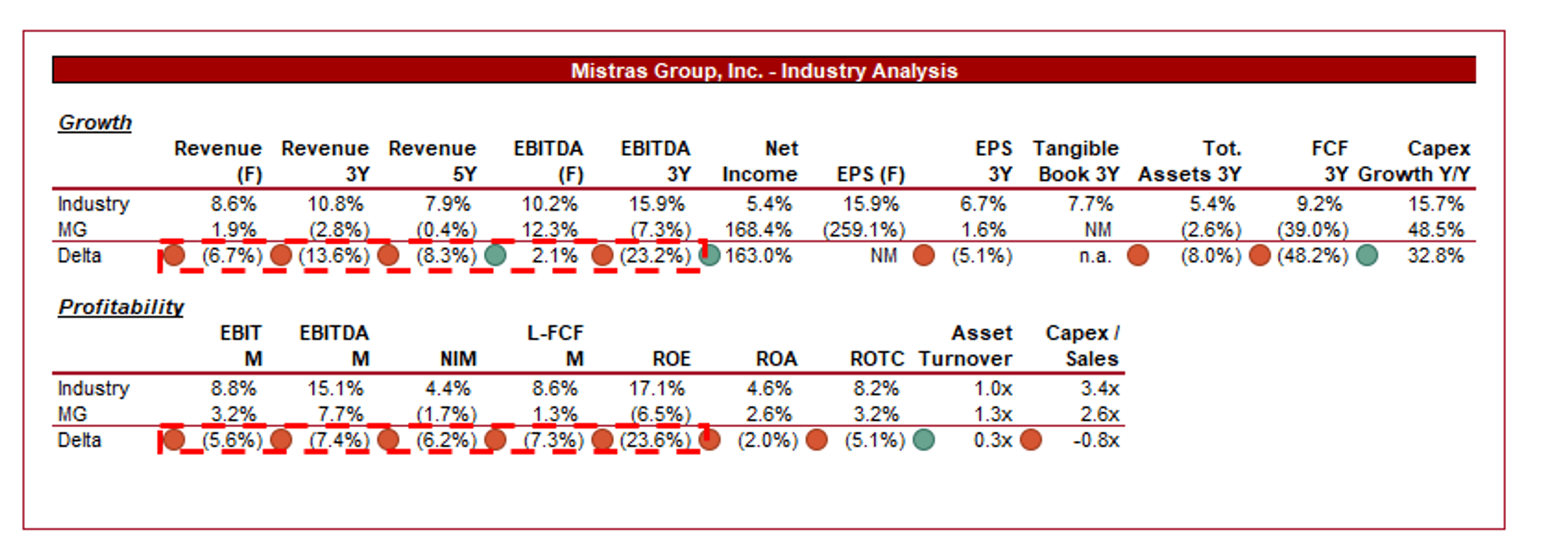

Industry analysis

{kind=link}

Presented above is a comparison of MG's growth and profitability to the average of its industry, as defined by Seeking Alpha (32 companies).

MG’s financial performance relative to its peers is disappointing, with lower growth and margins when compared to the average of its industry. This translates to a noticeably lower ROTC.

This is a reflection of a number of factors. MG’s segment, the asset protection, is highly mature with limited growth levers. Secondly, the company targets industries that are slow-moving and, in some cases, cyclical, such as O&G and Infrastructure. Contrast this with many in the peer group who target a broad range of industries, in many cases offer a SaaS model, and offer proprietary data analytics (compared to a service that is comparable among peers).

