MITSY - Mitsui Is Undervalued And Set To Climb Against Weakened Yen

2023-09-27 10:20:40 ET

Summary

- The article focuses on investment opportunities in Japan, specifically in Mitsui & Co, one of the world's largest conglomerates with a market cap of $57 billion.

- I conduct a deep analysis of Mitsui, examining its operational advantages, efficiency, core divisions, macroeconomic factors, valuation, and risks.

- Despite slowing revenue growth, I see Mitsui as a stable investment due to its tactful capital allocation, management of expenditures, increasing operating income and low valuation.

Introduction

Mitsui (MITSY) is one of the most stable investments operated from Japan at the time of this writing, and even against a weakened yen and Japanese macroeconomic uncertainty, the stock is trading well below value and has a wide global and industry diversification to secure future profits.

Mitsui is one of the largest conglomerates (or horizontal keiretsu: a diverse business linked by a central bank or trading company) in the world, has a market cap of $57 billion and ranks 14th in Japan on this metric at the time of this writing.

My article does a deep company analysis of fundamental factors, including operational advantages, efficiency and core divisions perspectives. This is balanced by a macroeconomic analysis of Japan's economy that relates it to other major investment countries, and how this may affect Mitsui's stock in the future. I analyse the risks associated with owning the stock and my discussion of valuation will detail what I think Mitsui is worth intrinsically given the full perspective of micro and macro-economic factors.

Company Analysis

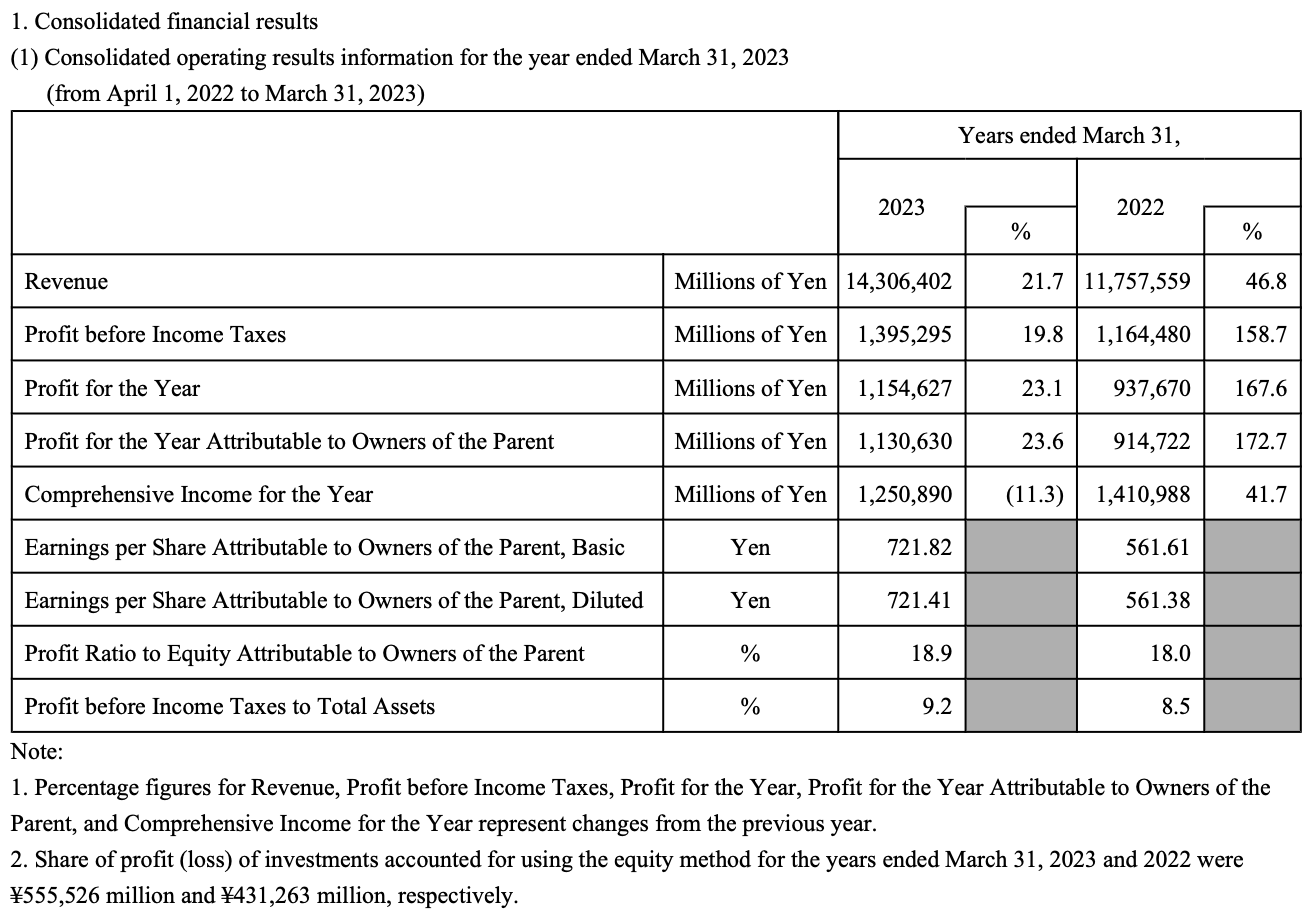

Revenue & Profit

Mitsui shows good revenue growth from FY 2022 to 2023, showing short-term momentum that supports longer-term growth. However, revenue growth is slowing; although this isn't an issue for long-term shareholders more focused on stability, it signals an ever-increasing stalwart nature to the conglomerate.

{kind=link}

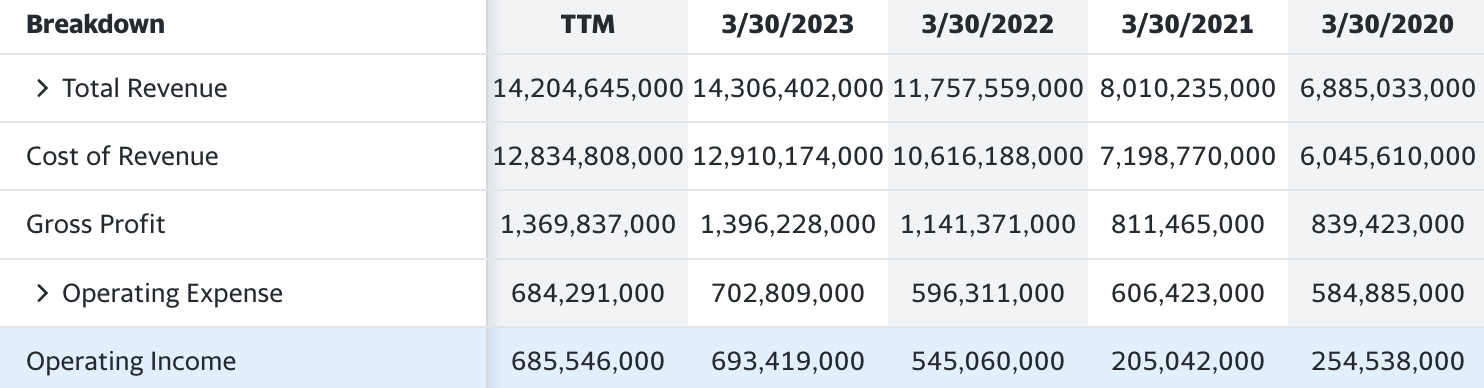

Gross profit is healthily increasing in line with revenue growth, showing tactful allocation of capital and management of expenditures. Perhaps most significant to demonstrate this is how the company is increasing operating income, which has seen a considerably larger percentage increase YoY compared to gross profit and total revenue. For example, total revenue has increased by 206% since 2020 and operating income has increased by 269%.

{kind=link}

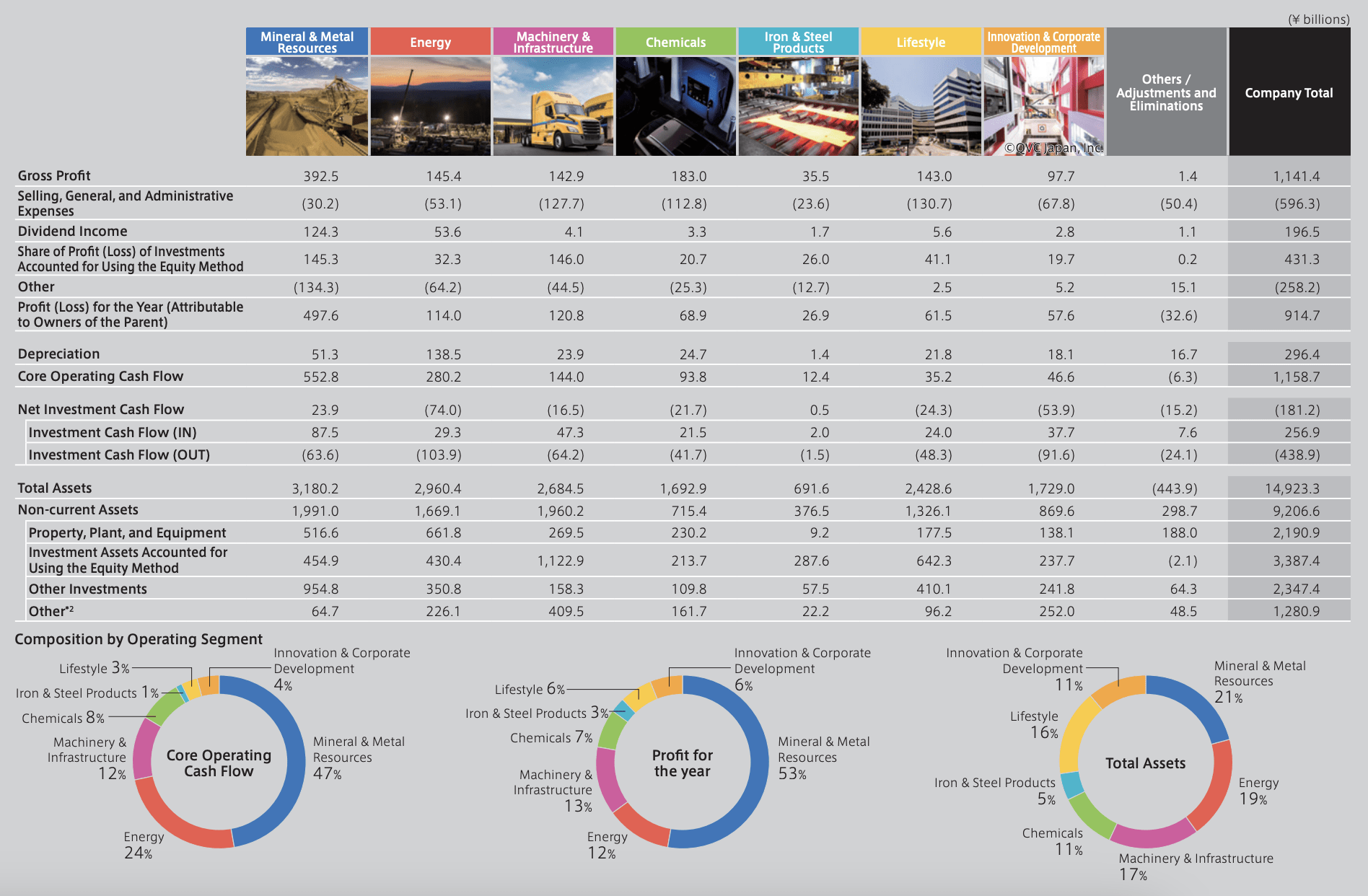

Dominant Markets

Zooming out from a foundational analysis of revenue and gross profit growth, the revenue is coming from 7 dominant markets . Mineral and metal resources are Mitsui's largest income generator. This sector also has minimal SG&A expenses in comparison to, for instance, lifestyle, which has a huge 130.7 billion yen expense as opposed to a 143.0 billion yen gross profit. The mineral & metal resources expenses are large given the nature of the work but are listed under 'other' expenses, totalling 134.3 billion yen against a 392.5 billion yen gross profit. Mitsui's focus on this sector, which harnesses less than 10% SG&A expense and a healthy 'other' expense component, indicates a continued focus on operating efficiency overall.

