SF - Moelis: Quality IB But Far Too Expensive

2023-04-20 06:59:12 ET

Summary

- Moelis & Company is an investment banking advisory firm.

- Current market and economic conditions suggest Moelis will struggle in the coming quarters as market activity remains low.

- The fundamentals of the business are attractive, with big project wins, MD hires, and superior margins. We are unlikely to see the benefit of this in the near term.

- Moelis is trading at a 10x premium to a cohort of IB peers. This looks unwarranted given that continued struggles are ahead.

Investment thesis

Our current investment thesis is:

- Moelis is a quality business, with strong recruitment driving its market share growth in the last decade.

- A strong restructuring practice could help the business hedge against economic downturns long-term, with the business becoming a well-rounded IB.

- Moelis looks to be tied to market conditions which are only declining, with our outlook suggesting a tough 12-18 months for the business.

- Moelis is trading at a large premium to its peers. Although this is partially warranted, the degree looks unreasonable.

Company description

Moelis & Company ( MC ) is an investment banking advisory firm that provides advisory services in areas such as mergers and acquisitions, recapitalizations and restructurings, capital markets transactions, and other corporate finance matters.

Share price

Moelis' share price has experienced a noticeable degree of volatility in the last decade, gaining over 40%. This volatility has an uncanny correlation with financial performance, with Moelis experiencing periods of substantial gain as it has grown.

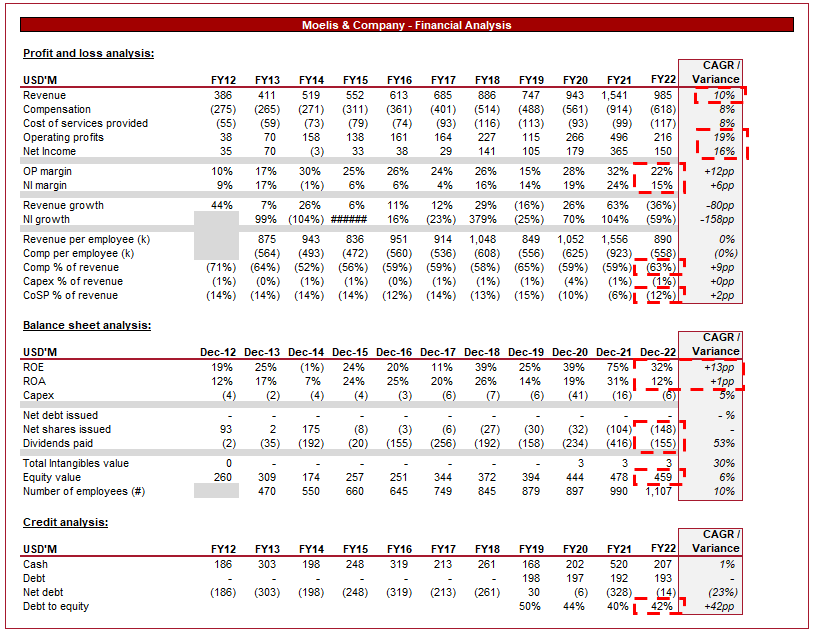

Financial analysis

Moelis' financials (Tikr Terminal)

{kind=link}

Presented above is Moelis' financial performance for the last decade. The business has done well to achieve growth but continues to experience volatility in earnings.

Revenue

Moelis' revenue has grown at an impressive rate of 10%, driven by several factors, primarily the development of its expertise and market positioning.

Current economic conditions are the primary reason why Moelis has experienced a 36% decline in revenue and why the coming 12-18 months may continue to be tough. The two key issues are recession fears and heightened interest rates. Recession fears make buy-side investors more hesitant to transact as a recession usually means a decline in company performance, as well as its valuations. Secondly, an increase in interest rates means the cost of capital is increasing, resulting in greater difficulty with financing transactions and a reduction in the valuation of future cash flows. As a result of this, buy-side investors are looking for a discount relative to the valuation seen before the rate hikes. Conversely, the sell-side is reluctant to sell during what is perceived to be a short period of heightened interest rates while inflation comes down. These two conflicting attitudes contribute to a widening of the valuation gap, making it far more difficult to get transactions across the line. As a result of this, M&A volume declines, reducing revenues. As the following graph illustrates, we have seen declining M&A value since mid-2021.

