MITSF - Mitsui And Co: Buffett Sees Oil Offsetting Metallurgical Coal

2023-05-01 11:23:02 ET

Summary

- Automotive has the obvious headwind in that credit markets are contracting, and this impacts the machinery business.

- Met coal has been benefiting from adverse weather effects in Australia, constraining supply. Lower steel demand from construction and supply normalisation is bad for Mitsui.

- Oil may be a decent end-market that can keep levels for Mitsui, although the picture is somewhat ambiguous.

- The company is cheap, and while there are going to be headwinds in some businesses, a year of high oil prices should balance the earnings picture out to sustain 18% earnings yield.

Mitsui & Co ( MITSY ) will probably sustain its earnings yields, but it depends on how oil does in 2023. The picture is a bit ambiguous, as some segments are surely going to see headwinds, and the tailwinds are primarily from incorporating structurally higher oil prices for a great chunk of 2023. The PE is low, and it makes sense why Buffett likes this stock. Japanese markets remain structurally cheap, and this might be a rare instance where a Buffett stock isn't just automatically overvalued. We'd consider hopping on if it weren't for the fact that we have our own Japan ideas that are more under the radar. The yield is also usually variable for Japanese stocks, so keep that in mind if you're focused on yield, especially where there are a lot of moving points to Mitsui's earnings.

Looking at the Q3

Let's start with the 9-month data to get an idea of the puts and takes.

{kind=link}

Mitsui Segments (Q3 2022 Pres)

The energy business as well as the mineral and metal resources businesses are the ones that dictate the majority of the results. The machinery and infrastructure business is reasonably important as well.