FY Ending March 2022. (Mitsui)

{kind=link}

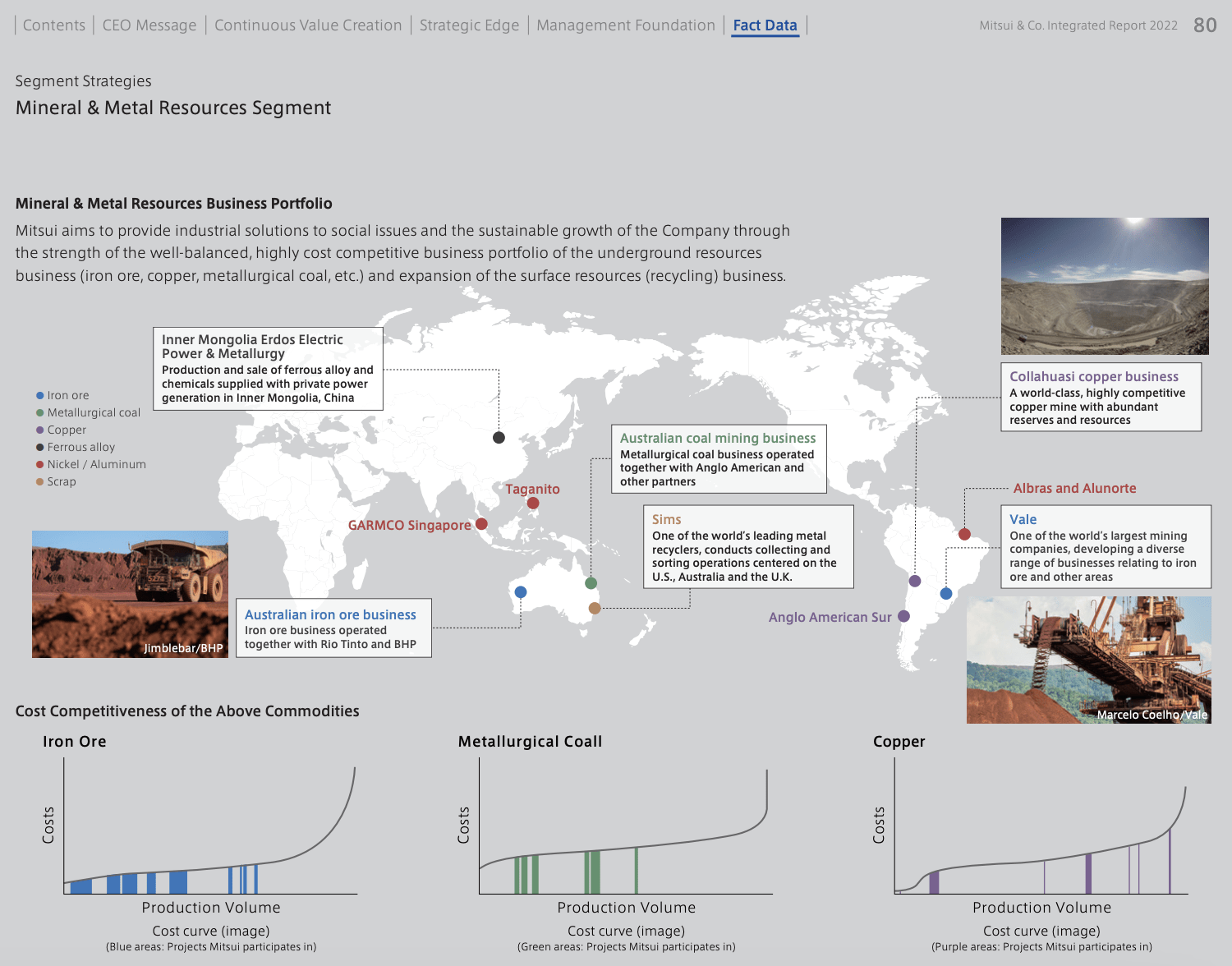

I am particularly interested to see how Mitsui continues to maximise profit by stressing efficiency. There are risks associated with the mineral and metal resources sector. In particular, as is noted in Mitsui's 2022 integrated fact data report , supply, demand and price issues are likely, due to a transition to a low-carbon economy, as well as supply chain issues from geopolitical risks and lingering COVID-19 effects.

Looking at the mineral and metal resources sector portfolio on page 4 of the fact data report, I have noticed particular safety nets that reinforce the business and keep it safe from geopolitical risks. In particular, Mitsui does not have mineral and metal resources operations in Russia, which creates certainty around geopolitical tensions regarding the Ukraine war. The operations are in Asia, Australia and South America, which creates a level of diversification that acts as a security net whilst not becoming too diluted, with each material having its own global segment of operation.

{kind=link}

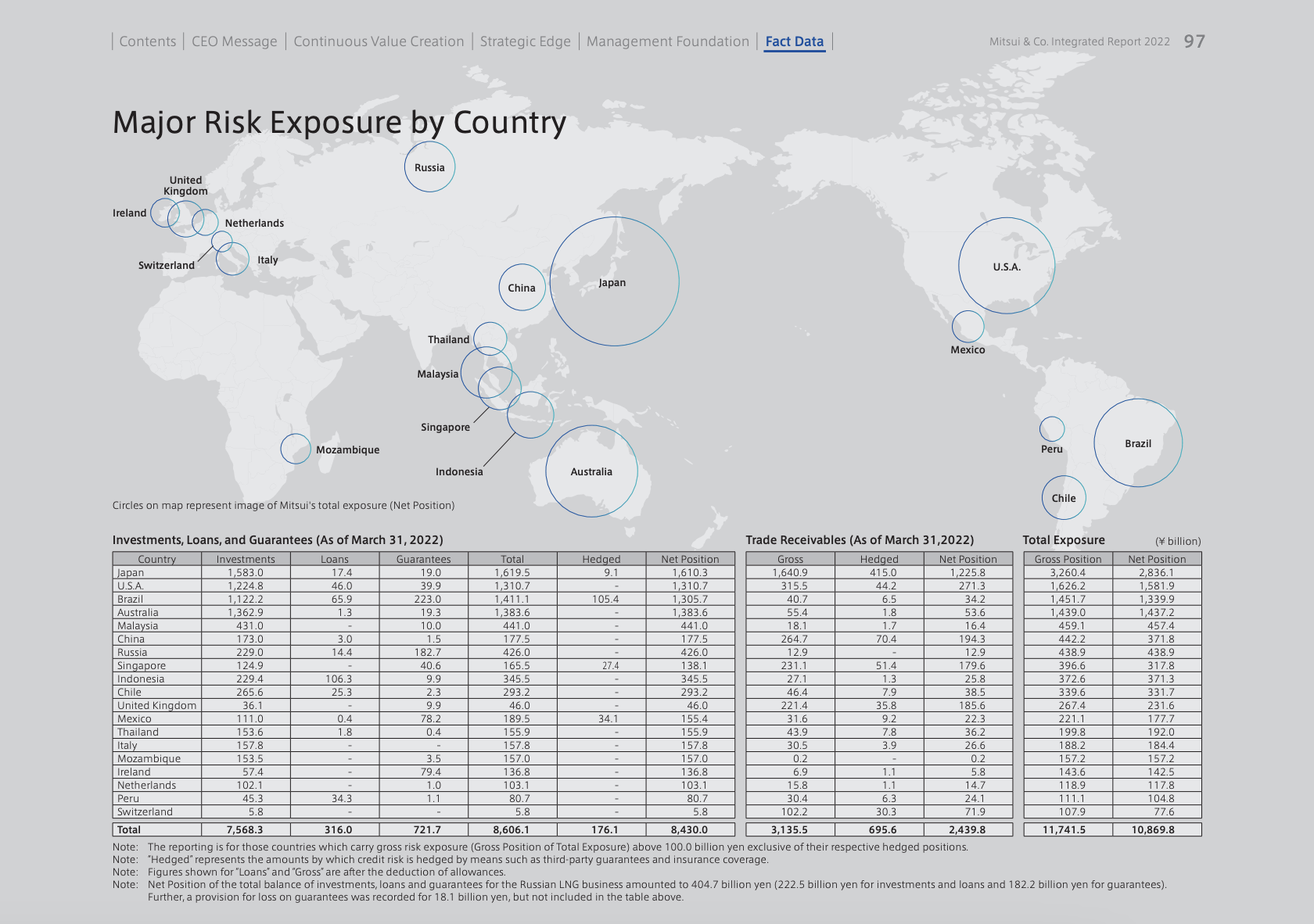

Global Risk Exposure

If we look at the major risk exposure by country, however, we can see the risk associated with Russia due to a current 229 billion yen investment in operations in the country. That being said, this only makes up 3% of the total investment pool and so remains an insignificant concern. The largest exposure is in Japan but is only 21% of the entire investment pool. The USA comes third, with an exposure of 16%, providing a large kickback from U.S. economics.

{kind=link}

Macroeconomic Analysis

When analysing the macroeconomic impact of Japanese economics on Mitsui I have heavily considered that exposure to the company means exposure to a web of global industries with dominant weighting in Japan, the USA, Brazil & Australia.

