MONRY - Moncler: A Solid And Continuously Growing Luxury Company

2023-09-19 03:46:47 ET

Summary

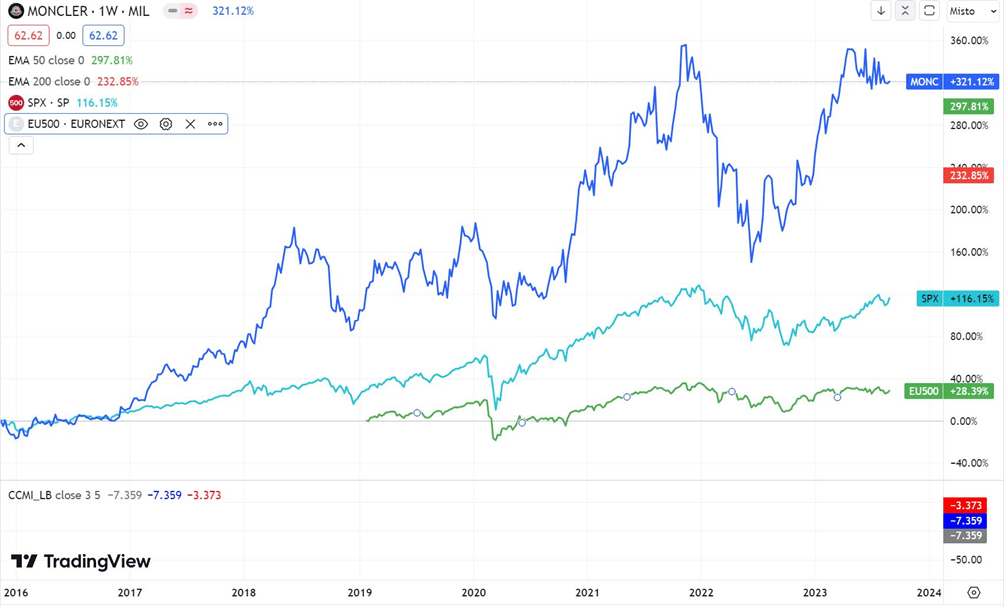

- Moncler has been outperforming the S&P 500, Europe 600 Index, and the ETF dedicated to luxury stocks, "Amundi S&P Global Luxury UCITS ETF," for years and is likely to continue outperforming in the coming years.

- For the entire year 2022, Moncler's revenue was €2.6 billion, with a 25% growth compared to the previous year, while net profit reached a record €606 million with a 23% margin (compared to €411 million in 2021 and 20% margin).

