GTX - Modine Manufacturing: Cheap For A Reason

Summary

- Modine Manufacturing Company has had something of a mixed operating history, and this year should prove to be no exception.

- Having said that, shares of the business are trading on the cheap, but a discount is usually warranted in cases like this.

- Overall, the firm doesn't look bad, but it's far from being a great prospect either.

The modern era has been defined by technological innovation. One technology that has been truly transformative involves thermal management. The ability to control temperature has had countless benefits and touches on a variety of applications ranging from indoor temperature changing to automotive functions. And one fairly small company that has made a name for itself dedicated to providing this kind of technology is Modine Manufacturing Company ( MOD ). Unfortunately, the past few years have been rather lackluster. Sales have shown no clear trend and the same holds true of profitability. On the other hand, the current fiscal year is looking up for the company and shares are trading at levels that should be considered generally attractive. As a value investor, I like buying companies on the cheap. But this doesn't mean that every cheap company makes for a great play. The absence of any real trend when it comes to sales and profits is a definite turn-off. And when you consider how the company is priced compared to similar firms, I would make the case that there are better opportunities to be had at this time. For all of these reasons, I've decided to rate the enterprise a ’hold’, reflecting my belief that it's likely to generate returns more in line with the market for the foreseeable future.

An HVAC Play

According to the management team at Modine Manufacturing, the company specializes in providing thermal management products and solutions to its customers. Namely, the company focuses on servicing customers in the commercial, industrial, and building heating, ventilating, air conditioning, and refrigeration markets. It does, however, provide other goods and services that are worth noting. For instance, it also produces heat transfer systems and heat transfer components for use in on and off-highway original equipment manufacturer vehicular applications. To best understand the firm, we should dig into each of the operating segments that it has. For the purpose of best understanding the business, we will discuss the segments it traditionally has had, and then discuss an important change the firm implemented this year.

The largest of the segments has been called Heavy Duty Equipment. Through this segment, the company provided powertrain and engine cooling products such as radiators, charge air coolers, condensers, oil coolers, fuel coolers, electronics cooling packages, and more. During its 2022 fiscal year, this particular segment accounted for 39% of the company's overall sales. However, it only was responsible for 23.2% of the firm's profits. Next in line, we have the Commercial and Industrial Solutions segment. This particular unit provided a broad offering of thermal management products to the heating, ventilation, air conditioning, and refrigeration markets across North America, EMEA (Europe, Middle East, and Africa), and China. Examples include, but are not limited to, indoor, outdoor, and mobile climates, food storage and transport refrigeration, and various industrial processes. The primary products produced by this segment included coils, coolers, and coatings. On the coolers side, the company lists commercial refrigeration units used for things like food storage and transportation, but it also includes the same technology for carbon dioxide and ammonia unit coolers, remote condensers, and more. This segment accounted for 30% of the company's revenue but just 23.2% of its profits last year.

Next, we had the Building HVAC Systems segment. This unit was responsible for selling a variety of heating, ventilating, and air conditioning products, many of which are used in commercial buildings and data centers throughout North America and Europe. However, it does have some exposure to the Middle East. These products are sold through a variety of channels, including wholesalers, distributors, consulting engineers, contractors, and other related parties. Some of these products are particularly advanced, especially those related to its data center activities. On this front, the company provides precision air cooling units, fan walls, condensers, and condensing units. Last year, this particular segment accounted for only 16% of the company's revenue but made up an impressive 30.5% of its profits. And finally, we have the Automotive segment, through which the company has offered powertrain and engine cooling products like radiators, charge air coolers, oil coolers, and more. This unit was responsible for only 15% of the company's revenue last year but it made up 23.2% of its profits.

All of this was the case until the company began its 2023 fiscal year. In an effort to better streamline operations, the company has taken these segments and combined them. The Building HVAC Systems segment and the Commercial and Industrial Solutions segment were added together to form the Climate Solutions segment. The one exception to this would be the CIS Coatings portion of the latter former segment. This was combined with the Heavy Duty Equipment and Automotive segments to create the Performance Technologies segment of the company. Using data from the most recent quarter, the Climate Solutions segment accounts for roughly 44.5% of the company's revenue but an impressive 78.5% of its profits. Meanwhile, the Performance Technologies segment makes up 55.5% of the company's revenue but only 21.5% of its profits.

