MOD - Modine Manufacturing Can Continue Its Outperformance

2023-09-15 01:56:03 ET

Summary

- Modine Manufacturing Company is experiencing healthy demand for its products, benefiting its revenue growth and order book.

- The company's revenue should continue to benefit from its 80/20 strategy and a healthy order book in the future.

- MOD is pursuing strategic M&As to expand its product lines and accelerate revenue growth in the medium to long term.

Investment Thesis

Modine Manufacturing Company's (MOD) stock price is up over 200% since my previous bullish article in August last year and if we look at the stock performance since my initial buy rating in March last year, the stock price has gained ~400%. Normally, when the stock has appreciated this significantly I usually prefer taking some chips off the table. However, not with this one. Modine is still reasonably valued and has multi-year growth prospects.

The company's revenue should continue to benefit from its 80/20 strategy with increasing focus on high growth markets. While the company's Climate Solutions segment is already halfway through 80/20 strategy implementation, its Performance Technologies segment is just getting started and we should continue to see benefits from this strategy's implementation. The company also has a healthy order book which should help revenues in the near term. Apart from organic growth, the company plans to pursue strategic M&As that expand or complement its product lines in the new and existing markets, which would accelerate the revenue growth in the medium to long term. The company's margin outlook is also favorable with it focusing on growing high-margin offerings to improve product mix. In addition, despite significant price appreciation over the last year, the company's valuation is still reasonable considering its growth prospects. Hence, I believe the company can continue to outperform in the future and maintain my buy rating.

Revenue Analysis and Outlook

Modine's sales have benefited from implementation of 80/20 strategy in its business and increasing focus on identifying and growing business verticals with high growth/high margin potential (e.g. Data Center cooling).

In the first quarter of 2024, MOD sales growth benefited from higher volumes in both of its segments and favorable pricing. As a result, the company posted a 15% Y/Y increase in net sales to $622.4 million .

