MNDY - monday.com: A High Quality Company That Is Also Very Expensive

2023-04-18 08:16:12 ET

Summary

- With its platform approach and existing capabilities, monday has a competitive advantage.

- And if you compare them to their competitors, you can clearly see that they are all high quality companies, but monday has the upper hand.

- Yet their shares are priced as if they are almost certain to succeed, leaving little room for missteps or weak outlooks.

Thesis

monday.com ( MNDY ) was quite hyped on social media at the end of '21 and into '22, but due to the challenging economic situation, the share price was hit hard. But as an investor you have to look at the underlying business and that is where monday's good FY22 results came from. monday is a high-growth, high-value business and it is unfortunately also priced like one.

The shares have been massively overvalued in the past, even taking into account low interest rates and growth. And I would argue that they are not cheap now. But quality and growth often come at a price, and a fast-growing company can also grow into its valuation quite quickly.

Analysis

{kind=link}

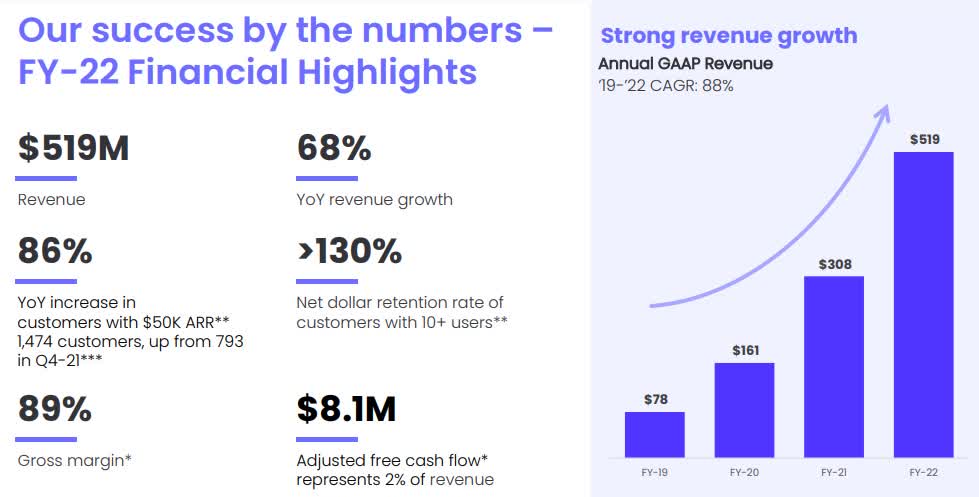

If we look at the results from 2022 instead of the share price, we see that monday has had a fabulous year. An astonishing 68% year-on-year revenue growth in a difficult economic year and an 89% gross margin. It is clearly a high quality growth business.

They are also FCF positive for the second year in a row. Even if it is really small at 8.1m for FY22, which is 2% of sales. But FCF is likely to rise in FY23 and this is still a company that is likely to grow at a high double-digit rate. There are not many companies with that kind of growth rate that are cash flow positive at such an early stage in their life.

This, combined with their strong cash position of 885.9m and almost no debt, shows that they have a really strong balance sheet and are well prepared for any eventuality.

{kind=link}

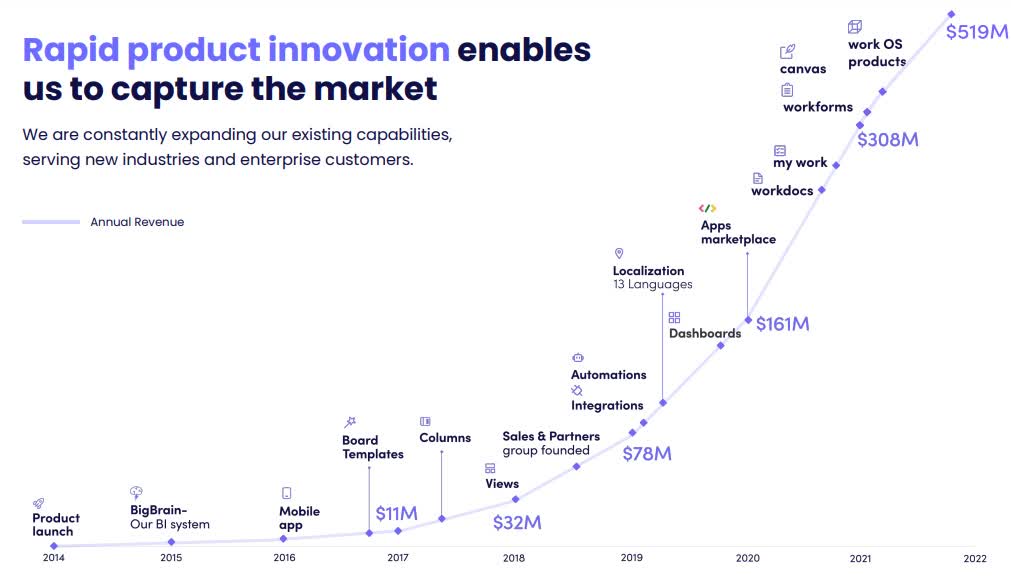

monday is all about innovation, as you can see in the picture above. They are trying to reach new industries and customers and expand their business offerings. As stated in their Q4 earnings call , the majority of new hires in 2023 will be in R&D departments. So they are clearly investing for growth.

{kind=link}

Unlike some of their competitors, they have a platform with add-ons and many customizable tools and products. This could be a competitive advantage. And one that could improve over the next few years.

