MITSY - Mitsui & Co.: Resiliency In A Tough Commodity Environment (Rating Downgrade)

2023-11-01 07:42:22 ET

Summary

- Mitsui & Co. announced an increase in its full-year forecast and dividend, although it was largely due to a weaker yen. Commodity prices have stabilized.

- Mitsui is pursuing its new 3-year plan, with lots of asset sales and acquisitions, resulting in a higher than normal level of one-time gains, offsetting some impairments.

- The company is meeting its commitment to return 37% of core operating cash flow to shareholders.

- Given the run-up in share price (even in USD) and valuation in the middle of the pack, Mitsui is now a Hold.

Setting The Tone

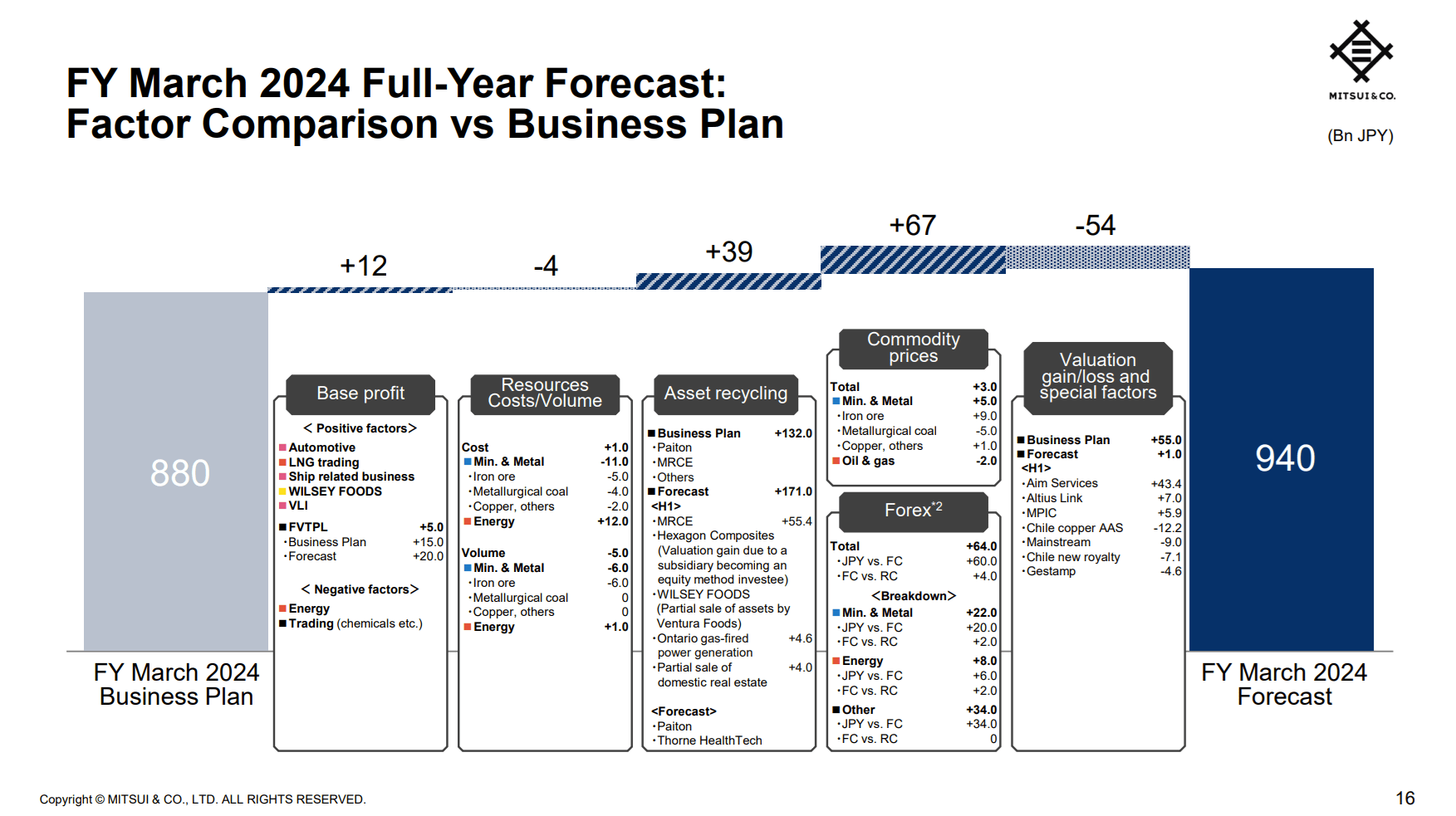

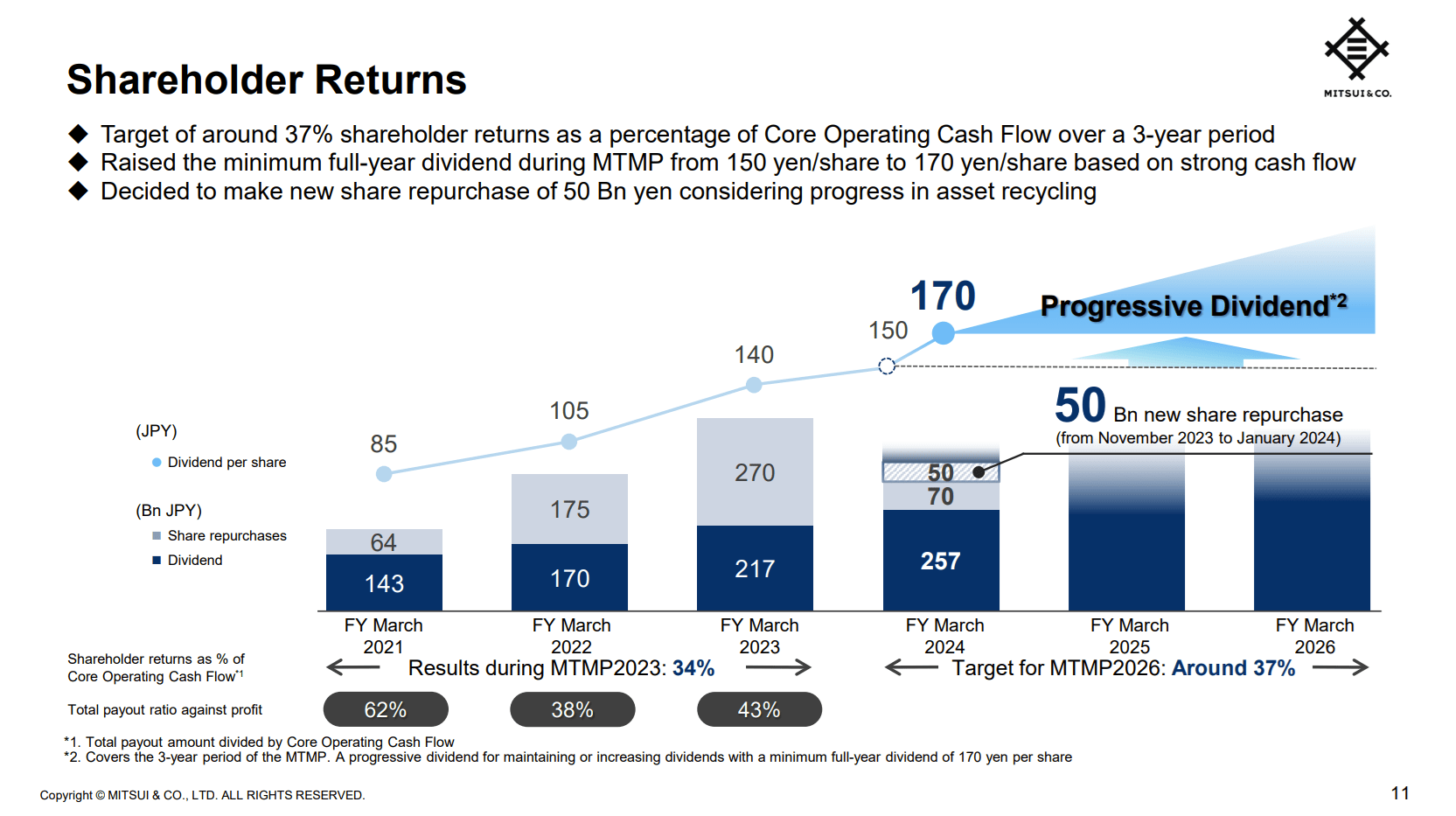

Mitsui & Co. (MITSF) (MITSY) was the first of the five major Japanese trading companies to report fiscal 1H 2023 earnings on 10/31. (Three others report on 11/2 and Itochu (ITOCY) (ITOCF) wraps up the season on 11/6.) Mitsui set the tone with an increase in the full year forecast (¥940 billion profit, up from ¥880 billion) and an even bigger increase in the dividend. The payout will now be ¥85 per share each half year for a total of ¥170, compared to the original FY 2024 plan of ¥150 and FY 2023 actual of ¥140.

