MCEM - Monarch Cement: Efficient Capital Allocation With An Impressive ROIIC

Summary

- A business that has been managed and controlled by the same family since decades with high insider ownership.

- 100% shareholder capital structure.

- A good ROIC of 14% with an even better ROIIC metric.

- A reasonably valued investment with a >15% yearly total return expectation over the next years.

Overview

The Monarch Cement Company manufactures and sells cement principally in the State of Kansas, the State of Iowa, southeast Nebraska, western Missouri, northwest Arkansas, and northern Oklahoma. The company was founded more than a century ago.

Insider ownership is above 20% (Page 5 & 6 Q3 Financials ). The management team has been in place for decades and controls a big part of the company, especially considering they own class B shares with 10X voting rights. I am favorable to companies which have big insider ownership because this likely aligns management of the company to the shareholders' interest.

The industry of cement production is not exactly something that attracts the attention of many investors that seek quick and exciting returns in the short term. Additionally, Monarch is a small cap at the border to a micro-cap. This name is too small to attract the attention of big value investors.

The company has practically 0 debt . There are only some minor long term liabilities on the balance sheet in the form of pension benefits, but these have been reduced by over 70% in the last decade. This puts this company in a very good spot because it can:

a) Distribute all the excess earnings to the shareholders and

b) Should they require cash because of an economic downturn or increased investment needs, they can easily issue some debt

Thesis

"The higher return a business can earn on its capital, the more cash it can produce, the more value is created. Over time, it is hard for investors to earn returns that are much higher than the underlying business' return on invested capital." Warren Buffett

Producing cement is a capital-intensive business. The companies that operate in this industry will have to reinvest a good part of their earnings into new equipment in order to grow, or even only sustain the business. Monarch has been reinvesting about 50% of their operating profits after tax into their operations. I have analyzed their ROIC (return on invested capital) and ROIIC (return on incremental invested capital) of the past years. Substantial improvements have been made to the allocation of capital over the years. This company is now returning 25% on every incremental capital invested. If they can keep up this allocation efficiency, then the stock price should do very well.

As stated by Warren Buffett (quote above), over the long term the share price returns tend to converge to the underlying business returns. Invested capital is the cash needed to run the underlying business. All the excess cash produced can be distributed to shareholders. As such, the ROIC is a good proxy for what the total-return of an investment in a stock will be (over the long run), given the valuation multiples don't move excessively.

ROIC: Return On Invested Capital

ROIC formula = NOPAT / Invested capital

NOPAT = EBIT *(1-Tax Rate)

Invested Capital = Equity + Debt or Working Capital+ Long Term Assets

In plain English, ROIC provides the return the capital structure (debt + equity holders) is producing.

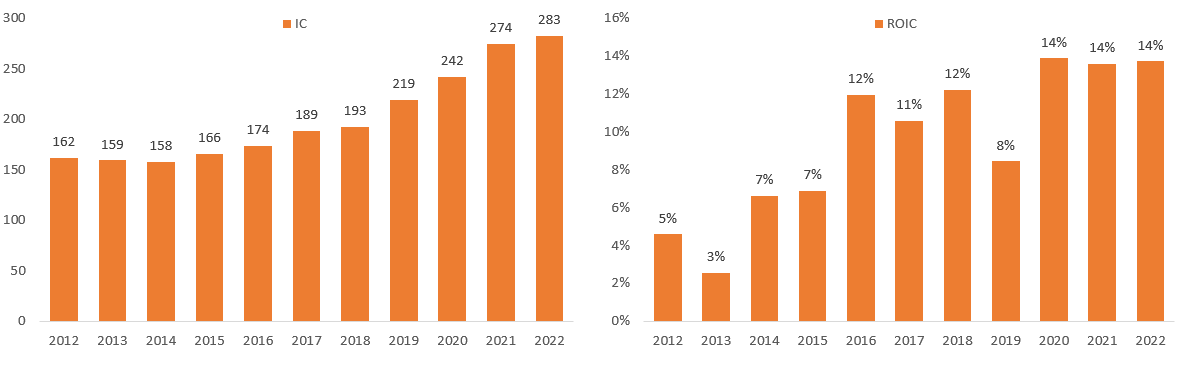

Monarch has improved very handsomely on this metric over the past decade. As they have improved considerably on their incremental capital allocation (which we will explore in the next paragraph), further investment and growth into the business is likely. After all, if they can invest in the company and expect to have returns in excess of 14%, then such a decision produces value for the shareholders.

