MOD - Modine Manufacturing Stock Now Has Even Bigger Potential Upside

2023-11-07 20:40:04 ET

Summary

- Modine Manufacturing Company, with a market cap of $2.2 billion, specializes in thermal management solutions. It's been one of the best 'Buy' calls of mine on Seeking Alpha so far.

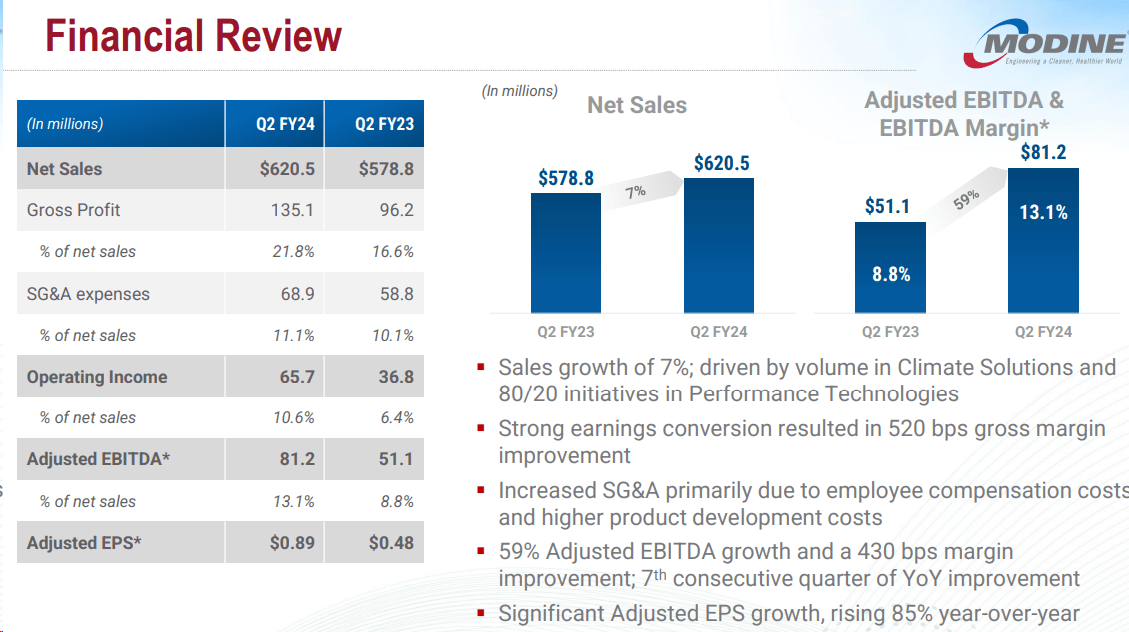

- In Q2 FY2024, MOD experienced a 7% revenue increase, and their adjusted EBITDA improved by 59% with a 13.1% margin.

- The rather cautious guidance led to a slight correction in the stock, even though the company beat EPS and sales consensus by a margin.

- In the base case scenario, the upside potential is 64.67% in 2 years, based on my calculations.

- Therefore, I reiterate my previous 'Buy' rating and expect MOD to go much higher in the next 2 years.

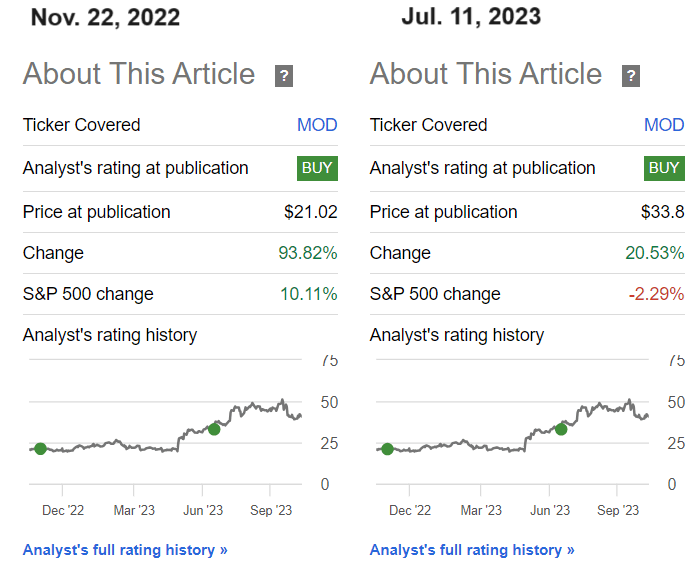

Since I started covering Modine Manufacturing Company ( MOD ) here on Seeking Alpha in November 2022 , I have only written 2 bullish articles on the company, both of which have far outperformed the broad market, making MOD one of my most successful 'Buy' calls on the platform.

