TPX.B:CC - Molson Coors Beverage: Strategy For Growth And Innovation

2024-01-01 22:00:06 ET

Summary

- Molson Coors Brewing Company is a global brewer with a diverse portfolio of beer brands and a wide distribution network.

- The company faces stiff competition from other global brewers and local craft breweries, but has differentiated itself well through its brand portfolio, innovation, and marketing.

- Revenue growth has been underwhelming, with analysts forecasting this to continue. Further, the company has seen its margins slide following the impact of inflation.

- The business is performing well in recent quarters, owing to an improvement in US market share. We believe this could be the foundations for a renewal in fortunes, although we would like to see this sustained.

- TAP appears slightly undervalued, although we are awaiting sustainable financial strength before rating the stock a buy.

Investment thesis

Our current investment thesis is:

- TAP is attractively positioned in the industry due to its large portfolio of brands across various beverage segments. This said, its financial performance implies weakness relative to its market-leading peers, implying TAP is a weaker constituent.

- The company has struggled to achieve consistent revenue growth, but has gained market share relative to Bud Light in in 2023 following controversy, representing an opportunity for improvement.

- Product development has been positive but with limited influence over revenue. Price is currently the primary revenue driver, with volume struggling.

- With the outlook mild and its valuation not sufficiently depressed, we rate the stock a hold.

Company description

Molson Coors Brewing Company ( TAP ) is one of the largest global brewers, known for its iconic beer brands such as Coors, Miller, Blue Moon, and Molson. With a rich history spanning centuries, the company operates across multiple regions, including North America, Europe, and International markets.

Share price

TAP's share price has underperformed the market, despite a continuation of the company's growth trajectory. This reflects an underwhelming development of profitability, as well as various impairment charges on assets.