Since 2012, the ROIC has trended up consistently to reach 14%. Considering that this company has practically no debt, this return is 100% attributable to shareholders.

Also worth mentioning, since 2012 the invested capital (IC) has increased consistently. This is providing shareholders with the compounding effect of higher returns on bigger capital investments. Invested capital now stands at $283 million, up from $162 million a decade ago.

Invested Capital & Return on Invested Capital (SA & Author)

{kind=link}

ROIIC: Return On Incremental Invested Capital

How has Monarch managed to increase the ROIC from a 5% level to a 14% in 2022? By allocating incremental capital at higher rates. Imagine if you had a $100 investment with a return of 5% and you add on another $100 to the initial investment for a return of 25%, then you end up having a $200 investment with an average return of 15%.

Over the past decade, MCEM has re-invested on average 45% of their yearly net operating profits into the business. This incremental investment produced on average a return in excess of 25% (ROIIC). Capital allocation at Monarch has become very efficient and the product is an overall respectable ROIC.

If you project ROIC into 2033, utilizing a NOPAT re-investment rate of 45% and a ROIIC of 25%, then the overall ROIC in a decade's time will be 20% on $642 invested capital (up from 14% ROIC on $283 million capital invested). This translates into NOPAT going from $40 million in 2022 to $130 million in 2033. Assuming the market multiplier on earnings would not change, then that would imply a market cap of $1.3 billion. This is a 14% CAGR appreciation, before accounting for dividends and buybacks, which could add another 5% per year to the performance.

Valuation

Even though MCEM is reasonably valued in terms of earnings multipliers, the improved business metrics have not gone unnoticed by the market. In fact, as you can see in the chart below, the p/b ratio has expanded over the past 10 years from 0.80 to 1.5.

Price / Book Ratio ( SA )

{kind=link}

From an EV/EBITDA metric, the company is in line with its own 10-year average of 5.4X.

EV / EBITDA Ratio ( SA )

{kind=link}

These valuation multiples and p/b levels might appear conservative but they are also specific to the industry.

From a growth perspective, this company has done extremely well. In part because they started from a very low base, but especially because they have been employing their capital in a very efficient way. One could argue that a company that has 13% free cash flow growth might have a more favorable multiplier than the one the market has been attributing to it in the past.

Growth Metrics (SA & Author)

Overall, MCEM valuation seems fair considering there are macroeconomic clouds on the horizon. One could argue that there might be better entry points down the road, but since this is a quality business, I don't like to postpone an entry and gamble on a possible dip that might never come.

Risks

Cement producers are capital intensive and depend on the regional economy. Products need to be shipped nearby because of the nature (bulky and heavy) of the product. The building industry is cyclical and could suffer from the recent interest rate developments since building activity might fall.

Monarch has an investment portfolio as reported in their 3rd quarter 2022 financi als . The following table shows the gross unrealized gains (losses) recorded in the income statement aggregated by the investment category:

Monarch Financials (Monarch Financials)

{kind=link}

2022 net income will be affected by the negative equity performance of these investments since these unrealized gains get reported in their earnings. These figures ($14 million loss) are material but pose little risks going forward, in my opinion, since the total size of these investments after the write-downs is relatively small ($37 million). To put things into perspective, their 2021 free cash flow was almost $30 million.

This investment might not be ideal for some who are looking for a quick appreciation. This stock has long periods of low volatility and the industry is kind of boring. Additionally, the fact that management has been at Monarch for decades and holds a big stake in the company makes this investment more of a "steady as it goes" story. I see the probability that a bigger company makes a high takeover offer as low, because of the familiar nature of this business (the Wulf family has been in control of this business for almost a century now).

ESG: Cement manufacturing is energy intensive and produces CO2 emissions. This industry will have to invest in procedures to hold pace with the increased scrutiny on this matter. I don't think the product is at risk of being disrupted, but alternative ways of construction could put future growth at risk.

Conclusion

Monarch is a boring investment. Cement itself is of low-value. But since its cumbersome to transport, shipping the product from far away makes it uneconomical. This creates a certain moat for producers to capture their regional market.

The company is debt free and has proven over the past decade that they are in the position to efficiently allocate new capital. The current ROIC of 14% is good and their ROIIC >25% is outstanding. I would not be surprised to see MCEM produce a total return in excess of 15% CAGR over the next decade.

The market cap of this company is small and, as such, excluded from the big passive indices and precluded big value investors. Overall, I think this is a good investment for those who are patient to buy and hold for several years.

For further details see:

Monarch Cement: Efficient Capital Allocation With An Impressive ROIIC