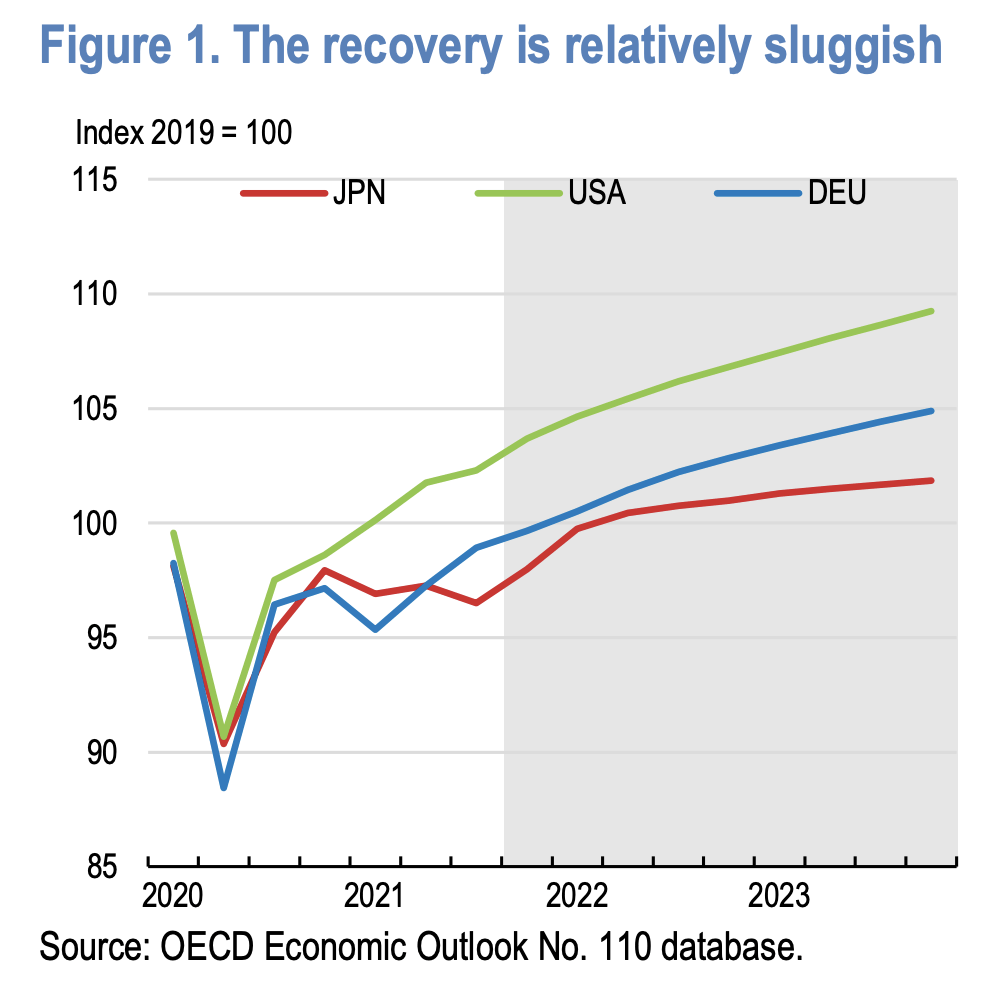

Japanese Economics

The effect of COVID-19 should be noted on Japan's slow recovery in comparison to the USA. The OECD 2021 survey on Japan recognises this issue but notes gaining momentum following a heavy hit by the virus.

OECD Japan 2021 Economic Survey

{kind=link}

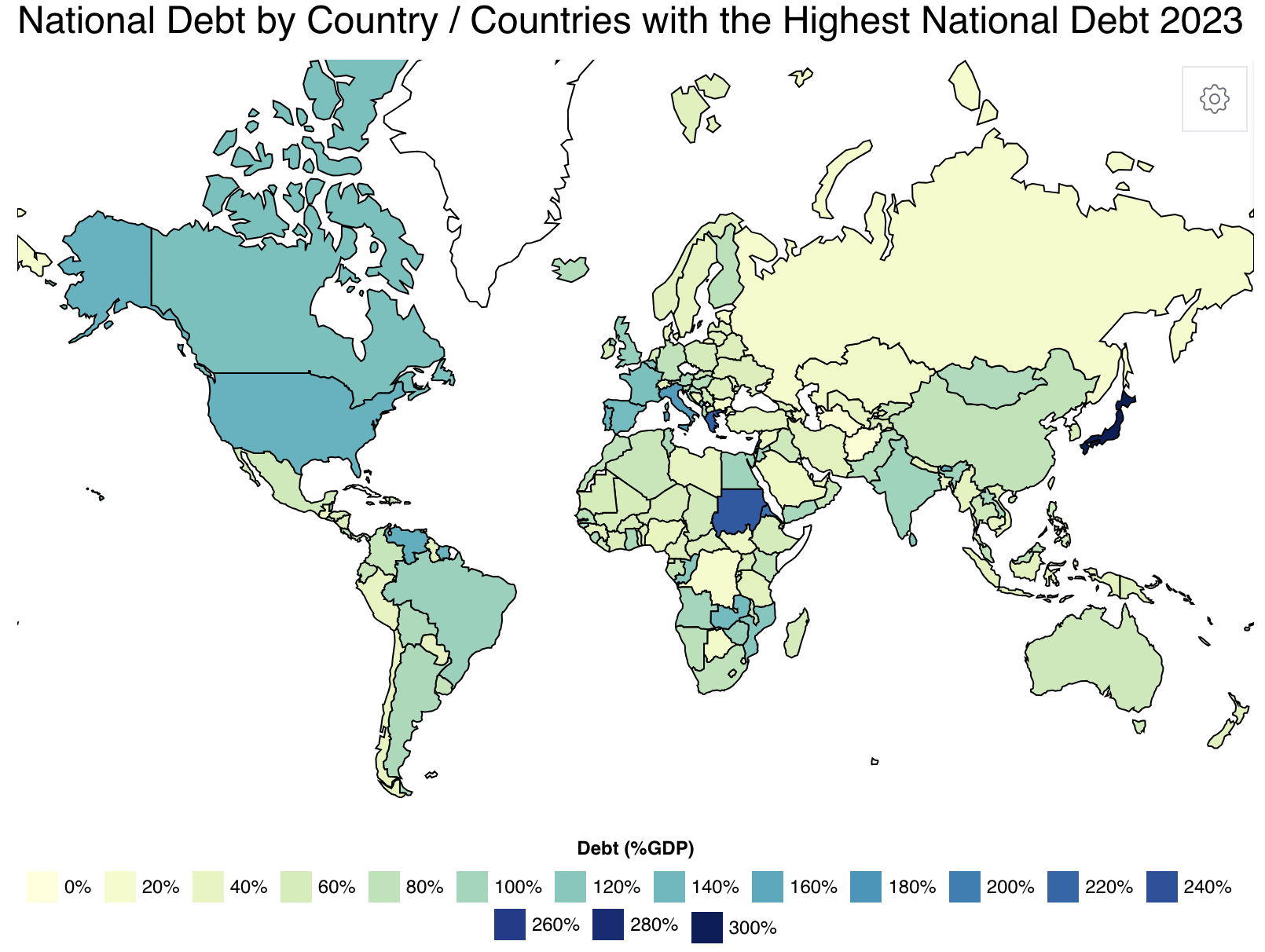

The debt situation in Japan as a percentage of GDP is relatively unbearable and is the least attractive aspect of Japanese macroeconomics for investors. The overall debt was exacerbated by COVID-19 as seen in 2019's new peak level.

OECD 2021 Report on Japan

The outlook is not positive for Japan on this front. Japan has the highest debt as a percentage of GDP in the world.

{kind=link}

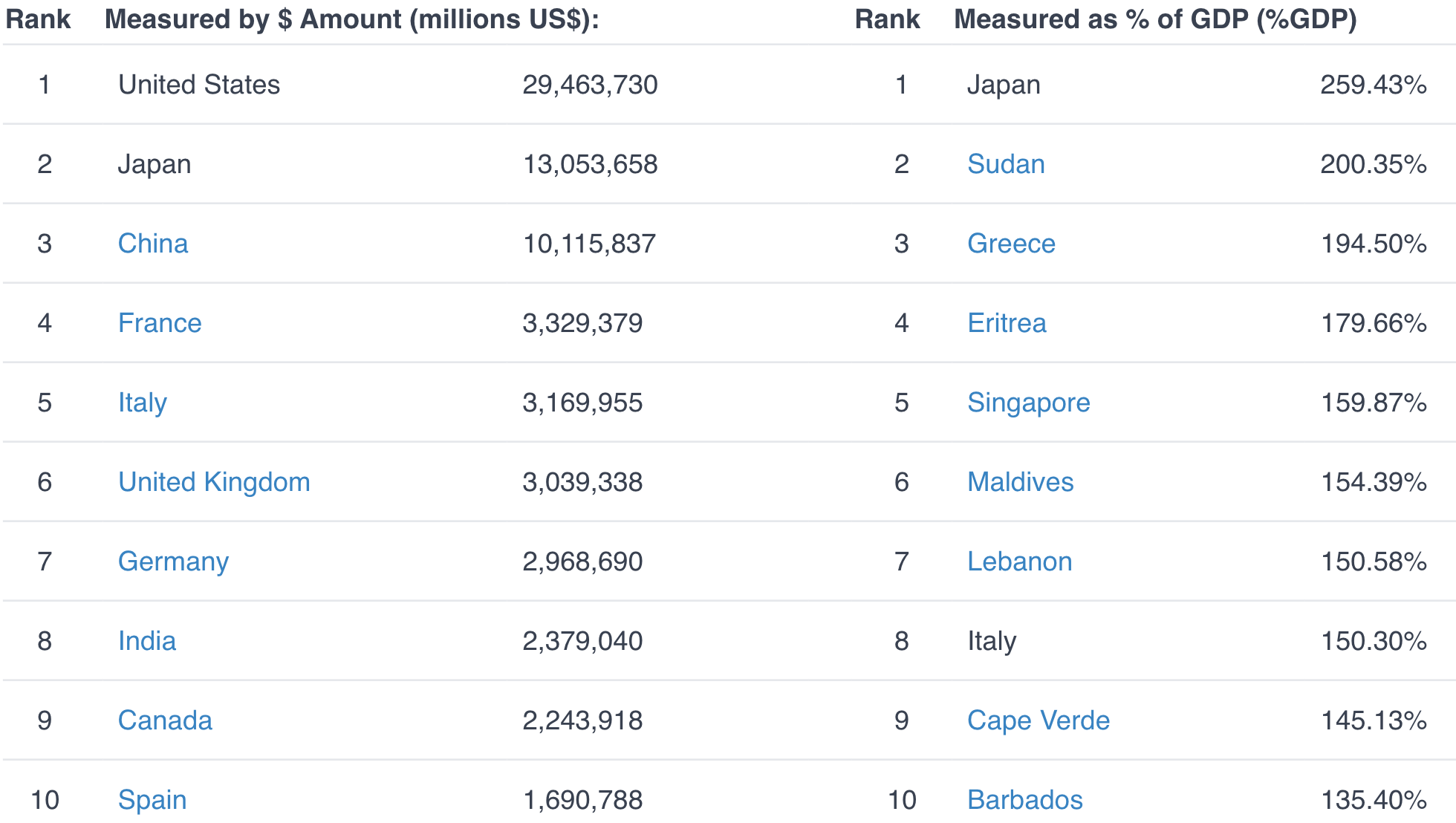

If we look at the top 10 countries ranked by debt amount, Japan is at number 2. If we analyse the debt as a percentage of GDP, Japan is number 1, by a considerable 59.08%. Sudan has better debt-to-GDP than the world's third-largest economy, Japan.

