MCEM - Monarch Cement: Good Company But A Bit Of A Risky Stock

2023-05-03 16:40:30 ET

Summary

- The Monarch Cement Company is a $422-million market cap US-based company that produces and sells Portland cement.

- MCEM looks like a fairly stable company from a fairly cyclical industry. It has one of the highest EBITDA margins among its peers.

- The upside that I derived from the EV/EBITDA calculation is barely 10% - I'd like to see a much larger margin of safety in a pink sheet stock.

- I rate MCEM stock as a Hold.

The Company

Based on Seeking Alpha's description, The Monarch Cement Company (MCEM) is a $422-million market cap US-based company that produces and sells Portland cement. They also offer masonry cement, ready-mixed concrete, and other building materials. The company mainly serves contractors, dealers, and governmental agencies in certain states including Kansas, Iowa, Nebraska, Missouri, Arkansas, and Oklahoma. MCEM was established in 1908 and is headquartered in Humboldt, Kansas.

Since MCEM is listed as a pink sheet stock, the most trustworthy information about the company and its potential can only be found in its SEC filings and external sources such as research studies and market outlooks. Unfortunately, there are no insights from the Street regarding revenue and EPS estimates.

{kind=link}

Due to its status as a pink sheet stock, MCEM has not received coverage from major banks, resulting in a lack of forecast estimates. So the stock remains quite underfollowed despite its $422-million market cap. Even the about-same-sized Peru-based Cementos Pacasmayo ( CPAC ) trades on NYSE and has EPS estimates up to FY2025.

Thus, if MCEM can differentiate itself from its more visible peers from a fundamental perspective, these fundamental characteristics may give investors some edge.

The Fundamentals

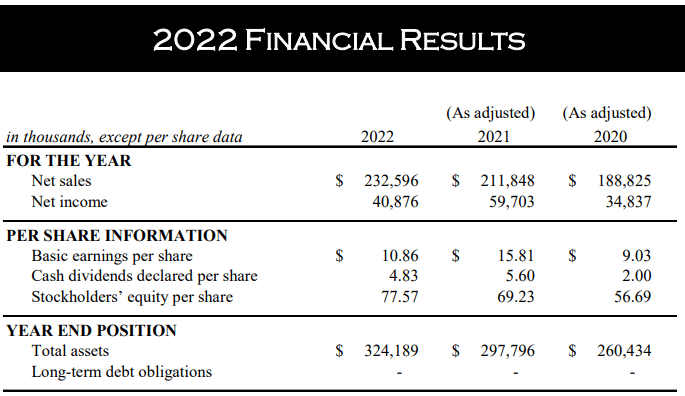

The company divides its operations into 2 lines of business - the Cement Business [60.2% of total sales] and the Ready-Mixed Concrete Business [39.8%]. The company had consolidated net sales of approximately $232.6 million in FY2022, which is $20.8 million or 9.79% higher than last year. The Cement Business segment contributed mainly to this growth, with an increase of $19.4 million in sales, driven by both volume sold and price increases. Specifically, the Cement Business sales saw an 8.0% rise in volume sold and a corresponding $9.7 million increase in sales due to price increases. In contrast, the Ready-Mixed Concrete Business segment witnessed a decline in sales volume by 3.4%, resulting in a decrease of $2.4 million in sales. However, a price increase offset this, leading to a $4.7 million increase in sales.

{kind=link}

Note: MCEM's 2022 annual report link

The company's cost of sales increased by $13.8 million in 2022 compared to the previous year. This dynamic was seen across all of MCEM's business segments. Despite the rise in COGS, the company's gross profit margin was 30.9% in FY2022, slightly higher than the previous year [30.6%]. The SG&A expenses increased by $1.7 million in 2022, which didn't stop the EBIT margin from staying stable and even growing a little bit [21.5% in FY2022 vs. 21.14% in FY2021]. MCEM experienced an unrealized loss on equity investments of ~$9.3 million compared to last year's gain of ~$14.2 million - hence the net income plunge of -31.5% YoY that you can see from the snapshot above.

