MCRI - Monarch Casino & Resort: Current Valuation Does Not Reflect Structurally Improved Financial Profile

2023-06-05 15:13:50 ET

Summary

- MCRI’s financial profile has improved substantially following the finished construction of its Black Hawk property, resulting in structurally improved margins and cash conversion.

- Stronger cash generation and low debt allow the business to pursue new growth opportunities faster and/or return capital to shareholders.

- The current TTM EV/EBITDA is ~50% below its five-year average despite the improved business, creating an attractive entry point to the stock.

Monarch Casino & Resort, Inc’s (MCRI) financial profile has reached an inflection point following the phased opening of its transformed Black Hawk property. The opening has resulted in structurally expanded margins and higher cash generation. Although this happened in February 2022, the company is still trading ~50% below its five-year average EV/EBITDA. We initiate a buy rating.

Summary Business Description

MCRI’s two primary assets are the Atlantis Casino Resort Spa (hereafter “Atlantis”) in Reno, Nevada, and the Monarch Casino Resort Spa (hereafter “Monarch Black Hawk”) in Black Hawk, Colorado. The resorts boast ~1,340 rooms, ~2,400 slot machines, and ~70 tables collectively, in addition to the usual resort facilities (restaurants, etc.). Both resorts are owned by MCRI.

The resorts have attractive locations. The Atlantis is located in the vibrant convention and shopping district of South Reno, being the only property that is connected to the Reno-Sparks Convention Center. The Monarch Black Hawk is located in a less urban area than the Atlantis but is no more than an hour away from downtown Denver by car, providing a big addressable market. The resort is even the first property encountered on Highway 119 by drivers coming from Denver. Moving onto demographics, the 4Q22 investor presentation shows that population growth and personal income levels in the Reno and Denver metro areas have historically been higher than the national average.

Financial Performance Has Reached An Inflection Point

In my opinion, MCRI’s financials have reached an inflection point that is not yet reflected in the valuation. The company started converting the Monarch Black Hawk into a full-scale resort with casino and spa facilities in 2013 while it started the phased opening of the hotel in the back-end of 2020. The phased opening ended in 1Q22 and now all facilities are fully open to customers. The transformed Monarch includes a 23-story hotel tower with 516 rooms and ~60 thousand square feet of casino space. The opening resulted in significant market share gains with market share rising from ~10% in 4Q20 to ~28% in 4Q22, according to the 4Q22 presentation.

The financial impact of this opening is very clear when analyzing recent performance. Revenue and EBITDA increased by ~21% each in 2022 as the Monarch Black Hawk ramped up. Looking at 1Q23, which is the slowest quarter of the year, revenue increased by ~8% YoY, which the Monarch Black Hawk mainly drove as weather disruptions in Northern California impacted the Atlantis. Northern California is a significant feeder market to the Atlantis.

I believe that there is plenty of growth to come as the Monarch Black Hawk is still ramping up and weather conditions improve. In 2022, the occupancy rate at Atlantis was 83% while it was 75% at the Monarch Black Hawk as per the 10-K for FY22 . Assuming that Atlantis is at maturity, there is good reason to believe that the Monarch Black Hawk will reach maturity at the same rate. We do not know the occupancy numbers for 1Q23.

Margins and cash conversion evidence the inflection point clearer. MCRI commanded EBITDA margins of 18% and 22% in 2020 and 2019, respectively. Margins increased to a hefty 32% in 2021 and 2022, showing the effect of the phased opening. Of course, some of this is also explained by the fact that margins are impacted by the normalization of operations after COVID. The EBITDA margin retracted slightly to 30% in 1Q23. The improvement in free cash flow to the firm (FCFF) is even more visible. Cash conversion (FCFF/EBITDA) has been negative between 2017 and 2020, but was 67% and 56% in 2020 and 2021, respectively. Cash conversion exploded in 1Q23, reaching 130%, although this is clearly not a normalized figure.

Given its improved cash situation, MCRI paid out a special dividend of $5.0 per share in early 2023 and has instated a recurring dividend of $1.2 per share (~1.75% dividend yield on the current share price of $68.1). Moreover, the improved cash generation allows MCRI to pursue growth opportunities faster, including upgrading its current facilities, development at Atlantis, and M&A. MCRI’s strong balance sheet also supports these prospects, standing at a leverage ratio (Net Debt/EBITDA) of 0.5x at 1Q23.