M&A by quarter (Dealogic)

The question then becomes when will rates come down? Our view is that a decline will only begin in 6-12 months, as inflation is looking difficult to battle. This suggests an extended period of softening advisory work, making it difficult for Moelis to achieve growth.

Thinking longer term, we believe transaction volume will bounce back at a higher level than seen in the last decade. This is because PE firms have record levels of dry powder , which is uninvested client money. This needs to go to use, otherwise leads to questions about why they are raising money in the first place. As a result of this, we will see transactions pick up as this dry powder value unwinds. This will take an extended period of time as firms are still fundraising and will to in larger numbers once market conditions improve. The key for Moelis is continuing to win work, which its track record suggests will occur.

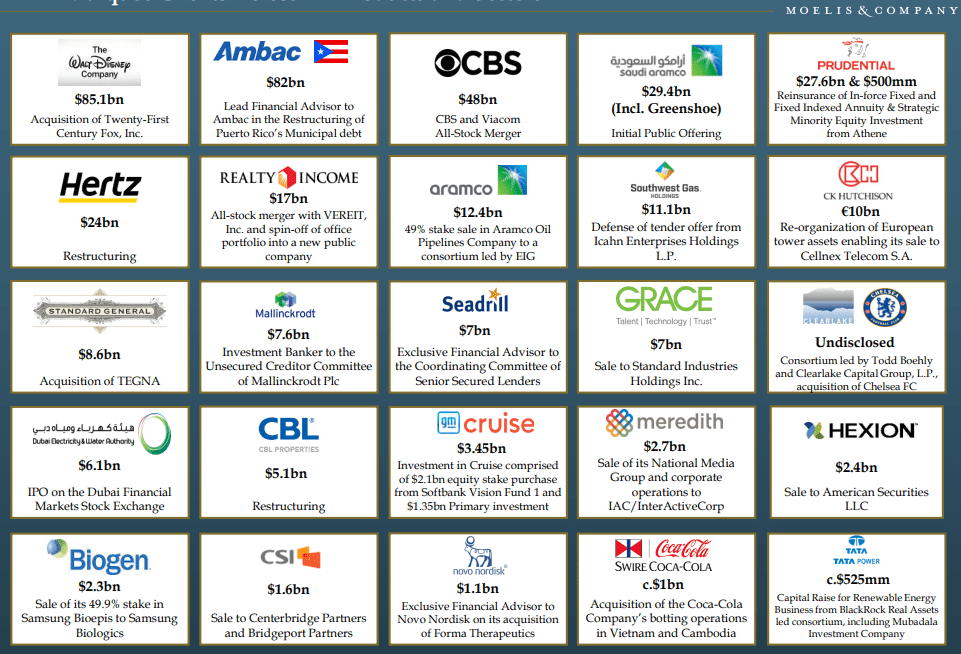

Moelis has done a good job of recruiting high-value bankers from the bulge bracket and elite boutique banks. The key to driving volume in the advisory space is having quality credentials and client connections, both of which come with the recruitment of experienced individuals. Despite trading since 2007, the business has an impressive resume of prior transactions.

Moelis - select transactions (Moelis)

