MHK - Mohawk Industries: The Firm Is Facing Rapid Deterioration (Rating Downgrade)

2023-05-02 15:22:25 ET

Summary

- Recent financial performance achieved by Mohawk Industries, Inc. has been awful due to weak market conditions.

- This is creating a lot of pain, particularly on the bottom line, that is very likely to worsen before it gets better.

- Mohawk Industries, Inc. shares are cheap, but in light of this weakness, investors may want to be more cautious.

Value investing can be a tricky way to make a profit in the market. You always have to balance the price that you're paying for the company with how fundamentals are changing. For instance, a company that is seeing a decline in revenue and profits can still make for an attractive investment. But the key is making sure you pay the right price for it. On the other hand, a company that is experiencing attractive growth can still not make sense to buy into because of how pricey shares are. A really good example of this former case can be seen when looking at Mohawk Industries, Inc. ( MHK ), an enterprise that's focused on the production and sale of flooring such as carpets, rugs, ceramic tiles, and more.

Recently, financial performance has been all over the map. Revenue has fallen, profits have tanked, and cash flow numbers have been under pressure. On the other hand, the stock is trading at levels that are largely attractive from a fundamental perspective. This leaves me with a mixed feeling about the enterprise. But when faced with a situation like this, it's important to note another tenet of value investing, which is that it's always better to be overly conservative and right in a good way, than overly liberal and wrong in a negative way. You don't need to swing at every questionable pitch. Because of this, I've decided to downgrade the company from a "Buy" to a "Hold" for now.