{kind=link}

The problem here for Japan is not the level of debt, but the debt as a percentage of GDP. It creates uncertainty for me as an investor who is concerned about the country not using its debt effectively and transferring poor performance to Mitsui in turn—although the relationship between Japan's immediate macroeconomic environment and Mitsui is balanced by its global investment portfolio.

Global Diversification as a Traditional Security Net

Mitsui's global portfolio of investments makes it more secure than if its operations were based solely in Japanese territory. This conglomerate nature of Mitsui is attractive and is exactly why Mitsui is a fantastic long-term holding for me as an investor looking for security and exposure to Japan. The question is 'Why exposure to Japan?', 'Why Mitsui at all, when there are much stronger companies in the U.S.?'

It is much better to look at Mitsui as a global conglomerate founded and operated in Japan than a Japanese company. It spans multiple fields of business, with similarities to Amazon (AMZN), LVMH (LVMHF) (EPA:MC.PA) and Berkshire Hathaway (BRK.A) (BRK.B). The core difference is that Mitsui has a much larger global diversification; hence, we are looking at increased security using traditional diversification. That being said, I know that means lower long-term returns, but that's exactly what I see in Mitsui shares: stability and safe profits.

Valuation

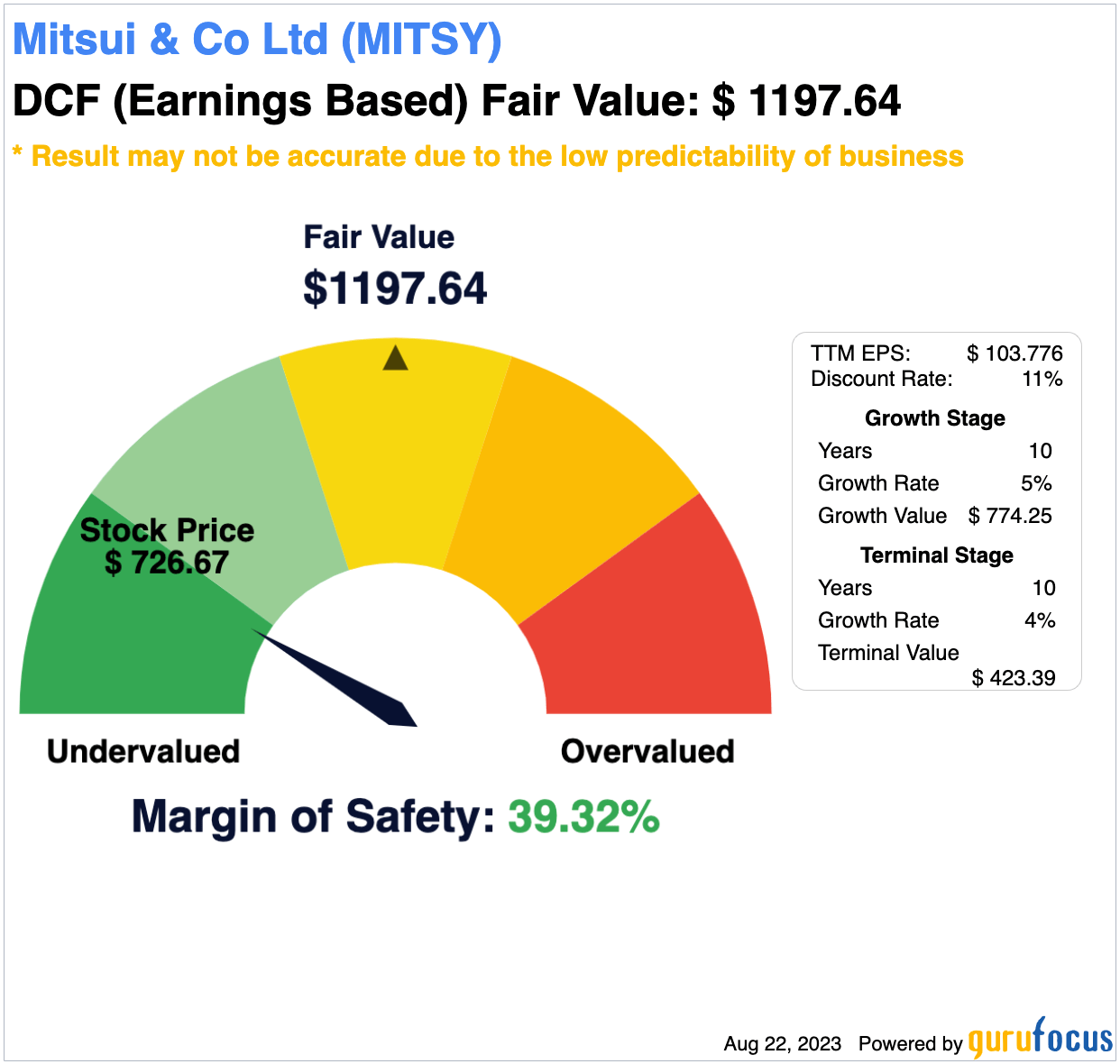

I have to come to some conclusion about what is a fair price for the company and that isn't always necessarily clear. With a PE ratio of 7.9 and a market cap of 8.6 trillion yen at the time of this writing, I am certain I am not overpaying for Mitsui and I am getting it at the moment below value. The risk profile is favourable given global and industry diversification with a weakened local macroeconomic background as discussed, and there are continued exceptional returns and increasing efficiencies in its core business components.

I've checked for DCF calculations that are earnings-based and found a stellar margin of safety of 39.32% for Mitsui at the time of analysis, which is a good indicator that my micro-and-macro-economic analysis of the stock is on base from a DCF standpoint. I would say the fair value is slightly above this estimate, but I wouldn't pay more than around $ 1,000 per share at the moment due to the lower-growth future recent income statements are signalling.