{kind=link}

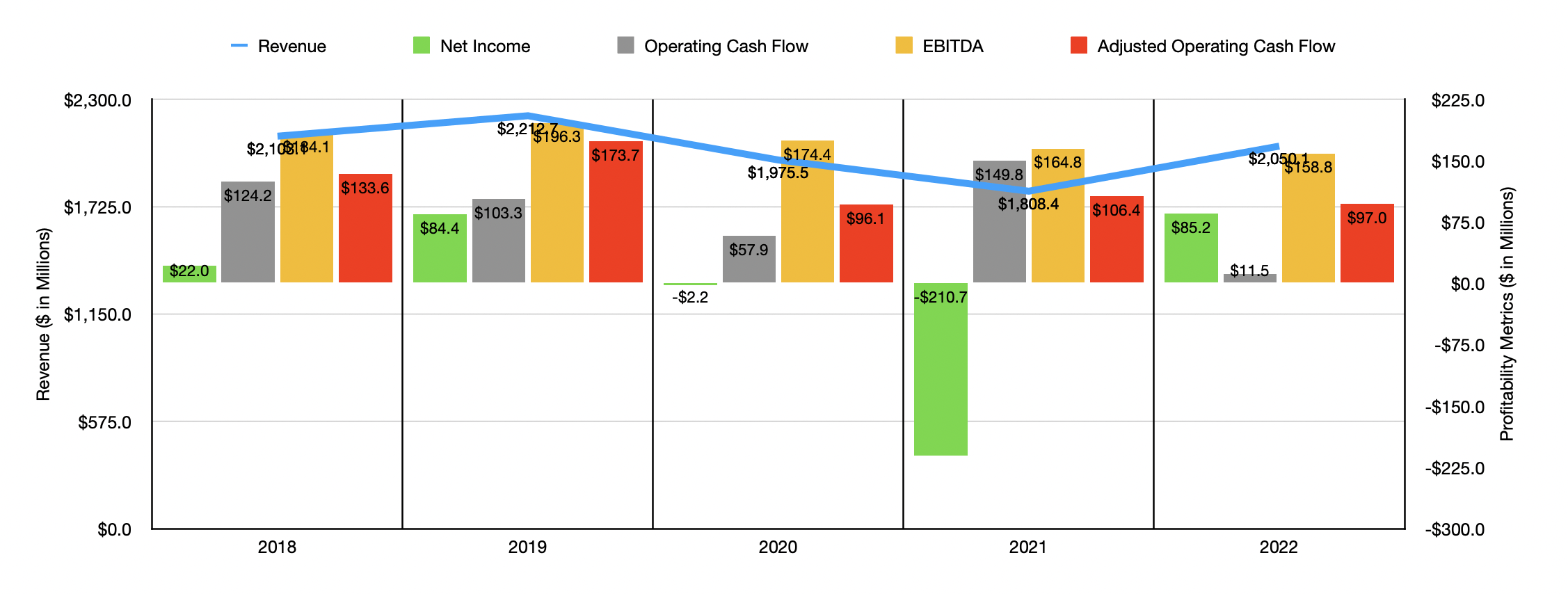

Over the past few years, the financial picture of the company has been somewhat mixed. Revenue has shown no clear trend, rising from 2018 to 2019 before dropping in 2020. In 2021, sales fell further, hitting $1.80 billion. This is down from the $2.21 billion in revenue generated in 2019. But then, in 2022, sales rebounded some to $2.05 billion. The increase in revenue, totaling about 13%, that was seen in 2022 came about as a result of higher sales volume and favorable pricing adjustments, the latter of which was in response to raw material price increases that the company had to deal with. Three of its four operating segments actually saw sales rise, with the Automotive segment being the weak spot.

Profitability has also been somewhat problematic for the business. Net income, for instance, rose from $22 million in 2018 to $84.4 million in 2019. In 2020, the company posted a loss of $2.2 million. And that loss grew to $210.7 million in 2021. Fortunately, 2022 proved to be something of a bright spot in this regard. Net income for that year came out to $85.2 million. Similar volatility can be seen when looking at other profitability metrics. Between 2018 and 2020, operating cash flow fell consistently, dropping from $124.2 million to $57.9 million. Cash flow spiked to $149.8 million in 2021 before plunging down to $11.5 million in 2022. If we adjust for changes in working capital, however, we do see some added stability. For instance, the decline from 2021 to 2022 was more modest, with the metric falling from $106.4 million to $97 million. Slightly more consistent has been EBITDA. That metric fell from $184.1 million in 2018 to $158.8 million in 2022, with only one year showing a deviation from the downward trend.

