MONRY - Moncler: China's Covid U-Turn Could Be A Catalyst For Growth

Summary

- Historically, the luxury sector companies have always been solid in situations of global economic difficulty.

- A major boost to revenue could come from China’s reopening.

- The Asian segment will probably continue to be Moncler's growth engine.

- The stock seems to be slightly undervalued.

Moncler S.p.A. ( MONRF ) is an Italian luxury company specialized in clothing and accessories under the trademarks Moncler and Stone Island. The easing of the anti-Covid policy in China could boost the company's revenue growth in the coming quarters, thanks to the increase in domestic consumption and the recovery of Chinese tourism in Europe. This scenario makes the company extremely attractive also when considering the current valuation. Furthermore, Moncler has shown resilience as its brand, positioned in the luxury market, has allowed it to have good pricing power making it well positioned against inflation. In conclusion, the company is currently a buy.

Good positioning in the current macro environment

Historically the companies linked to the luxury sector have always shown solid balance sheets and above average results in situations of global economic difficulty: Moncler is no exception.

Indeed, high-end brands can usually afford to raise the prices of their products, shifting the burden of inflation or increasing production costs onto their customers. Moreover, the demand for Moncler products does not seem to be decreasing, as shown by the results of the last quarter, and there already appears to be a recovery in the Asian segment.

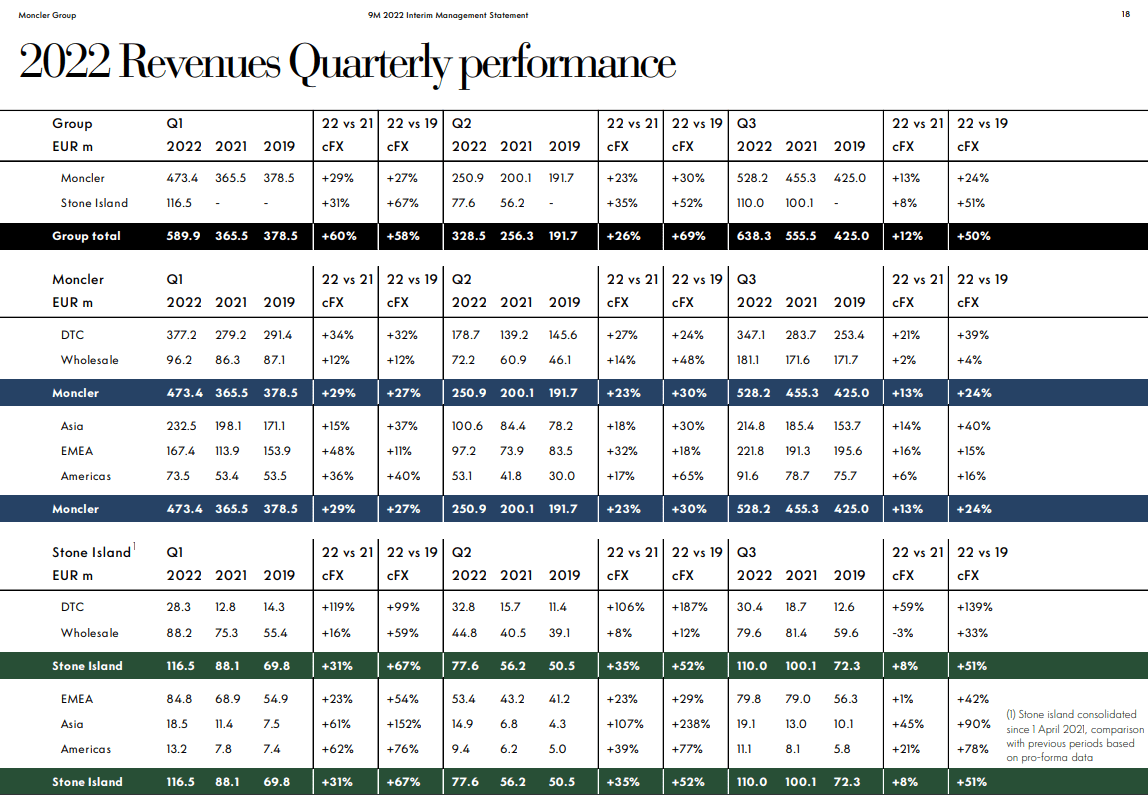

The Group’s revenue in the first nine months of 2022 reached €1,556.6 with a difference of +30% compared to the same period of 2021. Furthermore, although Europe and North America have been hit hard by inflation, the revenue of Moncler brand in the regions grew by 29% and 18% respectively. At the same time, EBIT margin improved from 14.9% in H1 FY21 to 19.6% in H1 FY22, and the Group Net Result improved from 9.4% in H1 FY21 (20.1% FY21) to 23.0% in H1 FY22.

