MOD - Modine Manufacturing: Accelerating Trajectory With Further Upside

2024-01-10 23:04:42 ET

Summary

- Modine Manufacturing’s revenue has grown well at a CAGR of +5% during the last decade, but the real accomplishment is its EBITDA development of +10%.

- Management has executed a revitalization strategy, which involves the implementation of the 80/20 approach and the transition of its offering to more complex services.

- Management is forecasting HSD growth alongside margin improvement, allowing for growing distributions, international expansion, and opportunistic M&A.

- MOD spent much of the last decade being heavily undervalued. This is no longer the case, but we still see value due to the scope for greater shareholder returns.

Investment thesis

Our current investment thesis is:

- MOD is likely in the early stages of a significant upswing, underpinned by industry tailwinds and a successful business model transition. We believe this will drive shareholder value, following a period of limited distributions and volatile financial results. This is important as even if Management is unable to wholly execute its strategic objectives, the fundamental improvement in the business is a value driver.

- MOD is trading at an FCF yield of ~4%, while Management forecasts revenue growth of HSDs and margin improvement by ~4ppts. When partnering this with its capital allocation strategy, we see scope for an acceleration.

Company description

Modine Manufacturing Company ( MOD ) is a global leader in thermal management solutions. Headquartered in Racine, Wisconsin, the company specializes in designing, manufacturing, and testing heat transfer products for various industries, including automotive, industrial, and HVAC markets. With a history dating back to 1916, Modine has established itself as an innovative and reliable provider of thermal management solutions.

Share price

MOD’s share price performance during much of the decade was disappointing, although a recent aggressive rally (+~177% 1Y) has contributed to returns in excess of the wider market. Modine’s inconsistent financial performance has restricted its expansion, although recent developments have driven shareholder sentiment.

Financial analysis

{kind=link}

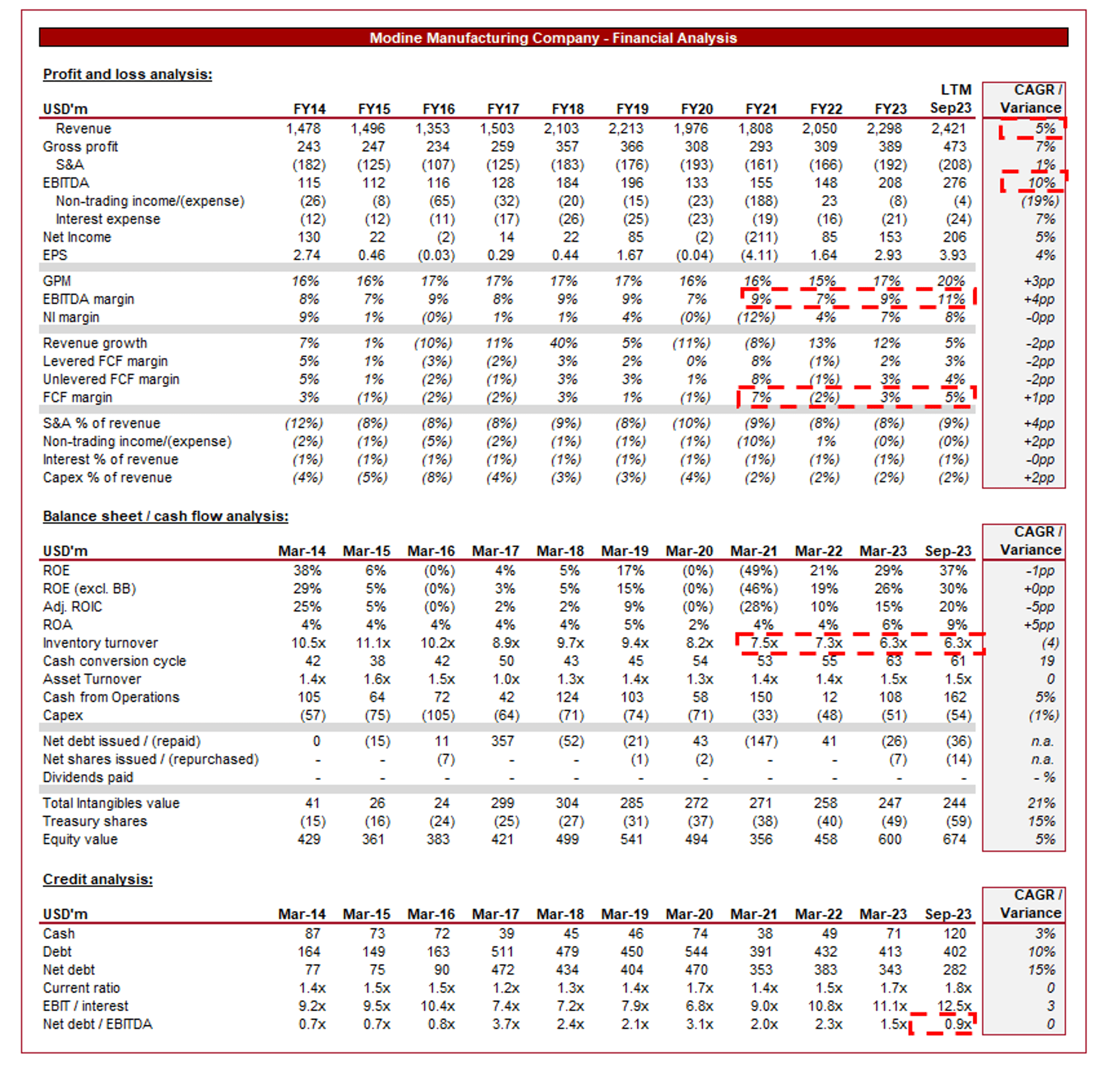

Presented above are MOD’s financial results.