{kind=link}

In the last article, I assumed that MOD theoretically has every chance of achieving a return of over 40% in the next 1-2 years thanks to the changing market landscape and the strong tailwind from the switch from ICE to electric vehicles. Only 4 months have passed since that statement was made and half of the projected growth potential has already been exhausted. As the company just released its Q2 2024 report a few days ago, I decided to test the strength of my earlier thesis: Does it still make sense to buy MOD at the current, already high share price level?

Financials And Prospects

Modine Manufacturing Company, with a market cap of $2.2 billion, specializes in thermal management solutions. They provide a wide range of environmentally responsible products and technologies that enhance indoor air quality, conserve natural resources, reduce emissions, and facilitate cleaner vehicles. Their customer base is diverse, serving HVAC&R OEMs, construction professionals, heating equipment wholesalers, industrial and agricultural equipment OEMs, as well as automobile, truck, bus, and specialty vehicle OEMs. The company is proactive in addressing changes, including new regulations and the growing demand for sustainable technologies driven by stricter emissions, fuel economy, and energy efficiency standards.

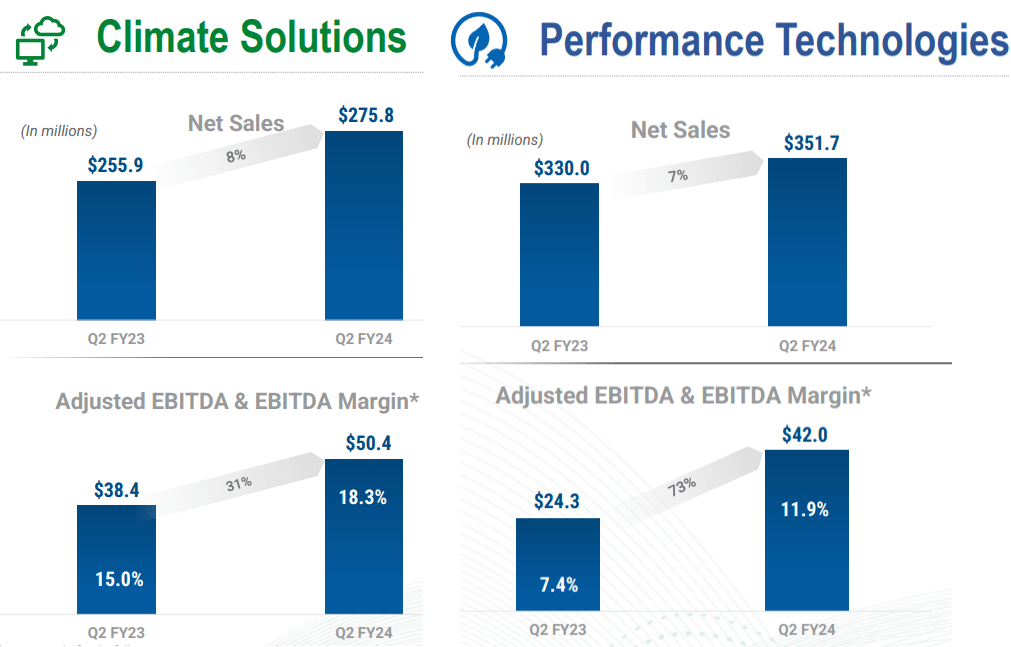

In Q2 FY2024 MOD achieved a 7% increase in revenue, with particular growth in their Climate Solutions and Performance Technologies segments. Adjusted EBITDA improved significantly, up 59% from the previous year, with an EBITDA margin of 13.1%.