Over the past year, they have gained market share as competitors have reduced their marketing spend and monday has introduced its CRM system, which it believes is simpler and more customizable than its competitors'. Almost half of the new customers came from the CRM.

FY22 Presentation monday.com

Looking at expenses as a percentage of revenues, it is clear that the cost of acquiring new customers has improved dramatically. From 148% in FY19 to 69% in FY22. So they had to spend a lot less, but they still grew 68% over the whole year. That is quite an achievement.

On another positive note, they gave guidance in their earnings call that they will be EBIT positive well before 2025. So from a business point of view, 2022 was a very good year for monday, so the only question is whether the share price is justified or whether it is overvalued. Because as a business they are clearly a strong business.

Competition

In this part, I want to compare them with some of their competitors, so I chose Asana ( ASAN ), Smartsheet ( SMAR ) and Atlassian ( TEAM ), which owns Trello.

{kind=link}

In terms of price-to-sales ratio, they all look quite expensive, but Asana and Smartsheet are slightly cheaper. In my opinion, this is mainly due to the quality of the company, as Atlassian and monday are better, and some other facts we will discuss below.

But a double-digit P/S ratio for monday is very expensive and does not leave much room for error as it would be punished quite severely.

{kind=link}

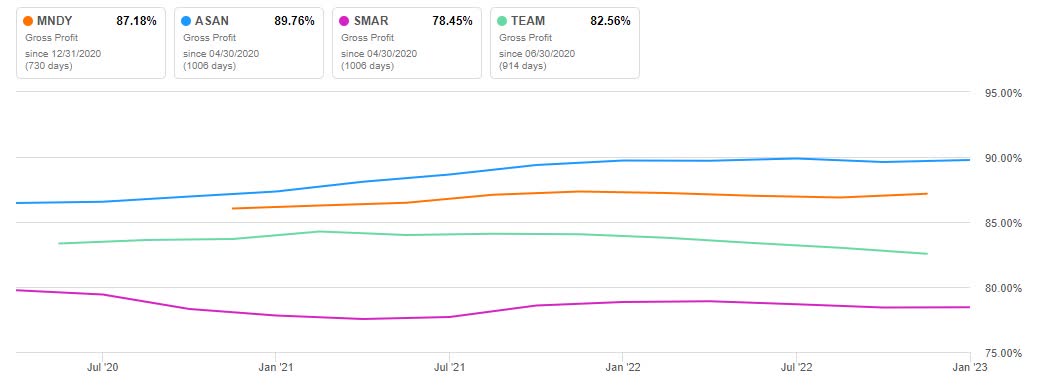

Here we see that monday and Asana both have very strong gross margins in the high 80s and low 90s, whereas the other two are in the low 80s and high 70s. That is a big difference.

{kind=link}

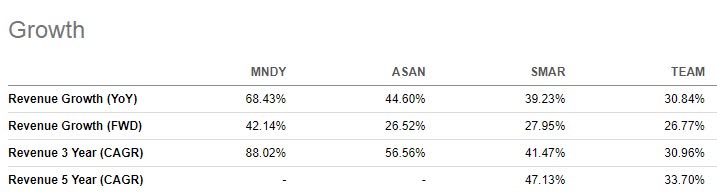

The biggest difference is when we look at revenue growth rates, where monday clearly dominates by a wide spread. To grow faster and with such an astonishing gross profit margin is something special.

{kind=link}

In addition, all 4 companies have strong balance sheets with high cash positions and negative net debt, which is good. But again, monday is a bit better than the competition.

And if we take the G2 ratings, we also see that there is an advantage for monday as their ratings are the best of the peer group.

- monday : 4,7 out of 5

- Trello : 4,4 out of 5

- Smartsheet : 4,4 out of 5

- Asana : 4,3 out of 5

According to G2, the main advantages are that monday offers more through its platform and that its products are easier to use. And a better user experience is, in my opinion, a clear competitive advantage that is hard to beat. It will also be difficult for competitors to replicate the success of the platform and, as monday showed with the new CRM product, they have the skills to win customers in new competitive markets.

I also believe that the management team is of exceptional quality, as evidenced by the reviews . The great culture and amazing leadership are things that are often praised, and a great product plus a great management team has the potential for a great outcome.

Risks

One of the big questions that remains is how important workflow management companies will be, and whether customers will rely on them or abandon them. At the moment, it looks like they could be important, and monday's Platform System, which will offer AI tools in the future, could be an important factor. But they are also investing heavily in R&D, which is a positive sign for the future.

New competitors may enter the market once they see how profitable it is, but I think monday's platform with all the little add-ons and extensions should act as a kind of barrier to entry because it is not that easy to replicate. They also have long-standing customer relationships and are an easy-to-use product, so the competition would have to be a much better product to get customers to switch.

Conclusion

monday is a quality company, there is no doubt about that, but the share price is also very expensive. For a long-term holding, I would prefer an entry price of around $100 or even a little lower. This would help to reduce the risk, as any mistake would be punished at today's valuation.

And so, as long as the business remains as strong as it is, it would be a good idea for existing shareholders to add on dips to the $100. The competitive advantage of the underlying business should act as a bit of a safety net, as the company could grow into its valuation quite quickly.

monday has a good chance of dominating the market or getting a really big chunk of market share. In particular, the very good gross margins could reward shareholders when the company is more mature and can focus on making the best profits. Then they would be able to return a massive amount of cash to shareholders.

But until then, it is a big step. And a lot can happen in the future. Most of the time, the risks that nobody thinks about are the ones that have the biggest impact.

For further details see:

monday.com: A High Quality Company That Is Also Very Expensive