PJT - Moelis & Company: Solid Company But A Rich Valuation

2023-11-23 23:05:34 ET

Summary

- Moelis & Company has significantly outperformed the S&P 500 since going public in 2014.

- The investment banking advisory industry is highly competitive, with low barriers to entry and low switching costs for customers.

- MC has used the recent industry downturn to significantly grow its managing director headcount and is poised to benefit once the industry recovers.

- The Company is currently trading at a high valuation relative to peers and its own historical norms, but the company now has significantly more earnings power than was the case in the past.

- I am initiating MC with a hold rating.

It is often challenging for companies that operate in highly competitive industries to generate attractive long-term returns for shareholders. However, there are exceptions to this rule for particularly well-run companies. Perhaps the best example of this is Southwest Airlines ( LUV ) which operates in the highly competitive airline industry. While LUV's recent performance has not been great, it is the only major U.S. airline that has not gone through bankruptcy. LUV has generated strong returns for early investors. Another example is Nucor ( NUE ), a company that operates in the ultra-competitive steel industry yet has been able to reward long-term holders with very compelling returns.

While less competitive than the airline business or steel business, the investment banking advisory industry is highly competitive. Despite operating in this highly competitive industry, Moelis & Company ( MC ) has generated a ~260% total return since going public in April 2014 compared to a ~190% return for the S&P 500 and ~139% return for the Financial Select Sector SPDR Fund ETF ( XLF ) during the same period. The competitive dynamics of the industry may make it hard for MC to continue outperforming the S&P 500 going forward.

Company Overview

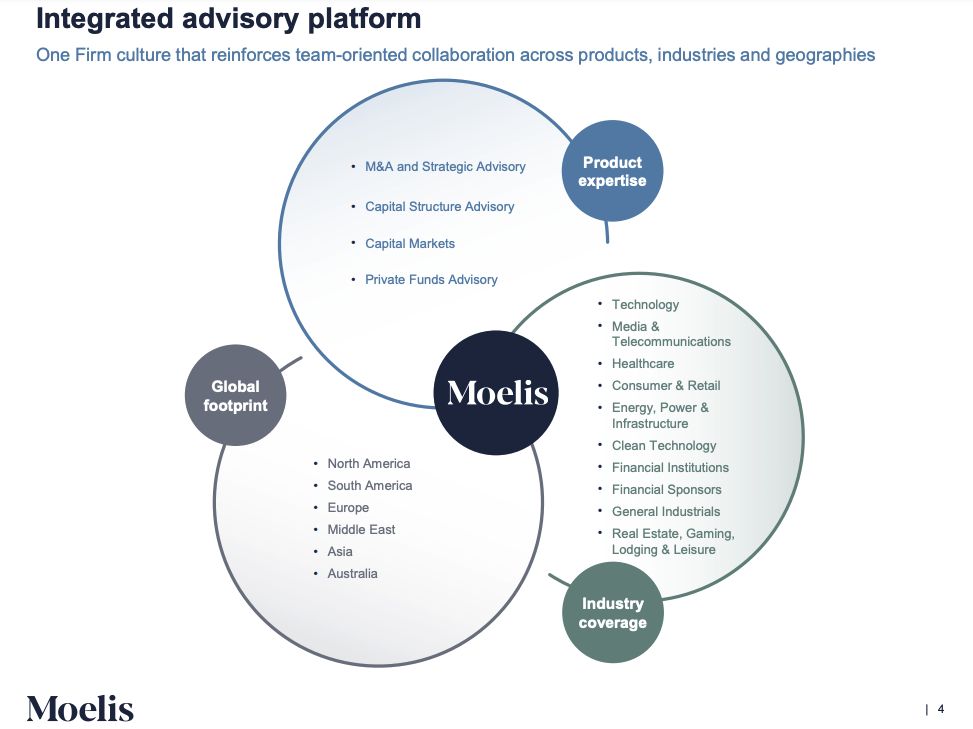

MC is a premier global independent advisory-focused investment bank. The company was founded by Ken Moelis and partners in 2007. MC has 23 locations globally and does business in more than 45 countries. Product coverage areas include M&A, Capital Structure Advisory, Capital Markets, and Private Funds Advisory.