{kind=link}

In the Climate Solutions segment, they saw an 8% revenue increase, driven by growth in data centers, resulting in an adjusted EBITDA margin of 18.3%. According to the management commentary during the latest earnings call , MOD expects some fluctuations in data center volume in the coming quarters, but the executive team continues to focus on key customer relationships and is developing new cooling solutions to meet future demands.

Modine's data center business has experienced substantial growth, with revenues more than doubling from the previous year. They have a significant backlog of projects, which provides stability despite fluctuations in quarter-to-quarter revenues.

Their HVAC&R business reported a modest revenue increase, and they are cautiously optimistic about the heating market. The Performance Technologies segment delivered an impressive 7% sales growth, with a strong focus on higher-margin businesses and continued progress with their 80/20 initiatives. They have divested non-strategic businesses in Germany and are actively adjusting their cost structure.

I see that Modine's business margins grew significantly faster in Q2 FY2024 than I had initially expected. At the same time, we are comparing the Q2 FY2023 results with the period when the effect of the coronavirus in Modine's business was already played out, i.e. we do not have a low base effect when comparing margin changes.

{kind=link}

In Q2 Modine achieved robust free cash flow of $58 million, mainly driven by increased earnings. Their net debt decreased by $63 million YTD, with a $43 million reduction during the quarter, resulting in an improved leverage ratio from 1.1x to 0.8x. Additionally, they restarted their share repurchase program, buying back 200,000 shares to offset dilution. From what I see, their balance sheet remains strong and well-positioned to support both organic growth and potential acquisitions in the future.

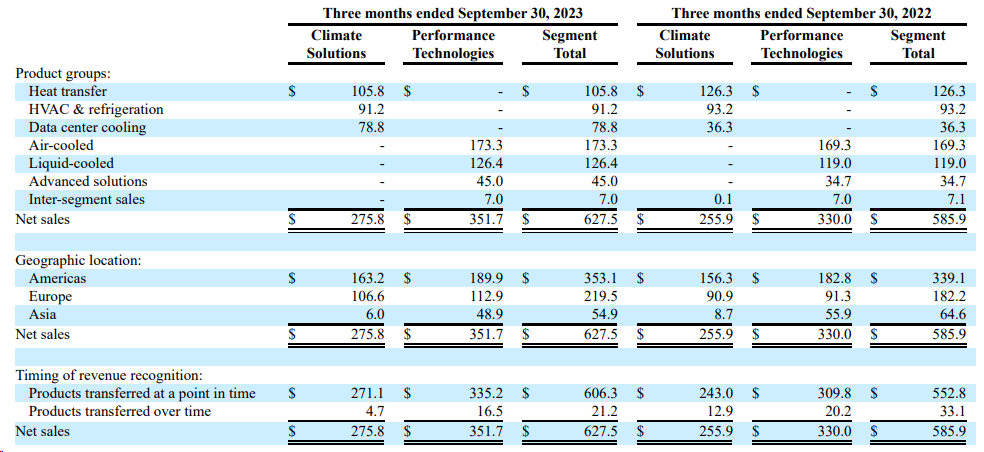

If we take a closer look at the sales growth for specific products, we will see that MOD will most likely place a greater emphasis on servicing data centers, as this is where the main growth comes from.

{kind=link}

According to Mordor Intelligence , the data center cooling market is currently valued at ~$16.56 billion and is projected to reach approximately ~$34.51 billion in the next 5 years, growing at a CAGR of 15.82% during this forecast period. The increased demand for data centers is primarily driven by the growing computational requirements of AI and media applications, leading to a significant expansion of data center infrastructure. In my opinion, this creates favorable conditions for the development of the MOD business.

Speaking of other MOD's segments, it's important to note Modine's Performance Technologies segment, which is experiencing growth in its EV systems and components, offering products for electric vehicles. They are expanding production to accommodate increased volumes in Europe, reflecting the growing market for electric vehicles and the transition away from internal combustion engines.

