WPC - Modiv: Might Be Moving In The Right Direction

2023-08-18 14:17:43 ET

Summary

- Modiv is an industrial REIT that wants to switch their focus purely to owning industrial manufacturing properties in the USA.

- To follow this strategy the company recently disposed of non-industrial assets and acquired more industrial manufacturing properties.

- My analysis leads me to a hold rating.

Dear readers/followers,

Industrial REITs play an essential part in the modern economic system by facilitating the transportation of goods worldwide. These characteristics, which serve as the foundation of the supply chain, have taken on new importance in the wake of the explosive growth of e-commerce and the evolution of customer preferences. The increased need for adequate storage and distribution facilities has pushed industrial real estate into the spotlight and made industrial REITs a top choice for investors looking to gain exposure to this industry. Therefore, I want to go over an industrial REIT Modiv Industrial (MDV), which has recently published its quarterly report for Q2 2023.

Overview

As I mentioned before, Modiv invests in industrial manufacturing facilities, via long-term net leases, to companies in the USA. The Gross Real Estate Value is $614 million. The company focuses on owning lasting properties which are able to generate stable income. These properties are leased to tenants that manufacture products critical to the U.S. economy such as food and beverages, infrastructure, and metals. Most of their investments belong to industrial manufacturing properties, but you can also see a few offices and one retail space in the portfolio. The REIT owns 45 properties overall in 16 states across the U.S. Modiv's tenants (currently 31) have a weighted average lease term of 14.3 years, which will provide the company with a steady stream of income for the next few years. One of its most prominent tenants, by the space leased, include Vistech (automotive component manufacturer), Lindsay (provider of infrastructure solutions), or the well-known 3M (MMM). Even though they only focus on industrial businesses, their tenant range is broad.

Modiv was founded in 2015 and went public at the start of 2022. After a huge spike (closing price of about $68) while listed on the New York Stock Exchange, the stock is continually below $20 and continues in decline. Current market capitalization equals $93.8 million. That is significantly lower compared to its peer's stocks, W. P. Carey Inc. (WPC) and Agree Realty Corporation (ADC), with their market capitalization reaching $13.8 billion and $5.8 billion, respectively. I will go further into this comparison later in the article.

{kind=link}

Second quarter results

Aaron Halfacre, the CEO of Modiv, shared the company's results and strategy. The strategy includes getting rid of non-industrial assets and acquiring industrial manufacturing ones. They recently disposed of 13 properties, 11 retail and 2 office, and sold them to Generation Income Properties (GIPR). This transaction cost GIPR $42 million at an exit cap rate of 7.55%. The transaction comprises $30 million in cash and $12 million in GIPR preferred shares, which will pay monthly dividends at a 9.5% annual yield. This repositioning is the long-term strategy of the company - having a super-majority of industrial assets. The CEO also believes that this process will continue until the complete disposition of non-industrial assets. The main focus is to achieve a scale of over $1 billion in gross industrial assets and become "the best pure-play net lease industrial manufacturing REIT. "

In spite of this strategy, Modiv Industrial purchased $29 million in industrial manufacturing properties in July 2023. The revenue increased by 16.7% YoY due to purchasing 16 industrial manufacturing sites over the last year. The FFO increased by more than 60% from $0.46 per share to the current $0.75. This revenue increase and interest expense decrease were due to unrealized gains on interest rate swap valuations. The AFFO is $0.31 per share, down from $0.35 per share in Q2 2022. This slight drop was caused by a higher straight-line rent adjustment.

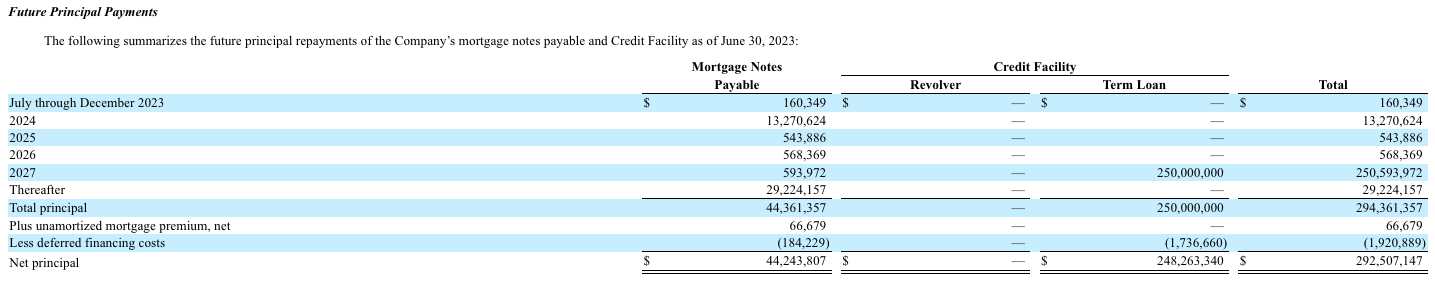

Now, a look at their balance sheet. Modiv has an outstanding net debt of $292.5 million with a net debt/adjusted EBITDA ratio of 7.8x (an increase from 6.6x in Q2 2022). The average interest rate is roughly 4.5% which is on the higher side. However, 93% of their debt is fixed, which is great. The 7% of the debt with floating rate is to be repaid this quarter, which will result in 100% of their debt being at a fixed rate. They have almost $10 million in cash and $129 million available on their revolver. They have little maturities in the next few years, which they should have no problem covering with their cash or by using their revolver. So overall, their balance sheet is pretty solid.

{kind=link}

The company is paying a monthly dividend of $0.09583 ($1.15 annually) per share, with a current yield of 9.25% and a payout ratio of 52%.

The promised comparison with two similar REITs is shown below. First, it's essential to note the primary distinctions between these funds. WPC's portfolio is reasonably diverse. The fund's primary concentration is in the United States, but some of the company's assets may also be in Europe, Canada, and Japan. WPC also leases warehouses, retail spaces, offices, and industrial assets. ADC, on the other hand, is wholly focused on retail across the United States. Modiv's FFO per share is significantly lower than that of the comparable funds ($0.31 vs $0.98 and $1.41, respectively). However, the P/FFO ratio (MDV - 6.55x), which indicates a cheap company in comparison to WPC (10.86x) and ADC (14.42x), is more appealing to investors. Finally, the dividend yield is attractive compared to its competitors, and it is given monthly, allowing the investor to redistribute their earnings more swiftly.

{kind=link}

Risks

As always, no investment comes without risks. Here are a few to consider in the case of Modiv.

Higher interest rates, which the company currently has, could be draining for MDV over time, especially if they use their revolver which has a really high interest rate of 6.7%.

Switching up their portfolio to purely industrial is going to be very costly, so the management needs to be cautious and have a good plan in process. If they fail to do, it would put the company under a lot of financial pressure.

Falling demand for distribution centers. Since there were countless distribution centers built as a result of the explosive e-commerce growth during the pandemic, it is possible that supply will be higher than demand over time. This would be problematic for MDV as they are moving towards a fully industrial portfolio and would suffer from vacancies.

Conclusion

Modiv is undeniably an intriguing stock. Their management has a defined vision and is focused on essential infrastructure in the United States. That means the corporation has little to worry about and can gradually raise its rent in response to the economic cycle. It's definitely worth keeping an eye on this REIT, if only for its P/FFO multiple and dividend yields, which have reached exciting levels. Moreover, the balance sheet looks pretty strong. However, I would like to see a few more quarters of results while they incorporate their strategy of focusing purely on industrial properties before taking a stance, which is why I rate the stock a HOLD for now.

For further details see:

Modiv: Might Be Moving In The Right Direction