MCEM - Monarch Cement: A Review Of The Bull And Bear Cases

2023-08-18 03:57:38 ET

Summary

- Monarch looks quite cheap at first glance, but it may not be due to its cyclical earnings and high capital intensity that leads to lumpy ROIIC.

- As the stock tends to move with ROIIC, the stock’s outlook depends on each investor's views of cement consumption going forward.

- If we are closer to a top and on our way down, I see the stock dropping closer to $120 or 1.3x its book value per share.

- If demand is sustainable due to high infrastructure spending, I see the stock trading closer to $188 per share based on EBITDA of $107.5 million and a 6x multiple.

- I usually invest with the mindset that typical cyclicality holds up over time, so I am waiting for the stock to trade closer to my bear case target of $120.

The Monarch Cement Company (MCEM) recently reported stellar Q2 financial results that contributed to what was a record breaking H1 2023. In H1 2023, revenue was up 27.2% year-over-year, operating income was up 63.5% year-over-year, and capital expenditures were down 15% year-over-year. This growth is even more impressive when considering that it was on top of a record breaking 2022.

With these results, the stock looks very cheap despite being up nicely year-to-date. It is currently trading between 5x and 6x trailing twelve month EBITDA on rising earnings and declining capital expenditures, shareholders will receive a 3% dividend on September 8th which includes a special dividend, and management is actively repurchasing shares. This all means that at the moment the stock is cheap, returns on incrementally invested capital are high, and management is returning a portion of excess cash to shareholders. This type of stock is usually a good one to buy.

However there are some risks that are worth taking note of the main one being that the business is cyclical despite growing revenue and earnings steadily over time. The cyclicality reveals itself through an examination of Monarch's ROIIC through the years, which I will review in more depth below. The stock tends to trade with this metric so it is worth keeping an eye on and worth understanding the factors that drive it up and down.