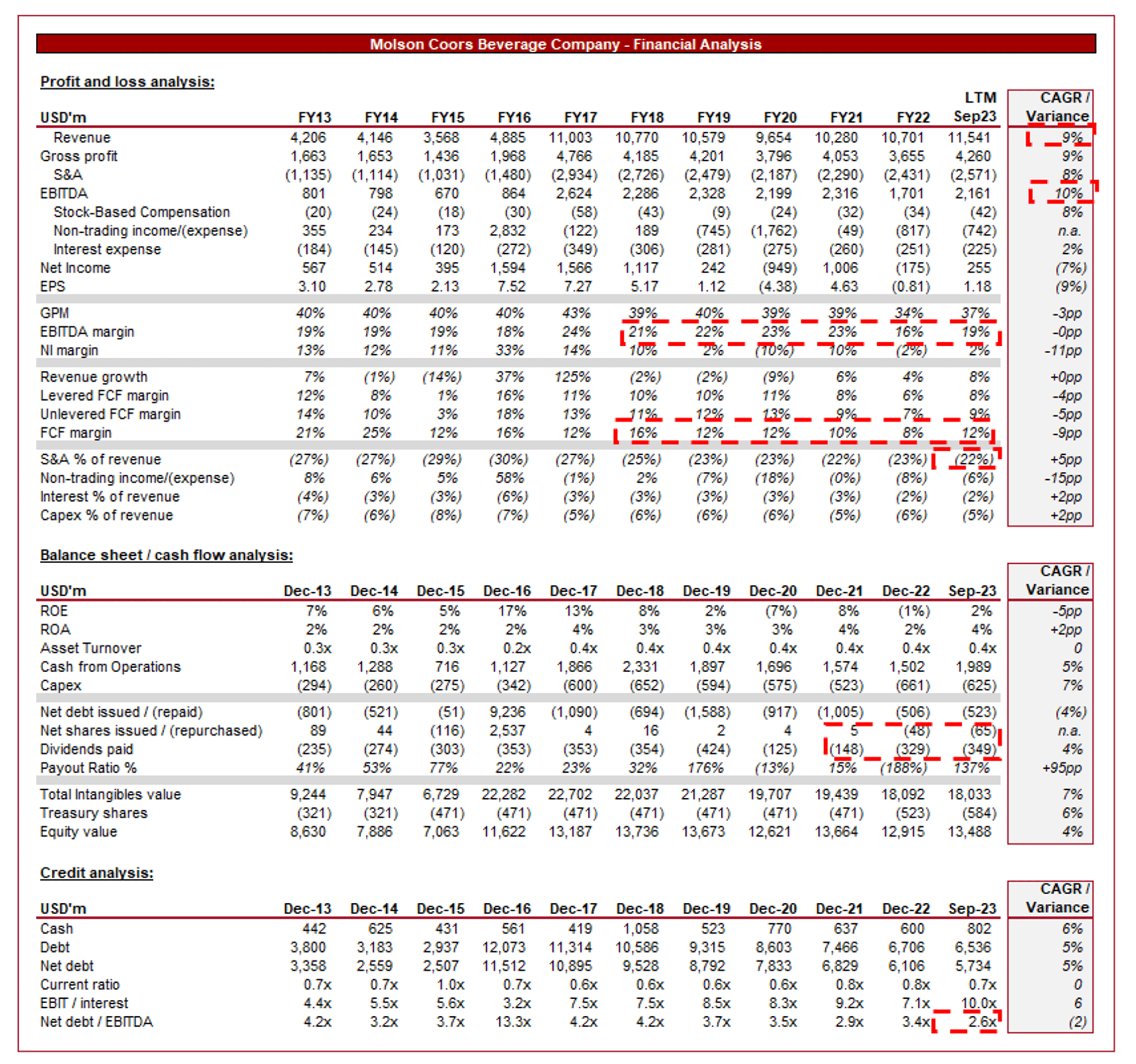

Financial analysis

Molson Coors Financials (Capital IQ)

{kind=link}

Presented above is TAP's financial performance for the last decade.

Revenue & Commercial Factors

TAP's revenue has grown well in the last 10 years, achieving a CAGR of 9%. This was materially enhanced by the acquisition of Miller in 2016 for c.$12bn . When excluding this acquisition, growth has been fairly underwhelming, reflecting competitive trading conditions.

Business Model

TAP engages in the brewing, marketing, and distribution of alcoholic and non-alcoholic beverages, including beer, cider, and other malt beverages. The company owns a diverse portfolio of well-established beer brands, allowing TAP to cater to different consumer preferences and market segments. This is a strategy conducted by many of its peers, as it allows for a greater portion of the market to be captured globally, while also increasing competitive pressure on peers for retail and bar space.

In conjunction with its reach achieved through brands, TAP benefits heavily from the ability to innovate and share competencies, ensuring it is exploring key growth avenues and remaining culturally relevant in its key markets. This is critical given that consumer trends and interest change over time, leaving single brands susceptible to a decline in revenue.

TAP operates through a network of breweries and partnerships worldwide, enabling broad market reach and localized production. This provides the business with significant operational capabilities, allowing the business to efficiently brew its large range of brands

Competitive Positioning

TAP's competitive advantage revolves around the following key factors:

- Strong brand loyalty and recognition, allowing the brand to capture a large share of the market, as well as new entrants. It cannot be understated how valuable it is to have loyal customers in the beverage market. Regular drinkers are unlikely to regularly depart from their usual choice, making demand incredibly sticky.

- The company's extensive distribution network facilitates the global support of its large range of brands.

Beverage Industry

Beverage businesses differentiate themselves through their taste, marketing, and brand strength. TAP faces competition from other global brewers like Anheuser-Busch InBev ( BUD ), Heineken ( HEINY ), and Carlsberg ( CABGY ), as well as craft breweries and local players.

The beer market has experienced growing demand for craft beer and other alternatively-flavored alcoholic beverages (Hard Seltzer, Iced Tea, etc.). This looks to be driven by experimentation, with consumers willing to go beyond their usual choices for interesting new products. This has caused disruption to the major players, as local/micro-breweries have achieved impressive growth. TAP has invested heavily in the development of these products, seeking to utilize this trend to enhance its brands. Although this is unlikely to move the needle in the near term given TAP's scale, creating a strong foundational offering will allow the business to partake in industry growth, should it truly reach mainstream status globally.