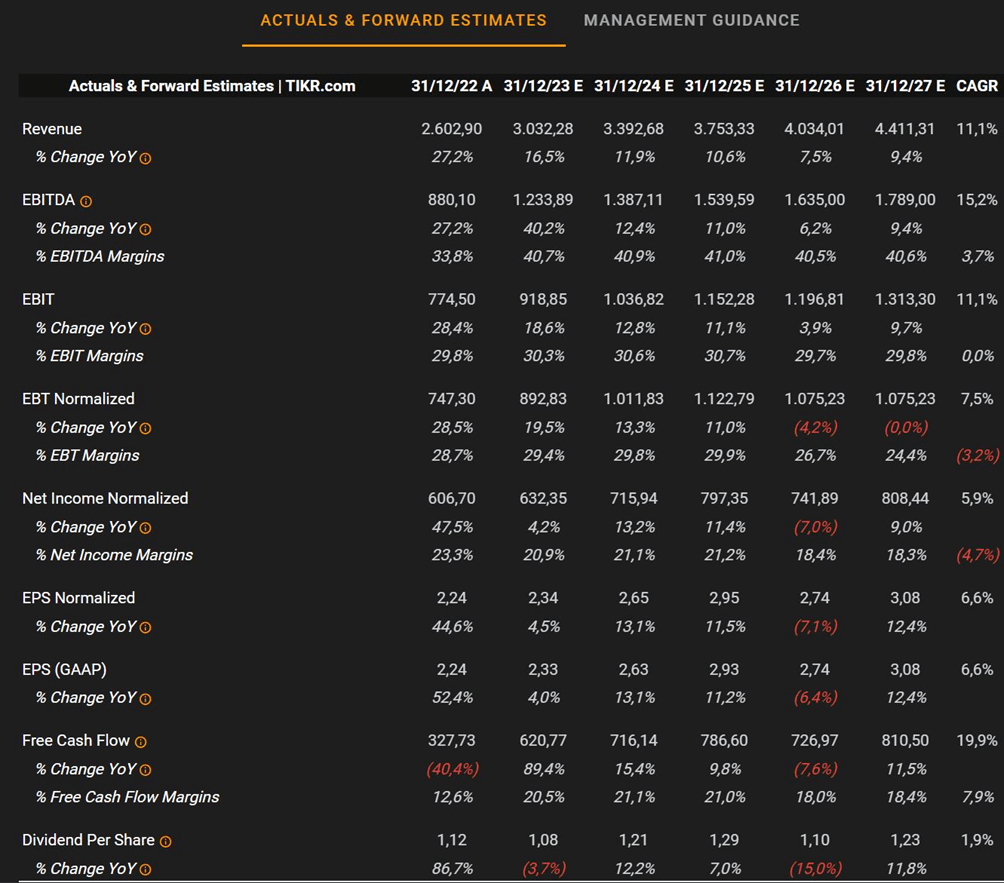

- Despite economic uncertainties, Moncler continues to have strong growth projections, with a projected revenue CAGR of 11% and a Free Cash Flow CAGR of 19%.

- Moncler is a well-managed company with an extremely solid balance sheet, and based on my evaluations, it appears to have a reasonable price today.

- I consider the stock a buy at current valuations and a strong buy around €53.00-€55.00 per share, with a target of approximately €120.00 per share by 2027.

Editor's note: Seeking Alpha is proud to welcome Alessandro Zanga as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

My investment thesis for Moncler ( MONRY , MONRF ) is that it is a company managed perfectly by its CEO Remo Ruffini, who is also the largest shareholder. Positioned in a growing sector, the company has demonstrated continuous growth, enviable margins, an excellent balance sheet, a renowned brand, and outstanding product quality. All of these factors make it an ideal investment for the medium and long term. The stock price is currently only slightly undervalued (around $63.00 per share), but over a 5-year horizon, the stock should provide excellent returns to its shareholders and outperform the market.

You can view MONCLER's official 2022 earnings presentation here for an overview of what I will be discussing later.

Company Introduction

Moncler is a luxury clothing company, founded in 1952 and renowned worldwide. The company specializes in high-quality down jackets and other outerwear, but it is also expanding its business into clothing, footwear, and accessories for all seasons. Since 2021, it has acquired Stone Island with the intention of leveraging its expertise to grow this brand, both in terms of revenue and profit margins (they are transitioning Stone Island from B2B to B2C).

Moncler has a strong presence in Europe, Asia, and America and consistently increases its monobrand stores each year (currently, there are 251 for Moncler and 72 for Stone Island). In addition, it has a significant online presence (which they aim to expand to account for up to 25% of total revenue) with a primarily B2C business model that is much more profitable than wholesale.

{kind=link}

The company has recorded strong and consistent growth over the past 10 years, with a revenue CAGR of 18% and a net profit CAGR of 23%. Furthermore, the luxury clothing sector is growing, and it is expected to continue growing in the medium and long term.

Moncler's Outperformance

{kind=link}

The fact that Moncler has been outperforming the S&P 500 , Europe 600 Index , and Amundi S&P Global Luxury UCITS ETF for several years is no coincidence. The market recognizes and rewards a company with a globally recognized brand, continuous growth, an excellent balance sheet, extremely high profit margins, and a management team that does exactly what you would want as a shareholder. That is, they invest a significant portion of resources in the company's growth because they know they have an exceptional business to fully capitalize on, without diverting resources to buybacks (which artificially inflate EPS) or expensive dividends on which you would then pay taxes (currently, Moncler pays a dividend with a yield of less than 2%, and its historical payout ratio is around 25%, so it is entirely sustainable).