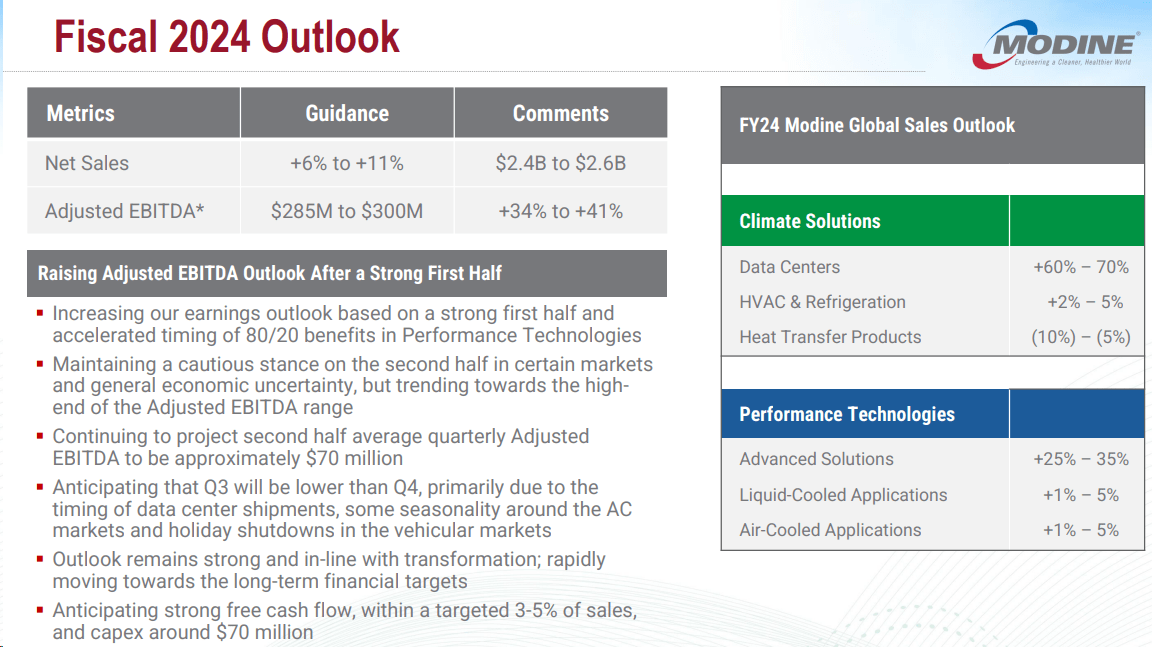

Modine's management decided to increase its earnings outlook due to a strong 1H FY2024 and accelerated 80/20 benefits in the Performance Technologies segment. They maintain a cautious stance for the 2H but expect to trend towards the higher end of the Adjusted EBITDA range. Q3 is projected to be lower than Q4, primarily due to the timing of data center shipments and seasonality in certain markets. But their outlook remains in line with their long-term targets, anticipating strong free cash flow (3-5% of sales) and CAPEX of around $70 million.

{kind=link}

I have not seen any clear red flags in the company’s reporting. On the contrary, MOD's business is accelerating both in terms of growth and margins. However, the rather cautious guidance led to a slight correction in the stock, even though the company has significantly outperformed Wall Street's consensus figures for earnings per share and sales.

Seeking Alpha

So should potential investors consider MOD as a long-term 'Buy'? Let's first take a look at the valuation.

