MC - Moelis: Deteriorating Financials And Further Downside Ahead

2023-07-12 10:06:43 ET

Summary

- Moelis & Company is facing financial underperformance due to a decrease in investment banking activity, and its stock is significantly overvalued compared to peers.

- The company's revenues are increasingly susceptible due to a lack of geographic diversification and heavy exposure to the U.S. market, whilst also facing increasing costs following ambitious hiring.

- Management insider transactions show heavy selling year-to-date, and the sell-side community consensus is skewed to the downside.

Investment Thesis

Moelis & Company ( MC ) is suffering from rapidly deteriorating financials, as investment banking activity dries up in the current macroeconomic environment. However, their stock price is yet to reflect this and is significantly overvalued in comparison to peers. I believe that negative stock performance will materialize soon, as confirmed by the bearish outlook of the sell-side community and the recent selling transactions by management on their own stock.

Company Summary & Industry Outlook

Moelis is a boutique investment bank that provides financial advisory and corporate finance services to its client, generating fees on activities such as mergers & acquisitions, recapitalizations, restructuring, and capital raising. The firm is led by Wall Street billionaire, Ken Moelis, as their founder, chairman, and CEO of the firm. Since its inception in 2007, the firm has established a top tier reputation for its deal-making and in possessing elite bankers. However, the company's fortunes have turned for the worse in recent quarters. The market and economic uncertainty following the Federal's Reserve aggressive monetary tightening to combat high and persistent inflation is weighing down on deal activity. Whilst this is a market wide trend for this sector, Moelis' revenues and net income appear to be increasingly susceptible, as it does not have the business diversification of bulge bracket banks such as Bank of America ( BAC ) and Citi ( C ), who offer services beyond just pure investment banking.

{kind=link}

Global M&A Trends (PwC)

As per the recent study on M&A trends by PwC , we can clearly see the difficulties that firms such as Moelis are facing, as both M&A deal volumes and deal values have dropped since a peak in the second half of 2021. At the same time, debt issuance is also down due to the significantly higher interest rate costs that issuers are facing. This results in a shrinking pool of investment banking revenues and fees that Moelis can fight for. Whilst the stock performance year-to-date has been positive and has kept up with the S&P500, Moelis looks well overvalued and I believe the stock is exposed to the downside, considering its deteriorating financials and concentrated business activities, particularly in M&A.

Deteriorating Financial Results

{kind=link}

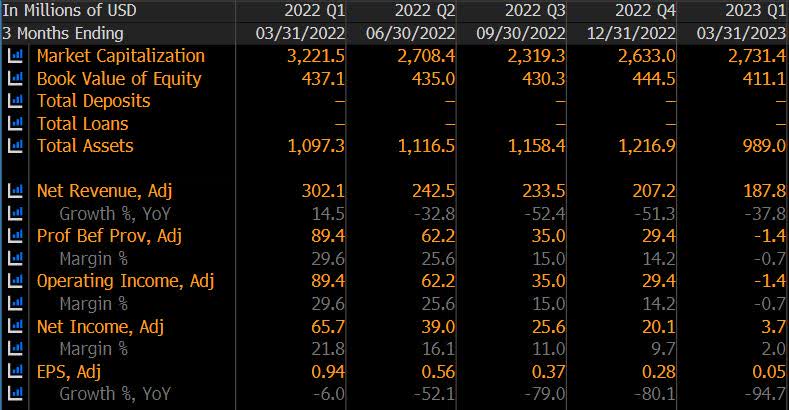

Moelis Financials (Bloomberg)

Moelis' financials in recent quarters make for tough reading. Total Revenues in Q1 23 dropped to $187.8 million , down ~9% from the prior period in Q4 22, and a stark ~38% from Q1 22. Net Income sank to $3.7 million, down from $20.1 million in the prior period. Worryingly, Operating Income Margin was -0.7%, a world away from last year's 29.6%. Unfortunately, Moelis is being hit by the double pain of lower revenues and higher expenses in their income statement.

At the same time, we can observe a few more concerning data points in their latest 10Q, as Cash & Cash Equivalents in Q1 23 were ~$135 million , down 35% from the prior quarter. The Investments line item on the balance sheet also dropped to ~$92 million, dow n from ~$265 million previously. Moelis posted a significantly negative Cash From Operations in the latest quarter.

Another risk to highlight in their financials, is the heavy exposure to the U.S. as their key revenue center, despite Moelis' branding as a global investment bank. In FY 22, over 85% of their revenues were generated in the US, making the bank much more susceptible to swings in the American economic cycle than other more geographically diversified banks.