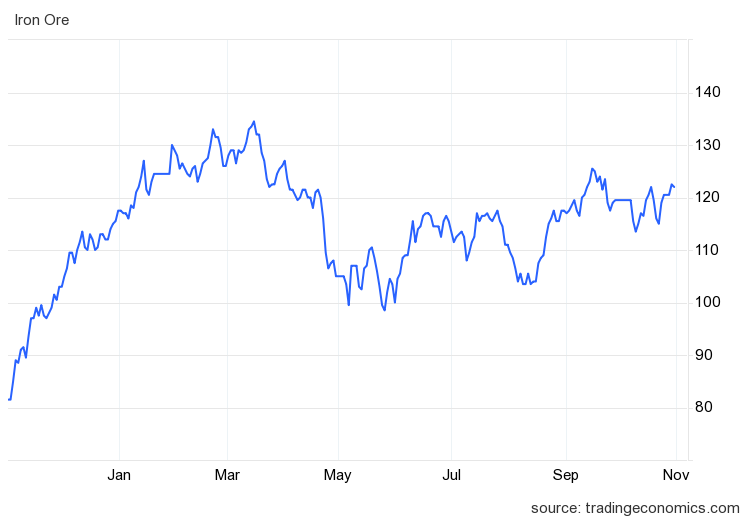

Unlike the last few years when the trading companies had to revise their forecasts each quarter because of commodity prices, prices haven't moved much since the annual plans were developed six months ago. You can read more about the pricing environment at that time in my last Mitsui article . While the outlook for iron ore , Mitsui's largest commodity, was pretty grim at that time, renewed stimulus measures and deficit spending in China have helped support demand. The price is back to end-March levels.

{kind=link}

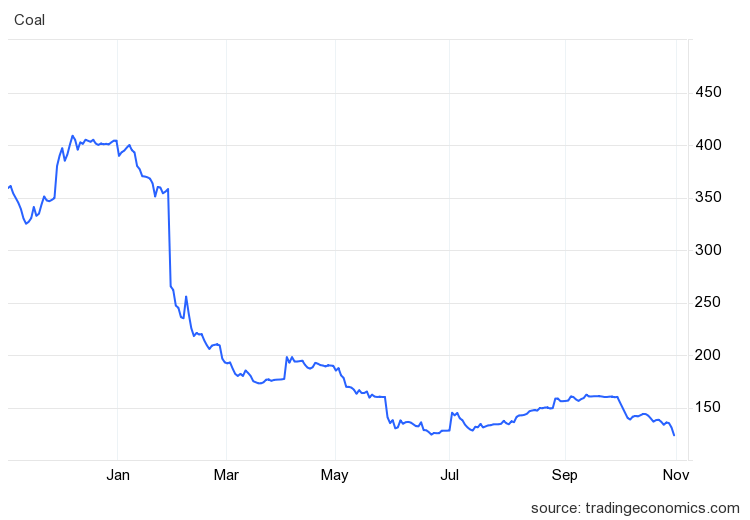

Coal prices have been scraping bottom all year after hitting unusual highs in 2022, however this was expected and is not a risk to the plan.

{kind=link}

The latest FY forecast for Mitsui's other key commodities are close to the original plan. Oil (company average realized price) is now forecasted at $91/bbl vs. $88 in the plan. Natural gas in now $2.62 vs. $2.99, and Copper is $8566/ton vs. $8600.