{kind=link}

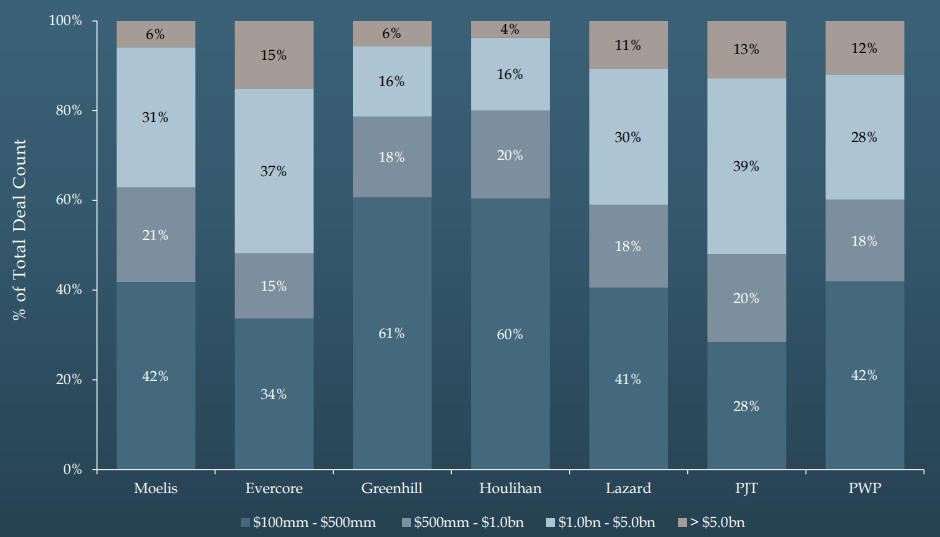

Further, 58% of transactions are over $500M in size, only exceeded by PJT, Lazard and, Evercore. These businesses have a substantially longer track record, showing the degree to which Moelis is overperforming relative to its time in the market.

{kind=link}

These factors are incredibly important as they illustrate the quality of the individuals working at Moelis. In financial services, the key differentiator is people and Moelis looks to have market-leading employees.

Looking ahead, the good work the business has done will inevitably compound, driving further project wins and improving market share. The scope in the near term looks impressive, as 35% of Moelis' current MDs have been at the firm for <3 years. As a result of this, they are still ramping up their operations, many of whom would have moved across with a non-compete. This should act as a nature tailwind in the coming years.

The economic fallout from the COVID-19 pandemic and the current bear market has led to a surge in demand for restructuring and debt advisory services, as businesses struggle with a change in market dynamics, as well as the increased cost of debt. Moelis has been actively involved in advising clients, with a landmark project to support Hertz with its restructuring. This is an invaluable credential that Moelis can use to show markets it has the expertise to work on large and complex projects.

Further, in current market conditions, having a counter-cyclical practice is key to buffering a decline in core services. With the current bear market, core M&A/Equity services are declining. Restructuring is a nature counterbalance, as work generally picks up when markets struggle. This allows for a degree of the loss in M&A work to be offset.

Further, Moelis has been expanding its presence in new geographies such as Asia and Europe, which has helped to diversify its revenue streams and reduce its reliance on the US market. The company has leveraged its brand value in the US to recruit quality senior individuals to lead local practices and win work at a similar level to that of the US.

Overall, we like Moelis' commercial profile. The business has grown rapidly in a highly competitive industry, boasting impressive credentials. This is a reflection of the people at the firm, giving us greater confidence that global expansion should drive continued gains. Current market conditions are concerning but restructuring should help offset some of the impacts.

Margin

Moelis' margins have varied wildly over the last decade but generally have been at an impressive level. In the IB industry, our view is that firms should target an OPM of >15% and a NI of >12% in order to outperform.

Both compensation and CoSP, which are all other cash costs to the business, have increased at an inferior rate to revenue. This is a positive characteristic as it shows that Management has aligned employee incentives with shareholders. Looking at this deeper, the company's compensation ratio is currently 63% but has historically been in the 50s. Our view is that anything below 63% is a good performance and so Moelis is doing well.

The only concern may be that revenue per employee has not materially increased from the levels at the start of the decade. This will be more evident if the company experiences another year of declining activity. This is, however, offset by compensation, which is increasing at a lower rate, again supporting the assertion that compensation is aligned with shareholder value.