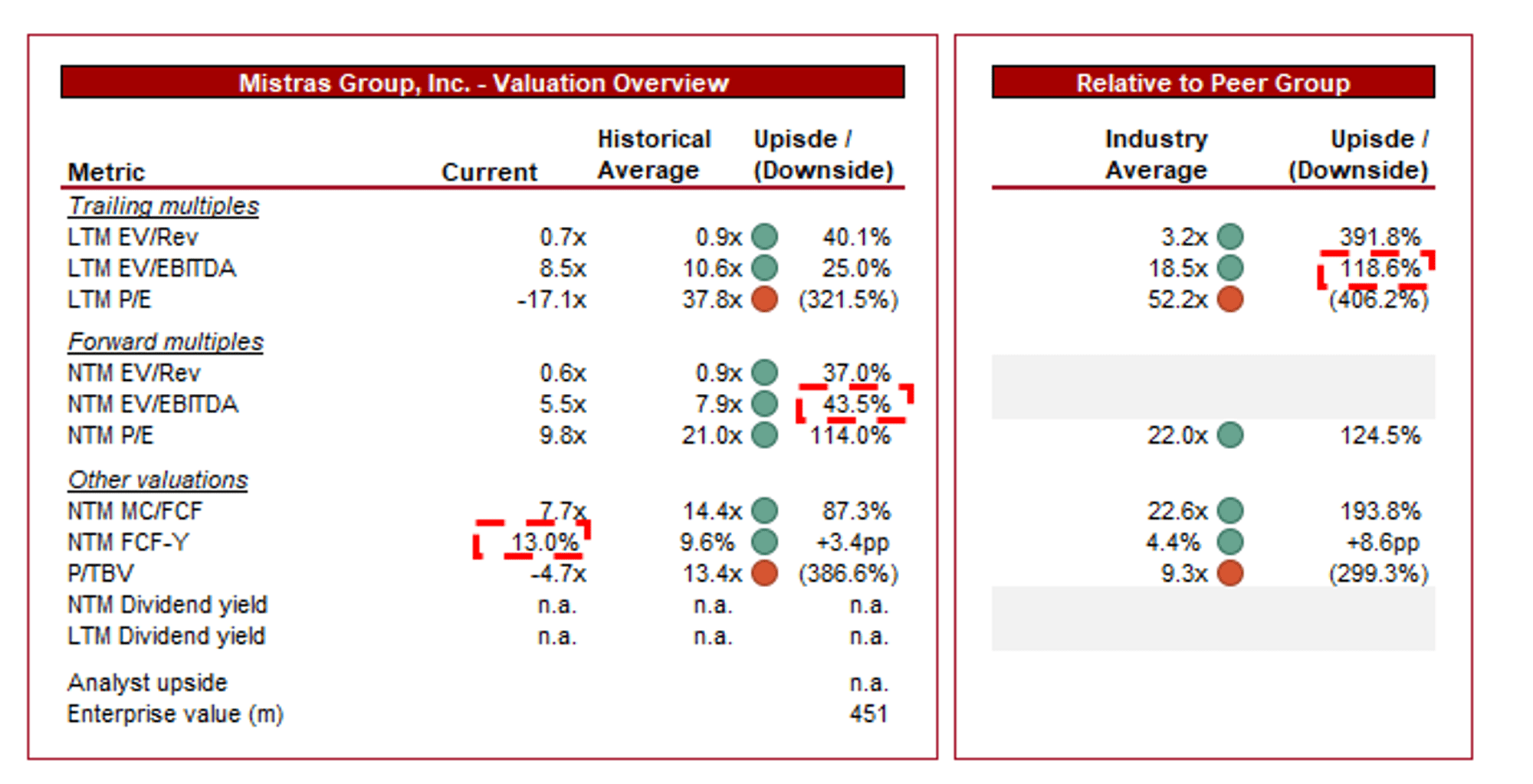

Valuation

{kind=link}

MG is currently trading at 9x LTM EBITDA and 6x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, although not to a substantial degree. The company’s volatile growth has been a systemic issue for a number of years, while its gradual margin decline is not wholly priced in. This is particularly the case given FCF margin has followed suit.

Further, MG is trading at a noticeable discount to its peers, both on an LTM EBITDA basis (~119%) and a NTM P/E basis (~125%). A discount is warranted, primarily due to the weaker financial performance and limited scope for upside longer term. This said, the size of the discount suggests potential value as the delta appears excessive when ROTC is only ~2% lower.

Overall, MG is likely slightly undervalued. It is trading at a substantial discount, which is reflected in its FCF yield of ~13%. This is over 3ppts above its historical average. Although MG has faced criticism, its industry is robust and the business is a leading player.

Key risks with our thesis

The risks to our current thesis are:

- Economic downturn impacting infrastructure spending.

- Failure to adapt to technological changes.

Final thoughts

MG is fairly lackluster in our view. Management’s execution has been poor and despite achieving growth, we feel the company has experienced a lost decade. This said, we do not think MG is hopeless. It has a strong market position and there are numerous industry tailwinds to benefit from. If Management is able to succeed with Project Phoenix, alongside improving its pipeline, we do believe MG could rapidly represent deep value, particularly at a current FCF yield of ~13%.

With the business appearing undervalued, we rate MG a soft buy.

For further details see:

Mistras Group: Trading Cheaply With Scope For Upside