Recent performance has been an issue

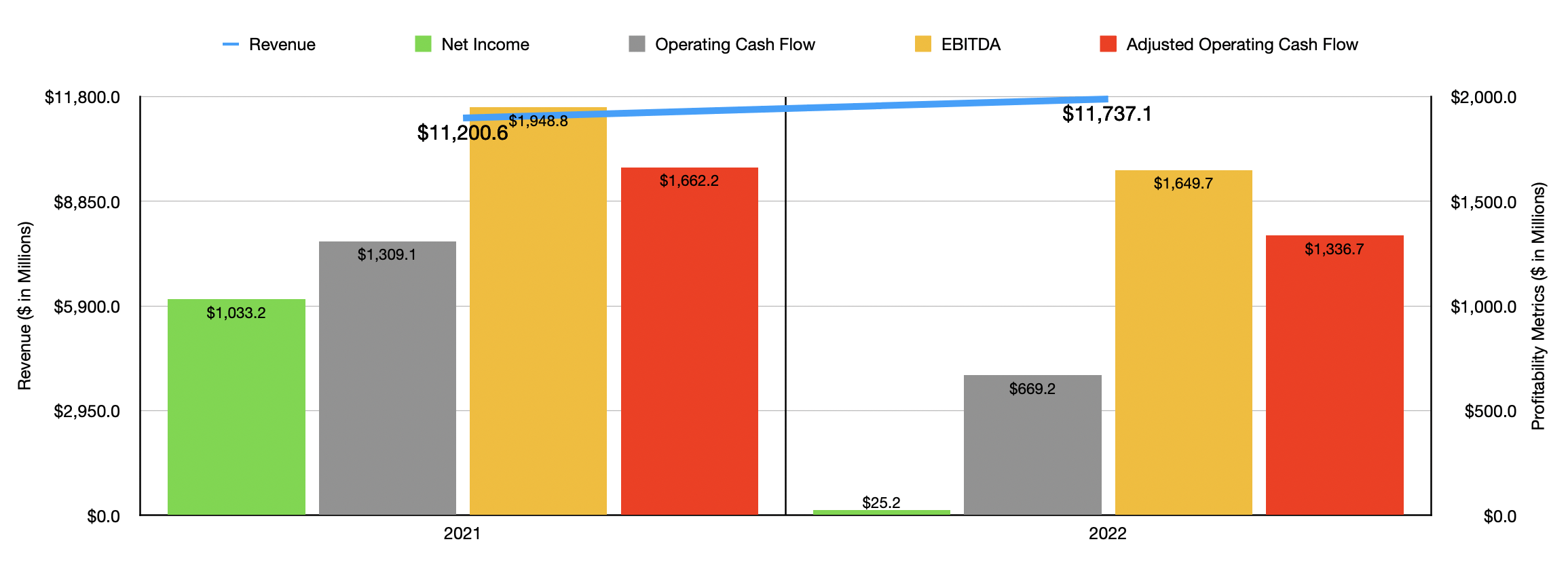

On April 27th, the management team at Mohawk Industries announced financial results covering the first quarter of the company's 2023 fiscal year. Before we get into those numbers, it would be helpful to provide a little refresher on how the company performed in 2022 . Revenue for the year came in at $11.74 billion. That was 4.8% higher than the $11.20 billion the company reported in 2021. Although the company suffered to the tune of $580 million because of lower sales volume, as well as $412 million because of foreign currency fluctuations, not to mention $40 million because of one less shipping day in 2022 compared to 2021, higher prices and a change in product mix pushed revenue up by $1.56 billion. The biggest growth for the company came from its Global Ceramic operations, with sales spiking 10%.

{kind=link}

On the bottom line, the picture was not quite as good. As you can see in the chart above, net profits declined, as did operating cash flow, adjusted operating cash flow, and EBITDA. A lot of this pain came from $695.8 million of goodwill and other intangible impairment charges. But another driver was a plunge in the firm's gross profit margin from 29.2% to 25.1%. That, according to management, was driven mostly by inflationary pressures, with lower sales volume and temporary plant shutdowns also having significant impacts.

{kind=link}

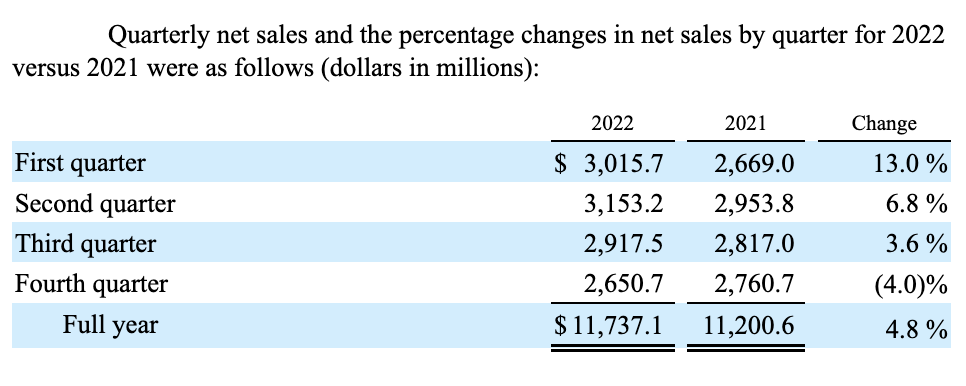

At first glance, you could say that 2022 was a mixed year. But that picture changed in the first quarter of this year. During that time, revenue came in at $2.81 billion. That was 6.9% lower than the $3.02 billion reported one year earlier. Despite this plunge, it is worth noting that sales beat analysts’ expectations by $66.5 million. That's likely one of the reasons why, after the company announced financial results for the quarter, shares jumped 7.2%. Although the company benefited to the tune of $160 million from a change in pricing and product mix, a reduction in sales volume hit the company to the tune of $335 million, even though the firm was able to benefit from some acquisitions it made. If it seems as though the first quarter sales decline came out of nowhere, you need only a look closer. As you can see in the image above, quarterly revenue for the company was on a continuous downtrend throughout 2022. The company started the year off with sales up 13%. But by the final quarter of the year, revenue dropped by 4%.

{kind=link}

This decline in revenue has brought with it a worsening of the firm's bottom line. Net income in the first quarter of the year, for instance, came in at $80.2 million. That pales in comparison to the $245.7 million reported for the first quarter of 2022. A sizable reduction in gross profit, as well as a surge in selling, general, and administrative costs, all hit the business materially. Although earnings per share of $1.26 missed analysts’ expectations by $0.04 per share, adjusted earnings of $1.75 beat expectations by the same amount. Unfortunately, most other profitability metrics followed a similar trajectory. It is true that operating cash flow spiked from $55 million to $257.3 million. But if we adjust for changes in working capital, it would have dropped from $407 million to $223.9 million. Meanwhile, EBITDA for the firm fell from $468.9 million to $308.6 million.