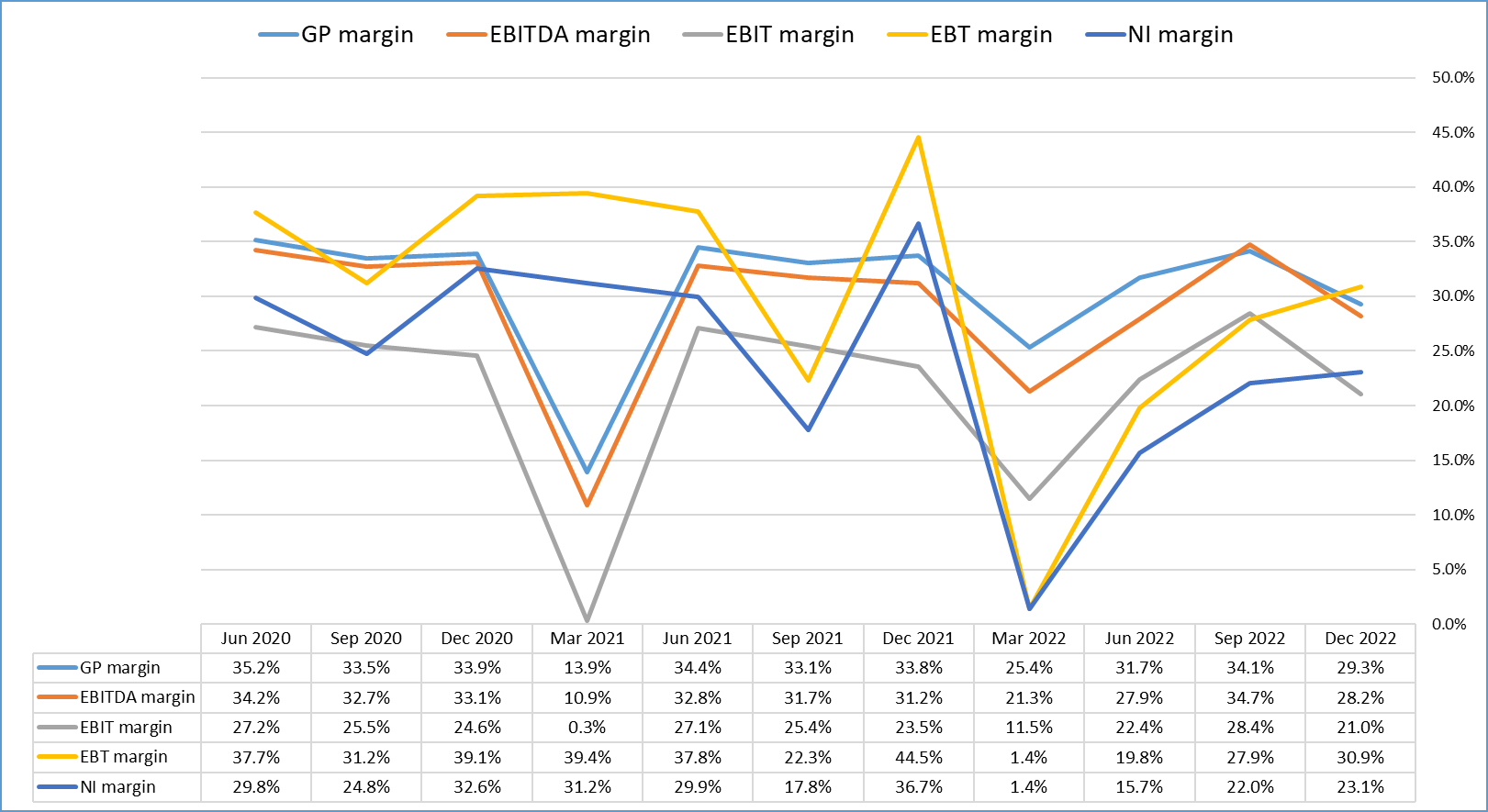

If we look at the company's quarterly financial results, we will notice quite impressive levels of EBITDA margin, which, regardless of the seasonality of sales, have never fallen below 10% in the last 11 quarters:

{kind=link}

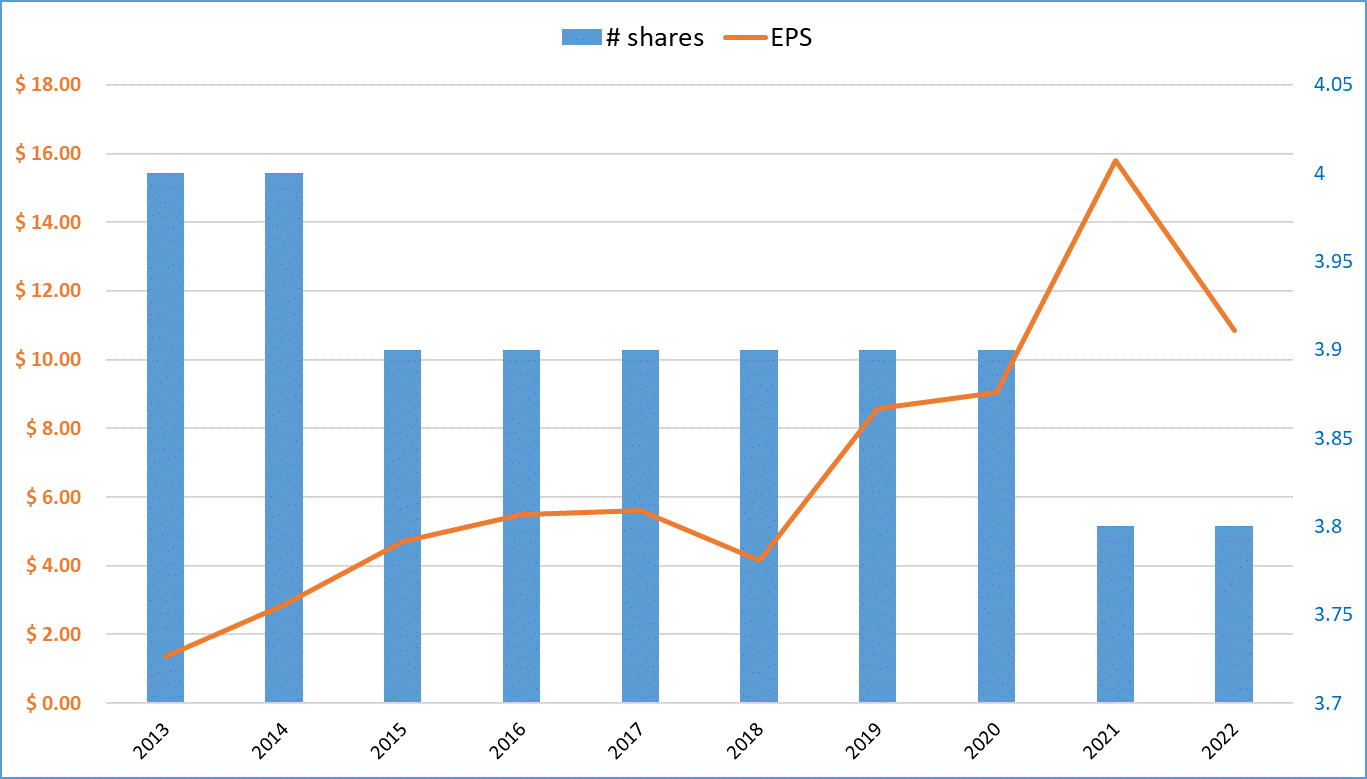

MCEM has a history of share buybacks that I would like to point out:

In November 2020, the company began a tender offer to buy up to $5 million in shares of either Capital or Class B shares for $60-$70 per share. The offer ended in December 2020, with the company buying 62,920 shares for $4.4 million and immediately retiring them. In Q4 2020, the company repurchased 1,040 Capital shares for $72,800 and retired them. In May 2021, the company bought and retired 34,610 Class B shares for $101.00 per share, spending a total of $3.5 million. Finally, in December 2022, the company bought and retired 58,186 Class B shares for $106.00 per share, spending $6.2 million.