{kind=link}

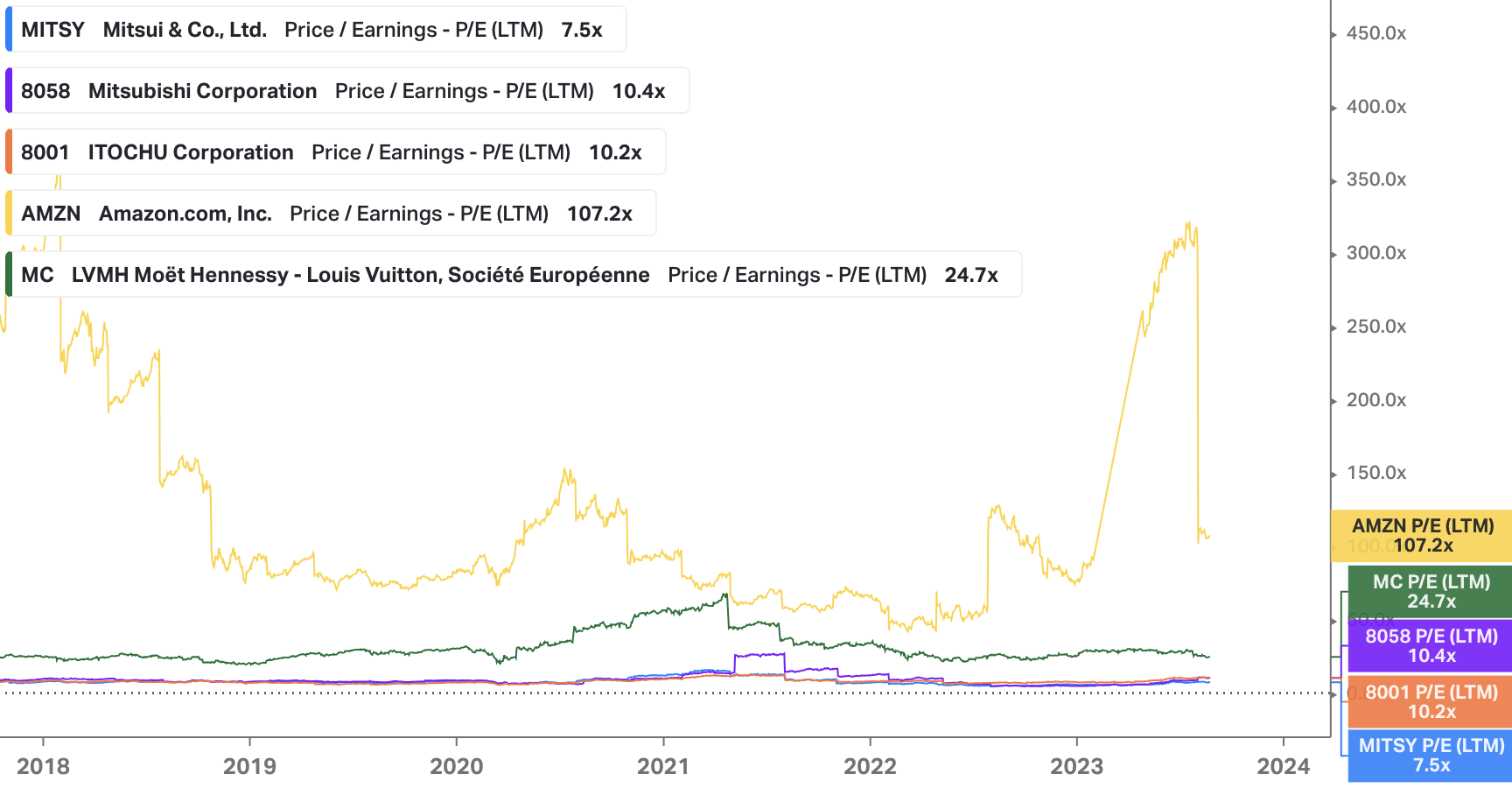

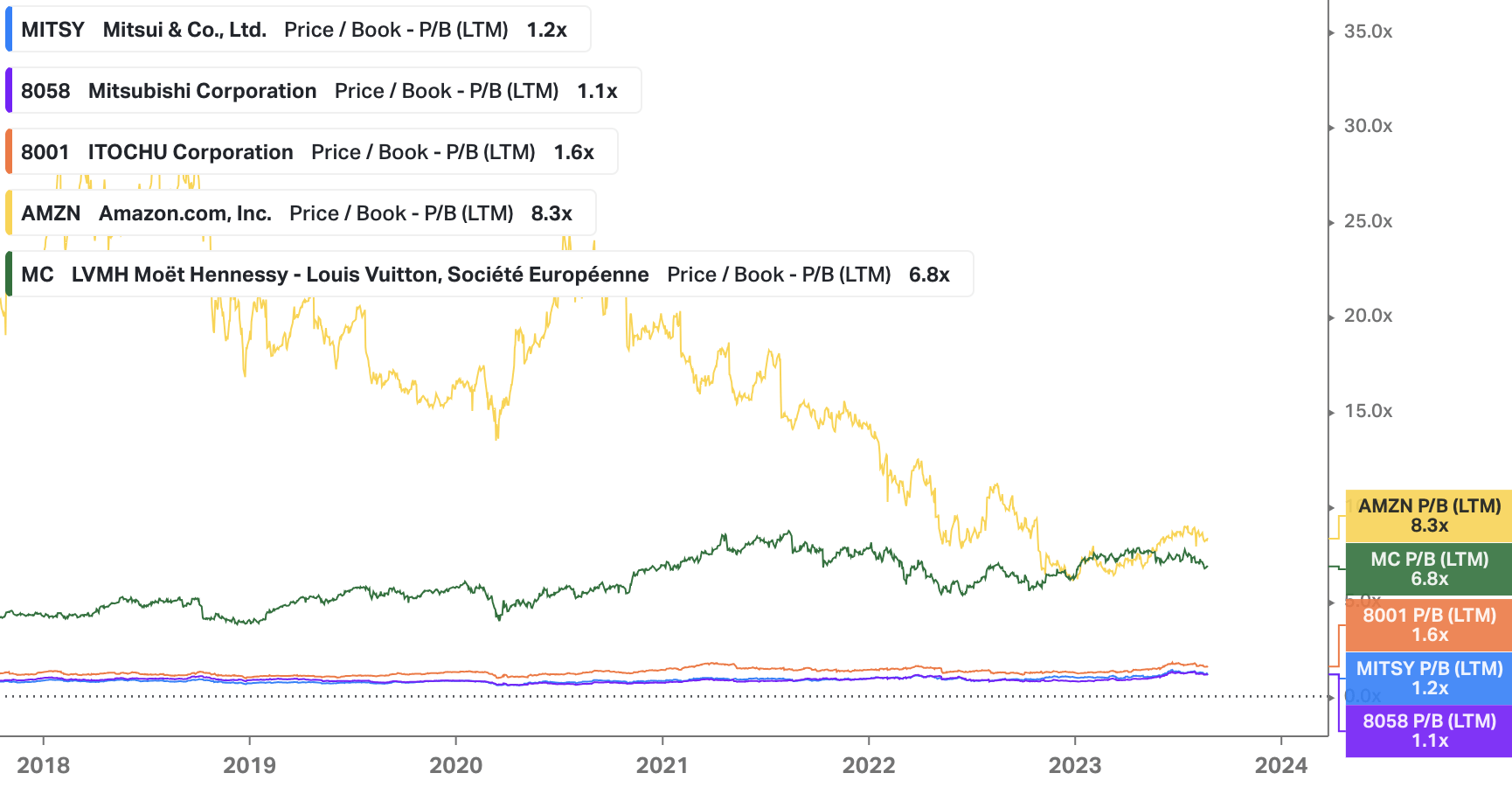

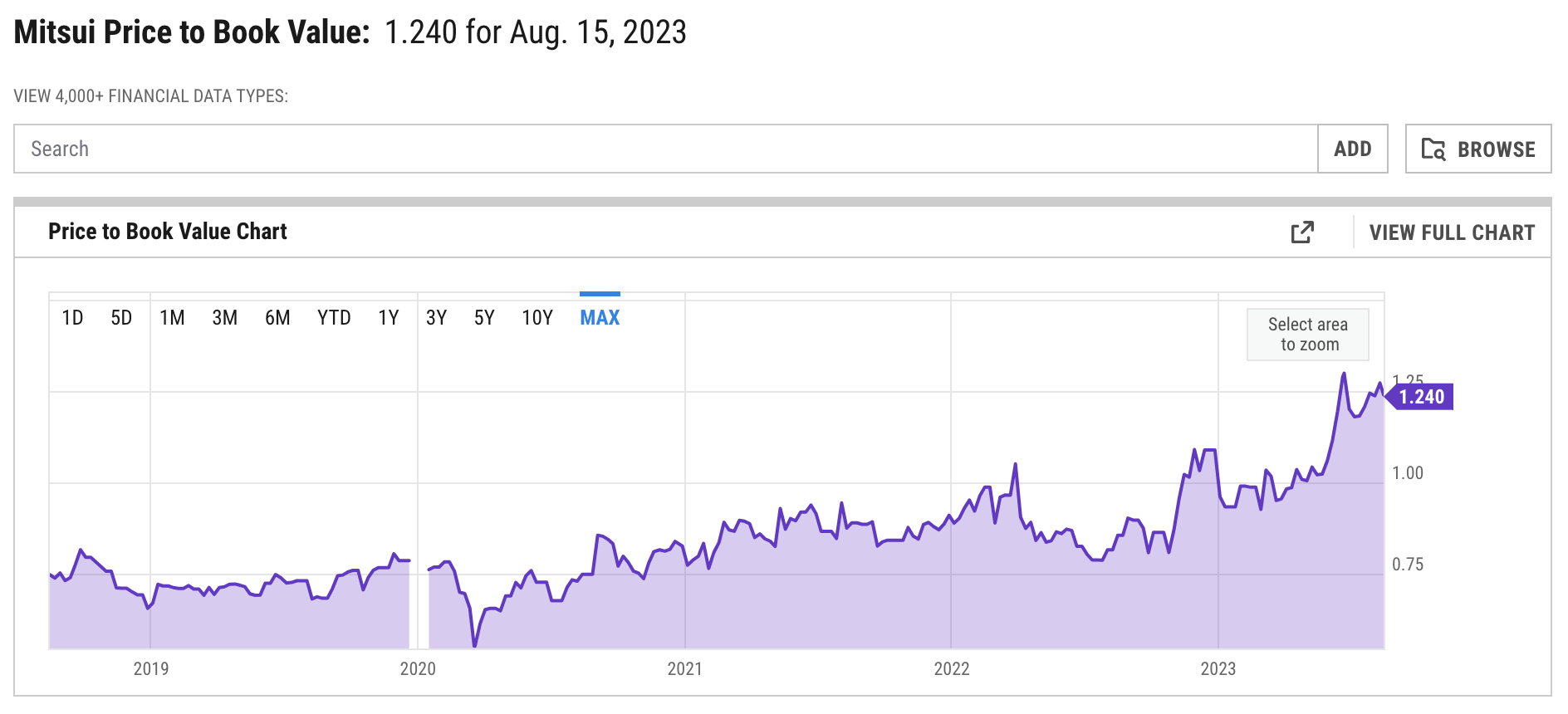

I have cross-referenced Mitsui against Mitsibushi, Itochu and Amazon to get some idea of the price to earnings and price to book in the Japanese region and against a successful Western conglomerate.

Price to Earnings Comparison (Koyfin) Price to Book Comparison (Koyfin)

{kind=link}

{kind=link}

From these charts, it is evident that Japanese companies in general are well undervalued in comparison to Western counterparts like Amazon and LVMH. Mitsui has the lowest P/E ratio of the group and almost joint lowest P/B ratio at the time of analysis, which makes it healthy even relative to its Japanese competitors.

People are beginning to pick up on undervaluation in Japanese businesses. That is why as an investor I see Mitsui as a company to act on now, before the herd.

