MNDY - monday.com: Guidance Will Be Revised Upward

2023-03-21 14:40:50 ET

Summary

- monday.com has been a very choppy stock of late. But share price choppiness aside, the business has solid momentum to its back.

- I lay out the case of why I believe that monday.com could revise its full-year revenue target upwards, to the delight of investors.

- I believe that it's possible that monday.com will end 2023 very close to non-GAAP breakeven.

Investment Thesis

monday.com ( MNDY ) appears to have found steady footing of late, with its share price up substantially from the November lows.

Here, I lay out some bearish aspects that investors should be mindful of. Nevertheless, I explain why I'm ultimately bullish on monday.com as I believe that monday.com could positively surprise investors on the back of its Q1 2023 results.

What's Next for monday.com?

As you know, it has been a very challenging period for small-cap companies. Investors have actively shunned anything that has been seen as ''untested''. Meaning that for businesses that have a compelling narrative but enter the current macro environment without proof of underlying profitability, investors have mostly wanted nothing to do with this space over the last couple of years.

Furthermore, in the past, there was the bearish thesis that monday.com was less well suited for an economic slowdown than some of its peers.

For instance, one of monday.com's competitors, Atlassian ( TEAM ), has been non-GAAP profitable for a few years. As a point of fact, Atlassian is fully self-sustainable. And yet, as we inch towards a potential recession, the stock performance of these two companies in the past 6 months tells a very different story.

We can see above how monday.com has substantially outperformed Atlassian.

Meanwhile, another consideration that has often plagued monday.com has been that its business model is better suited towards SMB customers, rather than large organizations. Why? Because large organizations are more likely to internally develop their own software capabilities rather than to subscribe to monday.com's Work OS.

Consequently, this leaves monday.com targeting SMB clients.

Indeed, if I were to hone in on one key bearish feature of monday.com's business model, it would be how to ensure there's more customer retention. Particularly as the economy contracts, as I'm sure you know, SMBs are the first cohort to cut back on any and all expenses that are not absolutely critical to survival.

Furthermore, for monday.com to outreach to larger enterprises it would require more sales efforts which means greater costs, so monday.com's current business model could perhaps be stuck with servicing SMBs, at least for now.

