ETD - Mohawk Industries: Still A Comfortable Prospect For A Value Portfolio

Summary

- Mohawk Industries has done well to grow sales recently, though profits and cash flows have been quite mixed.

- Despite some mixed results, shares of the business look to be cheap on an absolute basis and are cheap relative to some of its peers.

- Even if the firm sees some pain in the quarters to come, it's difficult imagining a scenario where shares are overvalued.

In an ideal world, shares that we buy would go up significantly and would do so in a fairly short window of time. Unfortunately, reality is not that great. Sometimes though, especially when you are talking about a difficult market, it can really be considered a win if your portfolio is up at a time when the market has declined. One of the companies that might have made this possible for investors in recent months is Mohawk Industries ( MHK ), an enterprise that focuses on the production and sale of flooring to its customers across the globe. It sells carpets, rugs, ceramic tiles, laminate, wood, stone, and a variety of other flooring options. Driven by continued sales growth and, to some extent, cash flow improvements, shares of the company have risen a bit over the past few months. This comes at a time when the broader market has declined and it illustrates for investors the benefit of buying shares that are trading at low multiples.

A bit of pleasure and a bit of pain

In early September of last year, I wrote an article that took a rather bullish stance on Mohawk Industries. In that article, I acknowledged the company's mixed operating history. But even given that, I mentioned that the past couple of years had resulted in significant improvement for shareholders. Although investors were alerted that the company was still worthy of being watched carefully because of its past performance, I felt that shares were cheap enough to warrant some upside moving forward. This ultimately led me to rate the company a ‘buy’, a rating that reflected my view that shares should outperform the broader market for the foreseeable future. So far, the firm has managed to do that, if barely. Since the publication of my article, investors in the company have generated upside of 0.5%. Although this is a small return in the grand scheme of things, it does beat out the 4.2% decline experienced by the S&P 500 over the same window of time.