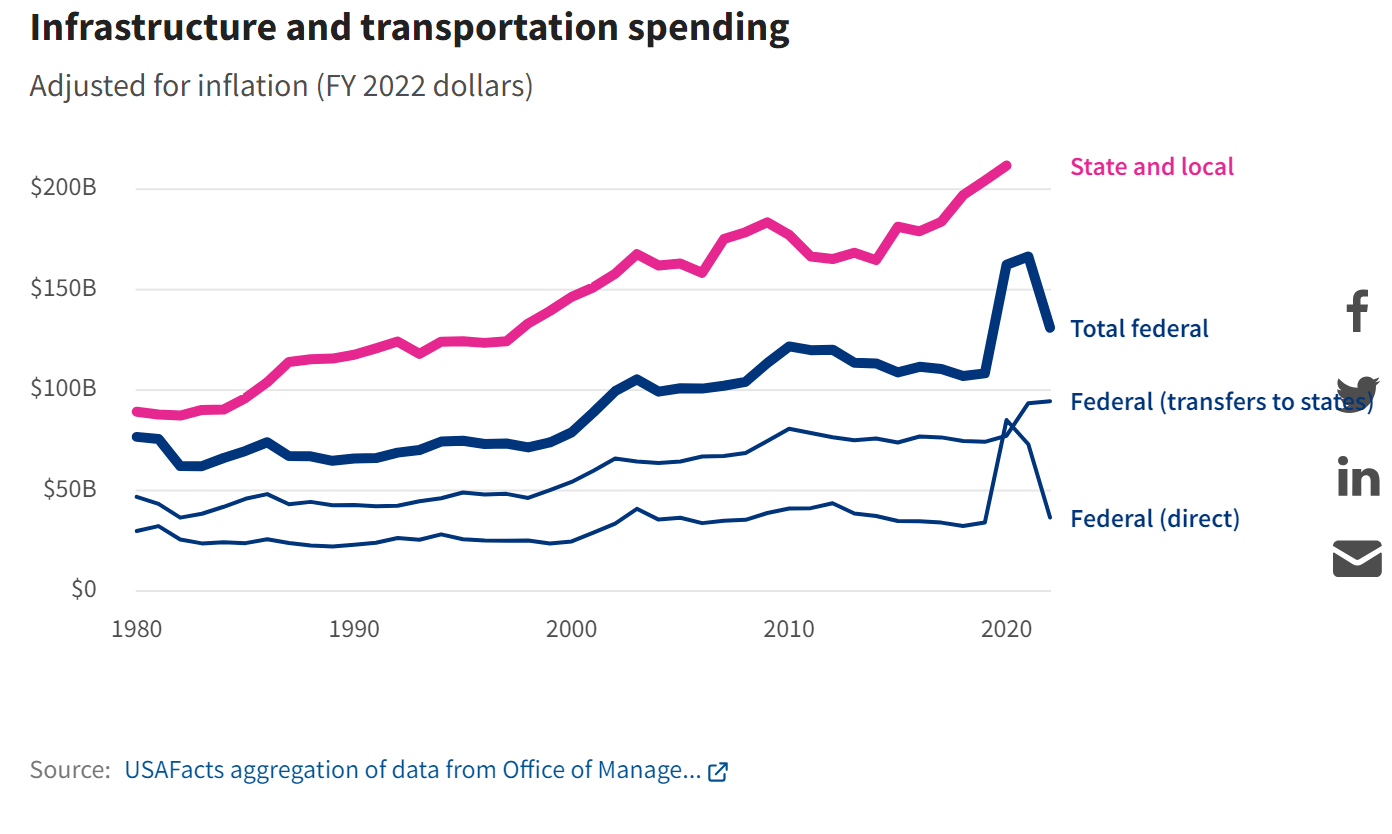

Additionally, there is economic risk. While U.S. infrastructure spending has surely been a tailwind for Monarch, a drop in economic activity could lead to lower ROIIC which would in turn hurt the stock even if it looks cheap due to its earnings multiple. Finally, the stock trades on the OTC exchange and as such does not command as high of an earnings multiple when compared to its peers.

U.S. Infrastructure Spending (USAFacts)

{kind=link}

Most of these risks are short term but are more important to keep an eye on due to the stock's recent rise. Longer term, I imagine Monarch will provide fine returns for investors as returns on incrementally invested capital remain high on average despite being very volatile year to year. The short term volatility could also help to juice longer term returns as the company can buy back stock when it is cheaper, and it could also help to attract buyers that are interested in acquiring the company.

Business Overview

Monarch manufactures and sells Portland cement, and has partial or full ownership of subsidiaries that are engaged in the ready-mix, concrete products, and building materials business. Concrete sales tend to be very localized as the cost of transportation is quite high.

Monarch sells its products primarily in Kansas, Iowa, Nebraska, Missouri, Arkansas and Oklahoma and has strong relationships with its customers due to its long history of operating in the area. This gives it somewhat of a local monopoly as businesses in the region can't buy cement from overseas or different regions due to the high costs, and will likely buy from Monarch due to the trust it has built in the area. Monarch has been in operation since 1908.