The Valuation

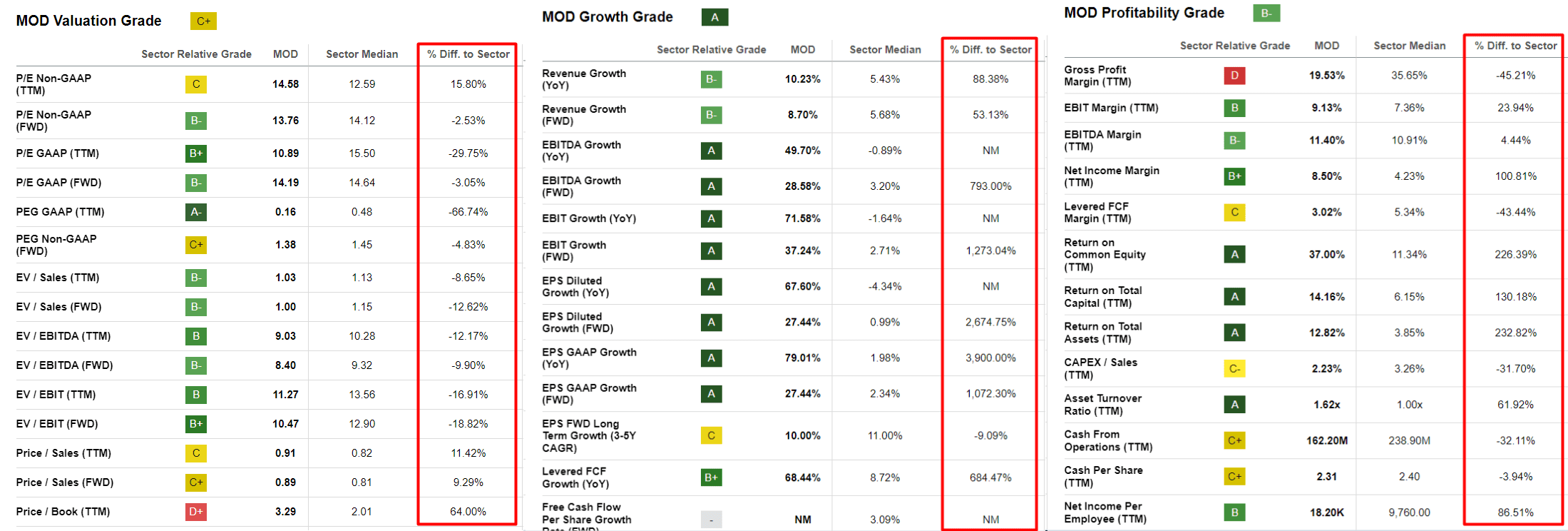

According to Seeking Alpha Quant System , Modine shares now look slightly more expensive than 6 months ago. But the deterioration of the rating from "B" to "C+" does not look so critical if we consider that the share price has doubled in the last six months.

Seeking Alpha's Quant System, author's notes

When I think in the context of the Consumer Discretionary sector , of which MOD is a part, I realize when comparing profitability and growth metrics that MOD's average discount in key multiples (~10-15%) is still unreasonably high because the company is growing much faster and, as we recall, is experiencing margin expansion that will most likely continue.