In sum, the above data persuades me that MCRI’s financial profile has reached an inflection point where margins and cash generation have structurally improved.

Attractive Valuation

MCRI is attractively valued at this point. The stock is down 4.3% YTD and is now priced at $68.1 per share (5th of June, 2023). This is 15.2% down from its 52-week high of $80.2. Looking at multiples, the EV/EBITDA TTM stands at 8.3x vs. its five-year average of 17.3x, according to SeekingAlpha data . We calculate the six-year average to stand at 13.2x, excluding 2020 due to the distortion caused by COVID (the FY22 EV/EBITDA reached ~38.8x).

We set a target price of $81.9 per share based on our 1Q24 LTM EBITDA forecast of $166.6m and 6Y average EV/EBITDA TTM multiple (excluding FY20) of 13.2x to which we apply a discount of 25% to be conservative and reflect only a gradual recovery in the multiple as recession fears weigh on consumer discretionary stocks. We expect the casino operator to maintain its 1Q23 leverage ratio of 0.5x for simplicity.

Source: SEC filings, SeekingAlpha data, and own calculations

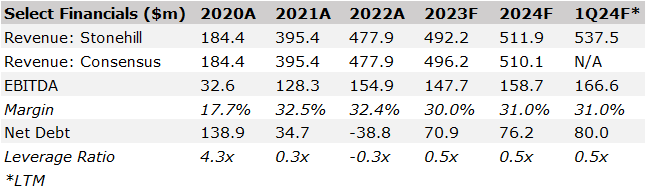

Stonehill’s target comes in at the bottom end of analyst estimates as per the table below.

Source: SeekingAlpha

Stonehill’s EBITDA target is based on moderate growth in revenue over 2023 and 2024, reflecting more normalized revenue levels at the Atlantis post 1Q23 and, to a lesser extent, continued ramp-up at the Monarch Black Hawk. The EBITDA margin estimates used in 2023 and 2024 are marginally lower than FY21/22 as we expect moderate intensification in competition.

Source: SEC filings, SeekingAlpha data, and own calculations

{kind=link}

Headline Risks

Concentration: MCRI only has two properties, so financial performance will be affected significantly if one of them faces difficulties.

Competition: Both of MCRI’s resorts are located in highly competitive environments. There are ~15 casinos in the Reno area and ~21 in the Black Hawk/Central City area, according to the FY22 10-K.

Litigation: MCRI is in an active litigation case with its Monarch Black Hawk general contractor. Expenses related to the case were $7.3 million in 2022 and $1.8 million in 1Q23. Costs from this might be ongoing.

Potential Recession: A recession will increase unemployment and limit discretionary spending, which will impact casino operators/owners like MCRI heavily. Opinions remain divided around whether we will face a hard or soft landing in 2023 with Morgan Stanley being the latest to jump into the soft landing camp as per this article .

Related Party Transactions: 32% of the company is owned by the CEO and President (they are brothers) including some family members, as per the FY22 10-K. This aligns interests, but there is a risk that the management team can use their significant holding to extract more value from MCRI than the 32% shareholding entails. Related party transactions include i) MCRI has leased a portion of the shopping center adjacent to the Atlantis, which is owned by the CEO, President and family members; ii) MCRI leases part of a driveway from the same company that owns the shopping center mentioned above; and iii) MCRI leases various other smaller things (e.g. billboards, storage space, etc.) from entities controlled by the family. For FY22, the total operating and lease expenses related to all of these were $1.7 million, measuring against a total EBITDA of $155.9 million.

Low Liquidity: With its market cap of $1.3 billion and a high level of institutional ownership, trading volumes are limited, resulting in big price swings from relatively small entries/exits to/from the stock.

Conclusion

MCRI’s financial performance has reached an inflection point after it opened its Monarch Black Hawk, resulting in structurally better margins and cash generation, but the stock is trading at a discount to its long-term multiples. This presents an opportunity to enter the stock and gain exposure to a sound business with considerable rerating potential. We initiate a buy rating and will consider turning around if the economy enters a severe recession or there are meaningful regulations impacting the gaming industry in MCRI’s markets.

For further details see:

Monarch Casino & Resort: Current Valuation Does Not Reflect Structurally Improved Financial Profile