TAP - Molson Coors Beverage: Growth Is Sustainable And Market Share Gains Should Stick

2023-11-29 07:25:05 ET

Summary

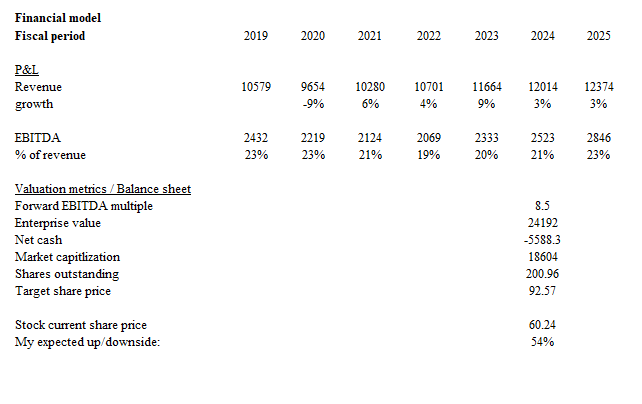

- I have a target price of $92.57, representing a 54% upside from the current share price.

- Molson Coors reported strong Q3 earnings with net sales growth of 12.4% and beat consensus estimates for EPS.

- The company should be able to meet its FY23 guidance and I have a positive outlook for FY24 with sustained market share and growth momentum.

Investment overview

I have a buy rating for Molson Coors ( TAP ) stock with a target price of $92.57, representing an upside of 54% vs. the current share price of $60.24. I believe TAP has the ability to sustain its current growth momentum and market share, and if it performs as I expected, multiples should start to see a positive re-rating.

Business description

TAP is in the business of manufacturing beers with a presence across the three key regions: North America, EMEA, and APAC. Of the 3 regions, North America represents the largest piece of the revenue pie (81.4% of total revenue), followed by EMEA and APAC, collectively representing 18.7% of total revenue. TOP has multiple brands under its belt, which can be found at this link , and below is a screenshot of some of the key brands that TAP offers. The business has gone through periods of ups and downs, but revenue has expanded at a very healthy clip since 2011, growing from $3.5 billion to $11.5 billion in the last 12 months [LTM]. The same growth can be seen in the EBITDA line, growing from $1.4 billion in 2014 to ~$2.4 billion in the LTM. TAP balance sheet has also continued to strengthen over time, reducing its net debt position over the past few years from $11.5 billion to $5.5 billion (or ~2.3x net debt to EBTIDA as of LTM).

{kind=link}

Solid 3Q23 earnings report

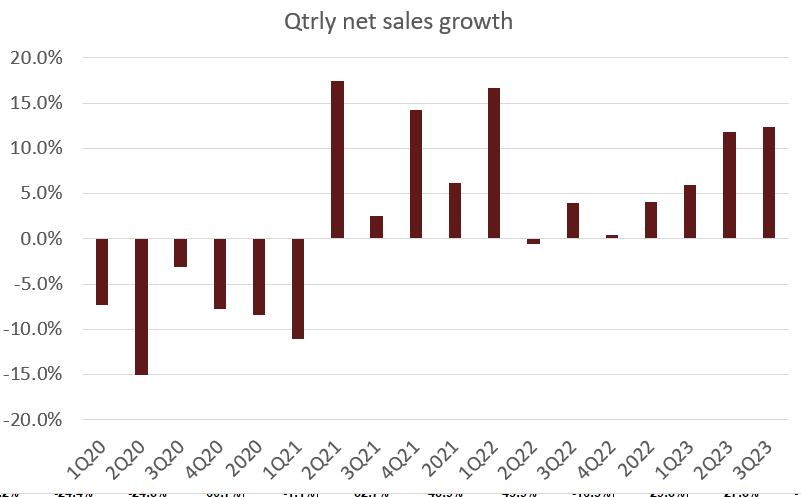

TAP reported 3Q23 net sales growth of 12.4% to ~$3.3 billion. The growth was driven by both volume and pricing/mix, with the latter being the major growth driver. Total volume growth was 3.2%, led by Americas volume increase of 6.6% but offset by EMEA and APAC volume decrease of 5.5%. Pricing/mix, on the other hand, was up 7.8%, which reflects really well on TAP’s portfolio premiumization and beyond beer strategy. Strong pricing and mix impact led to an improvement in overall gross margins, which saw an increase of 290bps to 39.8%. Strong topline and gross margin performance led to a 270bps improvement in EBIT margin to 17.2%. As a result, EPS came in at $1.92, beating consensus estimates of $1.55 by a big margin.

In my opinion, TAP reported very solid Q3 results, and the key question is whether TAP can continue this growth momentum and hold on to all the share gains that Budweiser lost during the scandal . Below, I list out my thoughts on TAP’s ability to continue its growth momentum in 4Q23 and FY24.

Meeting FY23 guidance is plausible

The strong 3Q23 performance led to management raising its FY23 guidance. In my opinion, the key updates are as follows:

- Net sales growth to reach the high end of high single-digit [HSD] percentage vs. the prior guide for just "HSD"

- Underlying income before income taxes growth of 32%–36% on a constant currency basis, a major step up from the prior guidance of 23% to 26%

The logical question to ask is whether these revised guidelines are possible to achieve, and I believe the answer is yes.