{kind=link}

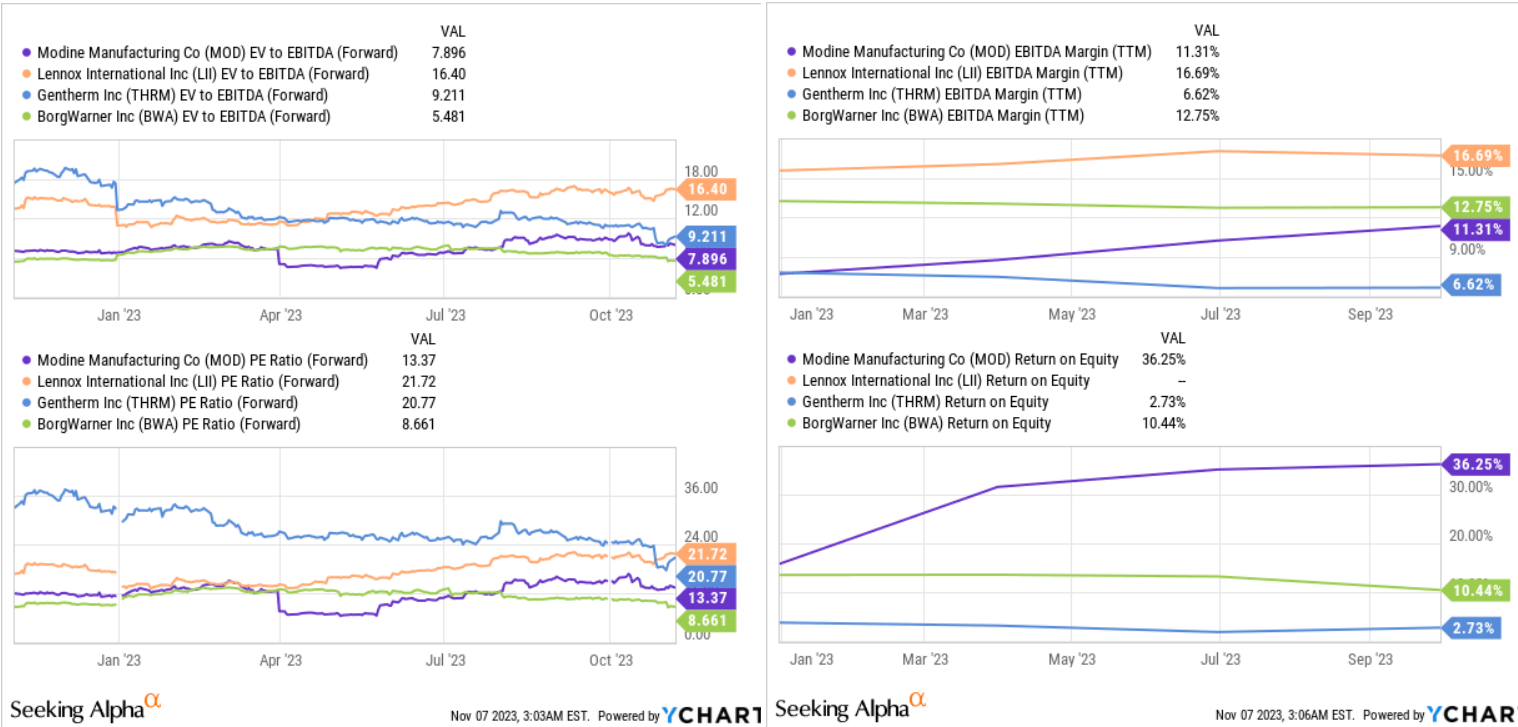

At the same time, MOD appears to be undervalued compared to its direct peers in terms of next-year EV/EBITDA and P/E ratios, while its TTM EBITDA margin is rising the fastest in the sample and its TTM ROE significantly exceeds that of the peer group.

{kind=link}

Wall Street's forecasts for MOD's EBITDA over the next couple of years have risen steadily despite the firm's management being relatively cautious recently:

If the consensus on MOD's EBITDA in 2 years is correct and the company manages to maintain and slightly improve its EBITDA margin (which is generally now in full swing), then instead of a 10-15% discount, I expect to see a premium of at least the same magnitude. At a projected EBITDA of $338.75 million in 2 years and an EV/EBITDA of 11x (including the premium I talked about above), Modine should be worth ~$3.5 billion in equity value after deducting the net debt of $222 million. That's my base-case scenario. It's important to keep in mind that Modine continues to reduce its net debt while reducing the number of shares outstanding, which also has a positive impact on the stock's growth. But anyway, in the base case scenario, the upside potential is 64.67% in 2 years, based on my calculations.

The Bottom Line

Everything you've just read does not mean that MOD is without risks. Modine, a thermal management solutions provider, heavily relies on the automotive industry for its financial performance, making it vulnerable to industry downturns. Operating internationally in regions like China, Mexico, and Europe exposes the company to economic and political risks, including currency fluctuations and tariffs. Supply chain disruptions, whether from natural disasters or political instability, could increase costs and hinder meeting customer demand. Also, strong competition in the thermal management sector and the need to stay technologically relevant through research and development are additional factors to keep in mind.

Despite the above risks, I believe MOD is a very high-quality small-cap stock that has been unfairly ignored by market participants following the Q2 FY2024 release. The company's business is growing and continues to develop qualitatively despite the headwinds from the automotive industry. The optimization of business processes according to the 80/20 principle really seems to be working. At the same time, it cannot be said that MOD has become more expensive in the last six months, during which the share price has doubled. As my calculations show, the upside potential has only increased. Therefore, I reiterate my previous 'Buy' rating and expect MOD to go much higher in the next 2 years.

Thanks for reading!

For further details see:

Modine Manufacturing Stock Now Has Even Bigger Potential Upside