Product development (Molson Coors)

{kind=link}

In conjunction with this, consumers are increasingly willing to pay a premium for higher-quality and unique beverage offerings. This is partially related to the above, but also the wider alcohol segment, be it traditional beers or ciders. This is music to the ears of the likes of TAP, as it allows for premium pricing at a smaller marginal cost. For this reason, there has been a big push for premiumization. Although we think TAP has done well regarding the alternative alcoholic beverage, the general premiumization of its brands still requires work in our view, especially in Europe.

Finally, greater awareness of the health implications of alcohol consumption and a general focus on living a healthier lifestyle is impacting the amount of alcohol consumption. This has contributed to a change in market dynamics. Firstly, brands have been forced to create zero-calorie alternatives, which can maintain flavor to the extent possible. Similar to its peers, TAP has done well in this regard. The divergence in the industry comes with the development of low-alcohol options, healthier options (ingredients), gluten-free, etc. The development in this regard is broad. TAP's focus looks to be on alternative beverages, with the above-discussed point, alongside the expansion of its "beyond beer" options. This involves its "healthy energy drink" line ZOA, as well as Whisky and Bourbon. Peroni, one of its largest brands, only recently launched a zero-alcohol option in the US, and only in select markets.

Economic & External Consideration

Current economic conditions are causing material disruption to the business. With elevated inflation and elevated rates, there is a risk that consumers will reduce consumption and social gatherings to protect finances, impacting demand.

In the most recent quarter, revenue growth beat analysts' estimates, up +12.4% YoY. This is a reflection of robust demand, pricing gains, and successful execution of its strategic goals. Furthermore, a portion of this is likely due to increased market share following the issues faced by AB-InBev.

The company has pushed hard to improve its exposure in the US following the uptick in market share, partnering with new distributors and seeking to secure more shelf space. Although the medium-term is uncertain, this implies consumer demand is resilient. It is critical that Management continues to pressure its US competitors and focuses on consolidating its improved position.

Margins

TAP's margins had been on an upward trajectory in the lead-up to the pandemic, subsequently declining noticeably. The business has faced inflationary cost pressures, with production costs rapidly rising in the last 2 years. Management has been active with price increases in recent quarters, as well as observing softening of costs more recently. This has contributed to margin appreciation in the LTM, with a reasonable runway to its pre-pandemic levels.

Our view is that TAP will likely see small incremental margin improvement QoQ in the coming 12 months, as these cost pressures continue to subside. It is critical that volume in monitored in conjunction with this as we have observed many businesses seeing elasticity rise due to macro weakness.

Balance sheet & Cash Flows

TAP is currently in the process of deleveraging, with a ND/EBITDA ratio of 2.6x. This balance is somewhat overstated by its various leases, and so we feel a healthy level has been reached. Distributions have continued despite the profitability weakness in recent years, partially due to the strength of its FCF, as many of these charges are one-off or non-cash in nature.

From this point, Management should feel comfortable to accelerate distributions and/or consider accretive M&A. This represents a potential catalyst for positive price actions.