Financial And Balance Sheet Data

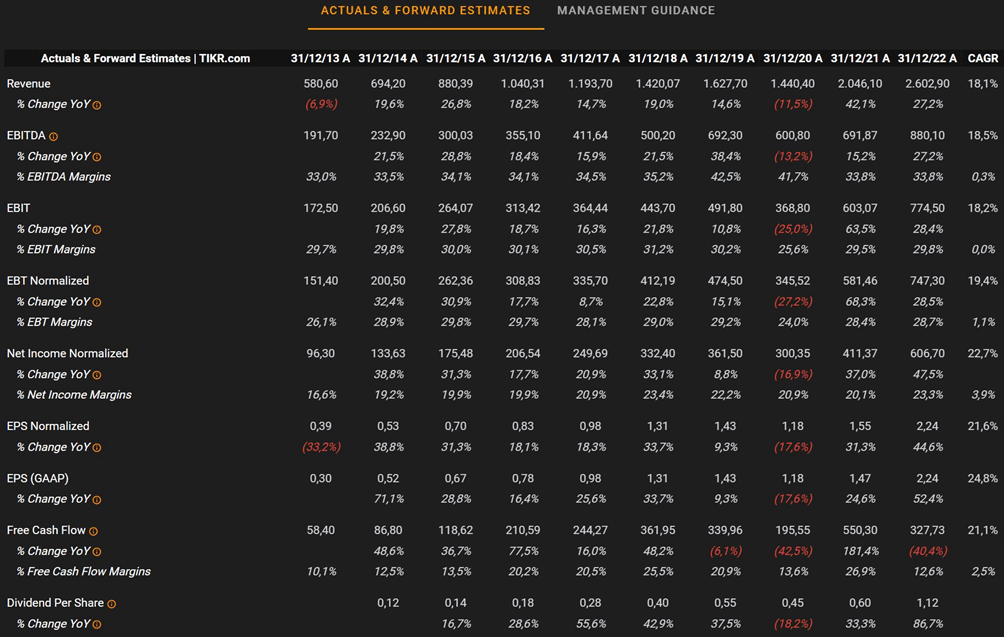

Now, let's move on to the financial and balance sheet data. There's not much to say here; it becomes really difficult to find any weaknesses, so I'll let the following image do the talking.

{kind=link}

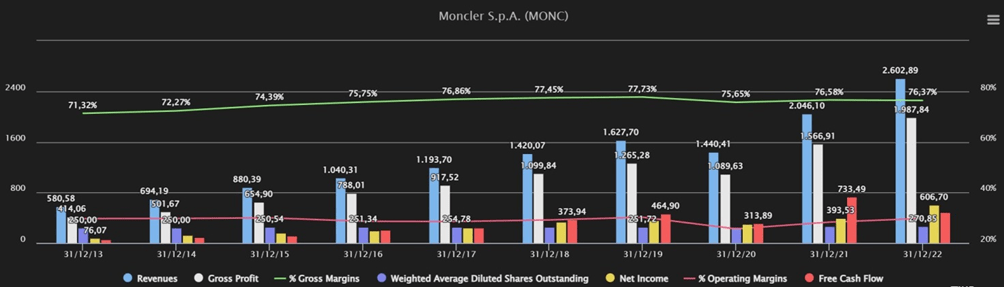

In the span of 10 years, as of December 31, 2022, the revenue has reached $2.8 billion, managing to more than quadruple from the $620 million recorded a decade earlier. The gross margin has increased from 71% to 76%, the operating margin remains stable around 30%, and the most impressive figure is the net profit, which has grown from $81 million in 2013 to $648 million in 2022. However, it's worth noting that out of the $648 million net profit in 2022, $98 million should be subtracted due to tax benefits related to the realignment of Stone Island's value, resulting in a real net profit of $550 million. This means that while revenue has more than quadrupled in 10 years, net profit has increased by more than sixfold. Taking into account the relatively stable number of shares (which is not a given for a company experiencing significant growth, especially considering the acquisition of Stone Island through a cash + stock transaction), the earnings per share ((EPS)) has also grown proportionally to the net profit. Additionally, the free cash flow is exceptionally positive as the company generates significant cash from its operations.