{kind=link}

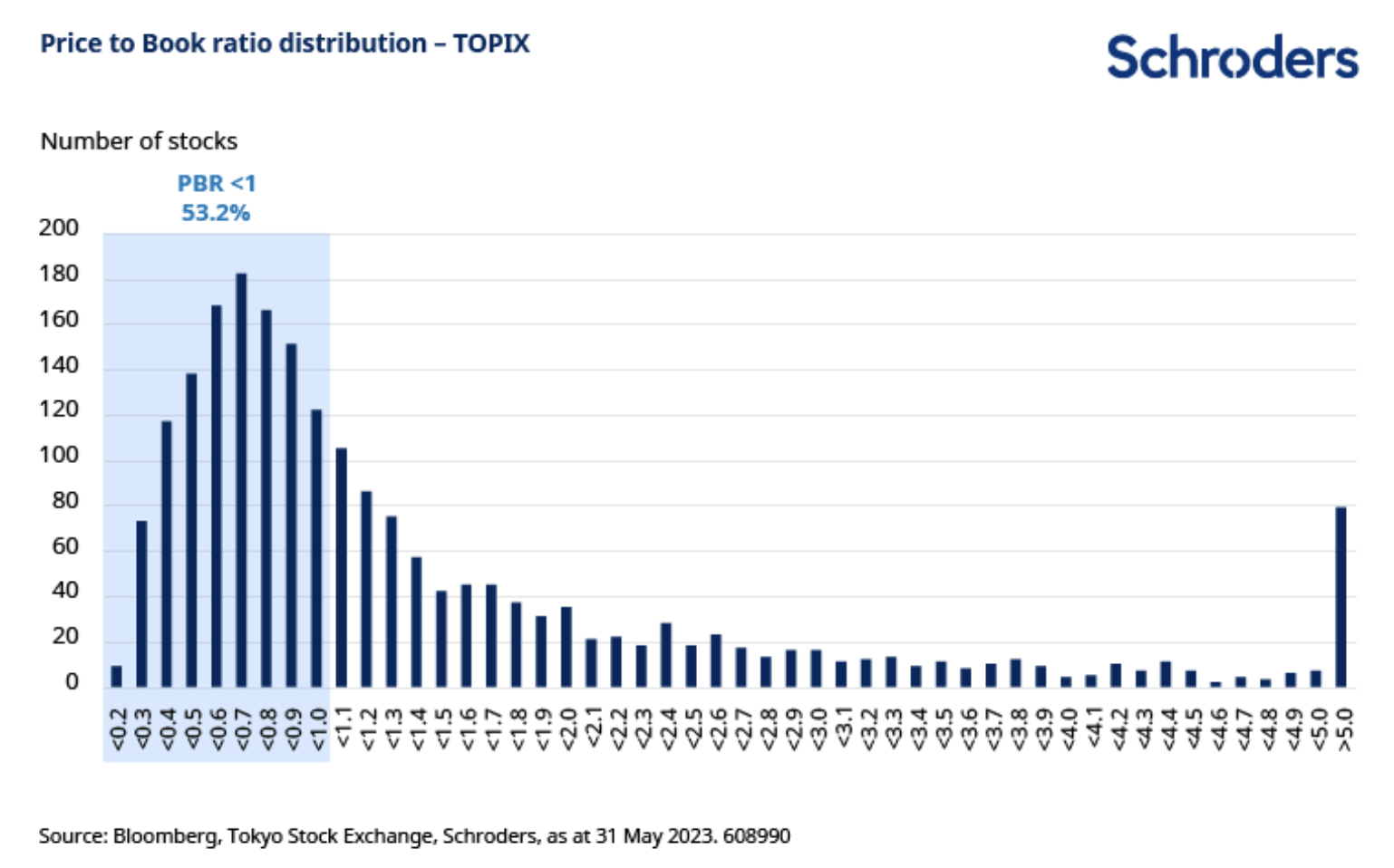

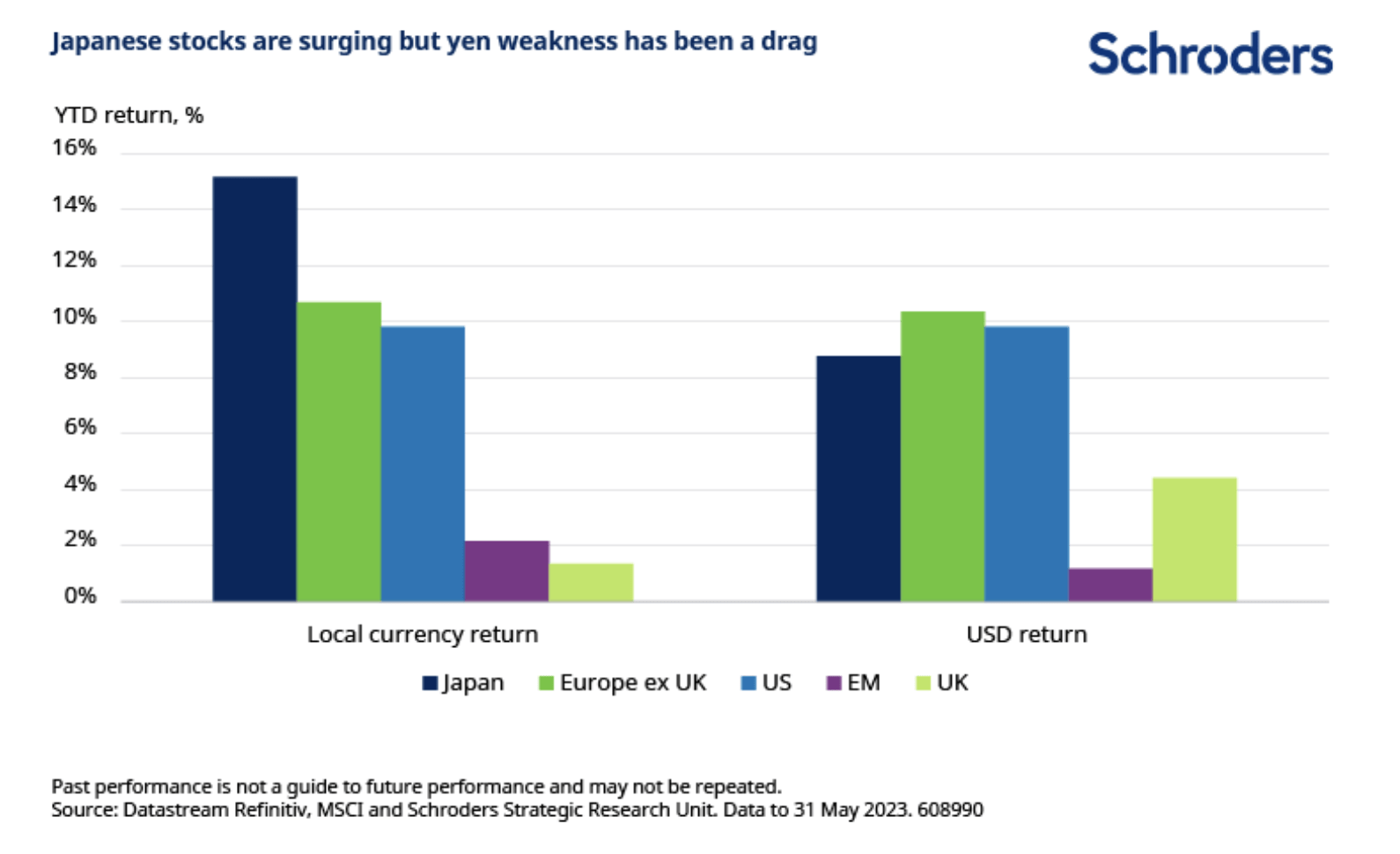

I found an interesting graph from Schroders, which outlines the favourable nature of Japanese companies and how the yen is dragging the stock returns down for international investors.

{kind=link}

The Schroders article depicting this graph is interesting in its description of many Japanese shares currently being valued at below book value, which screams opportunity for me as a value investor. The global markets are being slow to pick up on this and I need to be careful about the companies I pick. If companies are being valued poorly in Japan, I need to be wise enough to discern which companies are being valued incorrectly. With a conglomerate like Mitsui, there is less risk—the organisation is entrenched globally, and I'm not buying a potentially demising enterprise.

{kind=link}

Recent Earnings

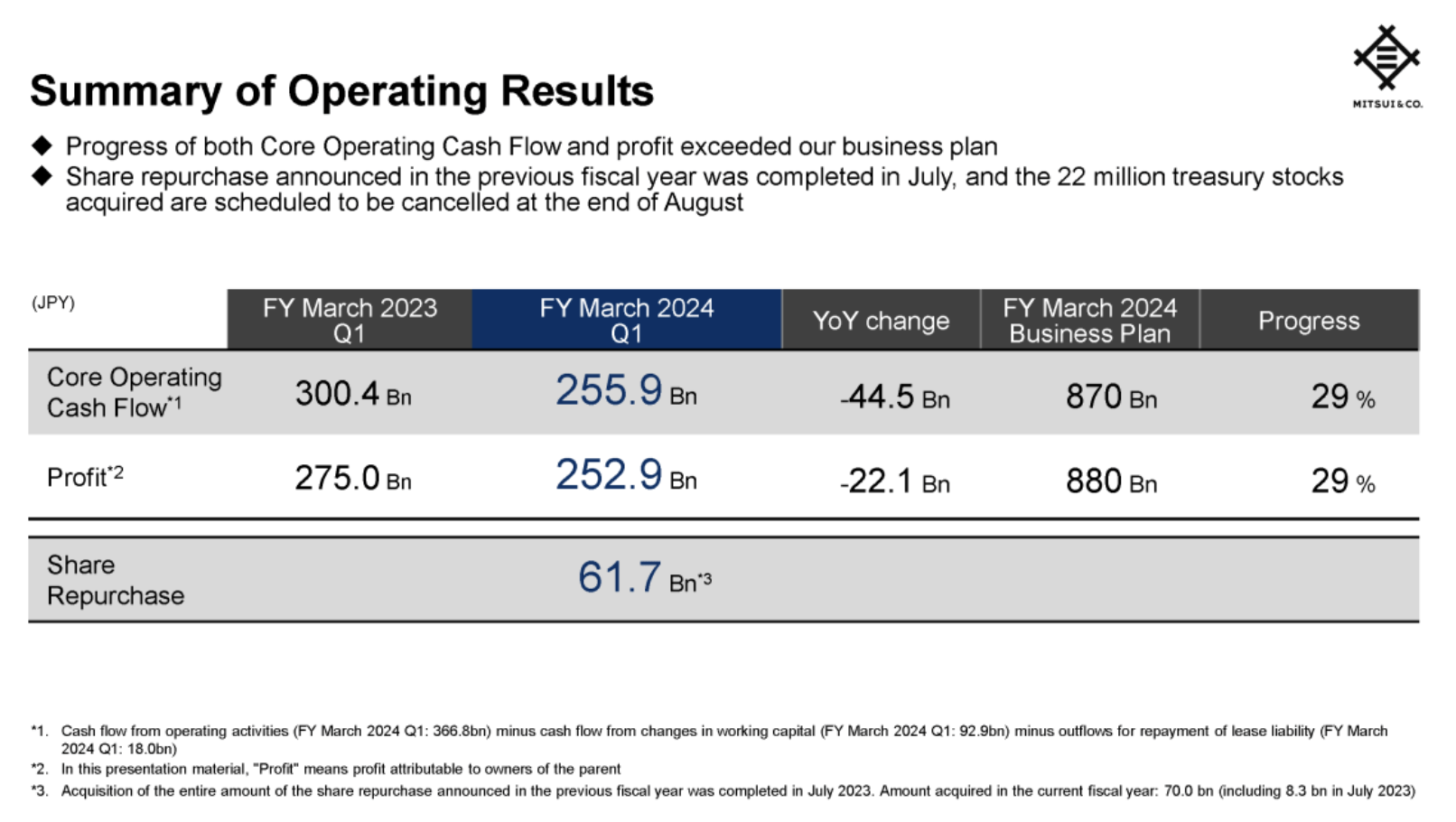

Q1 financial results for FY March 2024 were good but did show a reduction in core operating cash flow and profit, with a substantial share repurchase in Q1 2024, demonstrating a counterbalance of lowered operating income for the relative quarter with this financial measure to support stock growth.