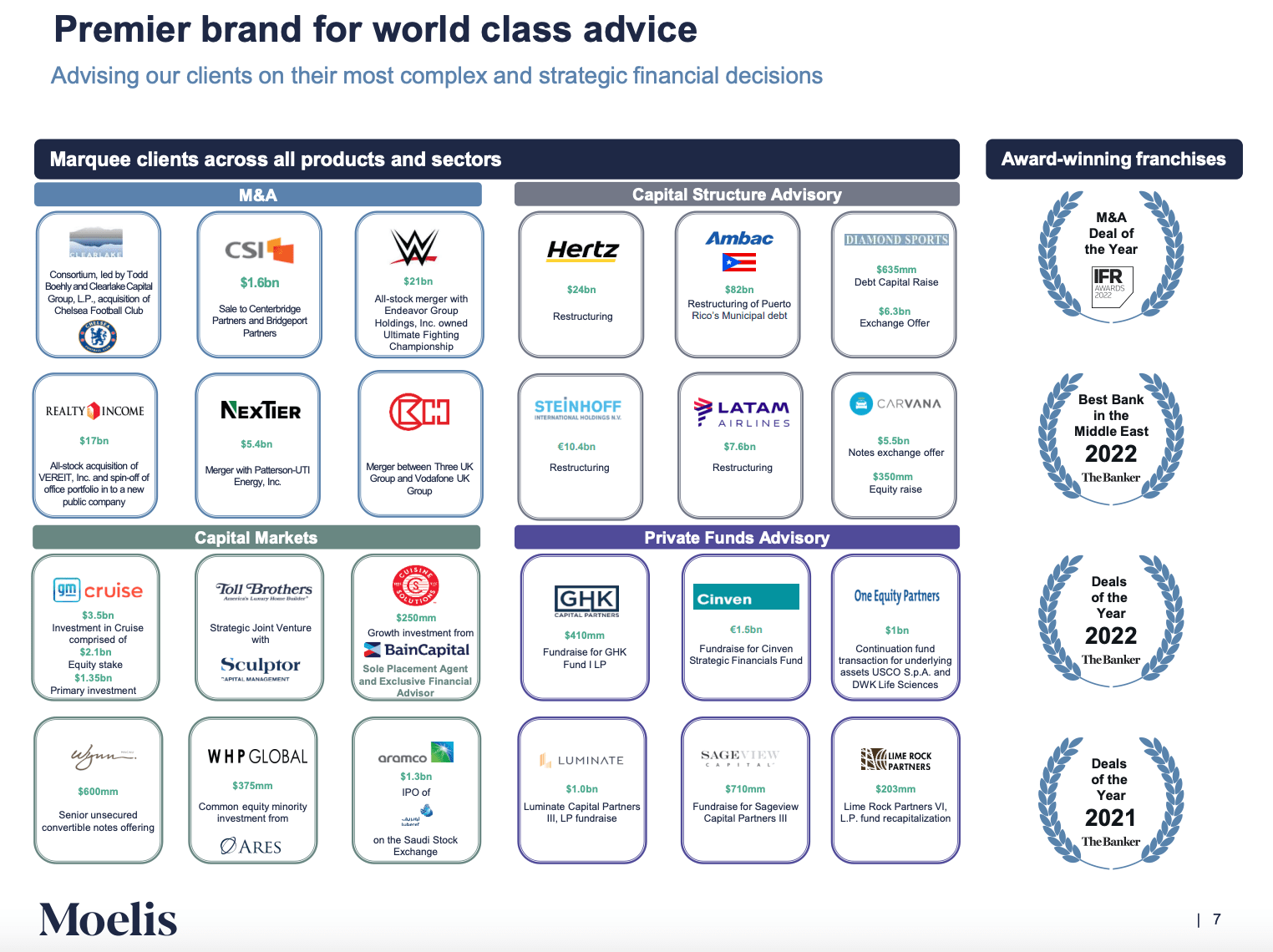

Despite its relatively small size with ~1,180 employees, MC has advised on a number of mega transactions including Hertz's $24 billion restructuring, Realty Income's $17 billion acquisition of VEREIT, and WWE's $21 billion merger with Endeavor Group Holdings.