{kind=link}

Geographic Revenue Analysis (Bloomberg)

The downward financial trend discussed above could be set to continue on both the top and bottom line. Revenues wise, the macroeconomic environment in the U.S. is expected to struggle to generate any meaningful GDP growth, with some economists even forecasting a recession. These conditions will impact the firm's ability to earn fees due to lower deal activity amidst this growing uncertainty. On the expenses front, Moelis has been pursuing opportunistic and ambitious hiring plans to further expand the quantity and quality of their staff. As per their April 26 press release , the firm doubled the size of their Technology team, adding 11 tech-sector Managing Directors from Silicon Valley Bank ((SIVBQ)), as well as other bankers joining other coverage teams from banks such as Credit Suisse ( CS ). Overall, there were approximately 150 Managing Directors at Q1 23, in comparison to 137 in Q1 22. Whilst this type of expansion may pay dividends in the future as the firm broadens their industry coverage and expertise, expenses will accelerate higher in the short to medium-term.

This view is shared by the consensus estimates on Bloomberg, with both EPS and Net Income forecasted to drop even lower in the Q2 23 results.

Consensus Estimates (Bloomberg)

Relative Valuation Looks Expensive

Given the poor earnings, the stock appears to be trading above fair value and warrants a lower price. Looking at the valuation metrics relative to peers on Seeking Alpha, Price-to-Earnings Ratio (GAAP TTM) currently sits 34.58x , at a significant premium to MC's 5 year average ratio of 17.24x, and far higher than the sector median of 9.24x. At the same time, the Price-to-Book Ratio ((TTM)) is 7.43x, in comparison to the median of 1.02x.

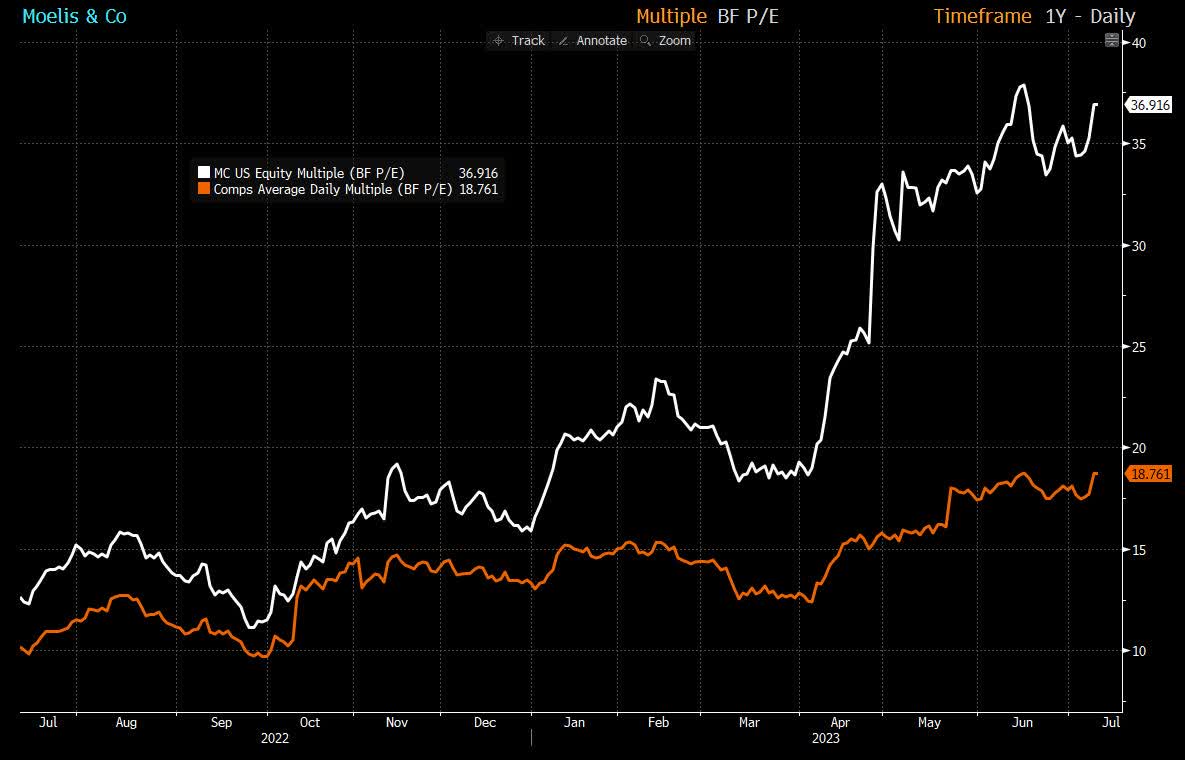

Looking at the Bloomberg Blended Forward P/E Ratio, which uses a time weighted average of fiscal year 1 and fiscal year 2 forward estimates, we can see the dramatic premium that MC currently enjoys over a peer group consisting of other U.S. M&A Boutique banks, such as Evercore and PJT Partners. The stock price should not be able to maintain this divergence for much longer, especially if Q2 23 results miss expectations, and we should see MC stock drift lower.