{kind=link}

Therefore, the company has not only overcome a period of high economic uncertainty without problems, but it has also improved its results thanks to the strong performance of its brands.

The Asian Segment may surprise in the coming quarters

A major boost to revenue could come from China, which according to estimates should record an increase in consumption, fueled by the U-turn of zero-Covid policy.

The easing of the anti-Covid measures announced in recent weeks and the stop to quarantines for travelers should favor tourism and therefore the shopping of luxury goods both in China and in other countries. In fact, consumption in Europe in 2021 and 2022 has also been negatively affected by the absence of Chinese tourists, while, last summer, as soon as the Chinese measures against Covid slightly widened, purchases for personal luxury goods immediately soared in the People's Republic.

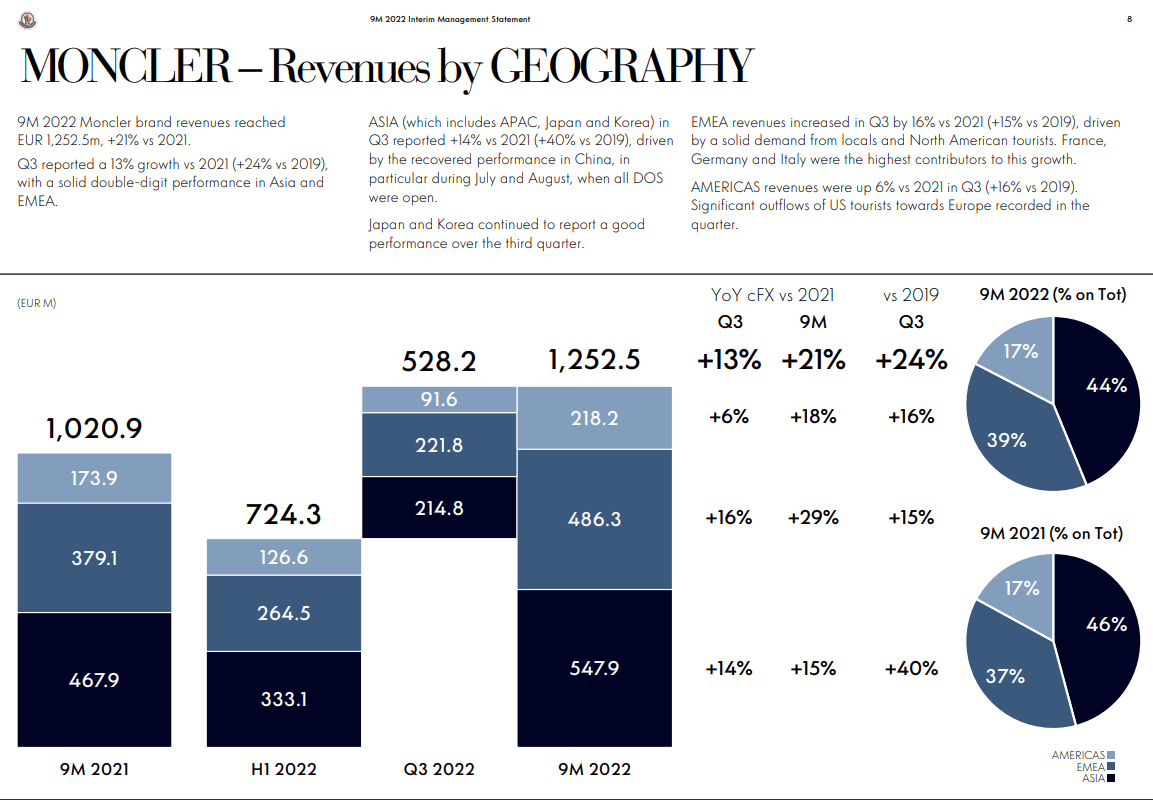

Moreover, the Asian segment (of which China accounts for the majority) represents 46% of Moncler brand's total revenue and 17% of the Stone Island brand. If we add that Asia has always been the main engine of the Group's growth (+40% compared to Q3 FY19) we can understand how a reopened China can strongly support the company's growth.