Revenue & Commercial Factors

MOD’s revenue has grown at a CAGR of +5% during the last decade, although the annual development has been volatile. Impressively, EBITDA has doubled this at +10%.

Business Model

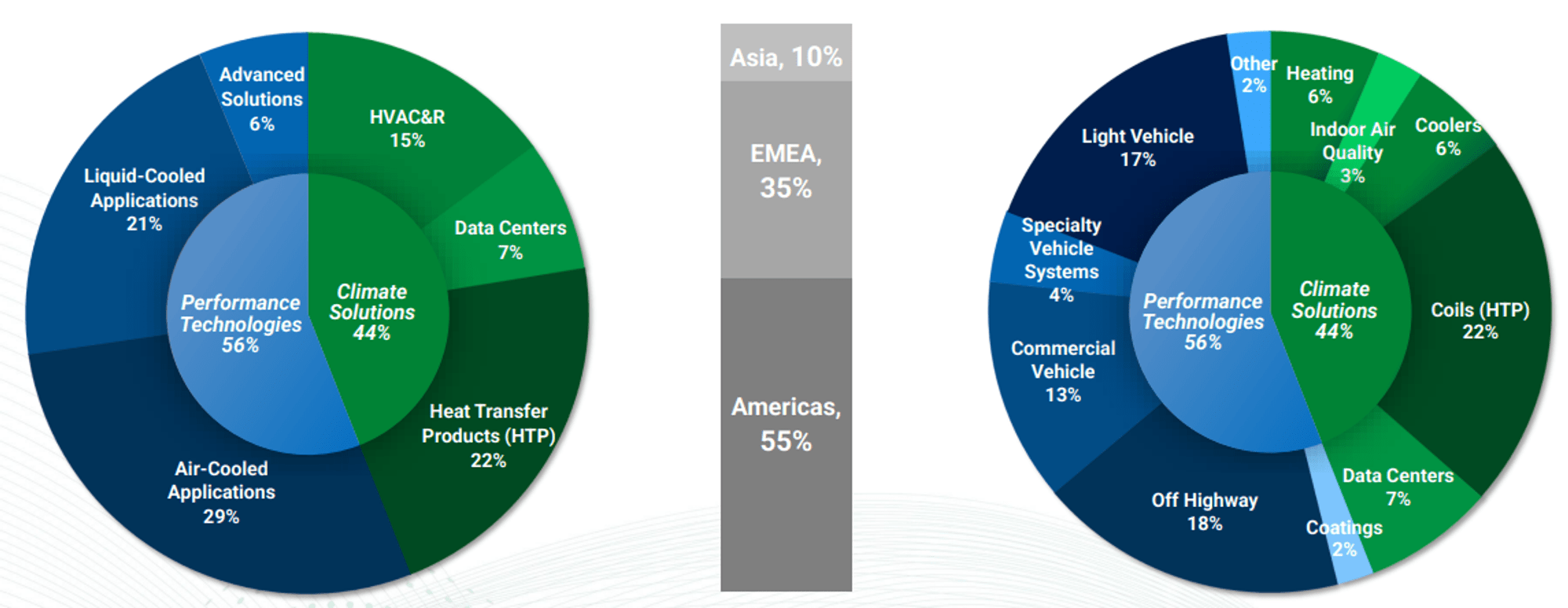

Modine operates in multiple business segments, including Vehicular Thermal Solutions ((VTS)), Commercial and Industrial Solutions ((CIS)), and Building HVAC Systems. These segments cater to different markets, providing diversified revenue streams while leveraging its core competencies and asset base.

{kind=link}

Briefly, its offering is described as follows:

- Vehicular Thermal Solutions ((VTS)) - MOD specializes in providing thermal management solutions for vehicular applications. This includes designing and manufacturing radiators, charge air coolers, and other components for automotive, commercial vehicle, and off-highway markets.

- Commercial and Industrial Solutions ((CIS)) - The CIS segment focuses on thermal management solutions for non-vehicular applications. This includes products for HVAC systems, industrial equipment, power generation, and other commercial and industrial processes.

- Building HVAC Systems - Modine also engages in the design and manufacture of HVAC systems for buildings. This includes products like unit heaters, infrared heaters, rooftop HVAC units, and ventilation systems.

MOD has a global presence, with 35 manufacturing facilities in ~13 countries, serving customers in various regions. This international footprint allows the company to tap into diverse markets and mitigate risks associated with regional economic fluctuations.

The company places a strong emphasis on innovation and technology, underpinned by patents and deep expertise, as this is the bedrock of its competitive position. Developing advanced thermal management solutions that meet industry standards but also enhance the value proposition for consumers is critical to differentiating itself, particularly as the demand for such products increases.

MOD provides aftermarket services, including replacement parts and support services. This enhances customer satisfaction and builds long-term relationships with clients and from a financial perspective, creates greater certainty/visibility of revenue generation due to its recurring nature.