Past Financial Results

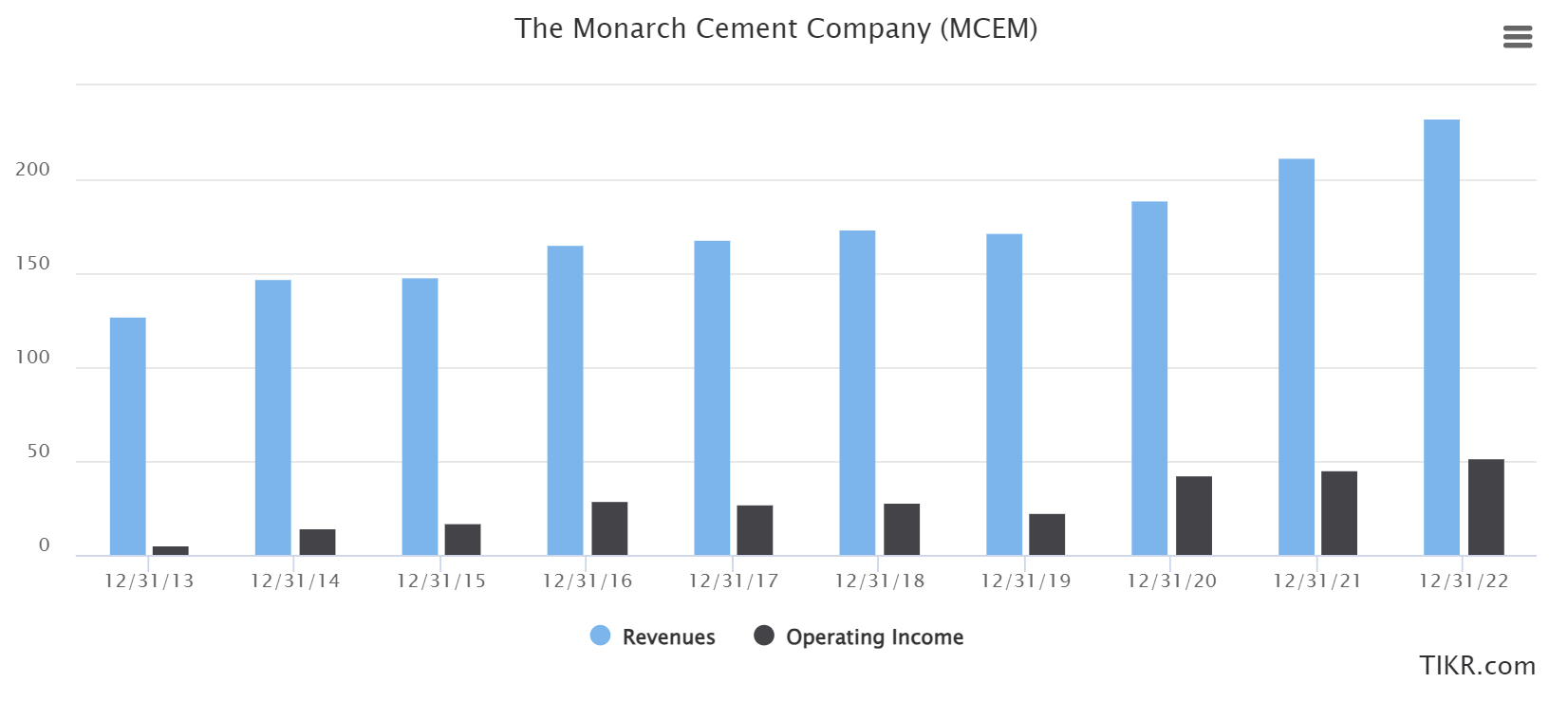

Monarch's financial results over the past decade have been impressive and show the monopoly like characteristics of the business. Revenue, margins, and earnings have marched upwards while the company has returned increasingly more capital to shareholders.

Since 2013, revenue has grown at a 7% CAGR and operating income has grown at an astonishing 30% CAGR. These results are a true testament to the operating leverage and pricing power that Monarch commands as it continues to generate high returns on invested capital.

Monarch Revenue and Operating Income (TIKR)

{kind=link}

Returns on invested capital have been lumpy since 2013 but the average in that period is about 13%. Over the past 5 years, average ROIC is closer to 16%. This recently higher average can be attributed to sustainably strong demand that has led to higher prices and more volume of cement sold.

Monarch does not generate the 20%+ ROIC that you would find in a tech or less capital intensive business that also has monopoly like characteristics, but the cement industry is also less likely to be impacted by innovations and new technology. Additionally, the high capital intensity and strong regional ties creates barriers to entry that has allowed Monarch to maintain an ROIC above its cost of capital for decades.