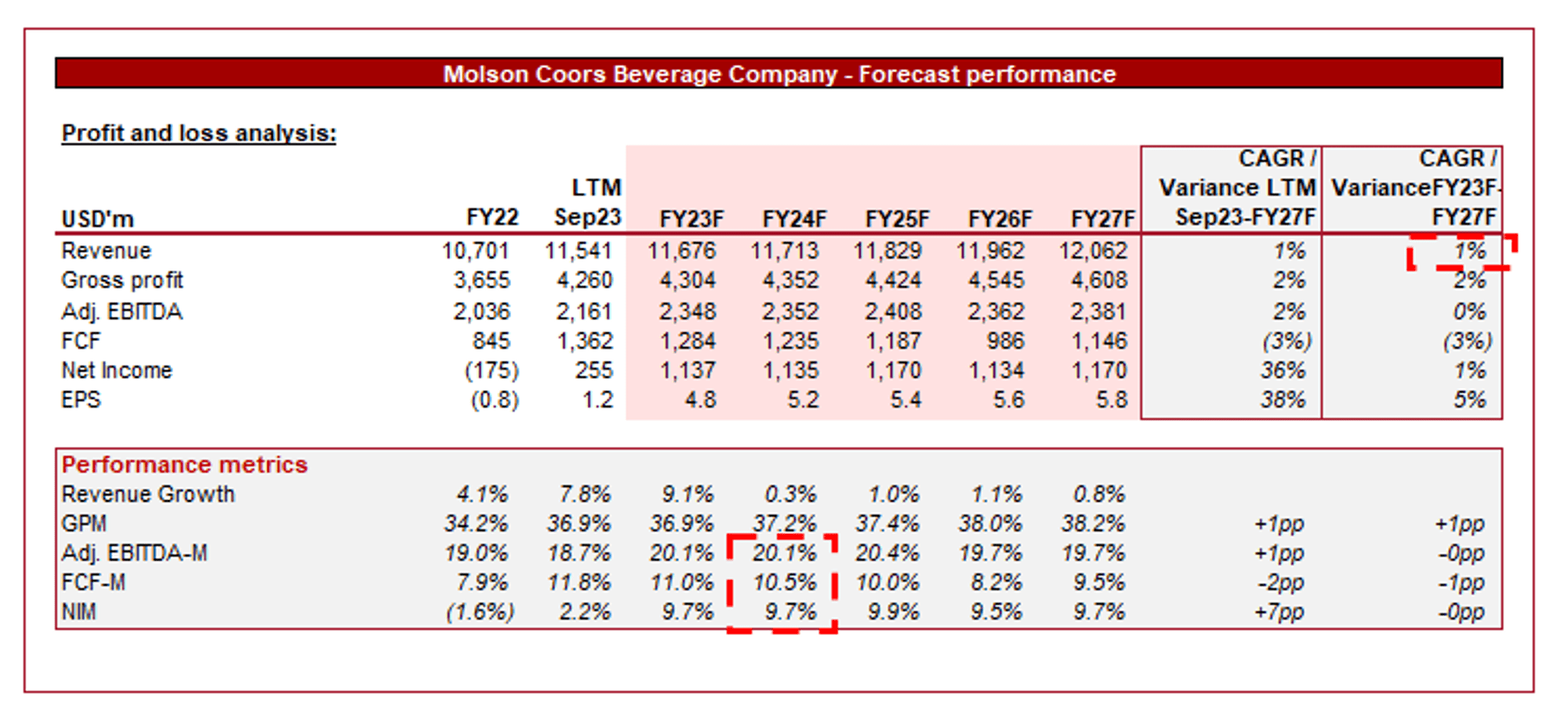

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Growth is expected to be poor in the coming years, a disappointing development given the inflation rate during this period will likely exceed 1%. Given the positive developments in recent quarters, we consider this highly conservative, even if the business has faced growth issues historically. We are seeing sufficient effort in brand building and operational improvements, which were lacking for much of the decade.

Margins are expected to slightly improve in the coming years, although will normalize at a lower level to what was achieved pre-pandemic. This suggests high competition will restrict TAP’s ability to sufficiently win back the margins through pricing, which we concur with.