{kind=link}

{kind=link}

…but beware of risks

However, while the reopening of China may be a catalyst for the stock, close attention should be paid to the associated risks. According to the estimates, Covid cases could rise again quickly and therefore the possibility of a new change of mind of the Chinese Government cannot be excluded, putting the Asian segment at risk again.

Valuation

I evaluated Moncler using a discounted cash flow model. I estimated the future free cash flows for the next 10 years starting from the three main financial statements.

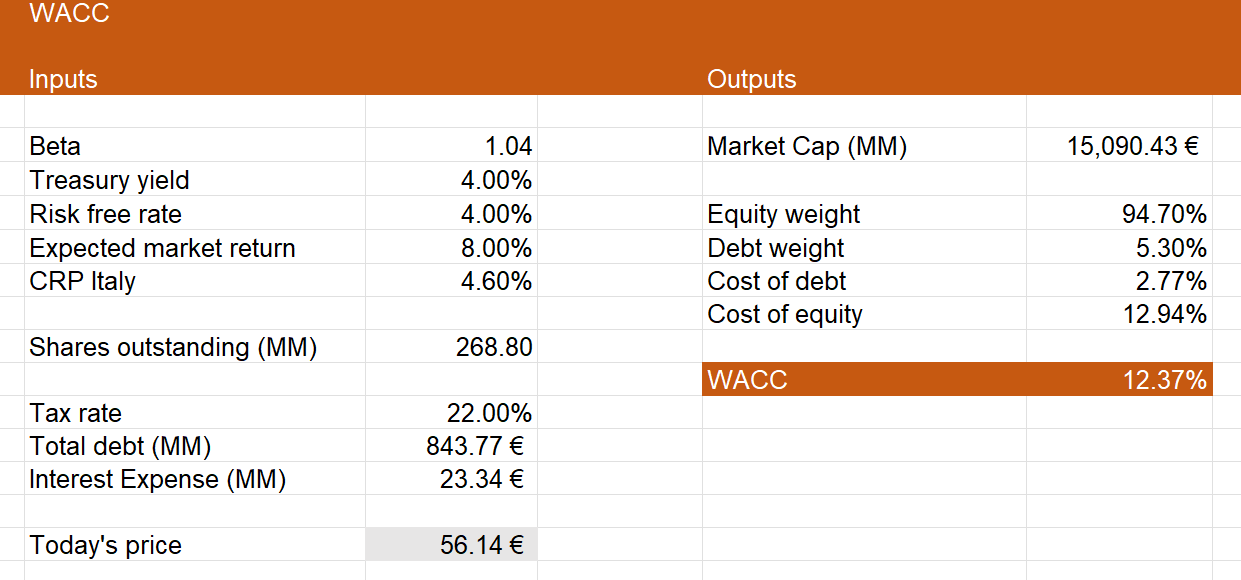

I estimated a risk-free rate of 4.00% (based on IT10Y Yield) and a country risk premium of 4.60% in order to calculate the WACC (weighted average cost of capital), which equaled 12.37%.

{kind=link}

I assumed a terminal growth rate of 3.00%, so the company’s NPV (Net Present Value) I calculated is €16.94 billion. Therefore, Moncler's NPV per share is €63.02, meaning that there is a potential upside of 12.26% from the current price (€56.14).

{kind=link}

It should be noted that all the results are in euros.

Conclusion

Moncler is a well-positioned company in the current macroeconomic context, thanks to its brand and positioning in the luxury sector. Furthermore, the probable growth of the Chinese segment following the end of the zero-Covid policy makes the stock very interesting not only from a long-term perspective, but also as a speculative play in the short-term.

For further details see:

Moncler: China's Covid U-Turn Could Be A Catalyst For Growth