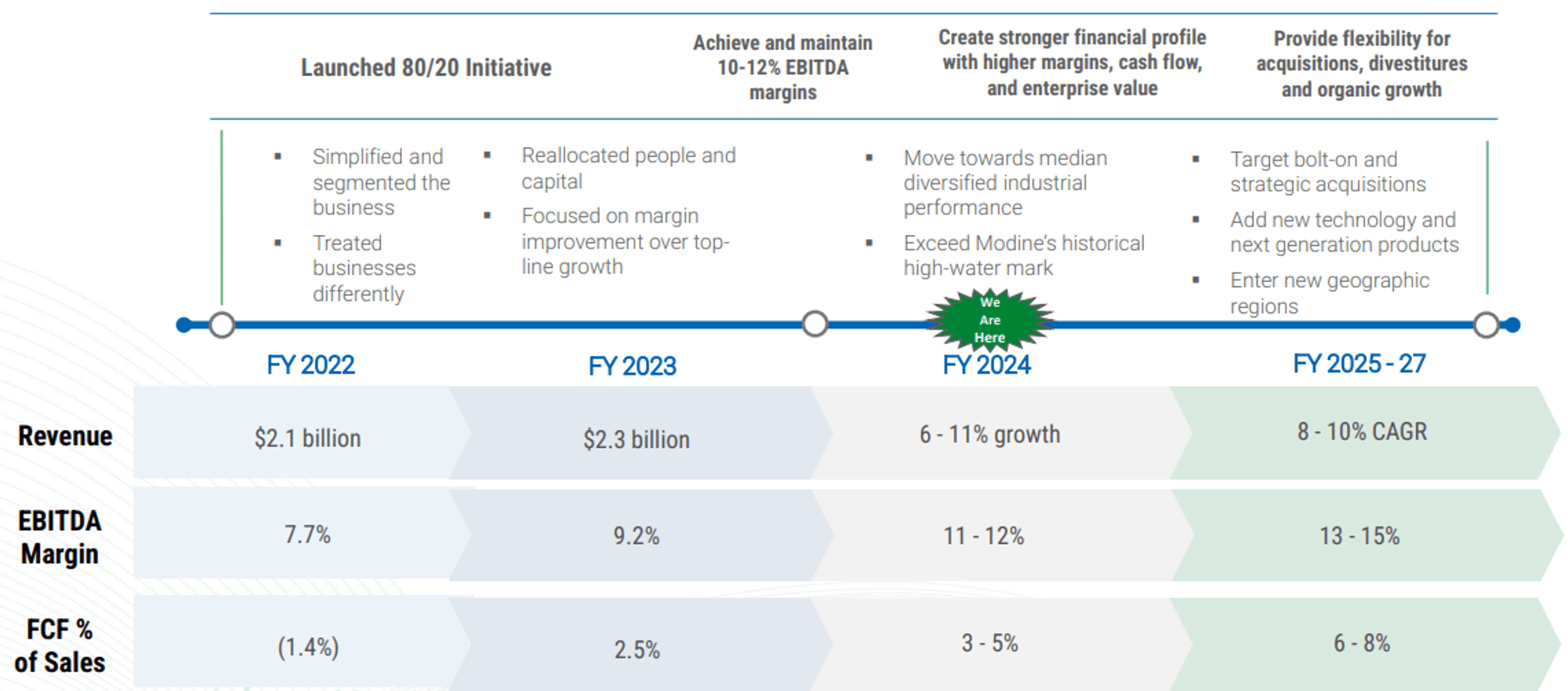

Business model transition

Management initiated a multi-year revitalization effort to improve the financial profile of MOD, as well as to increase returns for shareholders.

This has involved a number of steps, including:

- “Focus the organization” - Management has firstly sought to improve the culture and operational DNA of the company, implementing the 80/20 approach (20% of activities generate 80% of the results… so identify and focus on those) and simplifying and segmenting the company. Usually, the announcement of culture changes is just talk but we feel a tangible difference being made with this switch, which Management believes is evidenced by an improvement in its “Climate Solutions” segment.

- “Perform and deliver” - This involves a combination of maximizing market share in its target markets and simplifying its operations to focus on the end market it cares about. For example, efforts are being transitioned to servicing EVs and Data Centers (among others but these are used as examples), both of which are within industries experiencing long-term headwinds and thus are positioned for outsized growth. The full shift of focus positions MOD better than many of its peers, who would likely move more defensively by keeping one eye on its existing capabilities.

- “Accelerate profitable growth” - This is a combination of firstly product development, namely the transition from components to systems solutions, which involves deeply ingraining itself in its clients’ operations with more complex solutions. We believe this to be the biggest growth driver and is currently being delivered successfully. Secondly, Management is seeking to press more greatly on international expansion following the successes of its transition in the US, as well as opportunistic M&A.

{kind=link}

Thermal Management Industry

MOD faces competition from a range of global conglomerates, as well as specialist firms. The includes, but is not limited to: Johnson Controls ( JCI ), Lennox International ( LII ), Honeywell International ( HON ), and Trane Technologies ( TT ).

These companies compete on:

- Technological advancements in product offerings.

- Pricing strategies and after-sales services.