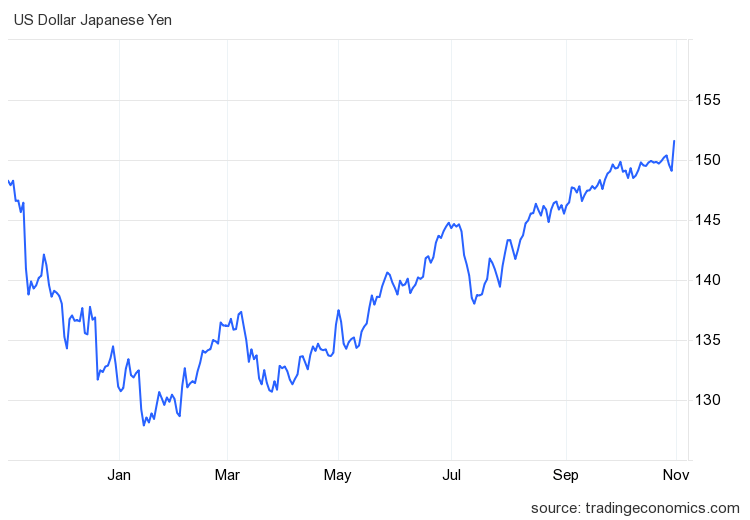

The real driver of the increase in the forecast is the weaker yen, which is adding ¥64 million vs. the original plan, a bit over the entire ¥60 million difference. US based shareholders will be happy with this as the ¥10 per half increase in the dividend at least offsets the decline in the exchange rate .

{kind=link}

The bridge from the original plan to the new forecast shows the importance of the exchange rate, but there are a couple of offsetting factors that are also worth looking at to see how Mitsui is repositioning within its new three-year plan that was rolled out in May.