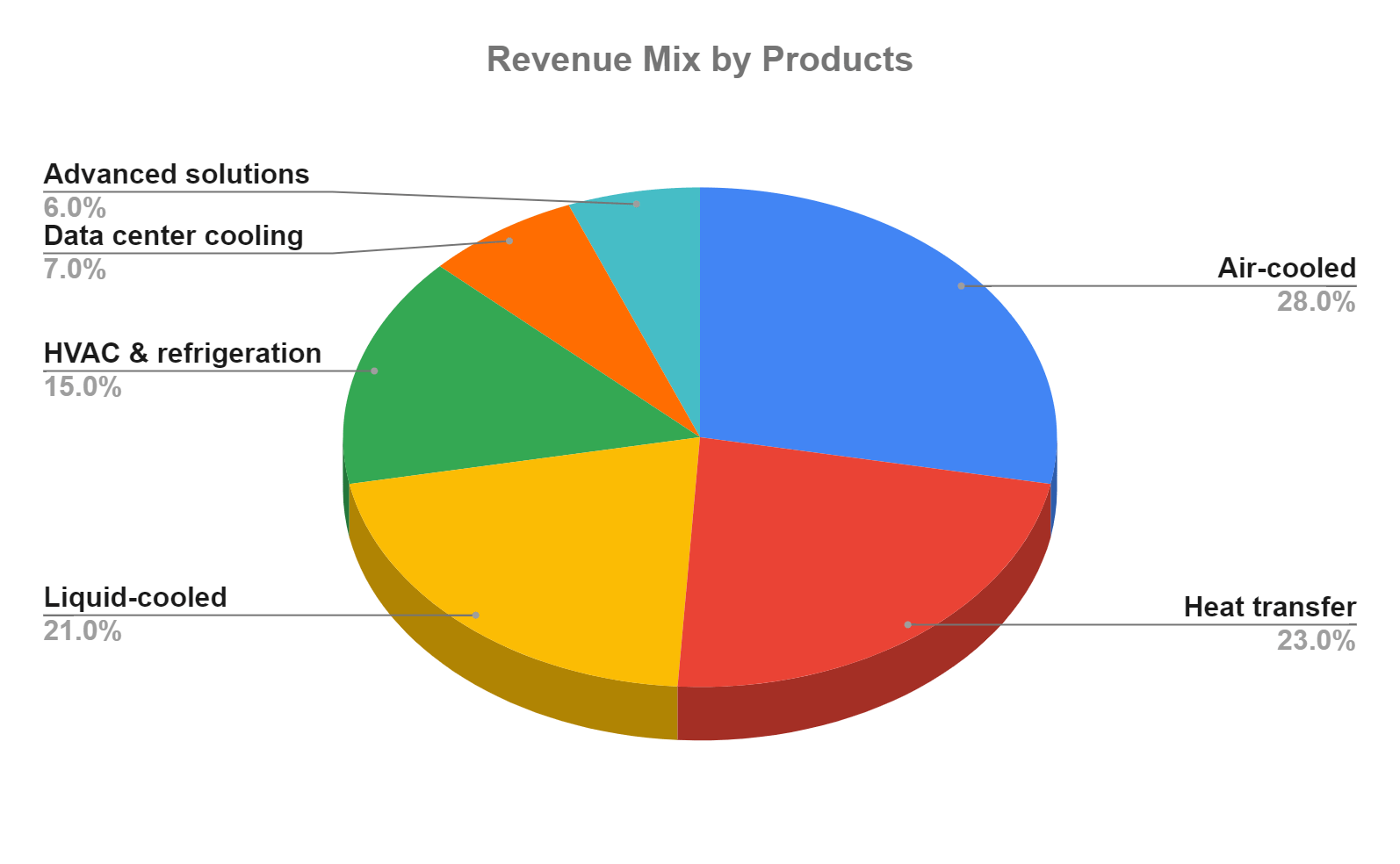

In the Climate Solutions segment, sales increased 11.2% Y/Y, driven by 123.6% Y/Y sales growth in the data center vertical, which more than offset the 6.5% Y/Y decline in heat transfer products and a 1.6% Y/Y decline in HVAC & Refrigeration sales. The HVAC&R sales decreased 1.6% Y/Y due to lower heating products sales due to market softness, partially offset by higher indoor air quality sales. Heat transfer product sales decreased 6.5% Y/Y driven by softness in commercial refrigeration and residential markets.

In the Performance Technologies segment, sales increased 17.9% Y/Y to $358.9 million, driven by strong commercial pricing and double-digit sales growth in its product group. Within the segment, sales of Air-Cooled Applications grew 12.9% Y/Y due to the robust demand from off-highway customers, with sales growth in genset or stationary power applications. Liquid-cooled applications sales increased 21.5% Y/Y, driven by strong demand from automotive, commercial vehicle, and off-highway customers. The sales in the Advanced Solutions business grew 31.3% Y/Y, attributed to higher sales for EV systems and component sales.

MOD's Historical Revenue Growth (Company data, GS Analytics Research) MOD's Revenue Mix by Product groups (as of FY23) (Company data, GS Analytics Research)

{kind=link}

Looking forward, Modine is well placed to continue benefiting from its 80/20 business transformation strategy where it is focusing on high growth high margin areas while exiting low growth low margin portfolio. The company has been implementing this strategy for over a year in its Climate Solutions business and, according to management, it is halfway through in terms of progress in implementing this strategy in the segment. Under this strategy, the company shifted its focus on high growth Data Centre Cooling business and the results are apparent. The segment's Data Centre Cooling vertical grew 80.5% Y/Y in FY23 and posted another 123.6%. Y/Y growth in Q1 FY24. With Heat Transfer and HVAC/R verticals seeing slowdown, in Q1 FY24, it was Data Centre Cooling business that helped the segment post meaningful Y/Y growth.