{kind=link}

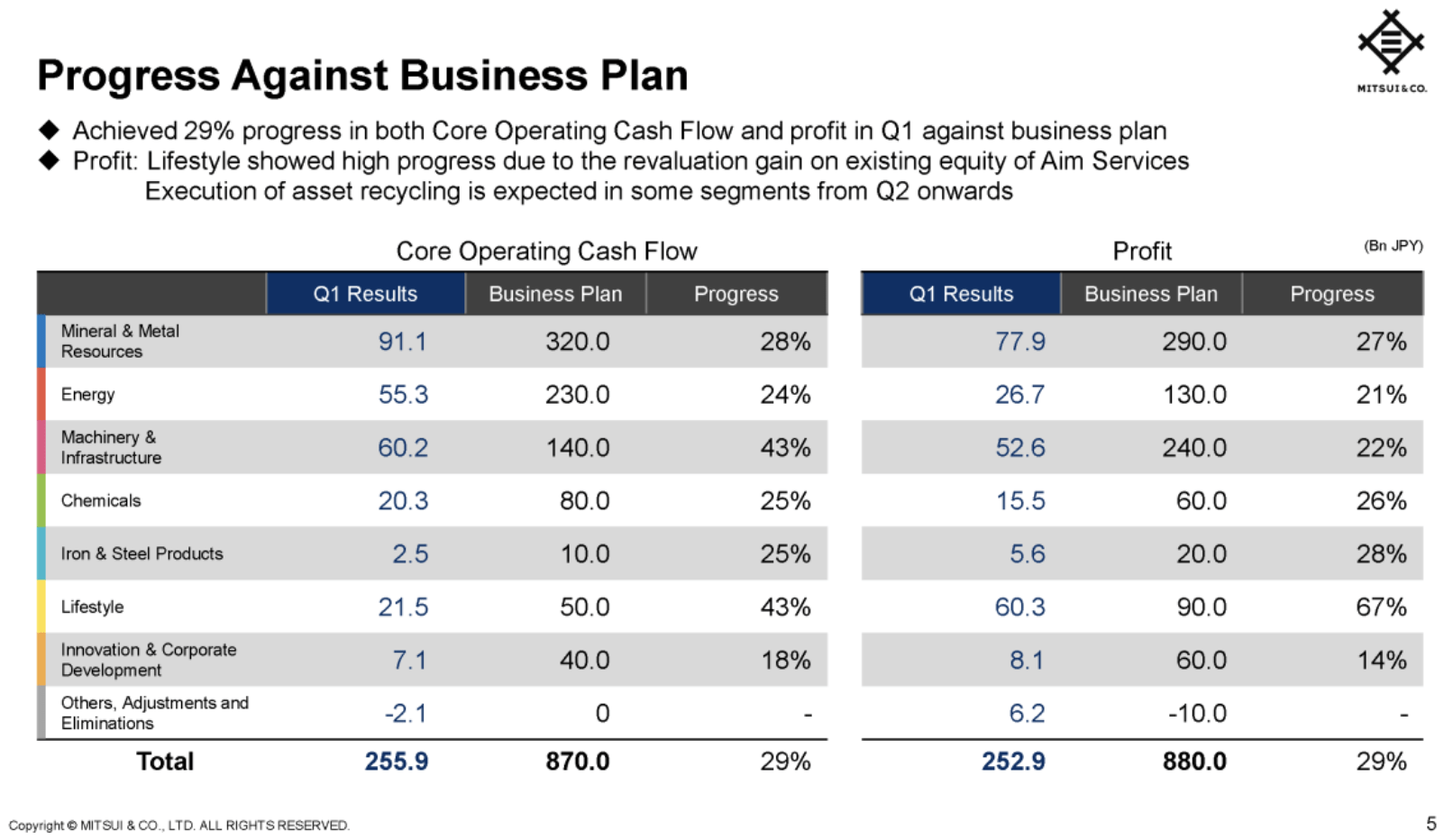

That being said, the company has mentioned that they are exceeding targets to hit their FY 2024 business plan, with machinery, infrastructure and lifestyle leading powerfully in Q1 on this measure, but lifestyle taking the lead dramatically in terms of profit in conjunction with core operating cash flow.

{kind=link}

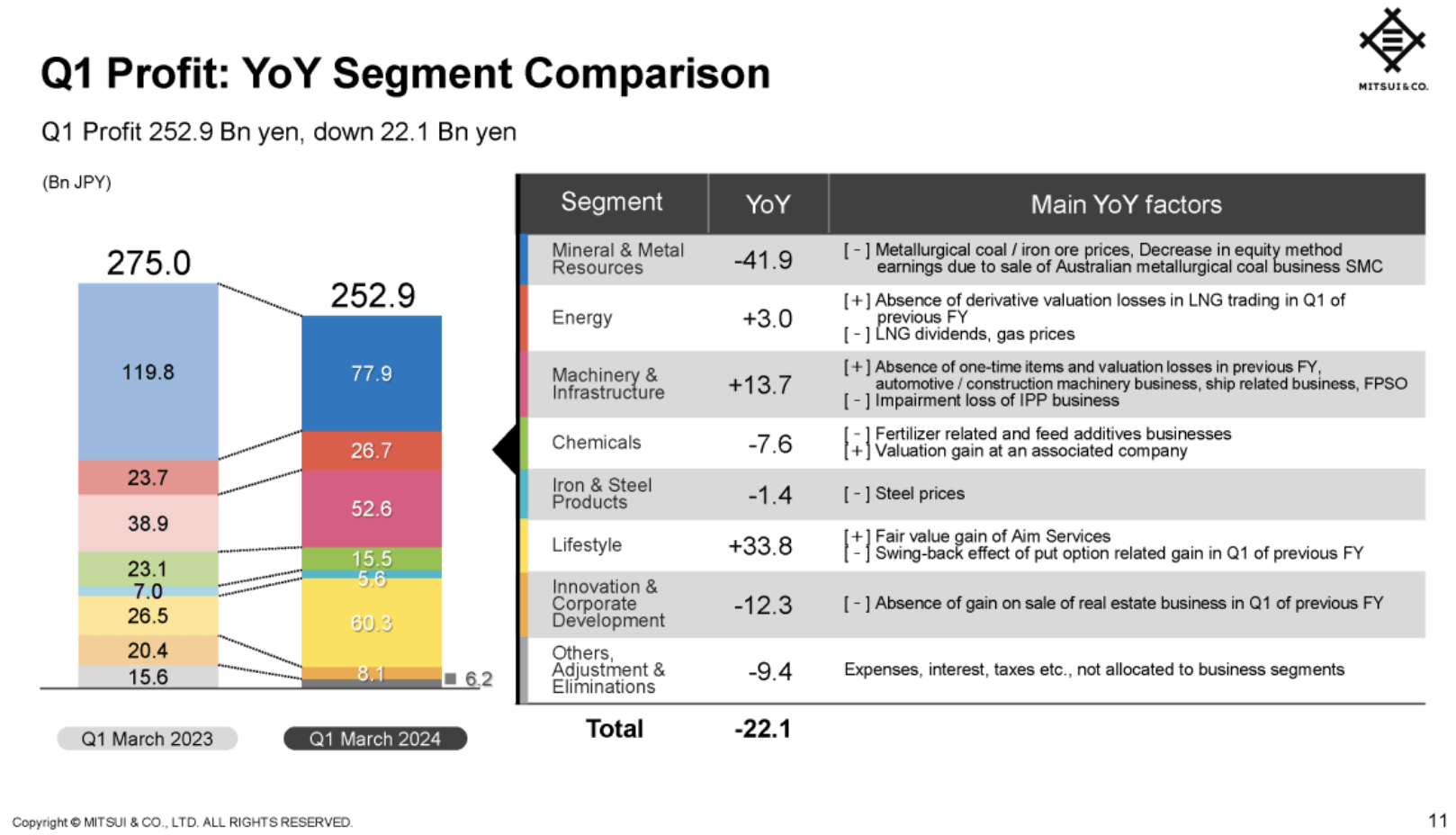

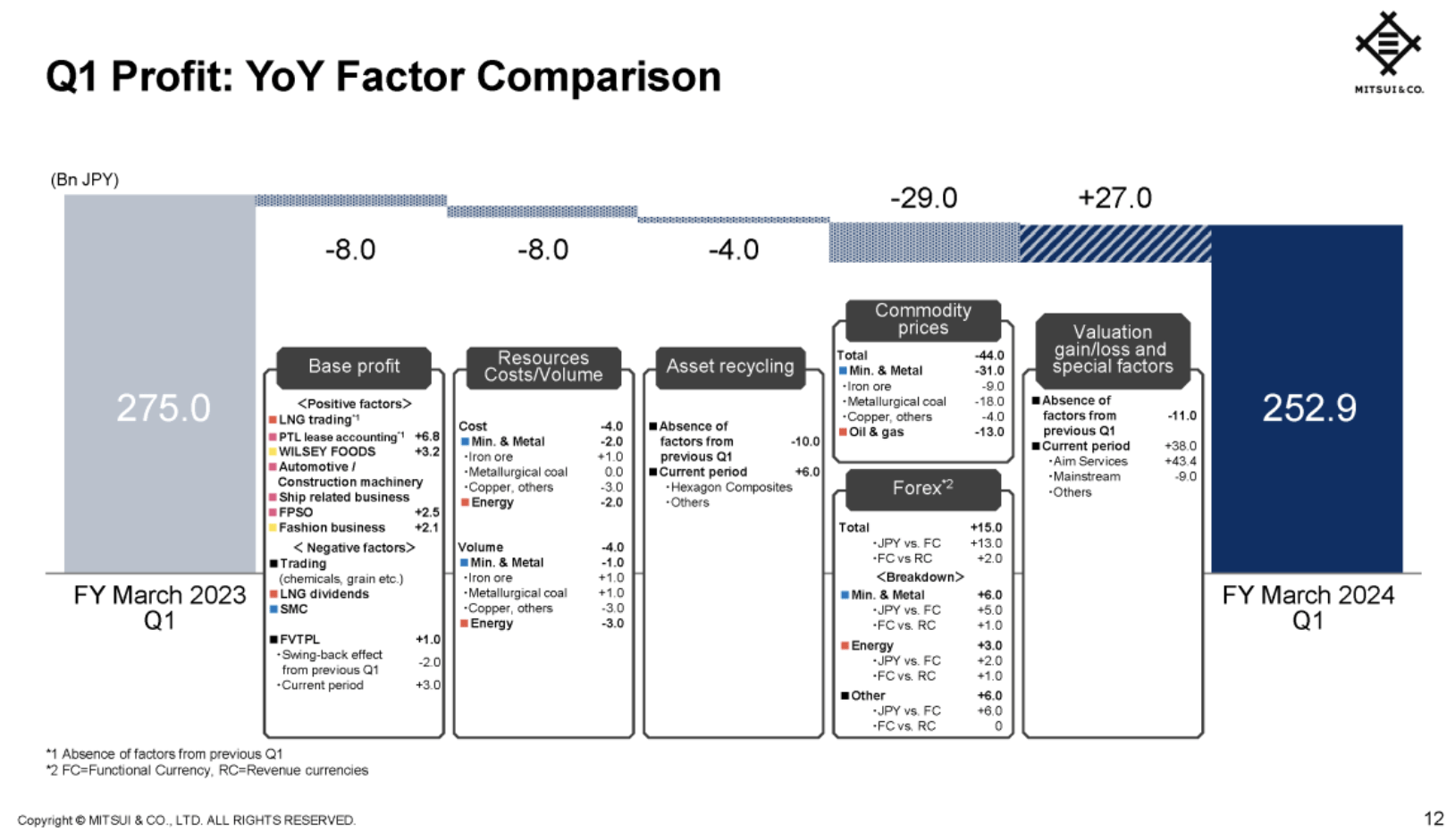

The IR Meeting on Three-Month Period Financial Results Ended June 30, 2023, which I have used to source this information on recent earnings displays powerful infographics such as the YoY Segment Comparison and YoY Factor Comparison for Q1 profit.