{kind=link}

P/E Relative Valuation (Bloomberg)

Uninspiring Management Transactions

Looking at the Bloomberg Management Insider Transactions, we see heavy selling from executive staff year-to-date. Over the period, Net Buys represented ~$244,000 worth of shares, whilst Net Sells were ~$427,000. This indicates a bearish view on their own stock and reinforces my outlook that the company is overvalued and due for a downward correction, especially as we are trading at prices that are in line with the heavy selling concentration seen at the start of the year.

{kind=link}

Management Insider Transactions (Bloomberg)

Bearish Analyst Recommendations

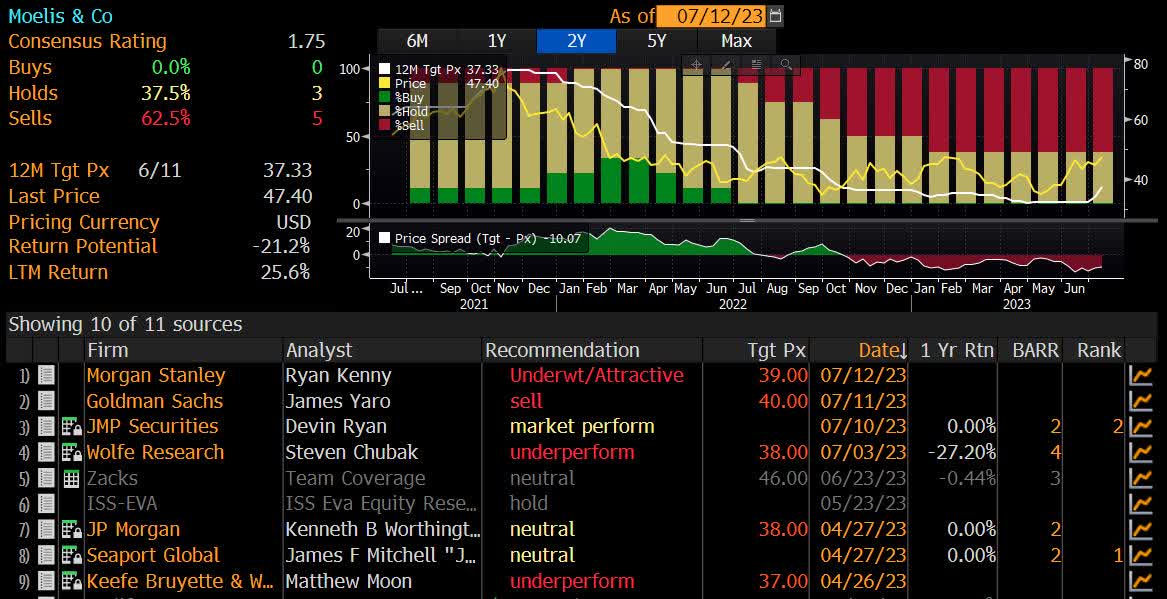

Finally, I look to confirm my assessment by comparing it to the consensus sentiment on the sell-side. Looking at the Bloomberg Analyst Recommendations from equity research at banks and brokers, none of the contributors see Moelis as a "BUY" recommendation. The majority of survey respondents issued a "SELL" rating and the rest were "HOLD". There is also a consensus 12 month target price of ~$37, which implies a downside of ~21% from the current stock level.

{kind=link}

MC Analyst Recommendations (Bloomberg)

Risks

MC stock looks set to face serious headwinds from the macroenvironment weighing on revenues, as well an expected jump on their cost base. The risks to my short thesis are that if the U.S. economy performs better than expected and the Federal Reserve manages to maneuver a "soft landing", this could lead to improving economic conditions in the medium to long-term. As a result, this would lead to a pickup in M&A activity and help lift fee generation opportunities for MC. Nevertheless, the expensive forward-looking valuation, management positioning, and analyst recommendations discussed above do not provide for much confidence in more positive prospects.

In Conclusion

Moelis is a reputable investment bank that is facing tough conditions from the depressed mega deal activity in the market amidst economic uncertainty. Their financial results have notably deteriorated in the past quarters, and I expect this to continue further, especially due to their business concentration in the U.S. market. The stock trades at unjustified valuations and we should expect a downwards move, as affirmed by the sell-side community's outlook and target prices.

For further details see:

Moelis: Deteriorating Financials And Further Downside Ahead