{kind=link}

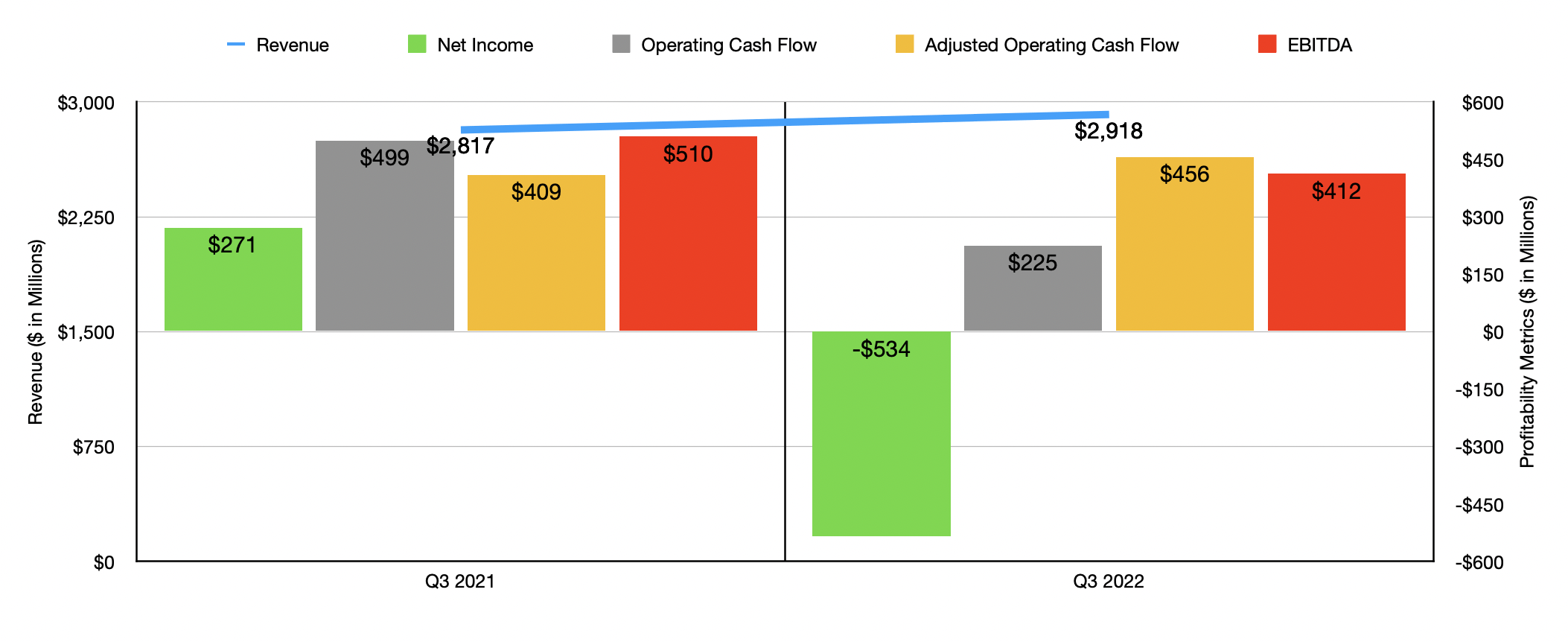

In my prior article on the firm, we only had data covering through the second quarter of its 2022 fiscal year. Fast forward to today, and that data now extends through the third quarter . Just as has been the case in the past, the data from the third quarter was rather mixed in nature. Revenue, for starters, came in positively, climbing by 3.6% from $2.82 billion in the third quarter of 2021 to $2.92 billion the same period of 2022. Favorable net pricing changes and product mix aided the company to the tune of $374 million. But this increase in pricing was not without cost. In response, the company saw lower sales volume amounting to $139 million. On top of that, it was also hit to the tune of $117 million from foreign currency fluctuations and $18 million from having one less shipping day in Europe in 2022 compared to 2021.

Although the revenue numbers were positive, the firm did experience some pain on the bottom line. The firm went from generating a net profit of $271 million in the third quarter of 2021 to generating a net loss of $534 million the same time last year. Despite the increase in revenue, the company was hit by a 5.2% decline in its gross profit margin. $348 million of increased costs associated with inflation, combined with $55 million attributable to short-term manufacturing disruptions, negatively impacted the company. Lower sales volume also hit it to the tune of $45 million. There were other, smaller issues as well. Relative to revenue, selling, general, and administrative costs all increased by roughly 1%, impacted by increased legal settlement costs and reserves, higher inflation, and the unfavorable net impact of price and product mix and other factors. Also during the quarter, the company booked a $695.8 million impairment charge due to the broader economic conditions impacting the enterprise. Other profitability metrics were largely weaker as well. Operating cash flow dropped from $499 million to $224.7 million. But if we adjust for changes in working capital, it would have risen from $409 million to $456.3 million. Over that same time, however, EBITDA dropped from $509.6 million to $412.4 million.