{kind=link}

Diving Into The Three-Year Plan

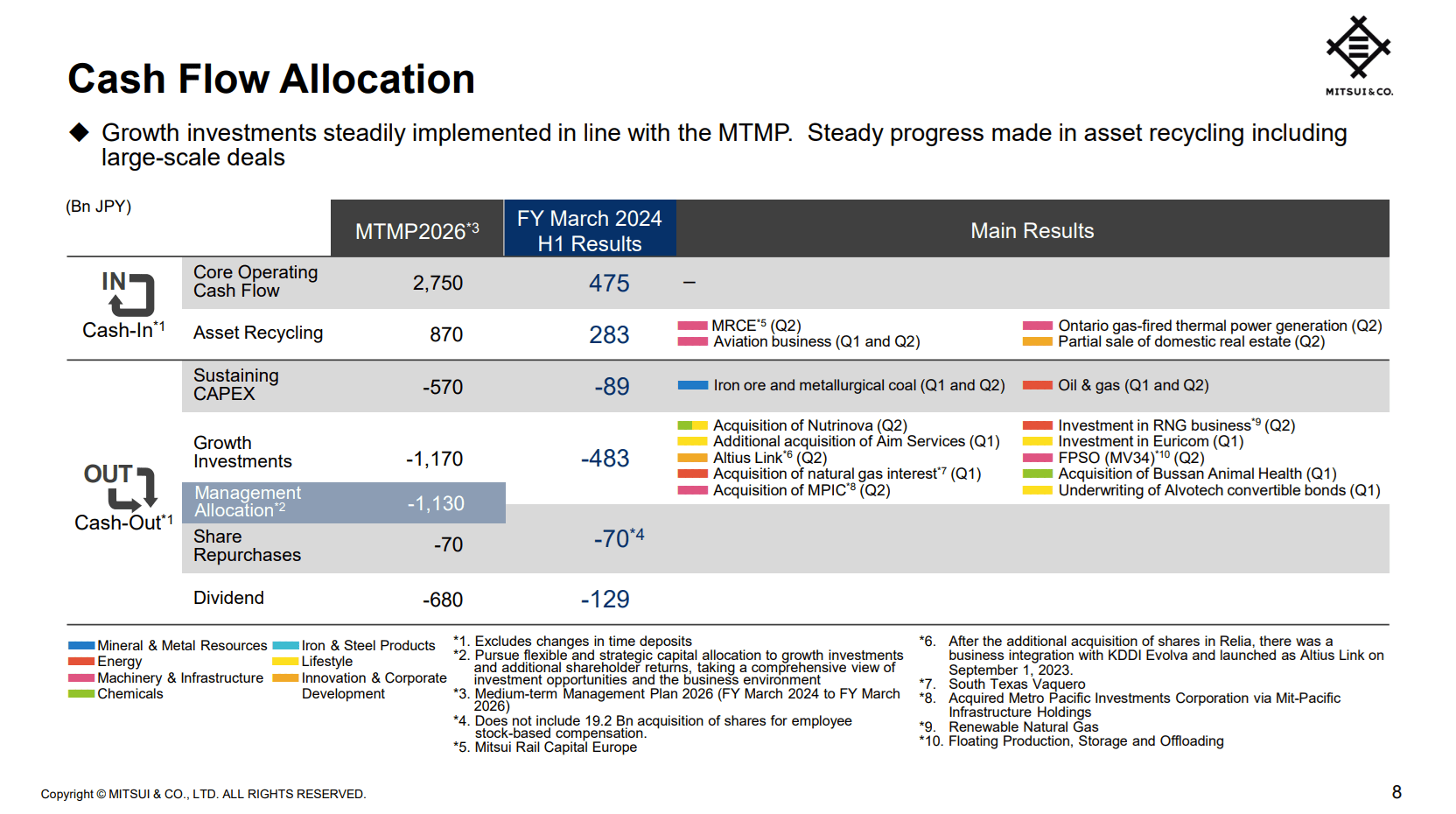

In my last Mitsui article, I provided more detail on Mitsui's new 3-year Medium-Term Management Plan, known as "Creating Sustainable Futures". While I pointed out in that article that Metals & Minerals and Energy were still a big part of the sustainable future, there are indeed lots of other businesses involved, and Mitsui has been busy the last six months trimming some and adding others. As we see on the chart below, Mitsui has already completed over 1/3 of its planned "asset recycling" despite being only 1/6 of the way through the 3-year plan. Businesses and assets disposed of include European rail car leasing, planes from its aircraft leasing business, a Canadian gas-fired power plant, and some Japanese real estate.

On the investment side, there are energy-related acquisitions including a floating production, storage, and offloading platform, and natural gas interests both traditional and renewable. However, there are also investments in infrastructure, food services, agricultural chemicals and veterinary medicine, communications, and IT call centers. Mitsui is over 40% toward its minimum planned growth investment spending just six months into the 3-year plan. The management allocation, however, may be split between additional growth capex and capital return as desired.

{kind=link}

Over time, these investments suggest Mitsui will become a less commodity-depended company, but the transition will be slow due to the size of the resource-based businesses. The stability in commodity price so far this fiscal year provides some safety for income investors.

For the current year, the higher-than-expected level of asset recycling produced gains on sale of ¥39 billion higher than the original plan. Some of the acquisitions also produced accounting gains when they became fully consolidated on the balance sheet because of the increase in Mitsui's stake. These gains were largely included in the original plan, however. Offsetting these are a few impairment losses. The largest ones resulted from the Chilean government's renegotiation of royalty agreements with foreign natural resource companies. This resulted in the impairment of a copper business and higher planned taxes, totaling over ¥19 billion. There were also impairments at Gestamp (a European auto parts supplier) and Mainstream (a renewable power company). Altogether, the improved outlook in asset recycling gains plus some positive mark-to-market investments in the base business is basically offset by the higher impairments. This leaves the exchange rate as the main driver of the increase in the profit forecast.