{kind=link}

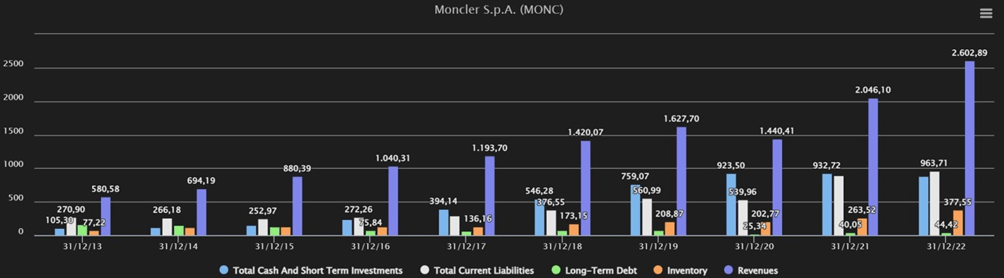

Regarding the balance sheet, Moncler has a Total cash and short-term investments that are roughly equivalent to the Total current liabilities, and long-term debt is virtually negligible. Additionally, while it may appear that the inventory is increasing, it remains within a range of 13% to 15% of revenues, consistent with historical averages. Moreover, more than 90% of the company's collections are sold out. I can attest to this based on my personal experience as a Moncler customer. I cannot help but appreciate the exceptional quality of their products and the wonderful shopping experience in one of their many stores. If you have the opportunity to visit one of their stores, I'm confident you'll share my sentiment!

Growth Projections

Moncler operates in the luxury sector, which, according to Statista , is expected to see the global luxury goods market increase from $354.8 billion in 2023 to $418.9 billion in 2028, with a CAGR of 3.4%. Despite uncertainties in the economy triggered by events like the COVID-19 pandemic, Brexit, the USA-China trade war, and the Russia-Ukraine conflict, which have led to a decline in discretionary spending, there has been a resurgence in demand. The recovery in Chinese and American demand, increased public spending, the growing influence of Millennials and Generation Z, and the consistent strength of online channels have all contributed to a strong market revival expected to continue in the medium to long term. The highest spending is expected in Asia, driven by the resurgence of China, followed by Europe, North America, Australia and Oceania, Africa, and South America.

The strength of the Moncler brand is robust in Europe and Asia and is expanding in the USA. In particular, I expect the company to continue growing in Asia, where the luxury clothing market is experiencing significant expansion. The company is also investing to expand its presence in the United States, a key market for luxury clothing, with significant collaborations with influencers like LeBron James , Jay-Z, Alicia Keys, Pharrell Williams , etc.

Furthermore, the strength of the brand enables the company to easily raise prices, as it did in 2022 by passing on production cost increases to customers. Despite this, the company has successfully increased its revenue this year while maintaining substantial profit margins.

In conclusion, Moncler, in addition to operating in a growing market, is itself a company experiencing significant growth. The favorable combination of the sector and the company allows us to estimate revenue and EPS growth with relative confidence (considering that, although it consistently outperforms analysts' estimates, Moncler's management rarely provides guidance on revenue and earnings).

{kind=link}

Valuation

Given that Moncler has consistently outperformed analyst estimates, we can assume a conservative CAGR for revenue between 10% and 15% (still lower than the 18% CAGR achieved so far) and a net profit margin between 22% and 24%. Therefore, I expect revenue to reach between $4.5 billion and $5.6 billion by the end of 2027, with a net profit ranging from $980 million to $1,320 million.

The next step is to determine a potential multiple to assign a future value to the company. Typically, I use various metrics and extract the most significant data, but with an exceptional company that generates profits, free cash flow, and practically no significant debts, the task is much simpler. For this reason, I will consider the Price to Earnings Ratio (P/E ratio).