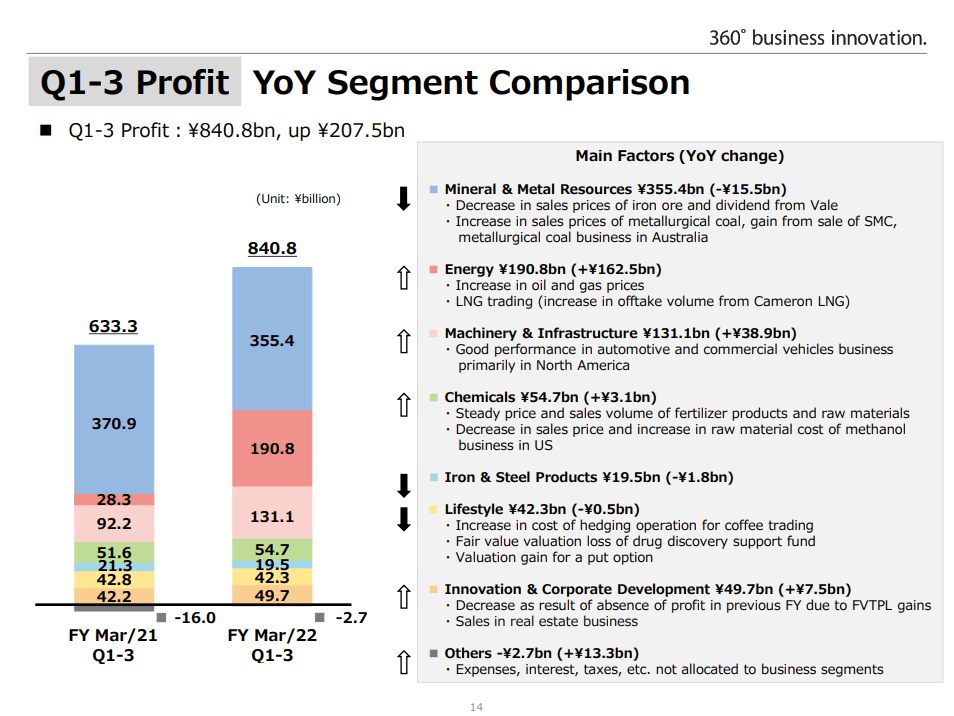

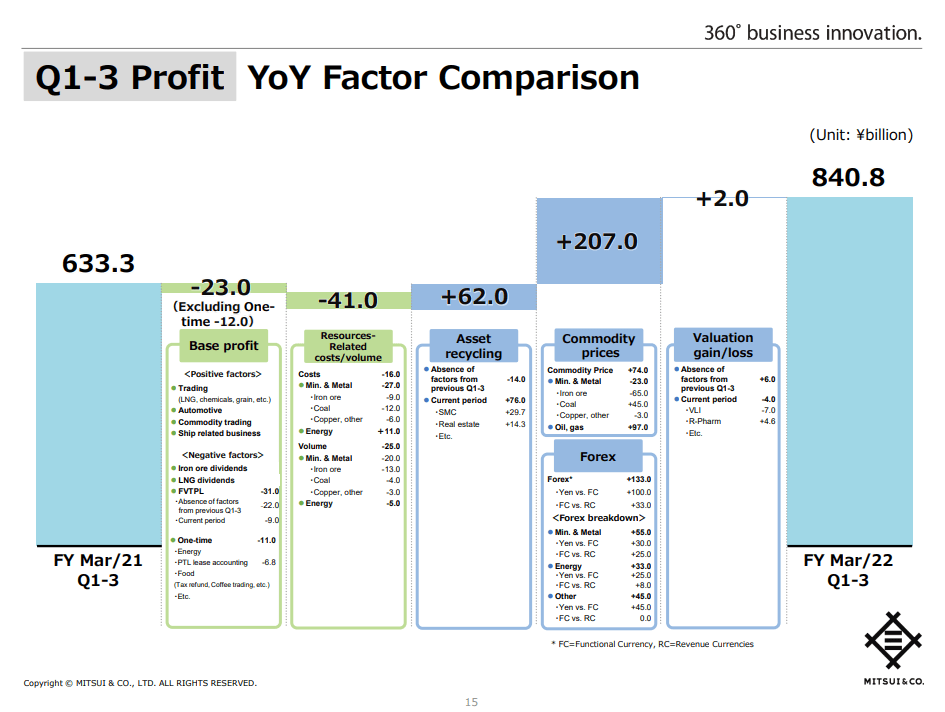

- In the 9m results, general commodity pressures after a fervent prior year has put some pressures on mineral and metal resources. The key positive in miner and metal resource has been the metallurgical coal prices, which have been extraordinarily high throughout 2022. While spot prices are substantially down from the average 2022 levels, about $370/tonne to $300, there is still a lot of room to fall as blast furnaces become less profitable with building and construction taking a downturn, as well as other key markets for steel. The reason is not only on the demand side, but the supply side constraints related to the Australian adverse weather effects limiting met coal supplies should subside. The S/D dynamics for met coal are really poor, and this backstop to the pretty limited declines so far in mineral and metal resources will no longer continue. Mitsui recognises this as shown in their forecasted profit evolutions.

- Energy has been doing extraordinarily well on account of structurally higher oil prices in the latter half of 2022, which has boosted a good chunk of the nine months that we have closed into Mitsui's latest earnings results that we're looking at here. Prices remain high as supply cuts continue and as issues around oil availability and supply, interacting with geopolitical factors around price caps and tanker insurance in the Black Sea, as well as strategic factors around oil reserves, and we think that the dynamics will continue to support high oil prices throughout 2023. Markets must think this as well because earnings are not forecast to fall much despite what will be a very strong FY 2022 once the FY closes in this latest quarter.

- Machinery and infrastructure have been driven by machinery in automotive end-markets, with dissipating issues on the supply side in semiconductors releasing the bottleneck on volumes and correlating with capacity expansion.

{kind=link}

9m Profit Evolution (Q3 2022 Pres)