- Market share and geographic reach.

We believe MOD is positioned well, particularly following the transition to system solutions, which has diversified the company further.

Opportunities

We see the following factors as key growth drivers in the coming years:

- Electrification Boom: Capitalizing on the increasing trend of electric vehicles.

- Smart HVAC Solutions: Investing in IoT-enabled products for enhanced control.

- Global Expansion: Tapping into emerging markets with growing infrastructure needs.

- Automotive and Industrial Demand: The demand for thermal management solutions in the automotive and industrial sectors has been robust.

- Focus on Energy Efficiency: MOD is focusing on developing energy-efficient HVAC solutions that align with market trends and customer preferences.

Economic & External Consideration

Current macroeconomic conditions represent near-term headwinds for MOD, as with elevated interest rates and inflation, consumers are feeling a squeeze on finances. This has impacted the corporate environment, with softening spending alongside inflationary pressure on its supply chain.

This is contributing to reduced capital spending as businesses seek to shore up their balance sheet. We are not overly concerned by this, considering it a natural cyclical swing that is unlikely to impact the competitive position of MOD.

Looking ahead, we suspect demand will be muted in 2024, likely declining to mid-single-digits. This remains uncertain, however, as there is a growing belief of both a recession and a step down in rates. How either or both develop will impact the demand environment.

Margins

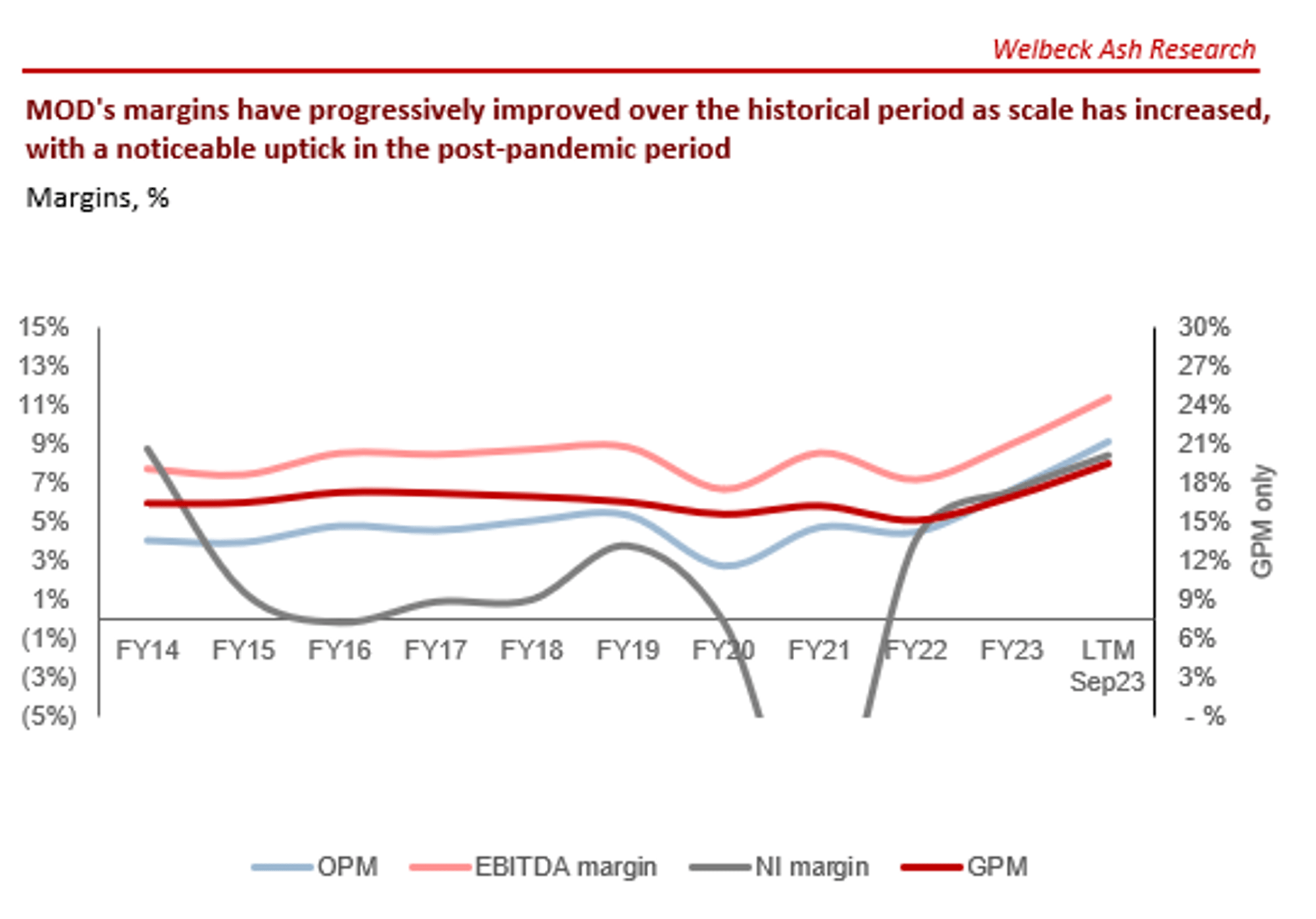

{kind=link}

MOD’s margins have progressively improved during the last decade, particularly accelerating in recent years. This is a reflection of its business model revitalization, with our belief that the current levels are sustainable, but also that further gains are possible. Management believes an EBITDA-M of ~15% can be reached by 2027, which we concur with.