{kind=link}

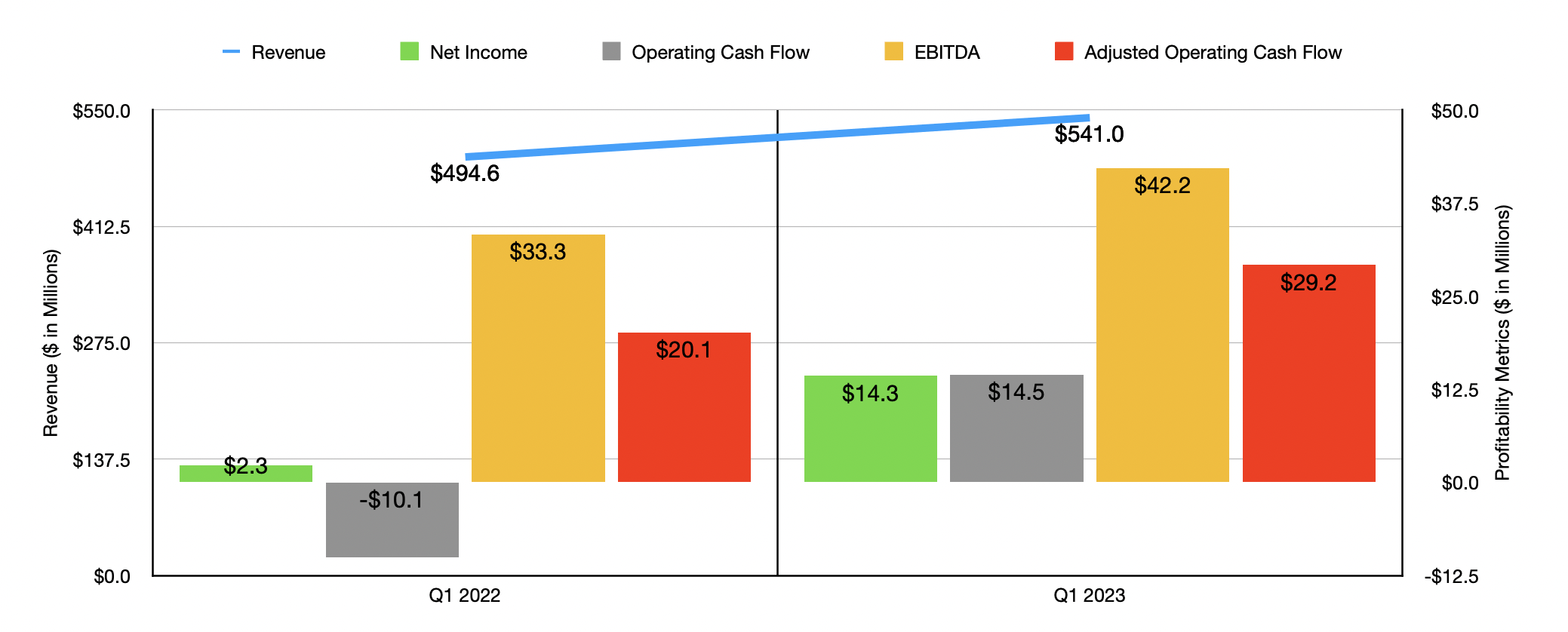

We do currently have some data covering the first quarter of 2023. At present, sales for the company are looking up, with revenue during the quarter totaling $541 million. That's 9.4% higher than the $494.6 million generated the same quarter last year. This increase, management said, is due largely to higher sales associated with Both of its segments. Revenue for the Climate Solutions segment jumped by 18.4%, while revenue associated with the Performance Technologies segment inched up just 2.4%. With this rise in sales, the company also saw improved profitability. Net income in the first quarter totaled $14.3 million. That compares favorably to the $2.3 million generated the same quarter last year. Operating cash flow went from negative $10.1 million to positive $14.5 million. If we adjust for changes in working capital, it still would have risen, climbing from $20.1 million to $29.2 million. Meanwhile, EBITDA for the company also increased, climbing from $33.3 million to $42.2 million.

When it comes to the 2023 fiscal year, management has provided some guidance . But I don't believe its top line guidance is all that valuable. I say this because management is currently forecasting revenue growth for the year of between 6% and 12%. This is a significant range with the spread between the high end and the low end totaling $123 million in all. Perhaps more reliable is the profitability guidance. At present, management thinks that EBITDA will be between $180 million and $195 million. No guidance was given when it came to operating cash flow. But if we assume that it will change at the same rate that EBITDA sure I did, then we should anticipate a reading this year of $114.5 million.