Source: MCEM's 2022 annual report, summary by the author

The decrease in shares outstanding really had a very positive impact on the company's EPS, allowing management to grow this metric by almost 7 times since 2013 [annual CAGR = 26%]:

{kind=link}

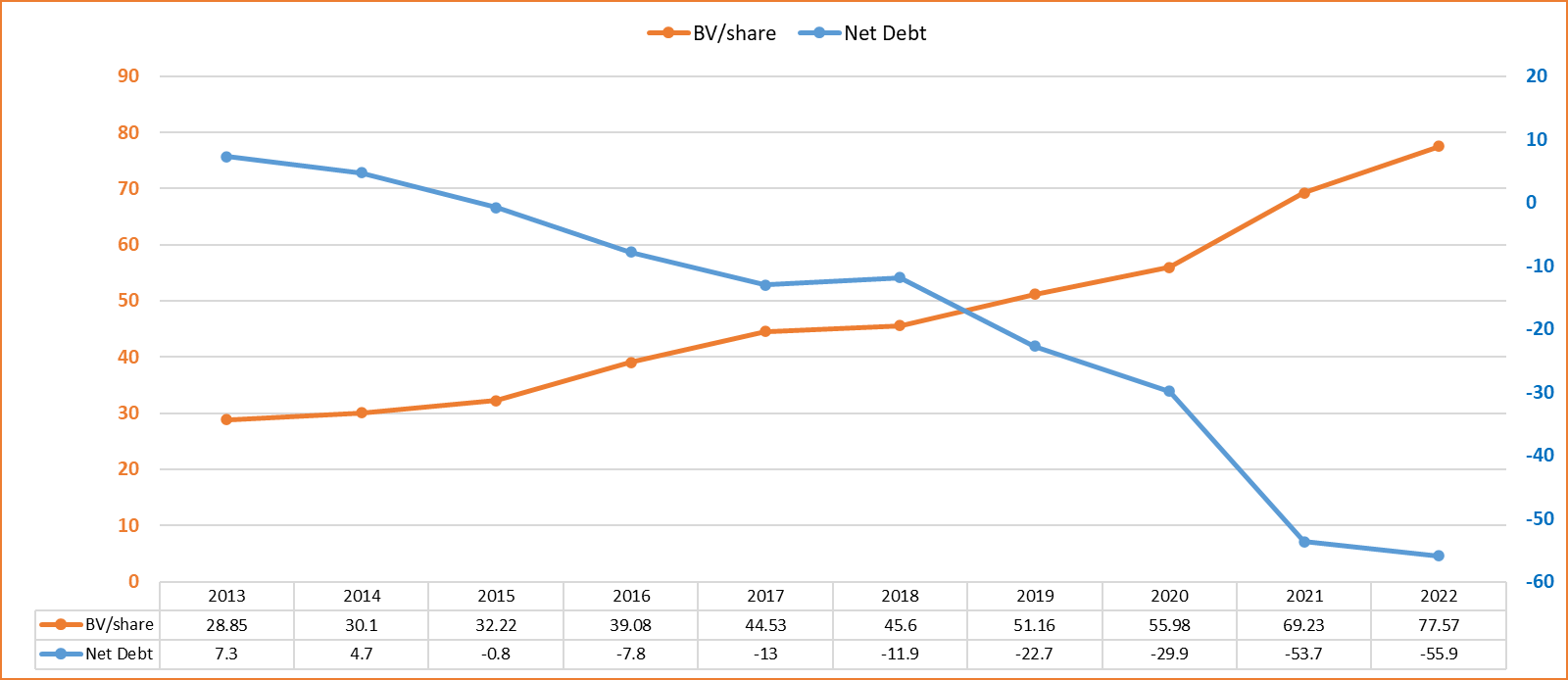

In terms of the company's balance sheet, MCEM looks very, very interesting. Net debt is negative [and keeps rolling lower], and book value per share is growing at a long-term CAGR of 11.6% on an annual basis:

{kind=link}

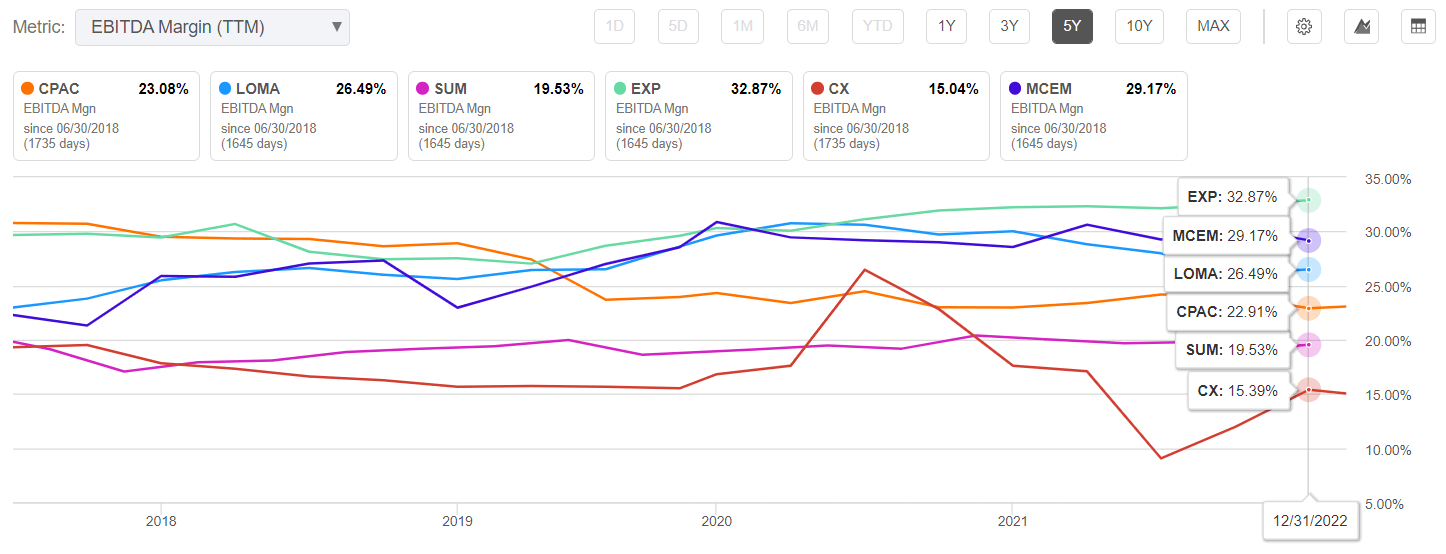

Based on the results of examining the company's financial statements, I could not see any bright red flags - Monarch Cement looks like a fairly stable company from a fairly cyclical industry. And it's worth noting that MCEM has one of the highest EBITDA margins among its peers, even among those many times larger than MCEM itself:

{kind=link}

Valuation

I expect MCEM to generate an EBITDA of $61.1 million in FY2023 with an EBITDA margin of 25%, on moderate year-over-year revenue growth of only 5%.

Right now MCEM stock trades at 5.41x TTM EV/EBITDA which is 30% less than the Materials sector and 22% less than Cementos Pacasmayo's multiple. Let's calculate MCEM's enterprise value together:

EV = Market cap + Debt - Cash - Pension Obligations [if any]

EV = ($114 * 3.763222M shares) + $0 - $55.9M - $11.34M

EV = $361.77 million

If MCEM's EV/EBITDA rises to at least 6.5x, which would already include some sort of pink-sheet discount, then MCEM's enterprise value should be $397.15 million. If we convert this value back to market capitalization, we get $464.39 million, which is 9.8% more than the company's current market cap.

The Verdict

Monarch Cement Company faces several risk factors that may deter potential investors. The company is heavily reliant on the construction industry, which is prone to economic downturns, and the cement and concrete market is highly competitive. The company's sales are mainly concentrated in 6 states, which could be adversely affected by regional economic conditions and changes in building codes and regulations. Additionally, Monarch Cement Company depends on key customers and suppliers, and disruptions in the supply chain could negatively impact operations. Changes in regulations, natural disasters, and fluctuations in financial markets are also significant risk factors that may affect the company's securities.

Moreover, no one should ignore the risk of the very low liquidity of MCEM stock - according to Seeking Alpha, on average, only 516 shares are traded daily, which is less than 60 thousand dollars. The risk of volatility is too high for MCEM - yes, the company is 24.68% owned by insiders, but the remaining 3/4 can potentially exert a lot of pressure on the market in case of massive selling.

In addition, the upside that I derived from the EV/EBITDA calculation is barely 10% - maybe I was too conservative in my core assumptions, but for the Buy rating I would like to see a much more pronounced margin of safety. That was 6 months ago - before MCEM was up 14%. So I am rating MCEM as a Hold this time around.

Thank you for reading!

For further details see:

Monarch Cement: Good Company, But A Bit Of A Risky Stock