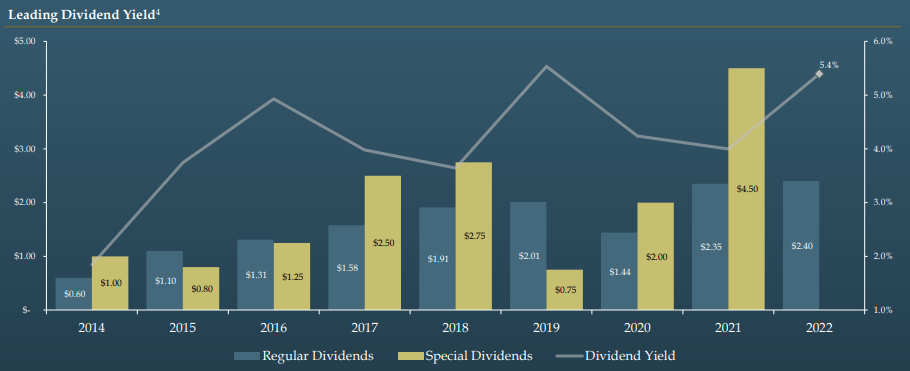

Balance sheet

Moelis has done well to consistently distribute to shareholders, with a market-leading dividend yield partnered with share buybacks. Management's policy is to distribute all free cash to shareholders.

{kind=link}

Outlook

Outlook (Tikr Terminal)

Presented above is Analysts' consensus view on Moelis' coming year. Given the nature of Banking, the figures are not to be relied on, however, can provide some useful directional guidance given analysts speak to Management.

Analysts are expecting revenue to decline, alongside margin contraction. This looks like a reasonable assessment as the reliance on advisory work leaves the business exposed to current market conditions. Margin contraction also looks reasonable as a degree of costs will always be fixed (Salaries) and so cannot move in line with revenue decline.

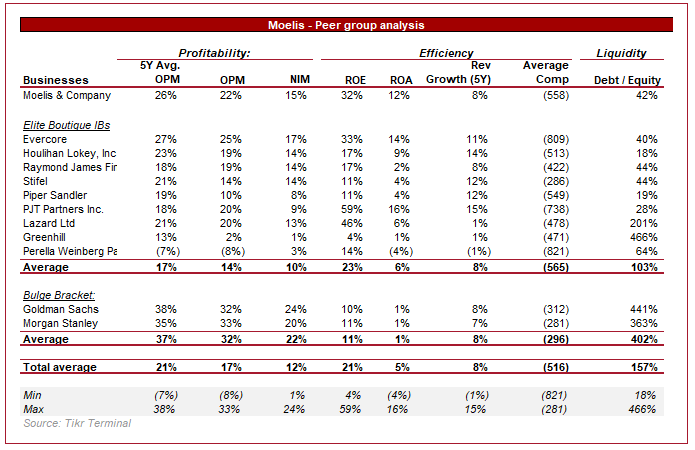

Peer comparison

Investment banking peers (Tikr Terminal)

{kind=link}

Presented above is a comparison of Moelis to its boutique IB peers.

Moelis outperforms the average performance, even if we exclude the underperforming stragglers. With a 5Y average OPM of 26% and a current NIM of 15%, only Evercore can boast superior performance. This is a significant outperformance in our view as this is an example of a bad year for Moelis, whereas some of the others are partially hedged through loan book operations, such as Stifel and RJF. Despite this, Moelis is ahead.

Growth is slightly below the average but is likely a reflection of Moelis' pricing, given the superiority in margins. Further, with less of a track record, the business is still developing its name in the market.

Valuation

With Moelis performing exceptionally well despite the difficult year, our view is that the business deserves a premium valuation.

Valuation (TIkr Terminal)

Moelis is currently trading at a substantial premium to its IB peers. Although we believe a premium is warranted, a 10x amount looks far too rich. The business does have key risks, those being:

- The volatility of revenue

- Despite having a restructuring practice, the business still looks tied to market conditions, which are not looking healthy.

- Declining financial performance looks reasonable, suggesting dividend cuts are possible.

Final thoughts

Moelis has done a fantastic job of growing its market share rapidly, especially in the lucrative high-value segment of the market. The company has recruited well and is positioned to grow well long term. Margins look attractive and importantly are higher than peers. The issue we see is that the company's valuation is far too high for what is a high-risk business, given its size. With continued declining performance likely, it is difficult to see how the business can justify its valuation.

For further details see:

Moelis: Quality IB But Far Too Expensive