Capital expenditures have been equal to about 10% of revenue over the past decade. This is quite high and is greater than Monarch's net income in some years, but it is never higher than cash from operations. This efficient conversion of earnings into cash flow allows Monarch to return cash to shareholders via dividends and share repurchases. In the past decade, Monarch has return $87.5 million to shareholders while it has generated $134 million of cumulative free cash flow. I don't see any reason to believe this ratio of capital returns won't continue going forward as the company continues to generate high ROIIC with little risk of competition.

This doesn't mean that there will not be short term volatility. Due to the cyclicality of demand and Monarch's high capital intensity, there are years where returns on incrementally invested capital decline or are negative. It is best to invest in the stock in these years as this return will continue to revert to its mean over time. After three to four years of high ROIIC, Monarch may be due for a down year.

Monarch's ROIIC (Created by Author)

{kind=link}

The stock did not follow the trend in 2018 when ROIIC was -12.66% when the stock rose 50%+ that year. This move against the trend occurred because the stock rose in sympathy with Ashgrove Cement which was acquired. After this rise, Monarch's stock steadily dropped in 2018 and 2019 as fundamentals caught up with the valuation.

Current Valuation, Risk and Reward

Monarch looks cheap at first glance but as with all equity investments, the value of the stock depends on the future.

Monarch's current trailing twelve month EV/EBITDA is between 5 and 6, and is likely to be even lower after the next 6 months as H2 2023 EBITDA will likely be much higher than H2 2022 EBITDA. This valuation, along with the company's history of averaging a high ROIC, means there's a good chance the stock will perform well from here for investors with long-term holding periods.