Quarterly results

MOD’s revenue uplift has softened but remains healthy, with top-line revenue growth of +11.5%, +7.6%, +15.0%, and +7.2%. In conjunction with this, as we have discussed, margins have sequentially improved.

Balance sheet & Cash Flows

MOD is conservatively financed, with an ND/EBITDA ratio of 0.9x. This has been achieved due to consistent FCF generation, allowing for reinvestment (and more recently distributions) to be funded through cash.

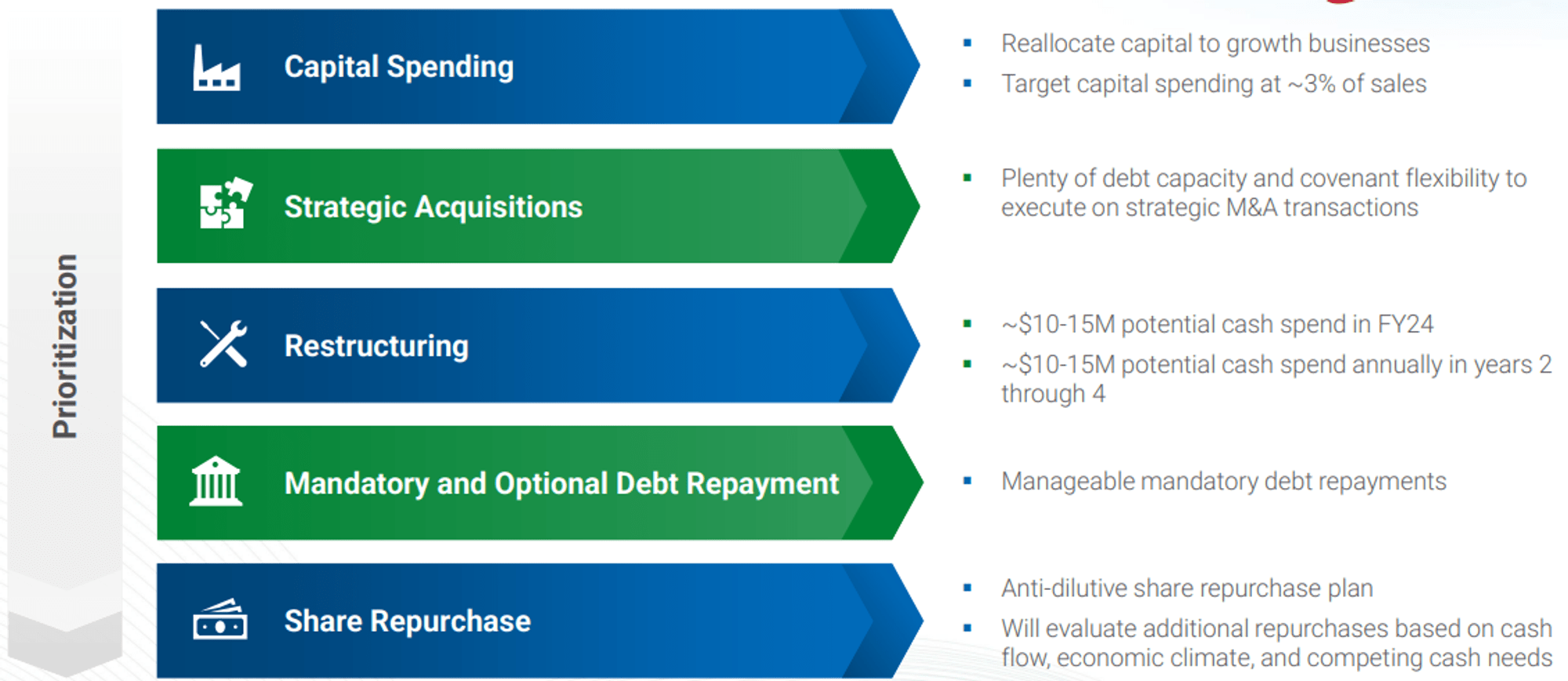

