NWL - Mitsubishi Pencil: A Niche Player Gaining Global Market Share

2023-08-29 09:40:27 ET

Summary

- Mitsubishi Pencil is bouncing back from the pandemic and gaining market share overseas with differentiated products.

- The company is undervalued with a PBR of 1.0x and has a strong track record of product development and free cash flow generation.

- Growth prospects include continued market share gains overseas, increased inbound tourism demand, and normalization of raw material prices.

Investment thesis

Mitsubishi Pencil ( MSBPF ) is a Japanese designer and manufacturer of writing equipment. The business has bounced back from the pandemic, is gaining market share overseas with differentiated products, and is cheaply valued at PBR 1.0x. We rate the shares as a buy, with a strong track record of product development and free cash flow generation.

Quick primer

Mitsubishi Pencil is a designer and manufacturer of writing instruments such as ballpoint pens, mechanical pencils, and pencils. Established in Tokyo in 1887, it started selling pencils for government use before developing pens and accessories for the general public. Its core brand is the 'Uni' and 'Uni-ball', with their rollerball products becoming globally popular since their release in 1979. Other brands include 'JETSTREAM' pens and 'eye Roller Fine'.

Despite the company name and similar company logo, Mitsubishi Pencil Company is unrelated to the Mitsubishi Group (unlisted). The largest shareholder is itself, with a 10.4% stake held as treasury stock.

Its key peers include PILOT Corporation ( POGHF ) (the manufacturer of 'FriXion' erasable pens), BIC ( BICEY ), Acco Brands ( ACCO ), Faber-Castell (unlisted), Pentel (unlisted) and Staedtler (unlisted).

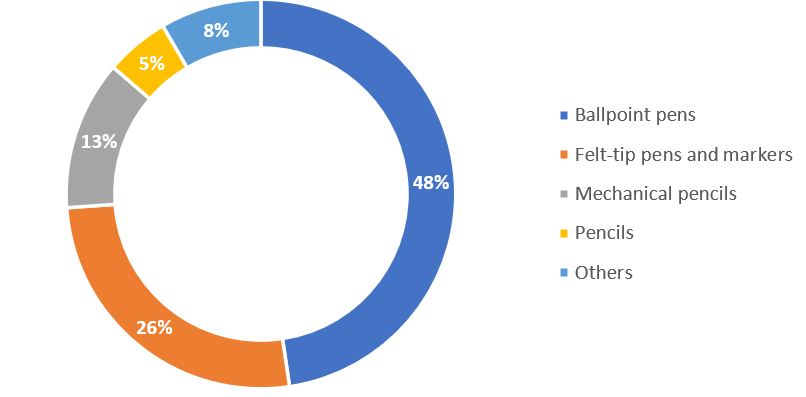

H1 FY12/2023 sales by product

{kind=link}

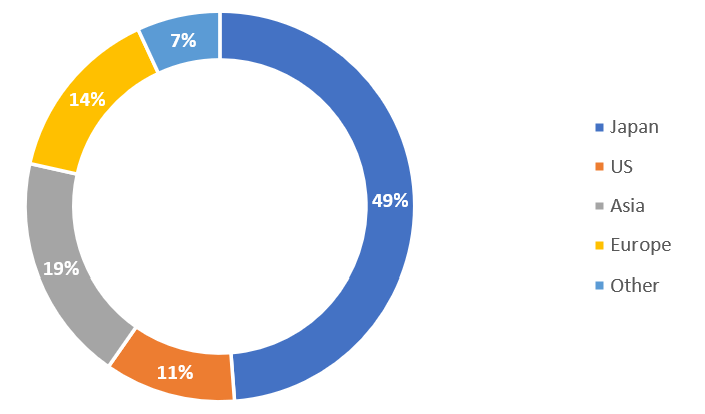

H1 FY12/2023 sales by geography

{kind=link}

Assessing growth prospects for this value stock

Mitsubishi Pencil and the stationery sector were negatively impacted by the pandemic, with the focus on digital transformation superseding demand for traditional writing equipment, particularly for office work as well as in the education sector. However, demand has bounced back stronger than expected, with Q2 FY12/2023 sales recording the highest level to date, together with gross margin reaching 50.2% ( page 6 ).