{kind=link}

{kind=link}

Highly Competitive Industry Resulting in a Thin Moat

The investment banking advisory business is highly competitive. Some of MC's direct competitors include PJT Partners ( PJT ), Lazard ( LAZ ), Houlihan Lokey ( HLI ), Evercore ( EVR ), Perella Weinberg ( PWP ), Centerview Partners, and Lincoln International. MC also competes with large investment banks such as Goldman Sachs ( GS ), Morgan Stanley ( MS ), JPMorgan Chase & Co. ( JPM ), Bank of America ( BAC ), Barclays ( BCS ), UBS Group ( UBS ), and many other global banks.

In addition to being highly competitive, the industry has very low barriers to entry. Each year a number of top investment bankers leave their firm to start an independent advisory firm. In fact, MC traces its roots to just this phenomenon as Ken Moelis left UBS in 2007 to launch the firm.

Investment banks also face that the challenge of retaining customers as customer switching costs are very low. A company can hire MC for one transaction and then decide to use another investment bank for its next transaction without any friction.

Another challenge for companies operating in the investment banking advisory business is the competitive market for talent. The main cost for providing investment banking services is the cost of labor. MC spent ~63% of revenue on compensation and benefits in FY 2022. Other independent advisory firms tend to spend a similar amount on employee costs while larger full-service investment banks tend to spend slightly less. The highly competitive nature of the industry means that investment banks are in constant competition with each other to retain top talent.

The combination of a highly competitive industry, lack of barriers to entry, low switching costs, and high costs for talent has led independent advisory firms to operate at very low profit margins. As shown by the chart below MC and its independent advisory firm peers tend to have net profit margins in the high single digits to low double digits. Comparably, more diversified investment banks such as Goldman Sachs ( GS ) and Morgan Stanley ( MS ) which are engaged in lending, sales and trading, asset management, and wealth management have much higher profit margins.

Strong Historical Performance and Strong Balance Sheet

MC has posted strong financial performance since going public. Since going public, MC has grown revenue at an average annual rate of 15.7% though it has not been a smooth ride as the company's business is highly cyclical. Similarly, the company has grown EPS at an average annual rate of 34.4% but has experienced a lot of volatility along the way.