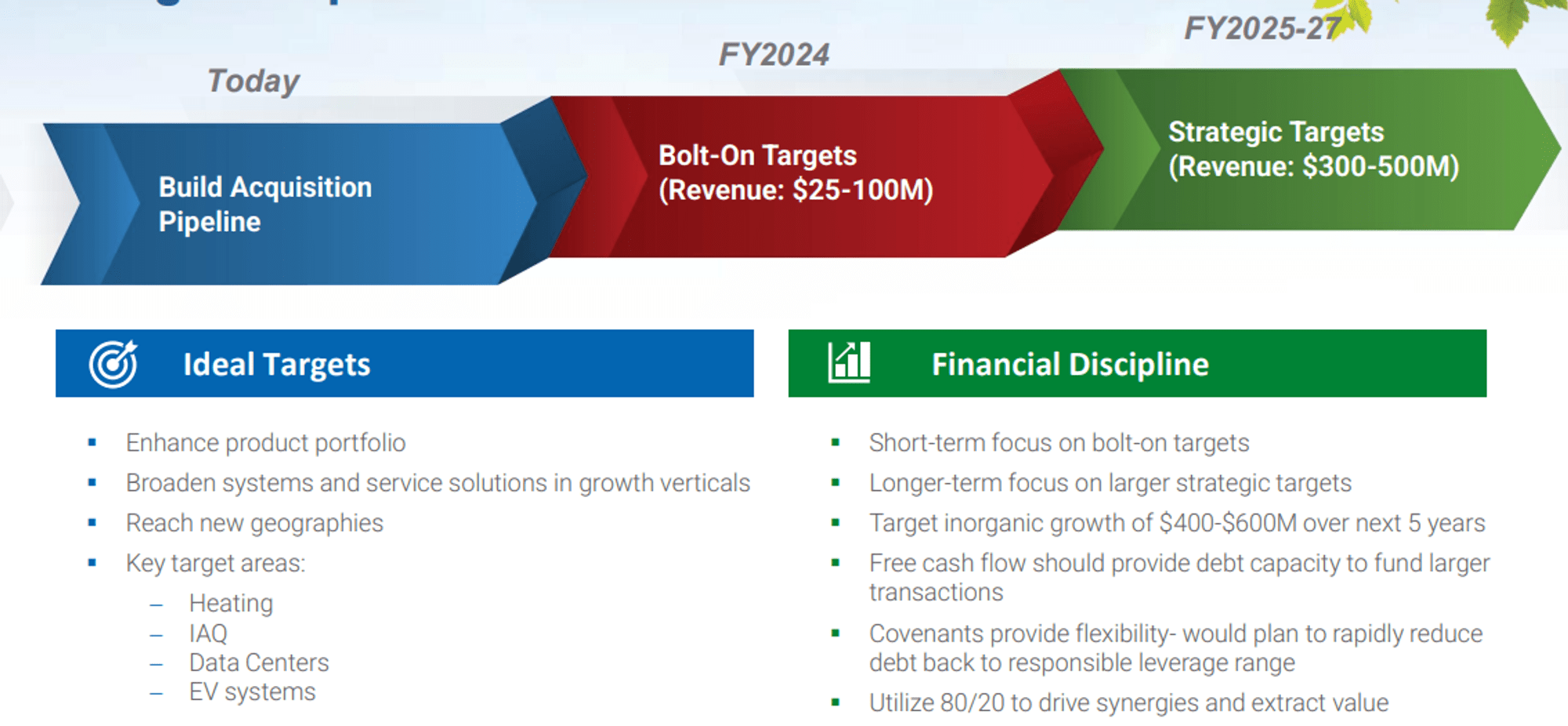

We expect a significant transition in its capital allocation strategy following its rapidly improving financial performance. Management has announced the following as its approach.

{kind=link}

We are supportive of this approach, noting the company has the optionality to raise debt to execute this once rates decline. Further, a renewed M&A strategy will complement the improvement in financial performance, accelerating its trajectory.