{kind=link}

{kind=link}

These results show that there are negative tailwinds, particularly in commodity prices, but forex advantages counterweight this to some degree. I am not concerned by the factors that have contributed to the overall profit decline for Q1 2024 vs. Q1 2023; the business at large is strong and base profit is only a marginal decrease in contrast to the commodity price disadvantages.

The stock price has had a sideways reaction thus far to these metrics, but I am not focused on the short-term reaction of this earnings report - the company stands to make the most profit for me as an investor on the long-term horizon, largely based on the valuation factors I have mentioned with continuing strong core business operations.

Risks

I see the risk profile of owning Mitsui as low at the time of this writing, primarily due to its global and industry diversification and the low valuation in comparison to Western similars. However, the largest concern remains the macroeconomic outlook of Mitsui's home country Japan.

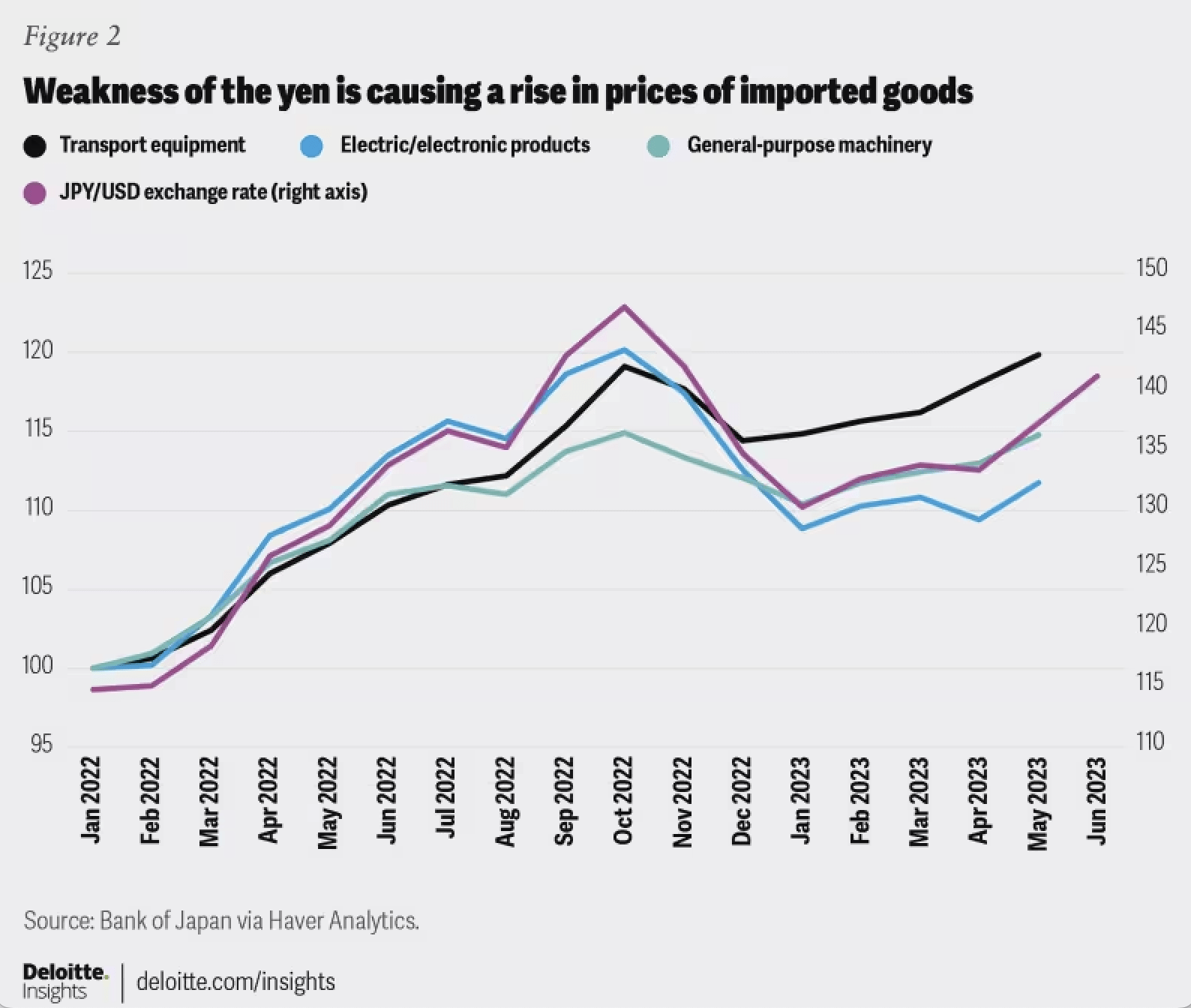

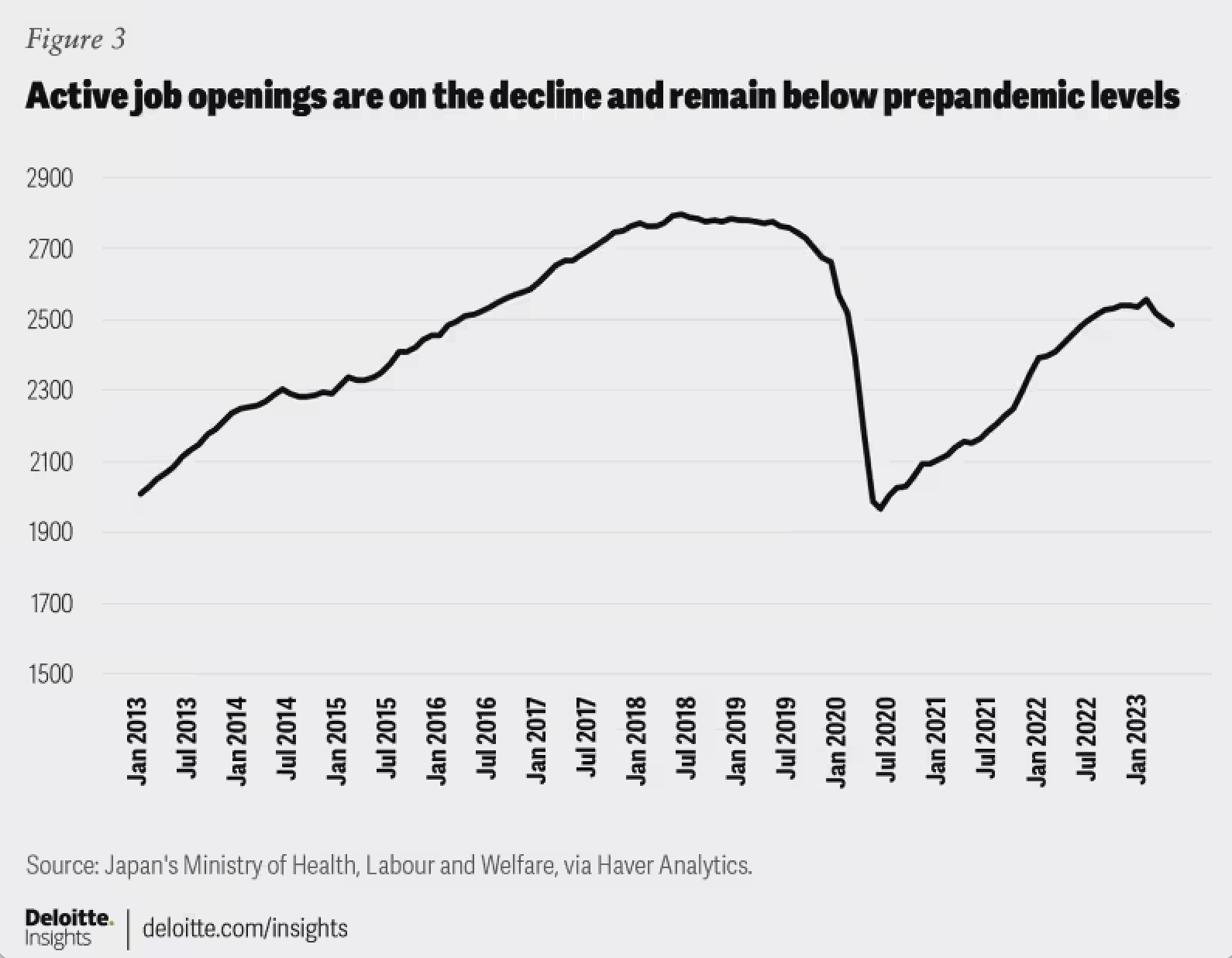

A Deloitte article I have used to research Japan's macroeconomics has shown the results of the weakening yen on imported goods prices, the highest level of inflation since 2001 and low active job openings.

{kind=link}

{kind=link}

There is opportunity here, however, due to depressed Japanese valuations as a result of consensus opinion on a stagnant national economy. This local disadvantage plays right into my hands as a Mitsui investor; I recently bought shares because I noticed the value play that gives me a large margin of safety based on the synergy between stellar business operations and lacklustre attention on Japanese stocks in general. Even better, the stock is well-secured by the global investment portfolio.

That being said, I have been careful not to overly allocate to Mitsui. Although I am not concerned about the Ukraine war affecting Mitsui stock, due to the country's sanctions against Russia and hence the support of Western economics and their large Western portfolio weighting, one of the largest risks would be the company realising unsubstantial returns in comparison to some U.S. companies. I think that is to be expected to some degree, but I like paying for the security that the company provides in giving me international diversification and the incredibly low valuation provides a great level of safety. I see Mitsui as a low-to-moderate risk investment with potential good-to-great returns. That, to me, is safer and better than a moderate-to-high-risk investment with very high return expectations, but equally high volatility and unfavourably high valuations, as is seen with AI companies, such as Advanced Micro Devices (AMD) - which I am thinking less favourably of right now.

Conclusion

Mitsui is an excellent long-term holding for my portfolio, especially because it is undervalued at the moment. The business operates efficiently and has an astute allocation amongst a diversified product and service set. While concerns related to the yen may bring the investment results down, it is counter-balanced by a global portfolio that Mitsui operates.

Given the quality of the company and its low valuation, I purchased shares in Mitsui as other opportunities did not persuade me more. My major concern is that the company is so large and established that it lacks traditional growth metrics that may be more compelling in smaller, newer, up-and-coming, undervalued Japanese companies. These opportunities I am sure to discuss in further analyses to come.

For further details see:

Mitsui Is Undervalued And Set To Climb Against Weakened Yen