{kind=link}

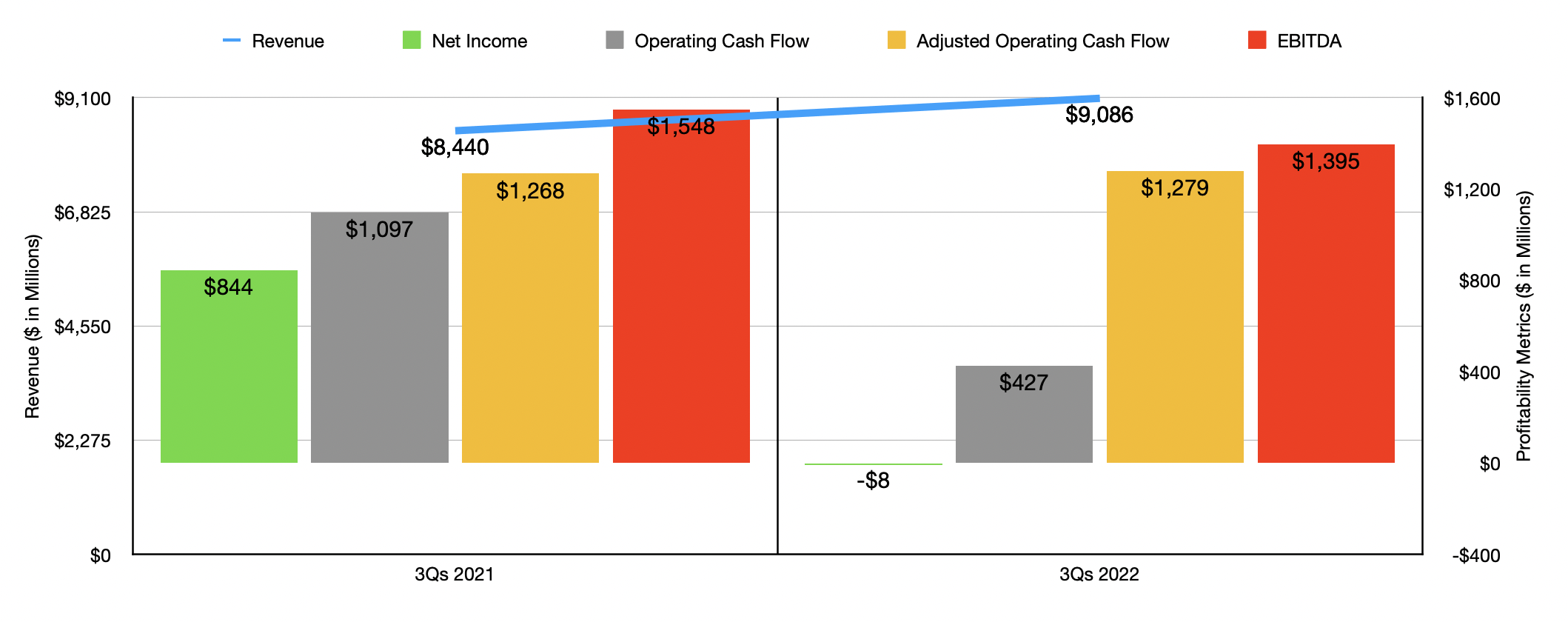

The results experienced in the third quarter were very similar to what the company experienced in the first three quarters of the year as a whole. Revenue increased from $8.44 billion to $9.09 billion. At the same time, net income dropped from $844.1 million to negative $8.2 million. According to the data available, operating cash flow during this time plunged from just under $1.10 billion to $427.4 million. Though on an adjusted basis, it actually ticked up modestly from $1.27 billion to $1.28 billion. Meanwhile, EBITDA also declined, falling from $1.55 billion to just under $1.40 billion.