{kind=link}

Outlook

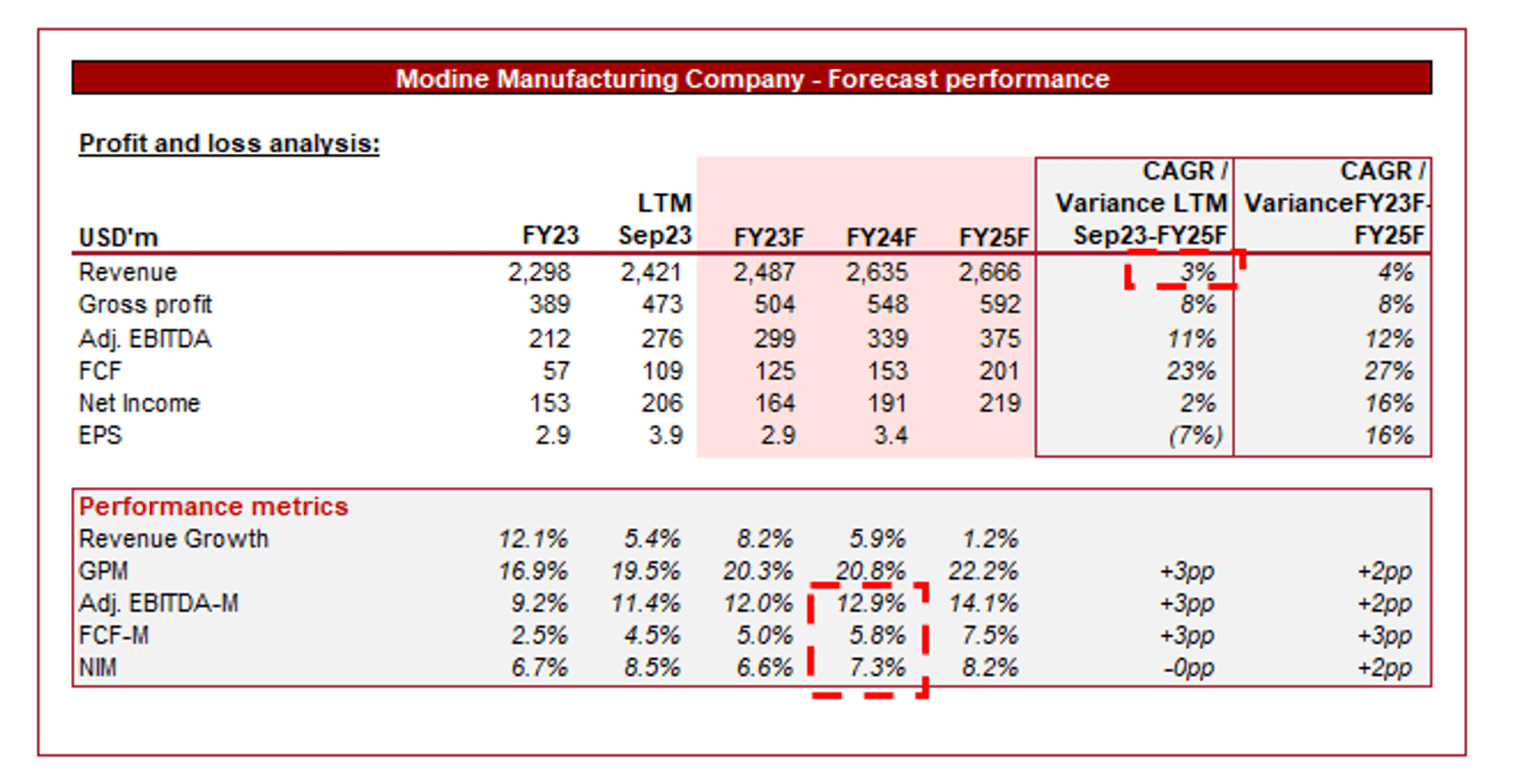

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting mild growth in the coming years, with a CAGR of +3%, alongside incremental margin improvement. From a growth perspective, this is noticeably below Management’s guidance, implying hesitancy around execution.

We acknowledge historical underperformance, particularly at the start of the decade, although its current trajectory and specifically development in sub-segments such as data centers imply MOD has upgraded itself significantly.

We suspect MOD will likely land closer to Management’s estimates.

{kind=link}

Industry analysis

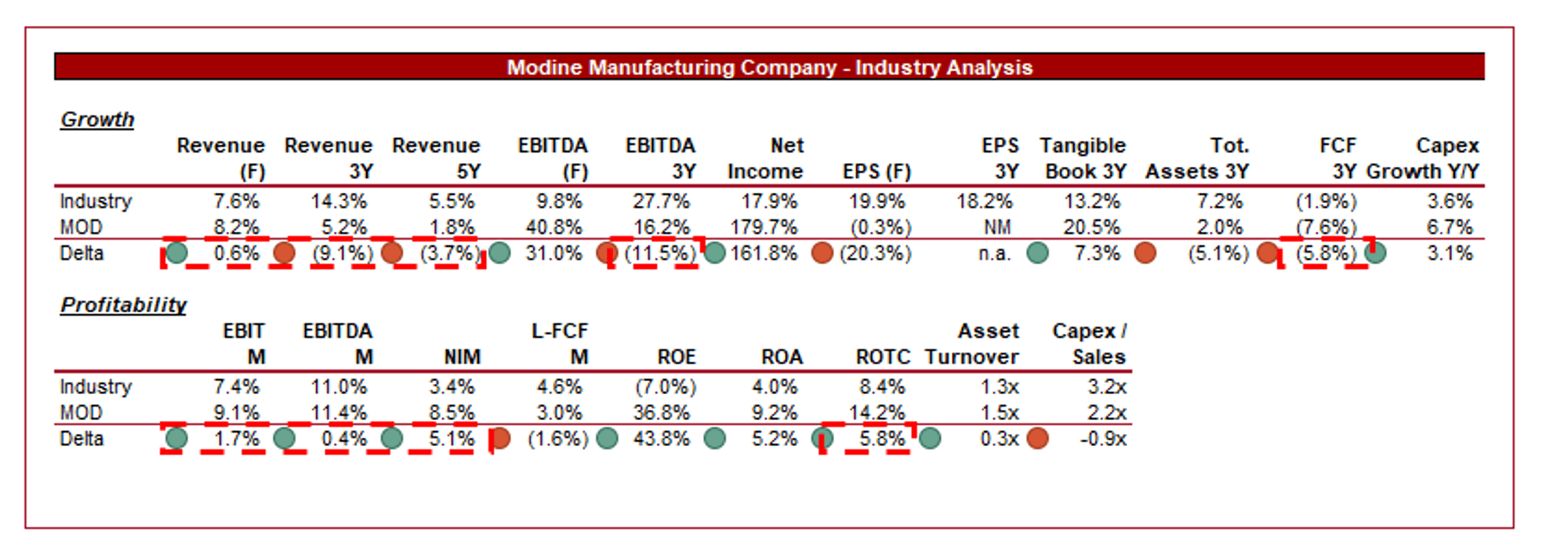

{kind=link}

Presented above is a comparison of MOD's growth and profitability to the average of its industry, as defined by Seeking Alpha (27 companies).

MOD performs well relative to its peers. The company’s growth has slightly lagged behind its peers, partially due to its lack of M&A strategy and relatively smaller size of its peers. We do not consider the delta overly concerning.

Further, MOD’s margins are slightly above average, with greater scope for improvement in the coming years. This has allowed the company to boast a noticeably superior ROE/ROTC, suggesting higher long-term returns.