Sadly, Mohawk Industries, Inc. management has not really provided any guidance when it comes to the future. The one exception is that they did say that adjusted earnings per share should be between $2.56 and $2.66 for the second quarter. This would represent a sizable decline from the $4.41 per share that the company reported on an adjusted basis in the second quarter of the 2022 fiscal year. Almost certainly, management is baking into that a continued worsening in the revenue picture, combined with a reduction in demand that is causing the firm to not be able to increase its pricing enough to offset inflationary pressures.

{kind=link}

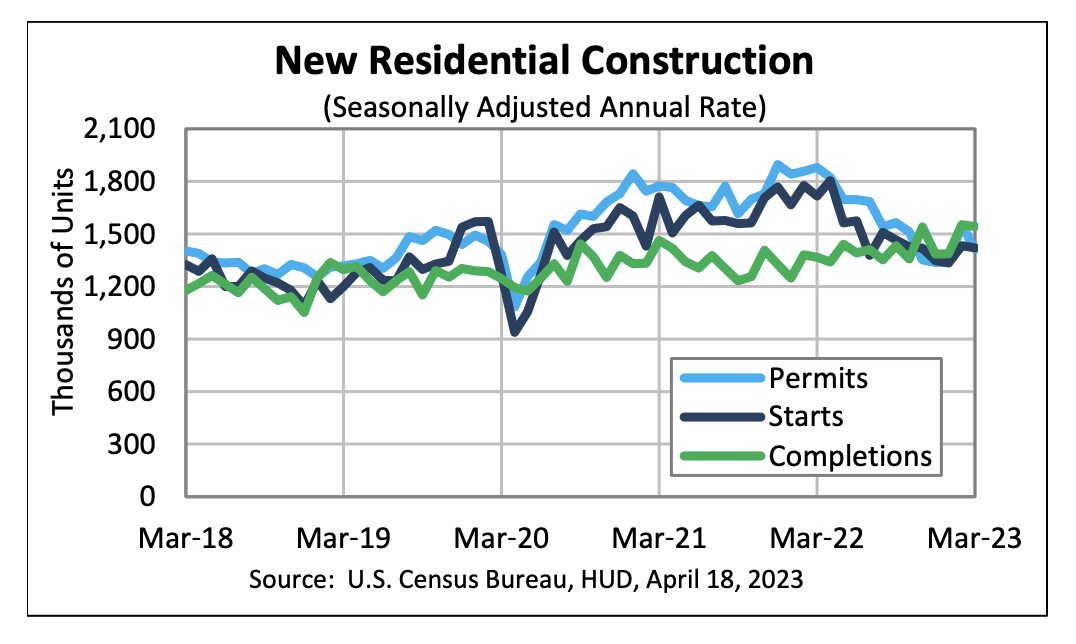

Truth be told, investors should expect this kind of weakness to continue at least through the 2023 fiscal year. It very well could extend some time beyond that. I say this because a good portion of the company's business is related to the construction market. Management said that commercial construction has been encouraging. However, they said that investments could weaken later this year. On the residential side, we are already seeing a great deal of pain. Take the month of March, which is the most recent month for which data is available. Residential building permits we're down 8.8% from one month earlier and we're 24.8% lower than the same time last year. Year over year, housing starts were down 17.2%. Housing completions were still up 12.9% in March compared to the same time one year earlier. So what this is suggesting is that current conditions are only just now getting worse.