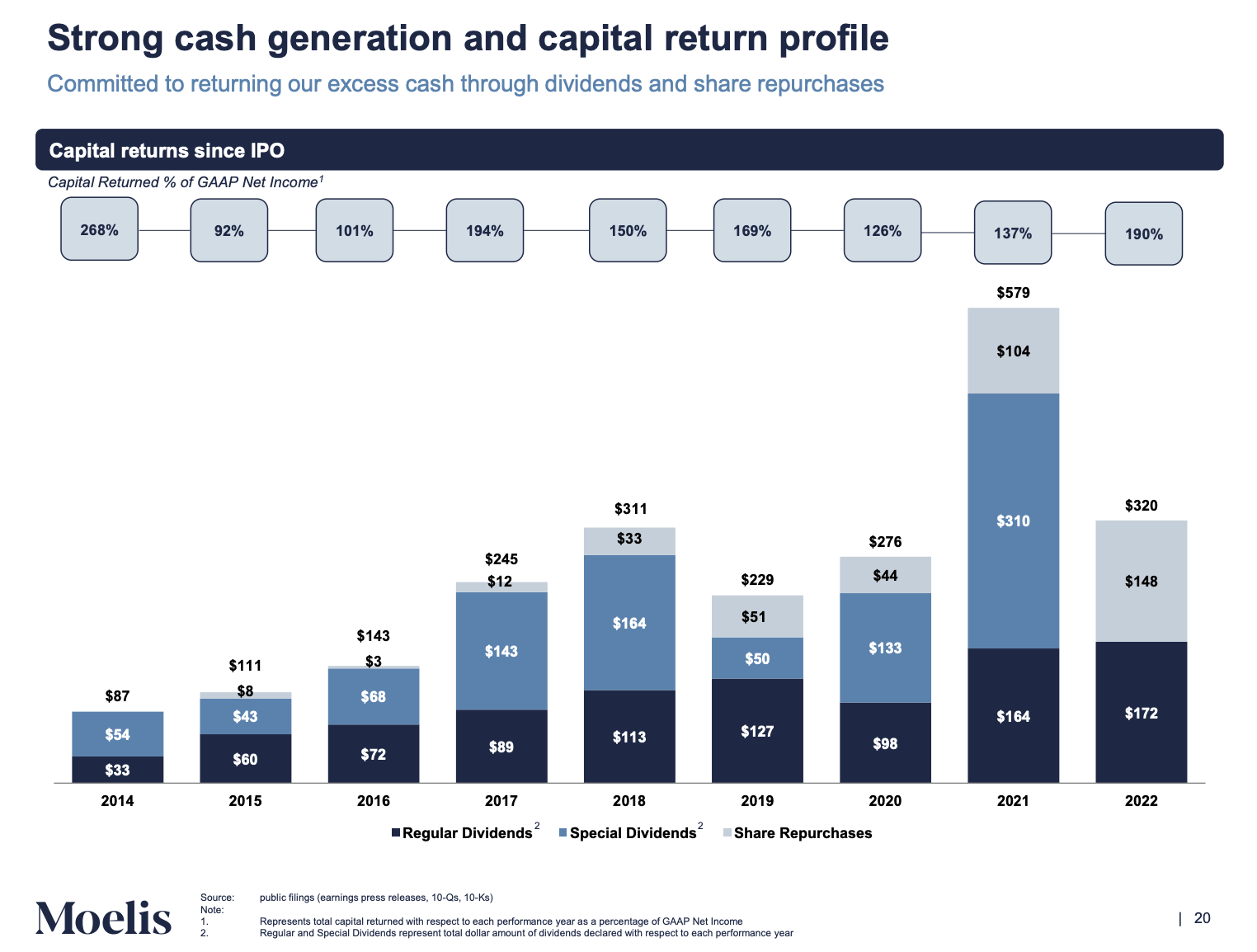

Strong financial performance has allowed MC to return a significant amount of capital to shareholders through repurchases and dividends. Since its IPO, MC has returned ~$2.5 billion to shareholders. For context, MC has a current market cap of ~$3.1 billion today.

MC has a very strong balance sheet with no long-term debt and ~$298 million of cash and liquid investments as of Q3 2023. The strength of MC's balance sheet is important given the highly volatile nature of the business and its high degree of economic cyclicality.