Valuation And Capital Management

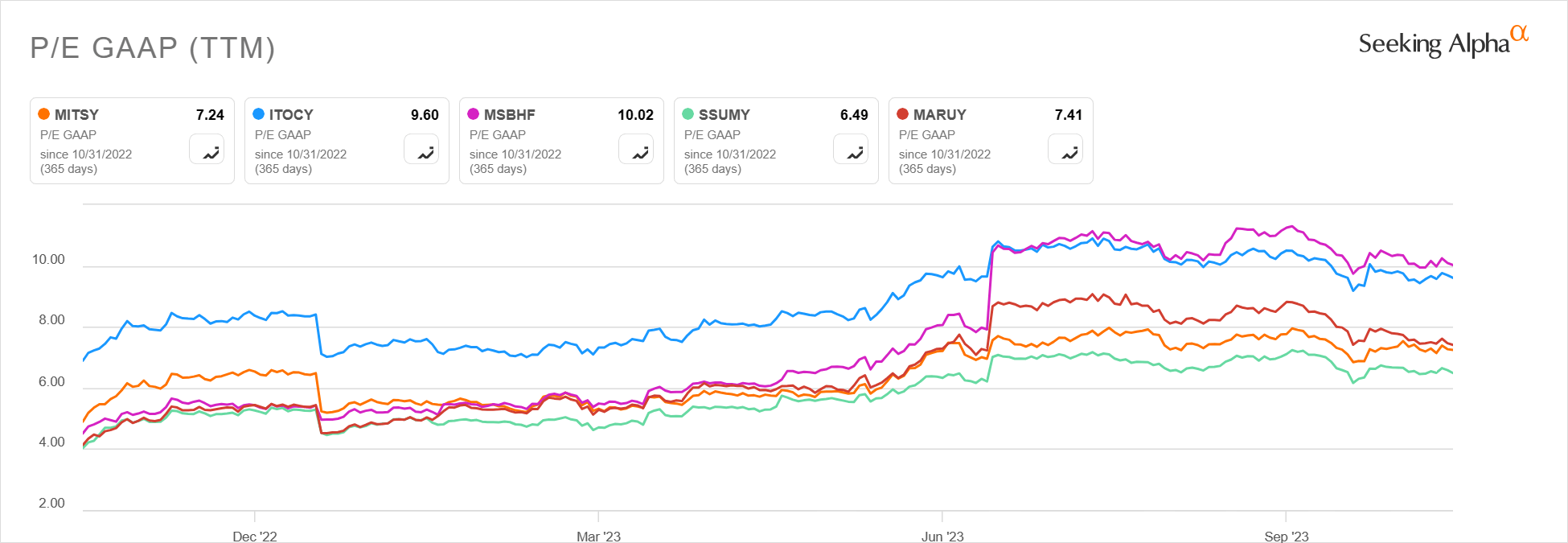

Mitsui shares in Tokyo have increased 27% since my article 6 months ago and closed at ¥5417 on the day of the earnings release. At that price, shares are 8.7 times the FY 2024 forecast. On a trailing P/E basis, Mitsui is now the second cheapest of the 5 trading companies.

{kind=link}

On a price/book basis, Mitsui is right in the middle of the pack at 1.16.

Mitsui's ¥170 full year dividend results in a yield of 3.1%. Compared to last year's actual dividend of ¥140, dividend growth is a strong 21.4%. For US-based shareholders, that even offsets the ~15% decline in the USD/JPY exchange rate.

The 2024 dividend is 27.3% of the new EPS forecast of ¥622.39 and will use ¥256 billion in cash. Mitsui has also completed ¥70 billion worth of buybacks this year and announced another ¥50 billion with 2H earnings. The resulting ¥376 billion of capital return this year is 39.1% of the latest operating cash flow forecast of ¥960 billion. This is slightly ahead of the 3-year plan target of 37%.

{kind=link}

Since the start of the fiscal year, debt is basically unchanged at ¥4.6 trillion, while cash is down ¥0.2 trillion to ¥1.2 trillion. The resulting net debt of ¥3.4 trillion is 0.48 times equity of ¥7.1 trillion. That represents a slight improvement in the debt/equity ratio from 0.50 at the start of the fiscal year.

Conclusion

Mitsui's 1H results set the tone for the Japanese trading companies. Unlike in recent years, commodity prices have been more stable and are not a big driver of changes in the profit forecast for the year. The weaker yen was the most significant driver of the improved forecast. In the week ahead, I would expect the other trading companies to issue similar forecasts with their 1H results.

Looking more closely at company-specific results, Mitsui is actively pursuing its new 3-year plan with an above-average amount of asset sales and acquisitions. These may not move the needle much on overall operating earnings, but the resulting gains on sale and revaluations have been positive. Unfortunately, these have been offset by some impairments, in particular due to Chile's new natural resource royalty policies.

Mitsui is now valued in the middle of the pack on price/book and is second cheapest on forward P/E. The announced dividend increase at least compensates foreign shareholders for the weaker exchange rate. When added to the increased buybacks, Mitsui is meeting its commitment to return 37% of core operating cash flow to shareholders.

Considering the increase in the shares (even in USD terms) since my last article and the possibility of the yen strengthening or commodities weakening in a slower economy, I am changing my rating on Mitsui to Hold from Buy. Nevertheless, the dividend looks safe and management appears committed to returning capital to shareholders. Therefore, current holders are being paid to wait for clearer skies.

For further details see:

Mitsui & Co.: Resiliency In A Tough Commodity Environment (Rating Downgrade)