GM - Mobileye Global: Worsening Prospects And Overvalued

2023-07-10 22:25:05 ET

Summary

- Mobileye is not the hot growth stock it used to be anymore as revenue is estimated to grow only 15% in 2023.

- The stock tanked 17% after the company lowered its guidance for 2023 due to a reduction in expectations for SuperVision volumes and a softer auto market.

- Despite this, we think that Mobileye is overvalued by ~50% and assign it a Sell rating.

Introduction

Mobileye Global ( MBLY ) is one of the first companies that pops up when looking in the autonomous driving sector. The company was spun off from Intel (NASDAQ: INTC ) in October 2022 and it seems that because it is profitable unlike its competitors the market is willing to pay a hefty premium for the stock. But given the slowdown in revenue they reported in the Q1 2023, we believe shares are significantly overpriced and the risk-reward ratio at the current price point is not attractive at all.

Overview

Before discussing the financial results of Mobileye we first need to understand how it generates sales. Around ~90% of revenue comes from the sale of EyeQ System-on-Chip (SoC). This chip has dominated the ADAS market with ~800 vehicle models and 50 OEMs incorporating it, including BMW (BMWYY), Volkswagen (VWAGY), and General Motors (NYSE: GM ). The EyeQ SoC utilizes cameras and sensors to provide passive/active ADAS and features including automatic emergency braking, adaptive cruise control, lane keeping assist, traffic jam assist, and forward collision warning.

The remainder ~10% of sales is mainly generated by SuperVision. SuperVision is an eyes-on/hands-off point-to-point assisted driving solution. In simpler terms, it's similar to what Autopilot represents for Tesla vehicles. This system is in its early stages but holds tremendous revenue potential, expected to be the primary driver of future revenue growth for the company.