{kind=link}

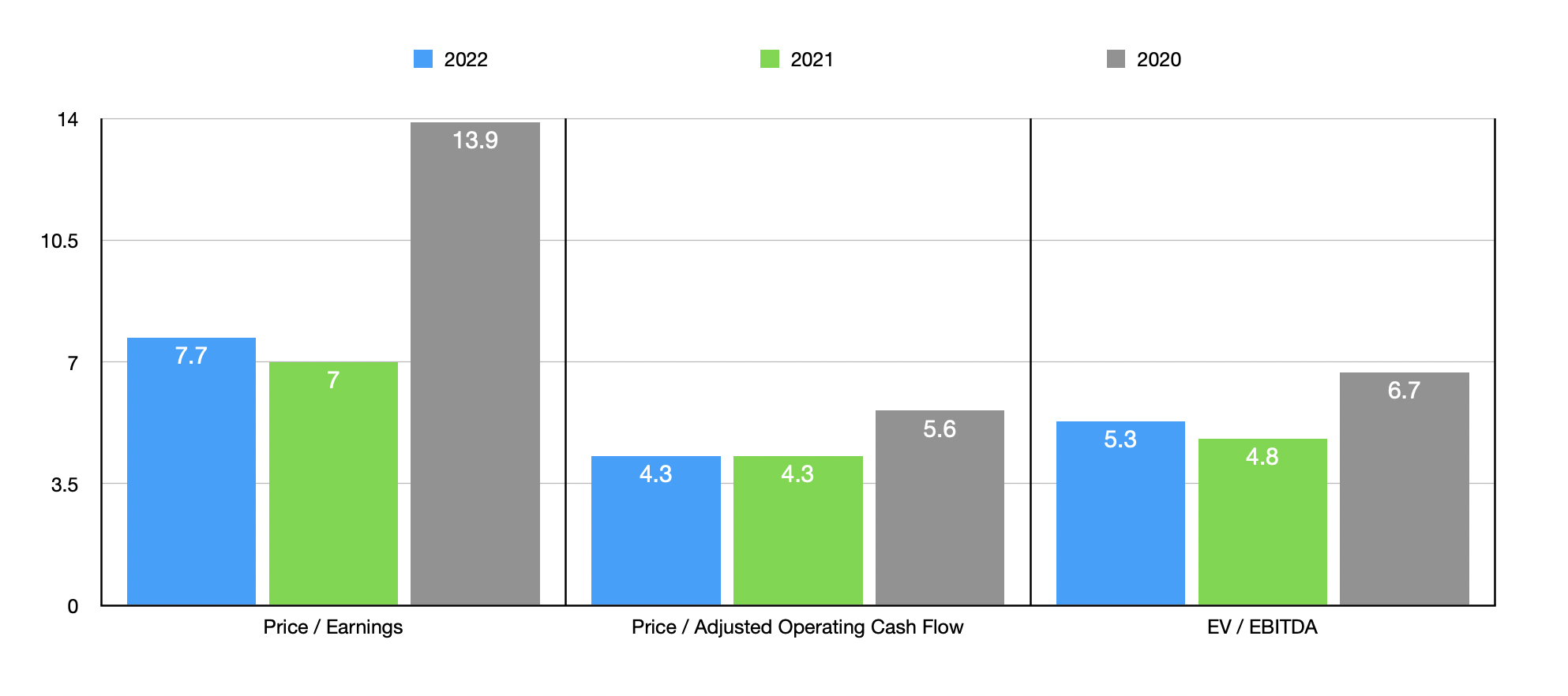

Because the management has not provided any guidance when it comes to 2022 as a whole, it's difficult to know what to expect for the final quarter. If we simply annualize results experienced so far for the year, we would get net income of $931.1 million (excluding the impairment and other one-time charges), adjusted operating cash flow of $1.68 billion, and EBITDA of $1.76 billion. This would give us a price-to-earnings multiple of 7.7, a price to adjusted operating cash flow multiple of 4.3, and an EV to EBITDA multiple of 5.3. But of course, given the uncertain economic conditions and the prospect of further weakness ahead, we should plan for a worse situation than this. In the chart above, you can also see pricing if we were to use data from 2021 or 2020. Even during the pandemic year of 2020, the picture does not look significantly worse than what the 2022 estimates suggest. If we do take the 2022 data as our lead, we can see how shares are priced compared to similar firms. Five similar companies that I looked at had priced earnings multiples between 6.2 and 12.9 and EV to EBITDA multiples of between 2.3 and 10.5. In both cases, two of the five firms were cheaper than Mohawk Industries. Meanwhile, using the price to operating cash flow approach, the range for these companies was between 7.8 and 23, with our prospect being the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Mohawk Industries |

| 7.7 |

| 4.3 |

| 5.3 |

| Leggett & Platt ( LEG ) |

| 12.8 |

| 12.0 |

| 8.7 |

| Tempur Sealy International ( TPX ) |

| 12.5 |

| 16.3 |

| 9.5 |

| La-Z-Boy Inc. ( LZB ) |

| 6.2 |

| 11.2 |

| 2.3 |

| Ethan Allen Interiors ( ETD ) |

| 6.3 |

| 7.8 |

| 3.3 |

| The Lovesac Company ( LOVE ) |

| 12.9 |

| 23.0 |

| 10.5 |

Takeaway

Based on the data currently available, I must say that I am of the opinion that Mohawk Industries It's far from a best-of-breed prospect. Even so, the picture for the firm remains decent and shares are cheap on both an absolute basis and, to a limited extent, relative to similar firms. Given these factors, I have no problem keeping the firm as a soft ‘buy’ at this time, reflective of my belief that shares should outperform the broader market moving forward.

For further details see:

Mohawk Industries: Still A Comfortable Prospect For A Value Portfolio