{kind=link}

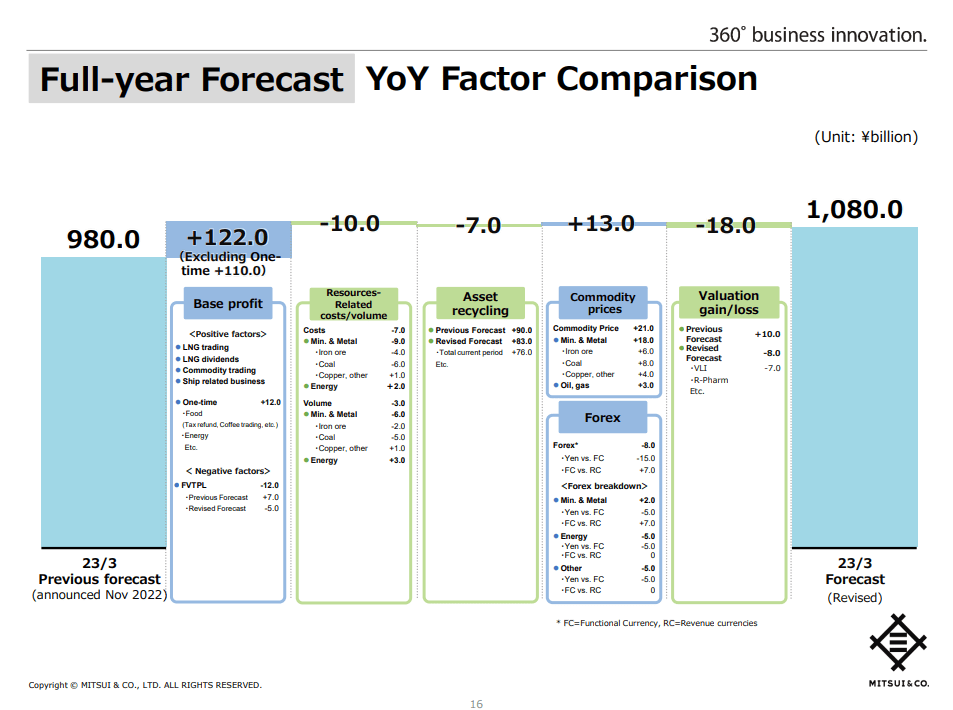

FY 2022 Forecast Earnings Evolution (Q3 2022 Pres)

What we think is coming

The FY forecast shows that met coal's impact will diminish meaningfully to result in only a small help for the FY 2022 increment. On the other hand, the latest quarters showing declines in copper and iron ore aren't expected to offset the amazing start these commodities had in terms of trading conditions at the beginning of the year. While there may be some latent demand for copper since it's heavily associated with electrification and the renewable transition, we don't have high hopes for iron ore, and similarly, we don't have much hope for met coal in producing another positive increment for the coming FY 2023.

Automotive is an interesting discussion because major sinks of automotive demand are experiencing credit crunches, that will eventually start impacting automotive market conditions. As of now, pent-up demand effects are offsetting any demand pressures being introduced by the credit situation. We think that for the final quarter of Mitsui's 2022, but also the following Q1 2023 should see a decent performance in these end-markets, but not too much incremental growth. This will mean that the machinery and infrastructure segment should be alright for another quarter or two, perhaps with some growth in the renewable power generation construction business.

The big new profit contributor is energy, and the major effect for understanding the direction of earnings is that 2022 did not incorporate a full year of structurally higher oil prices. We think that both the supply and demand side of oil present a rather high likelihood of another year of high oil prices, likely in line with their current levels.

This means that while commodities, especially met coal, will have a very disappointing showing relative to the brilliant 2022, oil prices at high levels should mean a full year of strong results from the energy segment, which is one of the higher in terms of operating leverage for Mitsui. This is certainly good news, because the <6x PE valuation, and consequent 18% earnings yield, is highly likely to be sustained for another year. This is why Warren Buffett likes these companies, and was the reason he cited for considering upping his positions across his Japanese holdings in the major trading companies. A high likelihood of another year of elevated earnings yields being sustained is a meaningful selling point for investors, and one that we respect.

However, we have our own Japanese ideas that are more under the radar and much higher conviction than these high visibility ideas. Moreover, even the trading companies don't offer any special advantage in terms of dividend yields, where payout policies are always variable and subject to pretty sudden changes based on discretionary CAPEX plans and perceived volatility in end-markets by management which tries to anticipate problems with a lowered dividend to shore up cash.

Mitsui is a solid idea, we think it's going to outperform, just not as much as other things.

For further details see:

Mitsui And Co: Buffett Sees Oil Offsetting Metallurgical Coal