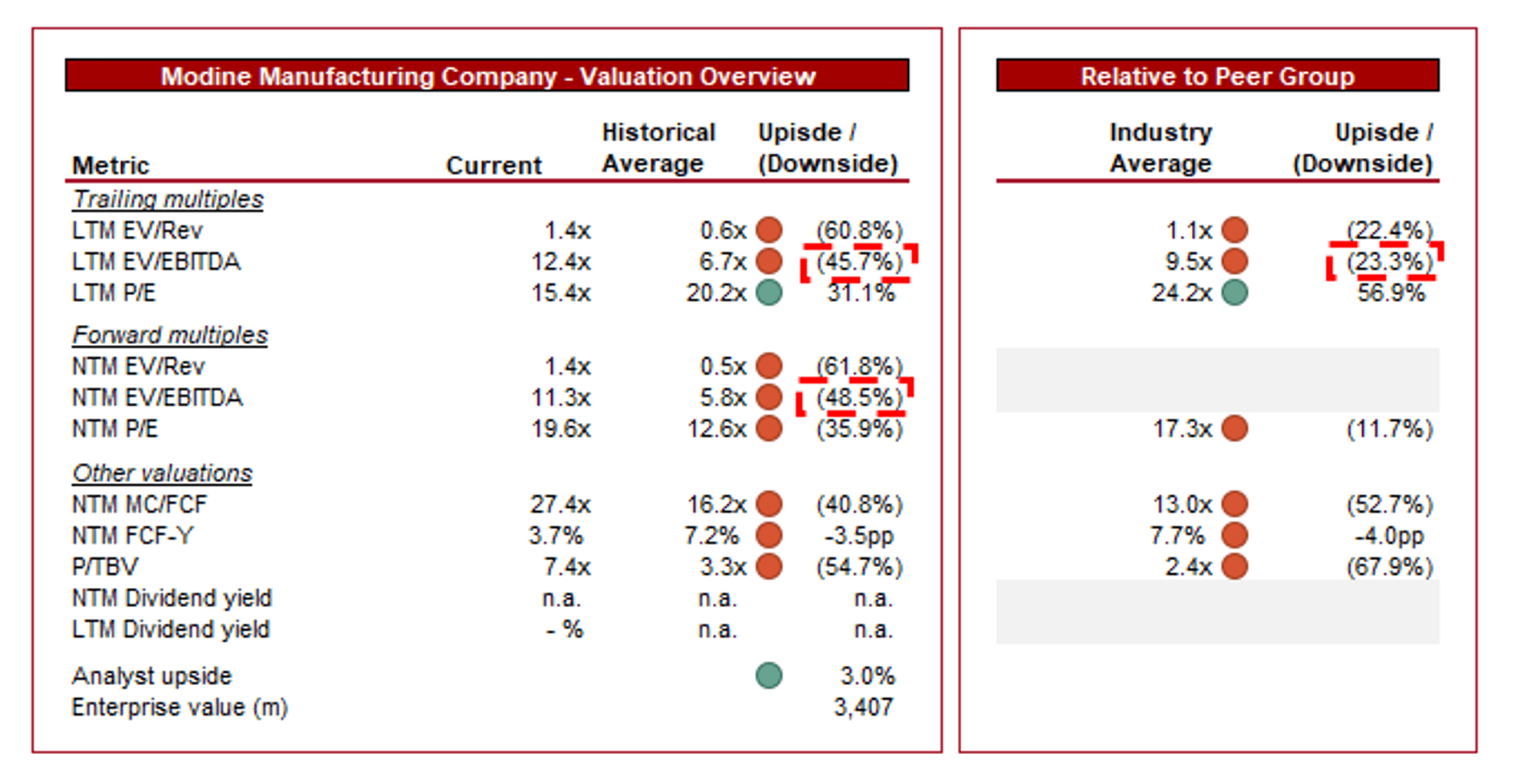

Valuation

{kind=link}

MOD is currently trading at 12x LTM EBITDA and 11x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is warranted in our view, owing to the company’s strong financial and commercial development during this period. The size of the discount appears extreme, and we agree, although we counter that MOD was likely undervalued for much of this period. MOD was trading at a 7% FCF yield while operating in a highly attractive industry experiencing tailwinds. At a ~4% FCF yield now, we think the company is attractive without being a standout buy (anymore).

Further, MOD is trading at a smaller premium to its peers, ~23% on an LTM EBITDA basis and ~12% on a NTM P/E basis. Purely from a margin basis, this is likely a top-range justifiable premium but its ROTC implies comfortably superior returns are possible. This will be buffeted by investor sentiment improving with distributions increasing.

Key risks with our thesis

The risks to our current thesis are:

- Economic downturn impacting demand for new installations.

- Slow adoption of innovative technologies affecting competitiveness.

Final thoughts

MOD is in the process of being transformed and its progress thus far is highly commendable. We have seen an immediate improvement in financial performance, alongside a fundamental shift in its business model that positions it perfectly for the future ahead.

Although there is execution risk in the medium term and uncertainty in the short term, we see a broadly upward trajectory based on the developments thus far. Importantly, shareholder returns will improve and margins still have sufficient room to run, implying investors will enjoy more of its ~4% FCF yield now than investors did historically from its ~7% FCF yield.

For further details see:

Modine Manufacturing: Accelerating Trajectory With Further Upside