{kind=link}

Q3 2023 Earnings & Senior Talent Hiring

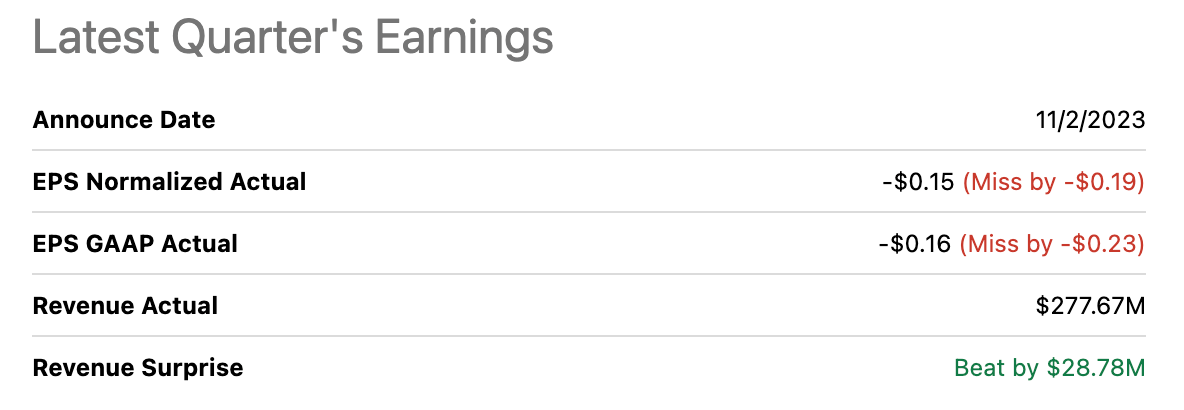

On November 2, 2023, MC reported Non-GAAP EPS of -$0.15 which missed consensus estimates by $0.19. Adjusted revenue came in at $277.7 million, up 19% vs the same period during the prior year, which beat consensus estimates by $28.8 million. The revenue increase was driven primarily by strength from the company's restructuring business but is not expected to recur during the next quarter.

For the first nine months of 2023, MC reported adjusted revenue of $645.2 million down 16% from the same period during the prior year.