{kind=link}

{kind=link}

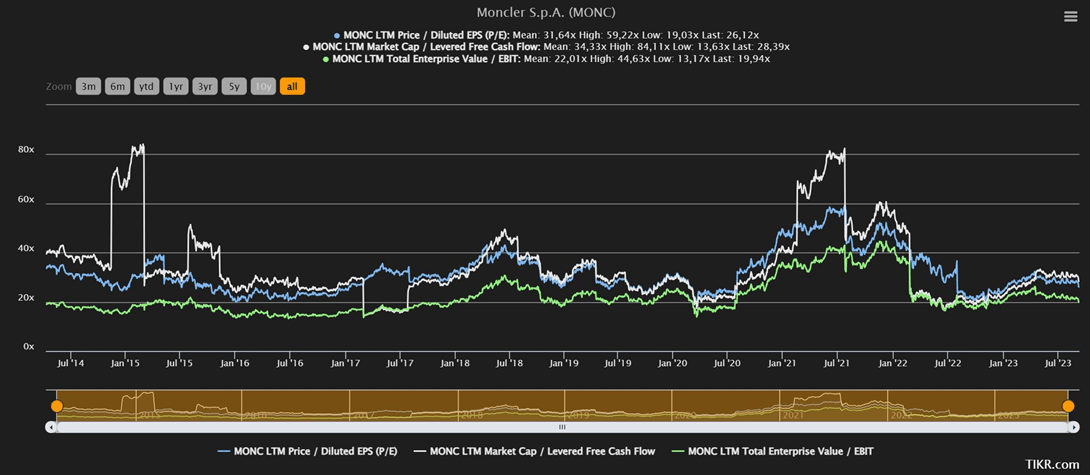

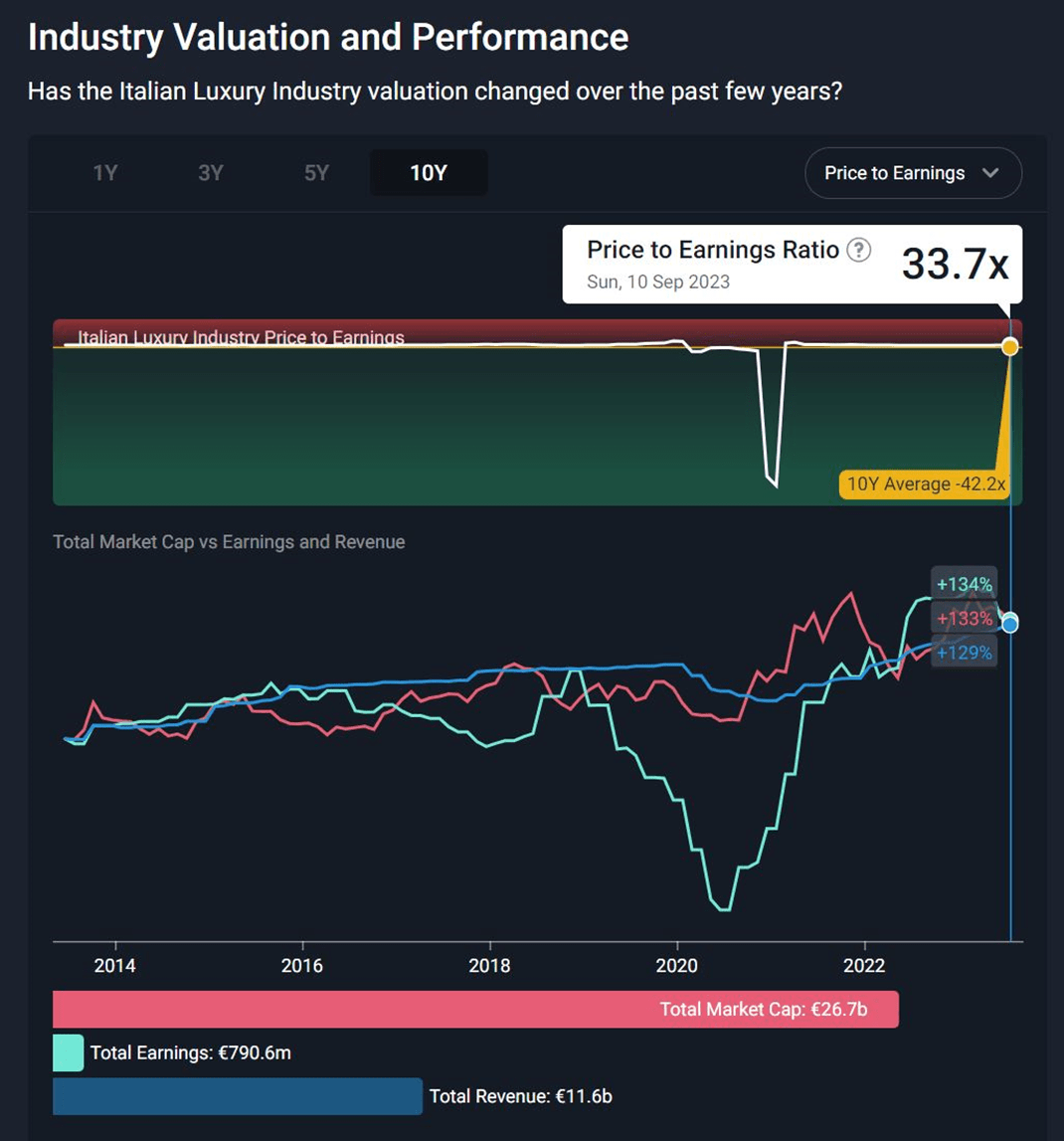

Historically, Moncler has had an average P/E ratio of 31, reaching peaks of 40 and 50 during times when Mr. Market was particularly euphoric. Very similar multiples (but slightly lower due to being considered an almost mature company) have also been seen with LVMH , which is considered the reference company in the luxury sector with a market cap of $390 billion, approximately 24 times greater than that of Moncler. On the other hand, the Italian luxury sector shows P/E multiples even slightly higher than those of Moncler.

Therefore, applying a P/E ratio of 30, slightly below its historical average, by December 31, 2027, it could reach a market capitalization ranging from $29 billion to $40 billion, with a stable number of shares at 265/270 million. This would put the stock in a range of $105-150 per share (without considering any potential buybacks).

Risks

Naturally, there are some risks that could hinder Moncler's growth. One of these risks is the possibility of a global economic slowdown, which could reduce the demand for luxury products, although in the past, only severe recessions have seen a decrease in the demand for luxury goods. Another risk is its strong exposure to the Asian market (which accounts for about 50%), especially China (33%). I consider this to be probably the most significant risk because recent data released by the Chinese government indicate that the nation is slowing down, and Moncler relies on Chinese growth to increase its business volumes. However, I believe that these risks are relatively contained as they are temporary, and Moncler has good chances of continuing to grow in the years to come thanks to the increase in retail outlets, product expansion, and the development of the Stone Island brand. Nevertheless, I would abandon my strong bullish position on the company if I had the certainty that its year-over-year growth would be below 10%.

Conclusion

Moncler is a luxury company with an extremely solid balance sheet, excellent cash flows, and strong, continuous growth with a promising future. The company holds a strong position in the global market, boasts a powerful brand, and has an experienced management team. Moncler's growth has been driven (and in my opinion will continue to be) by a series of factors, including expansion in Asia and the United States through new monobrand store openings, the development of new products, increased investments in marketing and communication, and the expansion of Stone Island's margins.

Based on my analysis, I believe that Moncler will continue to grow at a sustainable pace in the coming years. The company has a strong position in the global luxury apparel market, and its growth strategy is well-conceived.

Furthermore, I consider Moncler's management to be exceptional. The company has been growing steadily since it was acquired by Remo Ruffini in 2003. At the time, the company was in difficulty, but today it is one of the top companies in the luxury sector. The management has proven to be capable, prudent, and transparent. A fundamental aspect to consider is that the interests of management and shareholders are aligned, as CEO Remo Ruffini is also the company's largest shareholder.

At the current stock price (approximately $63.00 per share), I believe Moncler is undervalued, and I consider an excellent entry point to be around $56.00-$59.00 per share, with a target for 2027 of approximately $130.00 per share.

For further details see:

Moncler: A Solid And Continuously Growing Luxury Company