{kind=link}

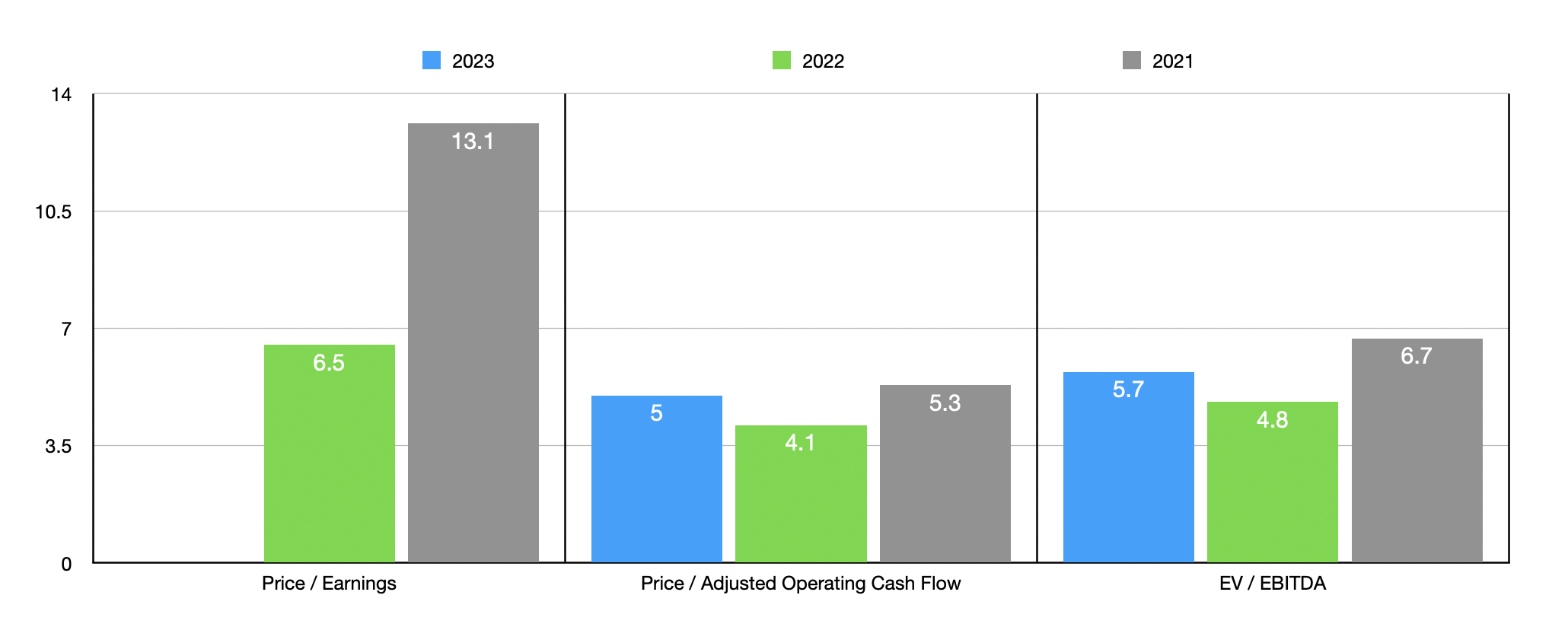

Valuing a company like this is very difficult. Given the volatility seen in the first quarter of the year, we have no idea what the rest of the year might look like. In the chart above, I did price the company using data for the past three completed fiscal years. I excluded from this the price to earnings multiple for 2022 because it would have made the rest of the chart unreadable. But for context, that multiple was 267.5. Although the earnings picture has been all over the map, cash flow has been a bit steady. Using the data from 2022, I compared the company to five similar firms. On a price to earnings basis, our prospect was definitely the most expensive of the group. When it comes to the price to operating cash flow approach, it was the cheapest, while the EV to EBITDA approach resulted in two of the companies being cheaper than it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Mohawk Industries |

| 267.5 |

| 5.0 |

| 5.7 |

| Leggett & Platt ( LEG ) |

| 13.8 |

| 9.7 |

| 9.1 |

| Tempur-Sealy International ( TPX ) |

| 14.7 |

| 17.6 |

| 11.4 |

| La-Z-Boy ( LZB ) |

| 7.0 |

| 7.6 |

| 2.7 |

| Ethan Allen Interiors ( ETD ) |

| 6.2 |

| 6.7 |

| 3.3 |

| The Lovesac Company ( LOVE ) |

| 15.2 |

| 23.0 |

| 7.1 |

Takeaway

From what I can see, things are not going particularly well for Mohawk Industries, Inc. When times are tough, I like to consider buying cheap stocks. That kind of strategy could very well work out in this case. I am encouraged by the Mohawk Industries, Inc. cash flow data. But the incredible amount of volatility that we are experiencing, combined with where we are in the cyclical downturn for construction, leads me to want to be a bit more cautious than I normally would be. Given these factors, I have decided to downgrade Mohawk Industries, Inc. from a "Buy" to a "Hold" until we see more clarity.

For further details see:

Mohawk Industries: The Firm Is Facing Rapid Deterioration (Rating Downgrade)