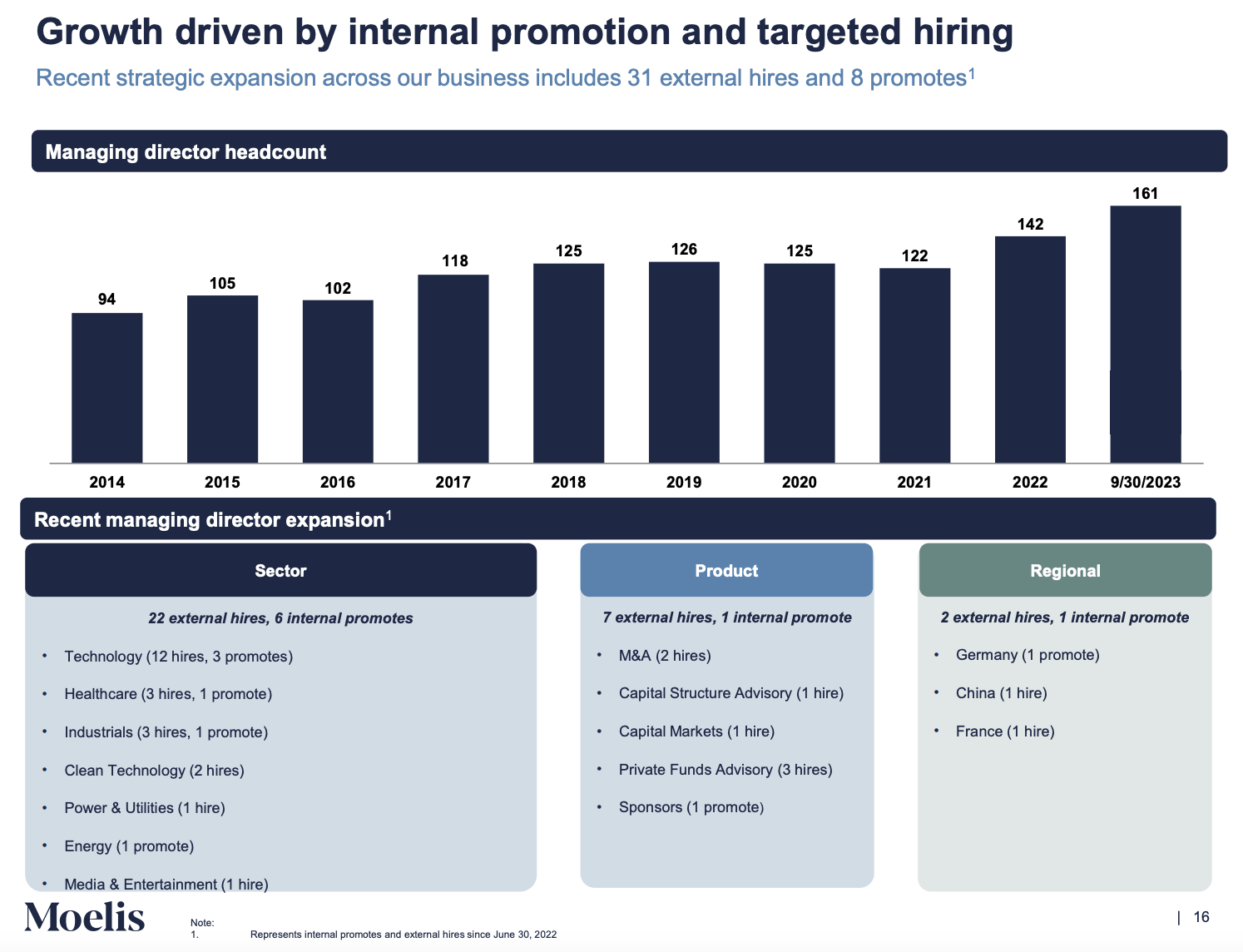

MC noted that it had hired 27 Managing Directors over the past year. MC CEO Ken Moelis added additional color on the new hires:

Over the last 12 months, we've hired 27 Managing Directors, while still managing overall headcount through targeted attrition. Although it is difficult to predict when the M&A business will recover, what we do know is that the cycle will turn and when it does, we are well positioned to capitalize on it for years to come. The investments we're making today have dramatically improved the firm's earnings power...

We hired 27 people in a year, it's almost -- it's more than 20% of the existing Managing Director base. And by the way, Devin, while we did that, you'll see that the headcount is only up 3% to 4%, at the end of the year. So, we actively managed a very significant amount of people out.

In April 2023, MC hired 11 Technology-Focused Managing Directors who formally worked at SVB Securities. This move represented a major investment by MC during what has been a down period for investment banking.

Historically, MC has generated $8 million to $12 million in revenue per managing director. Based on a current managing director count of 161, MC has potential to earn ~$1.6 billion (using a $10 million revenue per managing director number). This level of revenue compares to a record of $1.54 billion which was achieved in 2021 with 122 managing directors.