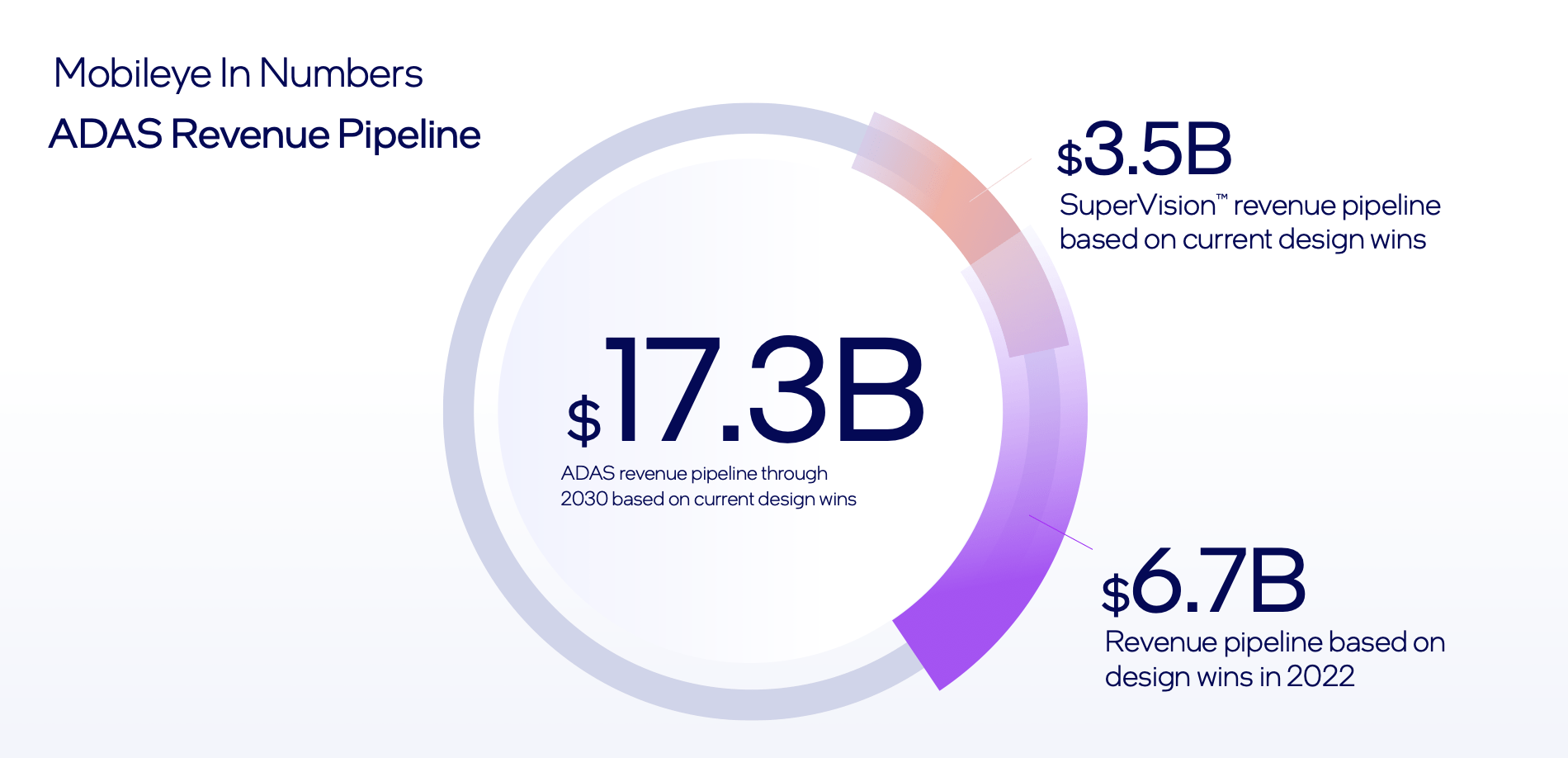

Overall, Mobileye allows OEMs to integrate Mobileye ADAS systems in their cars so that they don't need to spend a fortune developing their own in-house autonomous driving system like, for example, Tesla (NASDAQ: TSLA ) and Mercedes-Benz (MBGAF). Because of this, they already managed to secure $17.3 billion in ADAS contracts through 2030, including $3.5 billion for SuperVision.

{kind=link}

Financial Results

Mobileye reported Q1 financial results on April 27, which caused the stock to tank 17% after the release. Revenue increased only 16% YoY to $458 million. For a business regarded as a high-growth cutting-edge technology business, these growth rates fail to impress. Gross profit margin jumped slightly to 45.2% from 44.7% in Q1 2022 despite inflationary pressures.

On a GAAP basis, operating margin was -18% and net income was -$79 million. We emphasized on the GAAP measure because the company also reports non-GAAP metrics where operating margin jumps to 27% and net income to $115 million. We disregard these metrics since we consider that share based compensation and amortization are real costs that should be taken into account. However, investors can be easily tricked when reading these metrics in a press release and arrive at the wrong conclusions.

Nonetheless, one thing we can't argue against is the strength of its balance sheet and free cash flow generation. As of Q1 2023, the company had $1.16 billion in excess cash and equivalents and no debt, and in the first quarter they generated $171 million in operating cash flow and spent $25 million in capex. This is very important because the company doesn't rely on external sources of funding to run its business.

Outlook

We saw how the revenue growth started to slow this quarter and we expect the situation will only get worse. Mobileye lowered their guidance for 2023 due to a meaningful reduction in their expectations for SuperVision volumes in 2023 and a weaker electric vehicle market in China. At the beginning of the year , they expected revenue to be in the range of $2.192-2.282 billion and post and operating loss in the range of $160-110 million. Now they expect revenue to $149 million lower and operating loss to grow $45 million.