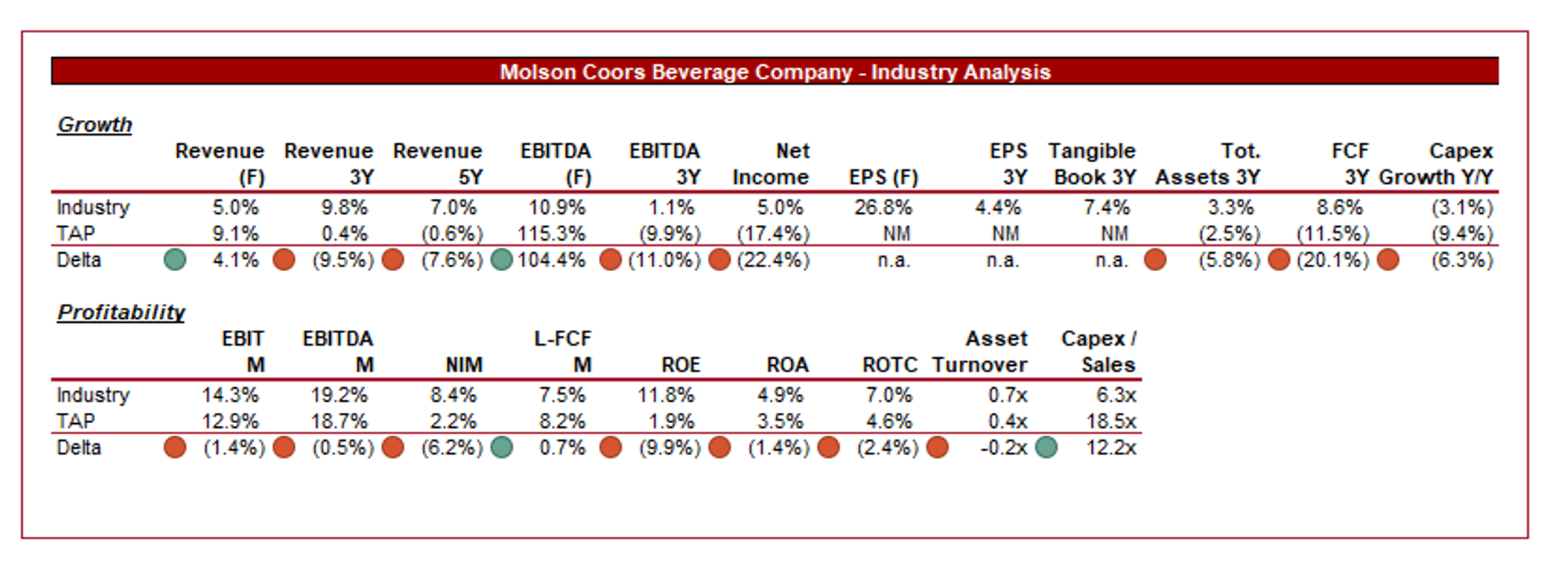

Industry analysis

Beverage industry (Seeking Alpha)

{kind=link}

Presented above is a comparison of TAP's growth and profitability to the average of its industry, as defined by Seeking Alpha (7 companies).

TAP is currently underperforming its peers. Growth has been noticeably below its peers, implying market share loss and an inability to exploit growth markets, restricting its future potential. This implies its response to industry developments and trends has been poor. Once again, this is evidence of poor management, even if the forward guidance has now improved.

TAP also has weaker margins. This is a reflection of its large deterioration in recent months. If we consider its adjusted EBITDA, stripping out one-off/non-cash items, TAP is only slightly above average. This is reflected in LFCF, which is above average. We struggle to see the company gaining an uplift sufficient to offset its growth weakness.

Based on this, we believe a discount to its peer group is appropriate (15-25%). This would adequately reflect its lower growth, as well as its respectable cash flows.