{kind=link}

{kind=link}

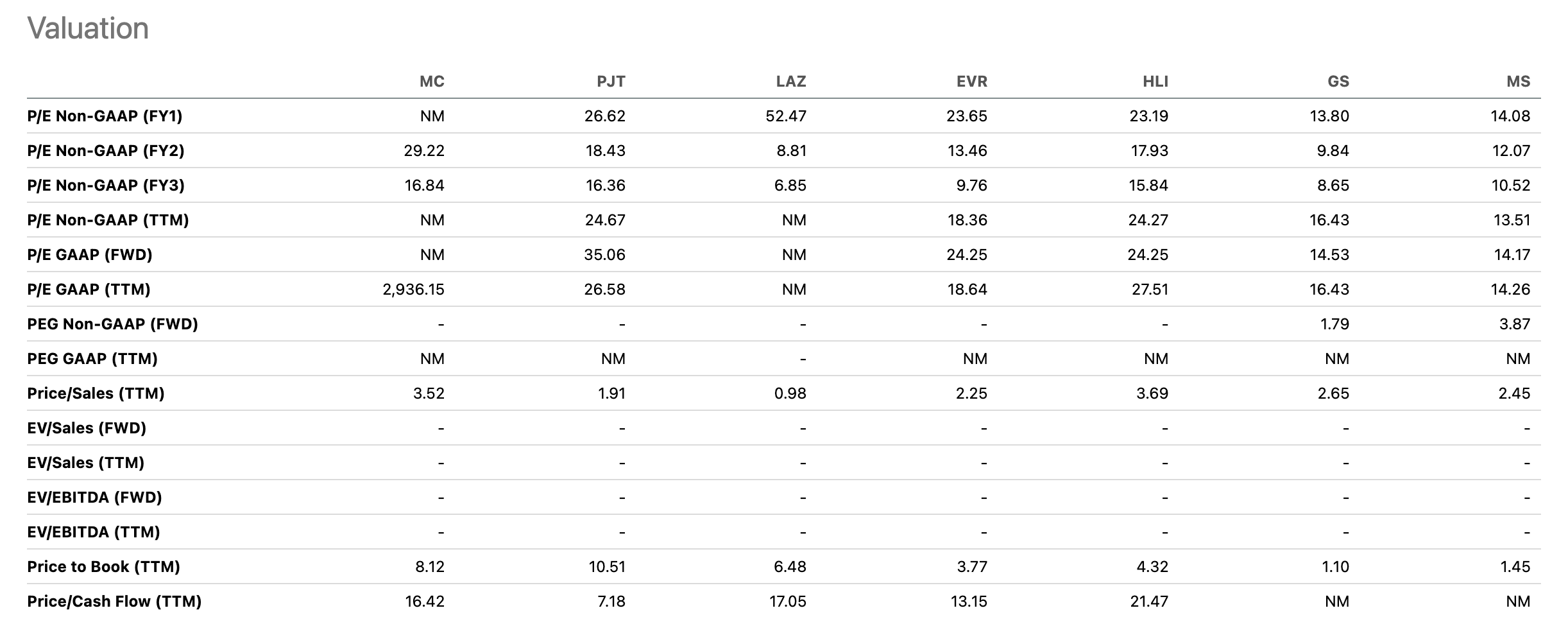

Relative Valuation Analysis

As shown by the table below, MC receives a D+ valuation grade from Seeking Alpha quant ratings. I am inclined to agree.

MC trades at 29.2x consensus FY 2024 earnings and 16.8x consensus FY 2025 earnings. Comparably, the S&P 500 trades at ~18.4x consensus 2024 earnings. However, given the highly volatile nature of MC's business, it also makes sense to consider that MC is trading at just 11.9x the average of 2020, 2021, and 2022 FY EPS.

MC is trading towards the upper end of the valuation range compared to advisory-only peers such as PJT, EVR, and HLI. However, MC is trading at a premium to more diversified investment banks such as GS and MS. While MC may be able to grow more quickly over the next few years, I believe GS and MS are higher quality businesses with a more defensive moat compared to MC.

MC has focused on using the recent investment banking downturn to invest in hiring additional key talent. The company has increased its Managing Director headcount by ~20% over the past year. Thus, MC has the potential to significantly grow earnings in the event that the investment banking business environment improves compared to more mature firms such as GS, MS, EVR, or HLI.

{kind=link}

Historical Valuation Analysis

MC is currently trading at the upper end of its historical valuation average both on a forward P/E basis and an EV to revenue basis. However, the company has experienced a significant decline in business over the past year due to cyclical headwinds.

Trailing 12-month revenue of $847 million compared to all-time high revenue of $1.54 billion achieved in FY 2021 and $985 million achieved in FY 2022. Given the recent increase in the managing director count, MC should be able to achieve significant revenue growth once the cycle turns.

Similarly, MC's forward EPS estimate of $1.53 compares to reported EPS of $5.83 in FY 2021 and $2.29 in FY 2022. Thus, once the cycle turns MC should experience significant earnings growth.

Conclusion

MC has delivered impressive results for shareholders and has significantly outperformed the S&P 500 and the financial sector more broadly since its IPO in 2014.

The company has been able to grow revenue and earnings but has experienced significant volatility due to high levels of cyclicality in the investment banking business.

MC has embarked on a major hiring spree over the past year and has increased its managing director base by ~20% to an all-time high level.

Currently, MC trades at a high valuation vs the S&P 500 and peers but has the potential to significantly grow earnings once the business environment improves. Given the company's strong history of delivering results, I believe it is likely that the company will be able to deliver strong results once the cycle turns. That said, the cycle has not yet turned and a prolonged or further economic downturn could prove especially challenging for MC to navigate given its increased hiring over the past year.

The combination of high levels of competition, low barriers to entry, high costs of talent, and low switching costs for customers make the investment banking advisory business a very challenging space to build a wide-moat business.

For these reasons, I rate MC a hold at current levels and will continue to evaluate the investment opportunity in the future. I would consider upgrading the stock if the overall investment banking business climate improves and MC's valuation picture improves.

For further details see:

Moelis & Company: Solid Company, But A Rich Valuation