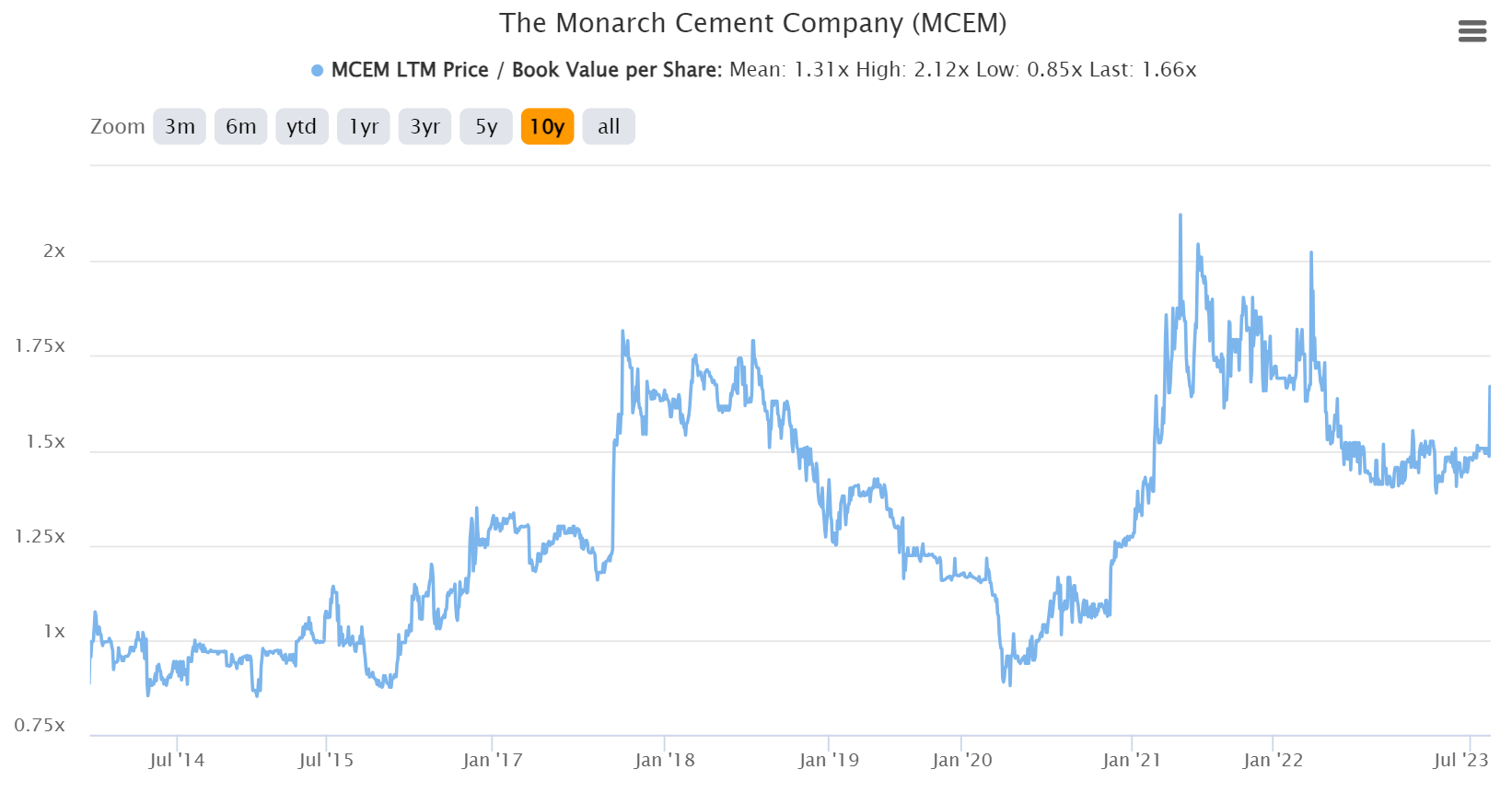

On the other hand, the stock is trading at a relatively high price-to-book ratio of about 1.65. Cash flows ultimately drive returns but often when Monarch's stock is trading at a high price-to-book ratio, it means that it is close to a top in cyclical demand for cement.

Monarch LTM Price to Book Ratio (TIKR)

{kind=link}

This does not necessarily mean that a downturn is coming as this time could truly be different due to the tailwinds from infrastructure spending, but it is something to keep in mind. If it were indeed near the top of a cycle, the stock could trade closer to 1.3x book value, the 10 year average, which would put the stock at around $120 per share. Again, book value is not a gauge of future cash flows but it can be a good gauge of where we are in the economic cycle.

Monarch's stock may look cheap relative to earnings regardless of its book value or where we are in the economic cycle, but the drop in book value per share would be caused by lower ROIIC which would indicate lower free cash flow. This would justify the lower book value multiple regardless of earnings.