On its last earnings call , management noted that the company has a strong backlog including both hyperscale and colocation customers as well as a pipeline of new products and new customers which should continue to drive above market growth rate in Data Centre Cooling business in the future. So, there is a good visibility on the segment's future growth prospects. Further, with the increased use of high-performance computing, Artificial intelligence, machine learning and other applications, the company is working on more advanced cooling technologies to deal with higher heat load and considering in-house research as well as potential acquisitions to address this need. I believe the ??mpany has a multi-year runway for growth in this market.

In the Performance Technologies segment, the company has only recently begun implementing 80/20 strategy and in the initial stages, the company has focused on improving pricing and renegotiating contracts to help offset some of the material, labor and overhead inflation seen in the last couple of years.

Further, the company is focusing on high growth markets for this business. One such opportunity is the company's Genset business. In this business, the company is actively collaborating with existing and prospective customers to facilitate a shift from copper brass to aluminum heat exchangers which have a cost as well as performance advantage. The company also sees good growth opportunities in its EV systems business and has won over 25 programs including two for its fuel cell products.

The company has seen encouraging early success in implementing 80/20 strategy in this segment and I see a long-term growth potential here as well.

In addition to good organic growth prospects, the company has also started focusing on M&As to improve its portfolio and position it for growth. In early July, the company acquired Napps Technology which has a small chiller range that provides additional product lines for the company's school market. The company has a healthy balance sheet with net debt of ~$265 mn at the end of the last quarter and net leverage of 1.1x. With continued earnings and FCF growth, I expect further M&As in the future which should complement the company's organic growth. So, I am optimistic about the company's growth prospects.

Margin Analysis and Outlook

In Q1 2024, the company's margins benefited from sales leverage in both segments, operating efficiencies from implementation of 80/20 initiatives, and improved material and freight costs. This resulted in a 510 bps Y/Y improvement in the adjusted EBITDA margin to 12.9%. The Climate Solutions segment's adjusted EBITDA margin improved 500 bps Y/Y to 18.3%, while in the Performance Technologies segment, the adjusted EBITDA margin increased 560 bps Y/Y to 11.2%.

MOD's Segment-Wise Adjusted EBITDA margin (Company data, GS Analytics Research)

{kind=link}

Looking forward, the company's margin outlook is positive as it continues to focus on growing high margin offerings which should continue to improve mix. The company has also achieved good success in raising prices and renegotiating contracts as a part of initial implementation of 80/20 program in Performance Technology business which should also help margins. In addition, management is also exiting low margin business. For example, last quarter the company discontinued 73 SKUs in its liquid cooling business which had negative gross margins. In addition to benefiting from applying the 80/20 approach to existing portfolio, the company should also benefit from potential M&As where it can acquire higher growth /higher margin product portfolio. So, I am optimistic about the company's long-term margin expansion prospects.

Valuation and Conclusion

MOD is currently trading at 15.32x FY24 consensus EPS estimate of $2.89 and 13.06x FY25 consensus EPS estimate of $3.39.

Modine Consensus EPS Estimates (Seeking Alpha)

{kind=link}

Given the company is still in early stages of transformation in its Performance Technologies business and only halfway through in Climate Solutions business, I believe the company has a multi-year runway of organic growth ahead of it. So, the valuation still looks reasonable considering the growth prospects. Further, the company is also just getting started with M&As which is the phase II of its business transformation plan. The high-quality secular growth stories in industrial sectors which focus on high growth verticals and tuck-in acquisitions to drive long-term growth usually trade around mid to high 20s or even low 30s P/E multiple. For example, Danaher ( DHR ) is trading at 28.56x FY23 P/E while Roper Technologies ( ROP ) is trading at 30.07x FY23 P/E. I believe the company is transforming into one of those secular growth stories and, as it continues to progress in its transformational initiatives, the valuation multiple should continue to re-rate. This along with EPS growth should result in a good upside. Hence, I believe the stock can outperform in the long run and continue to have a buy rating on it.

For further details see:

Modine Manufacturing Can Continue Its Outperformance