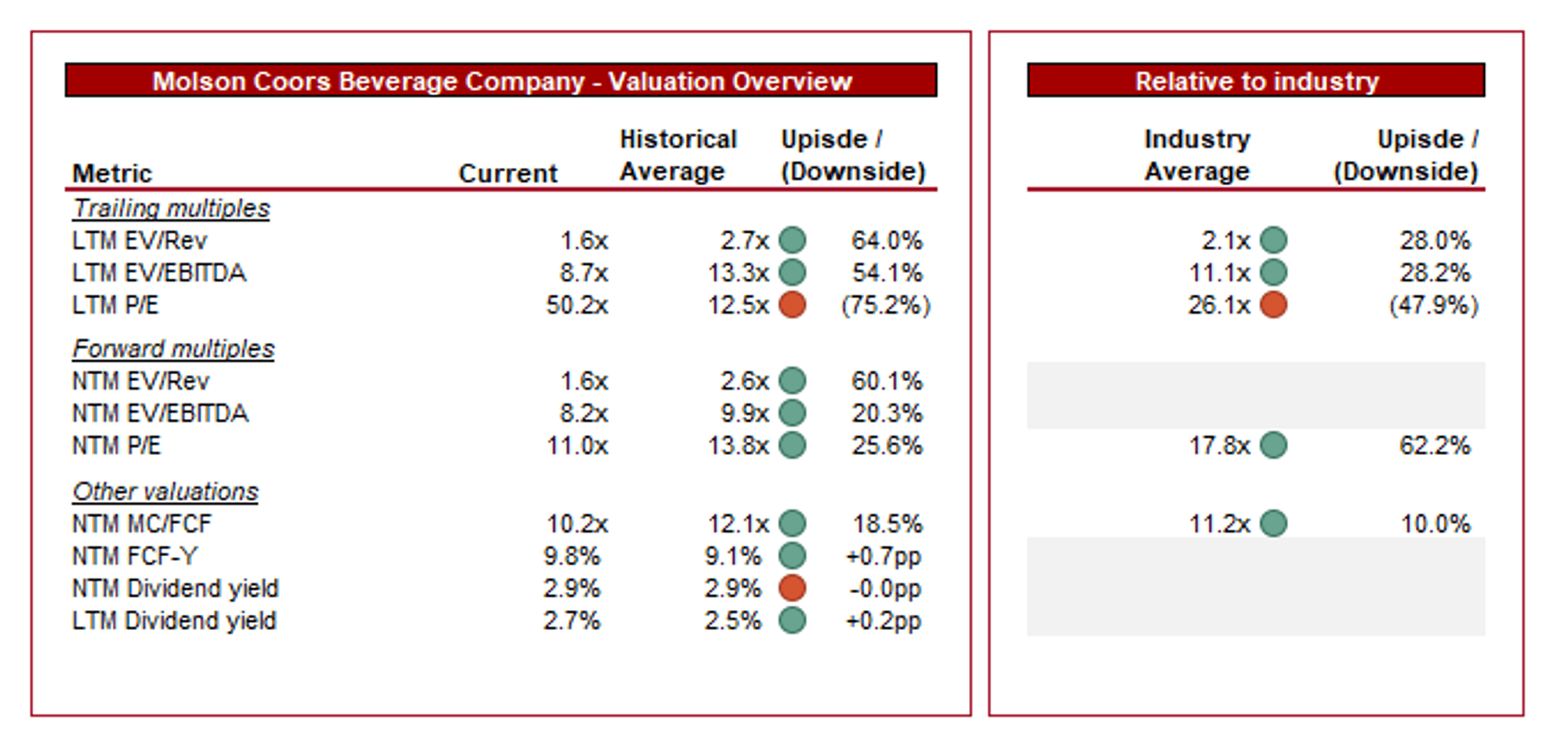

Valuation

{kind=link}

TAP is currently trading at 9x LTM EBITDA and 8x NTM EBITDA. This is a discount to its historical average.

Based on its historical average, we believe TAP should trade at a discount, as this reflects its weaker margins and continued struggles with growth. Despite the industry development, TAP has been unable to achieve healthy volume growth, implying an inherent weakness to peers. The current discount appears large in our view, particularly due to the recent improvement in performance.

Relative to peers, TAP is also trading at a discount. As discussed, TAP is currently underperforming from a growth perspective principally, with the expectation for this to continue beyond the forward period. At an LTM discount of ~28%, we consider TAP reasonably priced, if not slightly undervalued.

TAP’s valuation suggests upside in our view, although not materially so. We are hesitant to implying upside given the historical weakness experienced and the uncertainty surrounding the sustainability of its current improvement. With its FCF yield only 0.7ppts above its historical average, we conservatively suggest patience.

Final thoughts

TAP is well positioned in the industry, with a large range of highly regarded brands. The company is active in responding to industry trends, although is seemingly struggling to keep up with its peers. With lost market share and lost opportunities, we think TAP has materially damaged its future trajectory in the last decade. This said, with a deleveraged balance sheet and tailwinds from the Bud Light fallout, the foundations are present for an improvement in performance.

Before rating this stock a buy, we would like to see further sustainability in its current performance, particularly given the macroeconomic backdrop.

For further details see:

Molson Coors Beverage: Strategy For Growth And Innovation