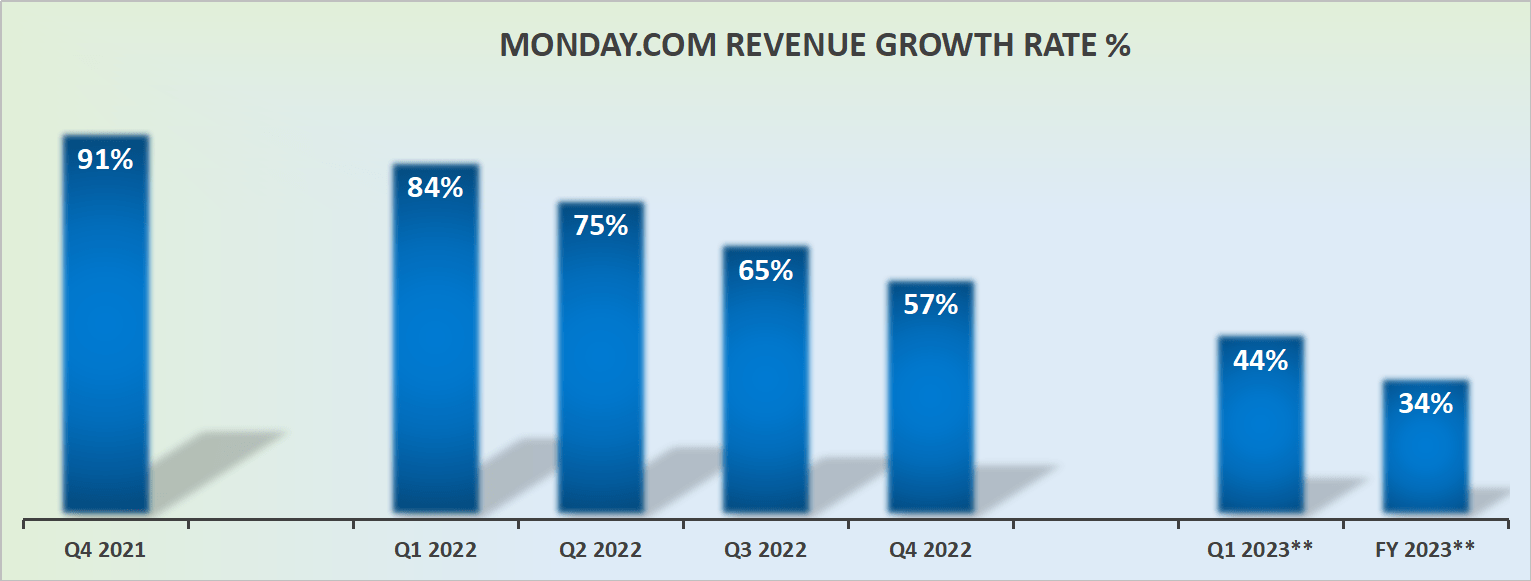

Revenue Growth Rates Have Room to Impress

{kind=link}

The graphic above reminds us that not too long ago, back in Q4 2021, monday.com's revenue growth rates were sizzling hot. In fact, as the business exited Q4 2021, monday.com was growing at more than 90% y/y, and few investors would have believed at that time that twelve months later, the exit rates from Q4 2022 would be 57% y/y, approximately 3,400 basis point deceleration in twelve months.

However, that rapid deceleration can be an opportunity too. Namely, we know that Q1 2023 is more than likely to report 44% y/y revenue growth rates, or even perhaps slightly higher.

But, at the same time, we must realize that Q1 2023 is up against the most challenging comparables with the prior year. Meaning that the remainder of 2023 will be much easier for monday.com.

With that in mind, I simply struggle to believe that monday.com's subsequent quarters will so dramatically decelerate as the year progresses, particularly after monday.com gets over its most challenging comparable quarter.

SA Premium

To put it more concretely, I believe that there's a more than likely chance that monday.com will upwards revise its full-year revenue outlook together with its Q1 results.

After all, this is a company that has a history of positively surprising investors with its revenue growth rates.

SA Premium

As you can see above, since its IPO, monday.com has consistently lowballed its guidance and then positively beat on its revenue line.

In sum, I believe that monday.com will probably end up growing this year by close to 40% CAGR.

The question, though, is can this business model grow profitably.

Bearish Consideration, monday.com is Unprofitable

Consider monday.com's 2023 non-GAAP operating outlook.

MNDY Q4 shareholder letter

The business is guided towards negative 5% operating margins. On the surface, investors will think that's great, after all, 2022 saw negative 9% non-GAAP operating margins.

However, when we consider that Q4 2022 reported positive 10% non-GAAP operating margins, investors would be excused for showing their disenchantment with monday.com. After all, by this stage, haven't all these unprofitable companies got the memo?

High gross margins businesses aren't being rewarded. What investors want is a profitable business, preferably GAAP profitable.

MNDY Stock Valuation - Less than 9x Forward Sales

As we look ahead, assuming that monday.com's full revenues reach around $720 million in 2023, this leaves the stock today priced at approximately 8.7x forward sales.

Clearly, that's the low end of its multiple range. It would be difficult to state that today investors are highly bullish on monday.com.

I believe that a fairer assertion could be that monday.com is fairly valued if the business continues to tick along in the current path.

But if you buy into my argument that monday.com has the potential to positively impress by upwards revising its full-year revenues, then it's likely that monday.com could even finish 2023 with breakeven non-GAAP profitability.

The Bottom Line

monday.com is likely to upwards revise its full-year outlook and, therefore, positively surprise investors. My contention here is that there are some blemishes in the investment thesis.

But if monday.com can continue to deliver upon its guidance and get investors to buy into the prospect that the business will end 2023 at non-GAAP breakeven or better, then this stock could easily move higher, rapidly.

For further details see:

monday.com: Guidance Will Be Revised Upward