{kind=link}

However, we don't think the situation will improve much during the remainder of the year. The last two years vehicle supply has been very thigh due to chip shortage, inflation, etc. while demand was very strong. However, these problems are now in the rearview(new vehicles inventory levels hit the highest level in 2 years ) and, according to Cox Automotive , dealers say that the economy and interest rates are the main issue holding back their business. A very interesting metric in the report is that 30% of dealers indicated that "credit availability for consumers" was a problem in Q2 2023, up from 26% in Q1 and only 17% in Q2 2022. This will only get exacerbated if the FED raises interest rates 50bps more this year as the market estimates. In other words, we think the problem going forward will turn into a demand problem rather than a supply problem. Consequently, this will make OEMs manufacture less cars and Mobileye to sell less chips.

Valuation

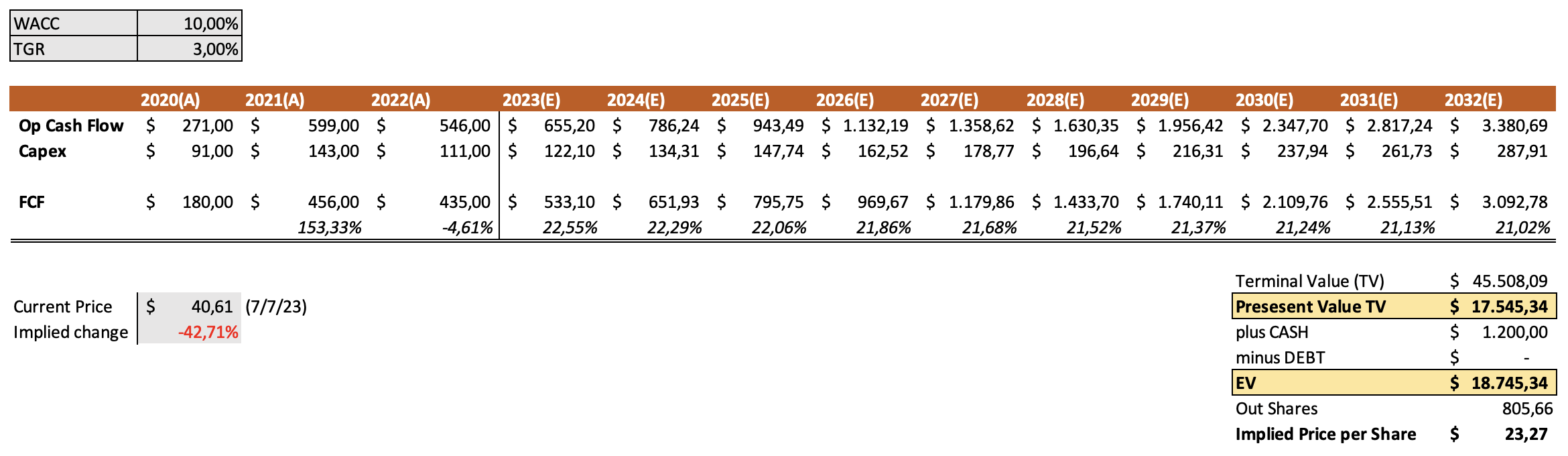

The problem we see with Mobileye, apart from the lack of growth, is its valuation. We built a 10-year DCF model assuming that operating cash flow will grow at a 20% rate per year and that capex will grow only at 10% per year. We used a WACC of 10% and a TGR of 3%. We feel that growing FCF ~21% per year for 10 years is definitely the bull case for Mobileye, but despite this we find that the stock fair price is $23.27 per share. This implies a 42% fall from the current prices. So even assuming the bull case we cannot justify the current valuation.

{kind=link}

Moreover the company is trading at very high multiples. The price to sales ratio is 16x. The problem is that Mobileye cannot grow into this valuation. If the company was growing revenue 60-70% per year this multiple would be more understandable, but revenue is forecast to increase only around 10-15% in 2023. Investors seem to value the stock based on the $17.3 billion revenue pipeline rather than the current revenue the company is able to generate.

Takeaway

The key takeaway for Mobileye investors is that despite the promising future of the business, right now most of that future growth is priced in. We believe current prices does not provide an attractive entry point and, if you are already a shareholder, should consider exiting or trimming your position and wait for better prices.

For further details see:

Mobileye Global: Worsening Prospects And Overvalued