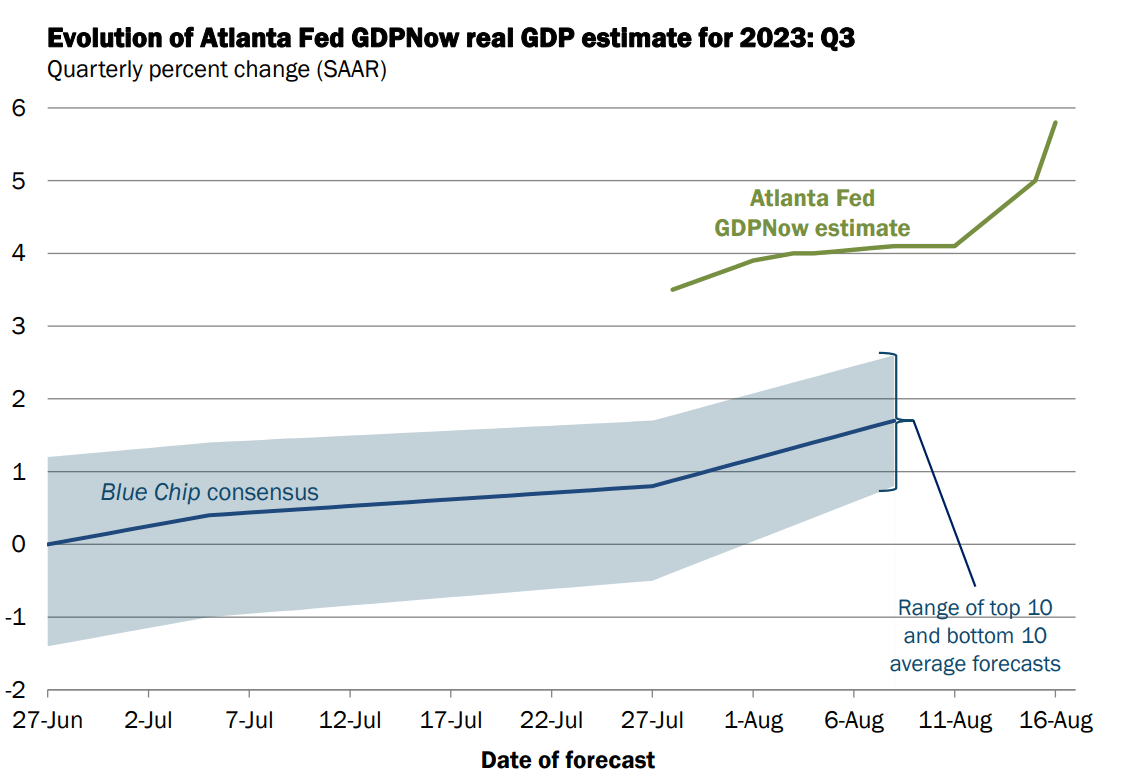

Of course, things could be different this time as many signs point to sustained economic growth which would lead to higher demand for cement products. For example, the Atlanta Fed's latest GDPNow Q3 2023 real GDP estimate was updated to a surprising 5.8% on August 16th.

{kind=link}

I like to keep the mean reversion point of view in mind as historical trends usually continue into the future.

If demand does end up being more sustainable, there could be solid upside for Monarch's stock as I estimate it will trade at 6x its current EBITDA run-rate of $107.5 million in this scenario. Assuming the company holds $50 million of net cash and has 3.7 million shares outstanding, the stock would trade at $188 for 30% upside over the next year.

An investor's thoughts on the probabilities of these scenarios depends on their opinions of economic growth, infrastructure spending, and the Federal Reserve's interest rate decisions going forward. I generally take an approach that assumes reversion to the mean is more likely than not and I plan on revisiting the stock if it trades closer to $120 per share, or 1.3x its book value.

There is also potential upside if Monarch is acquired. Ashgrove Cement was acquired in 2017 for around 11x EBITDA and this multiple would mean Monarch would be acquired for a 100% premium over what it is currently trading at. I prefer not to invest based on hopes of an acquisition, but this could be thought of as a right-tail event that would benefit long-term shareholders.

Notice the sharp increase in the stock price in 2017 that occurred at the time Ashgrove Cement was acquired.

It may also be tempting to say the stock should trade at this 11x acquirers multiple but as long as it trades on the OTC exchange, it will likely trade at a discount valuation compared to its peers.

Final Thoughts

Monarch looks cheap at first glance but due to its high capital intensity and lumpy earnings that lead to volatility in its ROIIC, its currently low earnings multiple does not mean the stock is an easy buy. If Monarch's earnings trends from the past continue, the company could be due for a down year as its ROIIC has been high for 3.5 years straight. If this down year did occur in 2024, the stock's premium over its typical multiple of book value per share would dissipate.

If government infrastructure spending and continued economic growth mean that past trends won't continue and that this time is truly different from the past, the stock could trade closer to $188 per share based on forward EBITDA of $107.5 million and a 6x EBITDA multiple. Additionally, there is the right-tail upside scenario of an acquisition at closer to 11x EBITDA for a 100% premium over the current stock price. There is precedence for this multiple from the Ashgrove Cement acquisition in 2017.

I personally don't want to bet against the cement industry's typical cyclicality, so I will wait to revisit if demand softens and the stock trades closer to $120, or 1.3x its book value per share.

For further details see:

Monarch Cement: A Review Of The Bull And Bear Cases