MITSF - Mitsui & Co Is Commodity Exposed And Cyclical

Summary

- Mitsui & Co is a Japanese conglomerate that invests in interests that give them front-to-back exposure in lots of hard value markets.

- Their exposures are strong in the lead up to today's environment, and they've seen strong growth thanks to being in all the right spots given the invasion.

- Most of their exposures are cyclical or commodity related, and their multiple pretty much reflects that, being in line with other E&P, gas and commodity players.

- There may be a material discount to other smoother full suite players because Japanese markets are a little less efficient.

Published on the Value Lab 9/10/22

Mitsui & Co ( MITSY ) is a pretty interesting Japanese conglomerate that takes positions in a lot of other businesses, primarily in hard asset businesses like commodity and energy, that gives them a fair bit of cyclicality. This is a Warren Buffett stock actually, with Berkshire ( BRK.A )( BRK.B ) investing in it about a year ago. They have some smoothness of earnings thanks to vertical integration in their various segments, but the cyclicality is simply there in most of their businesses. Overall, the company is not expensive on a P/B basis, despite its assets being attractive in the current environment, and its PE ratio looks fair, but there's cheaper Japanese companies out there. Nonetheless, relative to full suite US energy peers, there is some value in Mitsui.

Q1 Comments

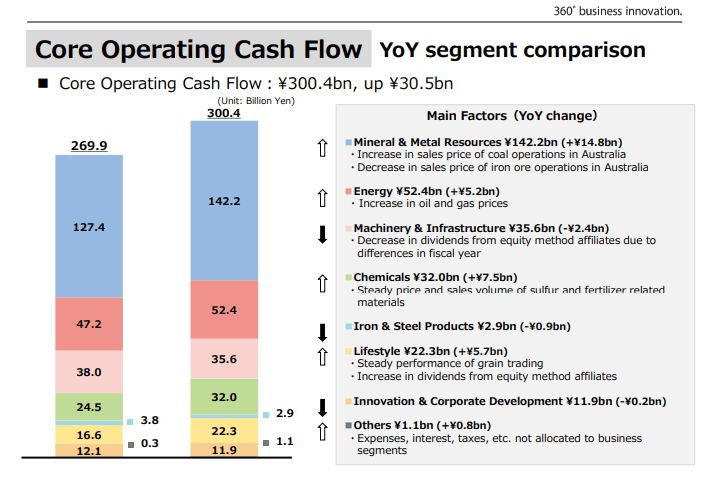

Mitsui is a sogo shosha, essentially a quintessential Japanese general trading company with a business model whereby they take interests in lots of projects, do a lot of distribution and act as an intermediary for a lot of processes. These are its segments and their split measured by core operating cash flow, which is basically operating cash flows excluding working capital effects.

{kind=link}

Let's quickly go through the segments by what they do:

- Mineral and Metal Resources - Own mining interests, recycling operations and do trading of metallurgical coal, iron ore, copper and nickel.

- Energy - Upstream oil and gas investments, LNG assets, nascent investment in next generation fuel logistics and infrastructure.

- Machinery and Infrastructure - Power generation assets, other infrastructure, automotive construction machinery with substantial US markets, aircraft leasing and purchasing, transportation assets, logistics and ships.

- Chemicals - Basic chemicals, performance monomers and coatings + functional materials, biomaterial and forestry, fungicide, fertiliser, seed business. Basically a pretty commodified chemicals portfolio with some more specialised stuff related to agriculture.

- Iron & Steel products - More downstream segment of processing iron and steel products, production of steel parts, steel production, wind power tower manufacturing and a power maintenance business.

- Lifestyle - Ownership of healthcare providers in Asia, distribution of pharmaceuticals, diagnostics businesses, grain trading, feed and food production and import/export businesses.

- Innovation and Corporate Development - Digital solutions, CRM, logistics tech as well the operations of managing the real estate portfolio.

The commodity related businesses are doing pretty good in Q1. The iron ore exposure in mineral and resources is a headwind and has limited growth, while energy related products like coal, electricity, oil and gas have been tailwinds to the mineral, energy and infra business respectively. The machinery business is also being supported by strength still in automotive machinery supply , but we don't believe in this market's resilience. In general, the machinery and infra business is being hit by a falling CAPEX cycle.

Chemicals has been solid thanks to the tight fertiliser and agrichemical market following the invasion of Ukraine. Similarly, the grain trading operations within the lifestyle segment are performing well. Iron and steel products have very thin margins due to weak recycling results, although those have improved since the market crash in 2016, and generally tight steel production margins. Parts production should be doing good.

Lifestyle is perhaps the most secularly interesting segment as while exposed somewhat to commodities, it also has other more stable healthcare exposures in Asia. Those are likely contributing to the growth, but the majority is coming from grain volatility. Innovation and corporate development is pretty irrelevant, and pressure on real estate will likely make this segment even more irrelevant in the mix going forward.

Segment Split (Integrated Report 2022)

Our judgement is that about 85% of the business is cyclical and commodity exposed, while the rest is in more secular markets. In general, your view on energy prices in general should dictate your view on Mitsui.

Remarks

Most of its interests are fully consolidated, and there are about $1 billion worth of company stock in holding to offset the net financial position. The multiple lies just above 10x EV/EBITDA, but the PE is about 7x because of pretty low below-the-line net costs.

As you can see from the segments, while all have some equity in production and more asset heavy activities, there is always an element of trading and supply that Mitsui will engage in between businesses or within the business vertical. In general, the full-suite activities do smooth out their exposure in commodity related businesses, but many of their businesses remain very cyclical, as said about 85%. The delta of that chunk will depend primarily on energy prices. Our view is that energy prices are likely to hold up quite well. Demand concerns meant speculators reduced the prices of oil for a bit, but OPEC supply cuts and general supply rationality soon followed to support prices. This pattern is likely to continue and therefore Mitsui is an oil play.

The multiples are in line with upstream oil and gas peers. Mitsui is a little more smoothed out than them in our opinion, and are going to have less volatile results. Relative to full suite oil and gas players in the US at least , they are a bit discounted, but in no way extraordinarily underpriced. It is a quality business, and likely the Japanese markets remain less properly parsed than the American ones, so there is probably some value here. The yield isn't bad either at 4%. Solid company.

For further details see:

Mitsui & Co Is Commodity Exposed And Cyclical