CPTNW - Modeling Lidar Companies' Survival And Profitability

2023-10-30 20:13:13 ET

Summary

- Lidar companies' sustainability is crucial for investment; many may need equity sales to survive.

- Revenue forecasts and cash expenditures play a significant role in determining a company's potential for profitability and longevity.

- Only Luminar and Ouster show financial resilience and the potential to achieve profitability by 2026, while other companies may require additional funding.

Introduction

As I eagerly await the release of Q3 2023 results, my objective for this article is to present predictive scenarios that extend beyond the immediate outcomes of the upcoming quarter. I intend to emphasize the sustainability of lidar companies as a compelling rationale for investment. By incorporating revenue forecasts and cash expenditures, it becomes evident that even the most appealing communication-driven companies, despite their record of the revenue book, cannot ensure their survival without resorting to equity sales.

In addition, their prospects are naturally diminished without achieving favorable gross margins or reaching specified revenue levels. Moreover, the perception of the future varies significantly when comparing it to market valuations, which may lead to outcomes that diverge from what the market anticipates. Consequently, investments in companies that initially appear robust may take on a different aspect upon closer analysis.

The fundamental concept is quite simple. If a company can generate substantial revenue, coupled with a subsequent gross profit that covers its expenses, then it is likely to endure the developmental phase and outlast its competitors. Investing in such a company becomes less risky when it faces fewer competitors and demonstrates the ability to achieve at least a satisfactory technological equilibrium on par with other industry players. As the market becomes more aware of tangible progress, the probability of achieving a return on investment, supported by organic growth, increases.

The landscape of companies in this field is significant enough to be bewildering without a structured analytical approach. However, it's not so vast that one risks becoming lost in the data. My analysis seeks to ascertain whether a particular company possesses the potential to achieve profitability and, if so, when it is likely to achieve it.

The companies included in the model are Western-based lidar sensor manufacturers: Luminar ( LAZR ), MicroVision ( MVIS ), Innoviz ( INVZ ), Ouster ( OUST ), Aeva ( AEVA ), Cepton ( CPTN ), and AEye ( LIDR ).

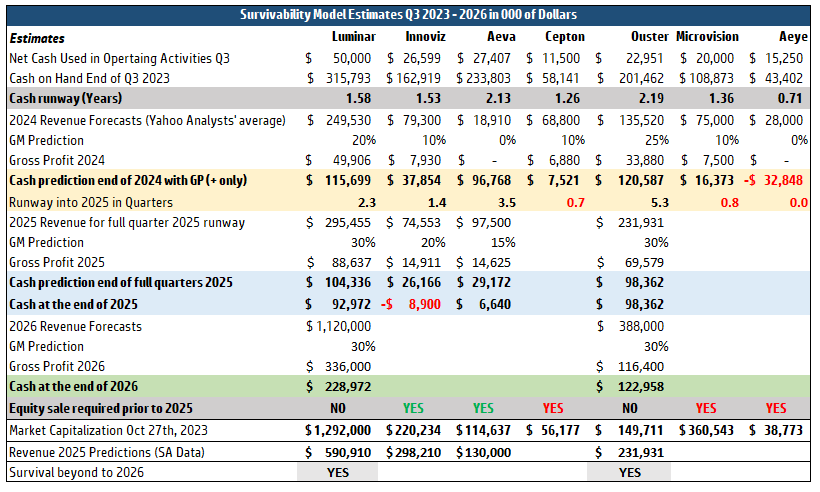

The table presented below provides a comprehensive overview of this analysis. As a predictive model for the future, it's important to note that all data in the table is based on estimates. When actual results become available for input into the model, they can further refine the outcomes.

The output results from extending Q3 projections through 2026 using cash reduction as a critical factor. This article provides information about net cash used in operations, which played a pivotal role in shaping this model. Additionally, I relied on analysts' revenue forecasts, sourcing data from Yahoo Finance for 2024 and Seeking Alpha for 2025 and 2026 for each company.

Furthermore, I considered savings announcements in examining cash expenditures, as exemplified by Ouster's case following its merger with Velodyne. While I aimed to incorporate gross margin assumptions based on each company's historical performance, most companies did not exhibit positive gross margins. Consequently, I have anticipated more favorable outcomes for companies traditionally operating with negative gross margins.

Survivability Model Estimates Q3 2023 - 2026 in $000 (Author, Yahoo Finance, Seeking Alpha)

{kind=link}

Net Cash Used in Operating Activities

Cash assumes a position of paramount importance, as demonstrated in the table, and its allocation will significantly impact each company's survival prospects. It's imperative to make a clear distinction here – the figures presented differ from operating expenses, as they do not encompass non-cash items like depreciation and stock-based compensation. Instead, they estimate the net cash employed in operating activities derived from the cash flow statement.

In forming these estimates, I have considered recent cost-saving initiatives some companies undertake and integrated these expectations into my calculations. Among these firms, I expect Luminar to reduce net cash used in operating activities from $73M in Q2 to my projected figure of $50M per quarter.

Furthermore, I have revised my expectations for Ouster to provide a more refined operating metric for Q3, landing at $24.6M rather than a mere average derived from post-merger activities.

On a contrasting note, MicroVision has been expanding its workforce, adding employees following the Ibeo acquisition and maintaining offices in Germany. Consequently, I anticipate an increase in MicroVision's quarterly cash outlay to $20M. The particular outcome of the Q3 results will stimulate spending in the model, as it will be used for cash spent for every quarter in the future.