TAP has already grown by 10.7% on a year-to-date basis (constant currency), and with the HSD guide, it implies mid-single-digit percentage growth in 4Q23. The hurdle is really low here. If we assume that management’s HSD means 9% on a constant currency basis, this implies that TAP only needs to grow by 4% in 4Q23, or more than half the rate it has grown on a year-to-date basis. While the year-to-date performance has been boosted by the increase in inventory in 3Q23 (in anticipation for 4Q), I am confident that TAP can easily achieve the implied growth rate of mid-single digit constant-currency as easily achievable. Firstly, the US beer industry has remained very healthy over the past few months, and management did not mention any particular shift in dynamics during the call, suggesting that 4Q23 is likely to see a similar strength.

Now, of course our business has benefited greatly from the broader dynamics of the U.S. beer industry over the past seven months. But as you can see, the improvement in our business is being driven by more than one market. Company 3Q23 earnings

Secondly, 4Q23 is going to see an easy comp against 4Q22, which was a period of weak consumer sentiment, which was reflective in the numbers: 4Q22 saw a net sales growth decline of 0.4%. As such, if we assume that 3Q23 momentum, which grew 12.4% on top of the 4% growth seen in 3Q22, has a delta of ~800 bps, 4Q23 is easily more than mid-single digits already (0.4% + 800 bps = 8.4%). I would also note that weather is going to be a tailwind for TAP in the 4Q as the US is going to see a warmer winter in 2023 , which should help with more outdoor dining and gatherings, especially with Christmas and New Year’s even in December.

{kind=link}

Positive outlook for FY24

Looking past FY23, I believe TAP should be able to continue holding on to the share gains from Budweiser, and the business growth should easily achieve low-single-digit growth. One of the concerns with TAP is that it might lose all the market share that it gained from Budweiser once people start to “forget” about it. However, I think the data has proven otherwise. According to management, TAP is not seeing any signs that suggest that its market share gains are slowing

“You know, certainly while some buyers are switching categories, and certainly our data says that some drinkers have left within the category. You know, we're gaining share. Miller Lite, Coors Light are healthy and growing share strongly. And that share has been stable for the last 25 weeks. It's a structural change to the industry that is sticking, whether you look at it on a 1-week basis, a 4-week basis, a 13-week basis, or a 26-week basis, it has stuck”

According to TAP's recent Strategy Day 2023 , the company plans to maintain a steady increase in organic sales by low single-digit percentage post-FY23. I believe TAP is well positioned to achieve this goal in 2024 based on three reasons. Firstly, as mentioned above, I expect market share to stick, which means FY24 is going to see a higher revenue base in FY23. Secondly, the reset in shelf spaces should further anchor TAP's ability to retain market share. For reference, Coors Light and Miller Lite saw 6 to 7% gains in shelf space, which is a massive amount of space for a brand of its size (according to management). With the current growth momentum, I believe TAP should be able to negotiate for more shelf space, which is going to happen in spring 2024. Capturing a larger shelf space will further solidify the FY24 growth outlook and increase the revenue base that FY25 will grow from. Thirdly, TAP’s ongoing premiumization and beyond-beer strategy should provide further pricing and mix benefits, as seen in 3Q23. For the benefit of new readers, TAP implemented its revitalization program in 2019, leading to significant changes to its portfolio, including the elimination of underperforming SKUs (so far, TAP has reduced these SKUs by 16%). These efforts have freed up capacity for new innovation in growing categories, which exposes the business to higher-growth opportunities. While Beyond Beer results today are still too small to move the needle, it is a fast-growing part of the business that should eventually become an important growth driver.

And from a shelf reset point of view, yes, I guess, everybody's fighting for space. The beauty of our position at the moment is that, we've got the facts and the data to support meaningful increases in space for our brands. Company 3Q23 earnings

Valuation

{kind=link}

As I have discussed above, I believe TAP can easily achieve the 9% revenue growth guidance for FY23 and low single-digits for the foreseeable future. Using these assumptions, I expect TAP to generate ~$12.8 billion in revenue in FY25. With the continuous focus on premiumization, which has proven to be effective in driving gross margin improvement, and also the Beyond Beer strategy (removing low-performing SKUs), I believe margin can expand back to historical levels. Over the next 2 years, I expect the margin to reach 100bps above pre-covid levels. I assumed TAP would achieve a 24% EBITDA margin in FY25, generating ~$3 billion in EBITDA. At the current 7.9x forward EBITDA valuation, TAP is trading at the lower end of its peer group, which consists of players like Boston Beer Company, Heineken, Budweiser, Ambev, Carlsberg, Constellation Brands, and Anheuser-Busch InBev. I believe part of the reason for the undervaluation was the concern that TAP would not be able to sustain its market share and growth momentum. However, as I listed above, I believe it is possible, and if TAP grows as I expected, valuation multiples should gradually improve to peers’ levels of 10x forward EBITDA. Being conservative, I assumed a modest improvement to 8.6x forward EBITDA. All of these led to my price target of $92.57.

Risk

The risk here is that TAP starts showing cracks in sustaining its market share position. Alternative data providers like Nielsen are able to provide data that public investors (like myself) are not able to access (unless one subscribes). These data might show that TAP is losing market share, causing the stock to react in advance of the results release. Even though these data might not be entirely representative of the business, narrative might take hold and cause valuation to see further pressure.

Conclusion

Closing off, I have a buy rating for TAP. TAP 3Q23 results were very positive, and I feel very optimistic about FY23 and the near term. For 4Q23, several positive tailwinds give comfort that guidance can be met, and if I were to look further ahead, I believe TAP can achieve its low-single-digit growth guidance as it sustains its market share, continues its premiumization strategy, and wins more shelf space in FY24.

For further details see:

Molson Coors Beverage: Growth Is Sustainable And Market Share Gains Should Stick