{kind=link}

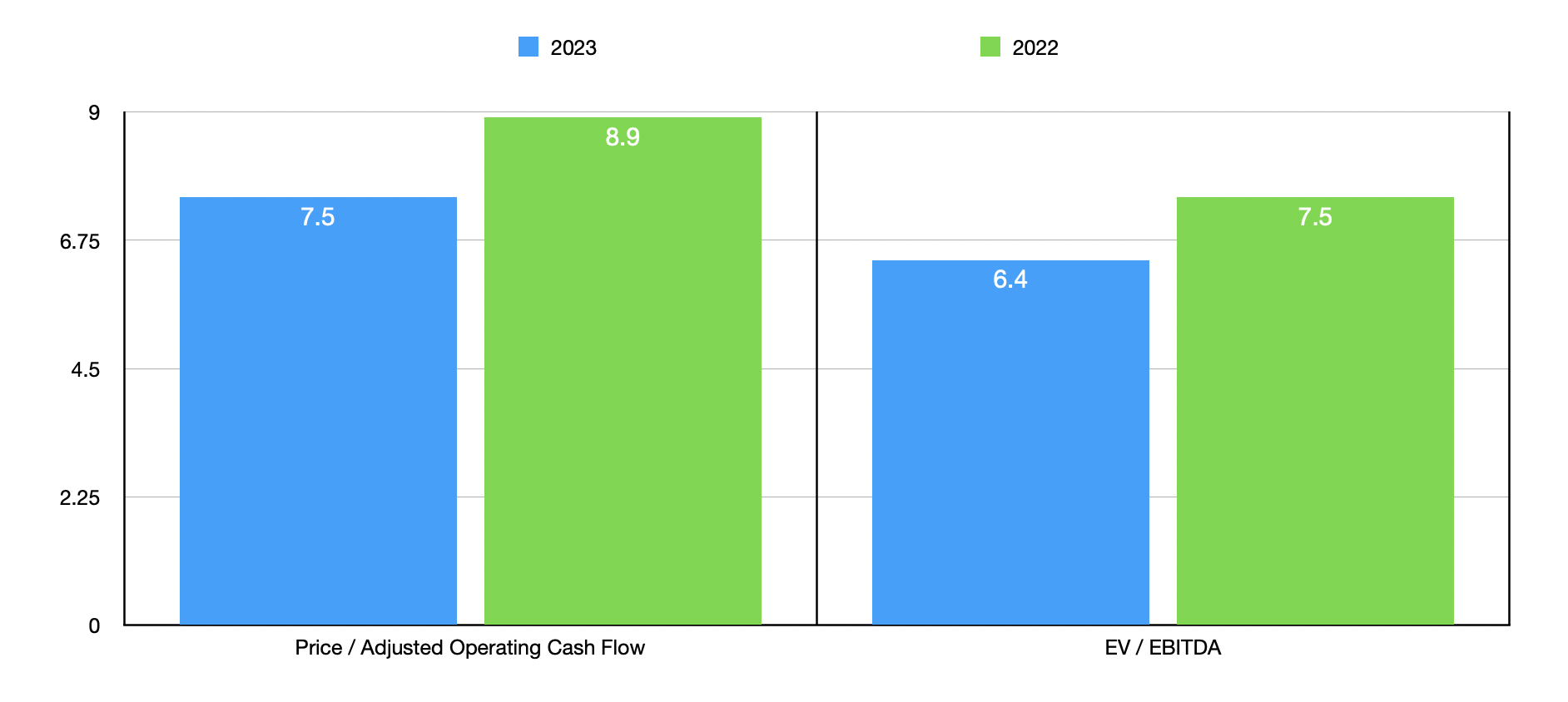

Using these figures, we can see that shares of the company are pretty cheap. The firm is trading at a forward price to adjusted operating cash flow multiple of 7.5. That's down from the 8.9 reading that we get using 2022’s results. And the EV to EBITDA multiple should come in at 6.4. That compares to the 7.5 reading that we get using results from 2022. As part of my analysis, I also compared the company to five similar firms. On a price to operating cash flow basis, only two of the five companies had positive results, with multiples of 1.9 and 6.9, for Garrett Motion (GTX) and Holley (HLLY), respectively. In this case, Modine Manufacturing was the most expensive of the group. Meanwhile, using the EV to EBITDA approach, the range should be between 2.7 and 18.4. In this case, two of the five companies were cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Modine Manufacturing Company |

| 8.9 |

| 7.5 |

| Standard Motor Products ( SMP ) |

| N/A |

| 8.5 |

| Holley ( HLLY ) |

| 6.9 |

| 7.6 |

| Stoneridge ( SRI ) |

| N/A |

| 18.4 |

| Garrett Motion ( GTX ) |

| 1.9 |

| 2.7 |

| Motorcar Parts of America ( MPAA ) |

| N/A |

| 5.7 |

Takeaway

As a value investor, I'd like to see stability in the companies that I buy into. I don't mind a company that is facing a difficult time. But prior to that difficult time, I still like to see some sort of favorable trend. When I don't see that, it suggests to me that the company might warrant some discount compared to other firms. And that is precisely what we get right now, given how cheap shares are trading at the moment. In all, I don't see this as a particularly appealing prospect given the company's historical track record. And even the guidance for this year seems somewhat unreliable. Because of this, I've decided to rate the business a ‘hold’ for now.

For further details see:

Modine Manufacturing: Cheap For A Reason