Revenue Estimates and Gross Margin

The revenue estimates for 2024 are based on the average offered by the Yahoo Finance analysis section. And further into the future via Seeking Alpha. While there may be inaccuracies in some of these estimates over time, they serve as a solid baseline to gauge each company's survivability based on available cash. They, too, can be adjusted in the model as actual results are produced or forecasts are revised.

I considered gross margins and the resulting gross profits to evaluate the revenue's contribution to the bottom line. Only two companies, Cepton and Ouster, attained positive gross margins within the group, while the remaining companies struggled with negative gross margins.

I have made the following assumptions in the model, following the premise that mass production offers cost reductions. Due to its historical data, Ouster maintains a 25% gross margin, which is a median figure for the company, excluding the period of post-merger activities. For the other companies, I have modeled gross margins based on the level of the revenue: over $200M in revenue with a 20% margin, over $100M with a 15% margin, over $50M with a 10% margin, and below $50M with a zero margin. Lastly, I anticipate that Ouster will have a 30% gross margin when the company surpasses $200M in revenue to be conservative.

I have included MicroVision's $35M equity sale in the calculation and Innoviz's $60M cash (net of fees) acquired through its equity issuance, executed in Q2.

Survivability Model

Based on my analysis, I foresee challenges for Cepton, MicroVision, and AEye in sustaining their operations beyond 2024 due to inadequate funds. These companies will require additional financing to continue operating beyond that year, even when factoring in gross profit contributions to their cash reserves. All three of them have significant increases in revenue forecasts, which do not align with recent announcements.

Cepton, for instance, has secured a production win, but it's limited to a single model that may produce just 1,000 cars a year. It isn't easy to envision generating $68M in revenue solely from this source. MicroVision has yet to secure any wins, which doubts the accuracy of a $75M revenue forecast. Even though the model credits the company with $7.5M, MicroVision lacks the necessary cash reserves, according to the model, to sustain operations beyond the first quarter of 2025. Therefore, MicroVision may need to sell equity well before 2025 arrives.

The current low market capitalization of Cepton and AEye reflects market concerns about their prospects. Conversely, MicroVision's high market capitalization, despite the absence of business wins, appears to be out of sync with the sector's prevailing market conditions. In my model, all three companies are deemed unattractive for investment until they address their cash constraints.

According to my analysis, only four companies have the potential to navigate into 2025. However, both Aeva and Innoviz appear to require additional capital injections to ensure their sustainability upon entering 2025. While this need is not as immediate as for the three companies mentioned earlier, equity sales will likely be necessary in late 2024 or early 2025.

In my model, Innoviz's cash resources will be exhausted in 2025 without securing additional funding. Aeva, while able to continue into 2025, lacks the cash capacity to sustain operations into the first quarter of 2026.

The vulnerability of revenue forecasts is a shared concern among all companies. However, for three of them – Aeva, Innoviz, and Luminar – the impact of gross margins is an additional factor to consider. Ouster, one of the four companies, achieved a 27% margin in Q2 when accounting for one-off effects from the merger. Setting a 25% margin for Ouster in the 2024 revenue model is a conservative estimate and appears more attainable than the 10% margin forecast for Innoviz or Aeva.

Only Luminar and Ouster exhibit the financial resilience to forgo the need for capital injections, assuming that all estimated inputs materialize as actual results. Based on my analysis, Luminar and Ouster are poised to achieve profitability by 2026.

Conclusion

My survival analysis has yielded some intriguing predictions, particularly when examining market capitalization trends. My forecasts contrast the market's valuation of Innoviz and MicroVision, which appear to be overvalued but align with Cepton and AEye's situations.

According to my analysis, Ouster presents the lowest level of investment risk. This conclusion is based on the company's relatively modest market valuation compared to its peers and its position within the model, indicating profitability by 2026 alongside Luminar. Several of Ouster's competitors seem unable to sustain their operations without an infusion of capital, which, if not obtained, could imperil their survival. Given their higher market capitalization, recouping the initial investment may be challenging.

In my model, Luminar is the second company poised to achieve profitability in 2026. However, unlike Ouster, Luminar carries considerably more significant risks tied to factors such as revenue scale, which is more than double Ouster's 2025 revenue forecast and three times higher for 2026. Additionally, the expected reduction in operating costs is more dramatic than Ouster's, and margin considerations remain uncertain. Luminar's valuation remains notably high, in stark contrast to Ouster, which appears to be an exceptional bargain, valued at just one-ninth of Luminar's market capitalization.

Remembering that the model currently represents a snapshot of the present status is crucial. Therefore, adding further revenue potential or significant developments could enhance the model's predictions. Conversely, losing a win, disappointing revenue from existing production wins, and technological deterioration could have severe repercussions for all companies.

I will monitor these crucial factors to enhance the model's predictability further, providing increased clarity for myself and those considering investments in lidar companies. However, right before the Q3 conference calls, my conviction about investing in Ouster remains unwavering. The recent waves of sell-offs have only highlighted the strikingly low valuation of Ouster, especially when compared to its peers, despite the model's predictions.

With optimism surrounding the Q3 results, which are expected to shed light on digital technology and the path to profitability, the market presents an opportunity for averaging down. Ouster stands out as a prime candidate for such a strategy.

For further details see:

Modeling Lidar Companies' Survival And Profitability