With the shares trading at a PBR of 1.0x, the company is over-capitalized with a net cash position of approximately JPY44 billion (equivalent to 37% of market capitalization), as well as JPY19 billion of long-term investment securities. The heavy balance sheet has meant a historically low ROE at 7%, although the company has a strong track record of free cash flow generation.

We want to assess whether 1) the recent recovery trend is a sustainable one, and 2) how management will act to slim down its balance sheet and allocate capital more effectively.

Demand drivers

With 51% of total sales in H1 FY12/2023 derived from overseas markets, the company is gaining market share in Europe and the US. This appears to be driven by unique new product offerings centered around its gel ink ballpoint pens. Q2 FY12/2023 sales grew 7.0% YoY driven by overseas demand, although there was a FX tailwind due to the weakened Japanese yen YoY. The gross margin reached 50.2% for the quarter shows that the company's products are differentiated which allows for some pricing power - BIC is at around 48%, although PILOT is higher at 53%.

Whilst European and American pen makers have a sizable presence in their home markets, Japanese companies like Mitsubishi Pencil have been gaining market share over the last 10 years via product innovation, quality, and price. The overseas mass market is now fairly comfortable using Japanese brands, with the higher-end markets being catered by the likes of Parker ( NWL ), and Shaeffer (unlisted), and going up to the luxury market with the likes of Mont Blanc (Richemont) ( CFRHF ).

The stationary market has also become somewhat hit-driven, with new products coming online to offer consumers the latest in design, function, and experience. Mitsubishi Pencil consistently spends 5% of sales on R&D expenditure, which has enabled it to develop successful products consistently.

We believe in the medium term, the growth drivers for the company will be 1) continued market share gains overseas, 2) a marked upturn from inbound tourism demand, with Chinese travelers coming back to Japan, and 3) longer-term normalization of raw material prices which currently remain at a high level which will improve profitability. The company is also aiming to diversify into cosmetics (primarily growing its eye shadow products).

Balance sheet

The company has excess capital due to its free cash flow generative nature but has a low dividend payout ratio steady at 30% and an ad hoc share buyback policy (the last announcement was a 1.22% share buyback plan in February 2023). Management has outlined plans to retire its treasury shares, although there have been no recent announcements.

M&A is not strategically important to the business, so we believe capital allocation will focus more on returning cash to shareholders. We believe that in the medium term, the dividend payout ratio will have to increase, and share buybacks will continue if management wants to maintain having a PBR multiple above 1.0x, something that is being actively encouraged by the Tokyo Stock Exchange. There is also a growing concern about becoming targeted by activist funds, which Japanese corporations are keen to avoid.

We do not expect to see a sudden change in Mitsubishi Pencil's shareholder returns policy. However, with its growing exposure to overseas markets, and its medium-term goal of becoming a global key player in the stationary market as it approaches its 150th anniversary in 2036, we believe that it is a matter of time until it adapts to more current investor expectations.

Valuation

The shares are trading on PBR 1.0x, and on PER FY12/2023 14.6x on company guidance. The dividend yield is 1.9% which is quite low and not very attractive. Overall, for a company with a strong net cash balance sheet, strong free cash flow, and a strong global niche brand, we believe the shares look cheap.

Risks

A sudden strengthening of the Japanese yen will act as a major headwind to sales growth and will dampen margin expansion. Intense market competition will mean that a sudden 'hit product' from a competitor could result in market share losses.

Upside risk comes from a sudden short-term upturn in domestic demand, fuelled by Chinese inbound tourist demand as group tours recommenced in August 2023. The continued weakening of the Japanese yen versus the US dollar will be a tailwind for trading in H2 FY12/2023, although hurdles will be set higher YoY.

Conclusion

Writing instruments is not a growth market, but there are market sub-segments where differentiated products make a difference. Mitsubishi Pencil is demonstrating that there is demand for quality pens via overseas market share gains and that it is set to continue generating shareholder value with a steady business. Valuations look too cheap for a niche franchise with decent fundamentals with a positive direction for improving shareholder returns. We rate the shares as a buy.

For further details see:

Mitsubishi Pencil: A Niche Player Gaining Global Market Share