HUBS - monday.com: Interminable Strength In A Challenging Time

2023-11-15 17:47:27 ET

Summary

- In the midst of war and a downcycle for software, some may have concluded that monday.com Ltd. would experience disruption in its pace of execution and evolution.

- However, as I will demonstrate today, monday.com has not skipped a beat: it now operates from its greatest position of strength as a company in its corporate history.

- This strength is not ethereal; rather, it's concrete. monday.com's strength derives from definitive strategy and crisp execution thereof, which I will briefly discuss with you today.

- In addition to a consideration of monday.com Ltd.'s strategy via which it's maintained elevated sales growth through a challenging time, I will review the company's most recent quarterly report and provide an update to you regarding the impact of the war on monday.com.

- In short, with $1.05B in cash, $0 in debt, 34% free cash flow margins, and virtually perfect execution of its multi-product, vertical integration strategy, I continue to like monday.com Ltd. shares at these levels.

A Battlefield Of A Different Kind

The world of business is often likened to a battlefield, though, following my decade of military service, I've tried to abandoned this likening. Success in business often determines the standard of living for an individual and their family in the same way war determines the fate of regions, and, in the past, earth; however, it's my opinion that nothing can mirror the atrocities and horrors of war.

To this end, I'd like to start this review of monday.com Ltd. (MNDY) aka "Monday" by expressing my sincere concern for those in Israel during this time. I actually have one community member who recently took a job at Monday as an executive developing its product suite, and we have a handful of members who live in Israel. I sincerely hope that peace is restored to the region in short order, and I send my love and strength.

All of this being said, investors have questioned what impact the war would have on Monday. While Monday is very much a global business, with employees and offices distributed all around the world, including New York, Japan, and Australia, to name just a few of its many locations, it is very much an Israeli-company, with its central headquarters located in Tel-Aviv.

Monday's Many Office Locations

{kind=link}

In light of it being very much Israeli-centric, on Monday's Q3 2023 earnings call , analysts' inquired as to how the war has impacted the business.

In short, Monday has had 7% of its workforce brought out of its reserves for active duty in defense of the country during this period. While obviously a relatively small number, it actually surprised me that this many individuals were being brought out of Israel's reserve force to defend the country during this period.

Below, I quoted co-CEO Roy Mann, who detailed for us the impacts of the war on Monday's operations (emphasis added):

As we reflect on our most recent quarter, it is with heavy hearts that we acknowledge the recent tragic events that have unfolded in Israel. Our thoughts are with all those affected by recent violent terrorist attacks.

At this time, the impact on the current situation of our global operation is minimal, and we remain confident in our ability to meet all our business and financial targets. In terms of revenue, Israel accounts for a low single-digit percentage of our total ARR.

While only approximately 7% of our global workforce have been called up for reserve duty, our global employees have gone above and beyond to seamlessly feel any gaps to help ensure our business continues to run smoothly.

Furthermore, all of our data servers are distributed globally across North America, Europe and Australia, ensuring our operations will continue seamlessly. We are monitoring the situation closely and will make necessary estimate to our plans as needed.

Roy Mann, co-CEO, Q3 2023 Monday Earnings Call.

While some may believe that this should be seen negatively, I am, as always, of the opinion that setbacks and adversity should be seen through a positive lens.

Instead of weakening the Monday organization, I believe this will galvanize its 93% civilian employees to work harder than ever, ensuring that they do their part in supporting their colleagues who are now risking their lives in defense of Israel.

Instead of disrupting Monday's operations, I believe this period will serve to make Monday more durable, more agile, and more resilient.

I will not belabor my thinking in this respect; however, I did find one other exchange on Monday's earnings call to be insightful as to how the company has managed itself during this tumultuous period.

Steve Enders: I'm glad to hear everyone is safe over at Monday. I guess maybe just would like to kind of start on that part. I think you called out 7% of employees have been called up to reserves at this point. I guess, how do you go about managing the organization when you have that level of disruption. And I guess, secondarily, like as you think about hiring, it seems like discontinued expectations for that going into next year. How do you think about what that means for future hiring plans and backfilling some of those called up individuals there?

Roy Mann: So the impact we have right now on the plans we have is minimal. The is impact but it's something we're dealing with, and it has a very short-term effect. Regarding hiring, we're have a very strong hiring plan for next year and also this year. So we're on track, and that's been going well.

Eran Zinman: I can add that Israel only accounts for a low single-digit percentage of our ARR, and there's very little impact over there, although we see a little bit, but very small impact, and it's a small part of our revenue. And also in terms of data servers, it's all distributed globally. We don't have currently any data centers in Israel across North America, Europe, Australia. So in terms of data integrity, servers, operations, we see no impact. And as we mentioned on the business side, it's minimal impact mostly to Israeli customers.

Q3 2023 Monday Earnings Call.

To close this brief introduction, Monday announced a new regional sales structure in its Q3 2023 shareholder letter . I don't believe this had anything to do with the war, but it is worth noting that Monday is a globally-oriented company that will likely become more decentralized, and thereby even more durable, over time:

Monday Q3 2023 Shareholder Letter

We announced last quarter that we promoted both Jamison to be a regional manager for North America and Dean for APAC region. And definitely, it's part of the movement that we're receiving a stronger presence in both of those regions, but also scaling those regions dramatically. As we said, we're also doing a lot of outbound sales reaching larger customers, Fortune 500 customers, in addition to our performance marketing. So for us, it's continued that momentum as a company. And it just gives us over time more access to larger and larger enterprises, and we continue to scale that effort.

Eran Zinman, CEO, Q3 2023 Monday Earnings Call.

With these ideas in mind, let's turn to a review of Monday's report via a series of charts, then I will conclude with a valuation exercise and some thoughts on why we own the business generally.

Monday In Charts

Over the last few years now, I've studied the IPO class of 2020 and 2021, and Monday unequivocally has been one of the best performers from that period, if not the best (quite controversially, I believe Affirm Holdings (AFRM) has been the best performer from a business execution perspective).

I do not say this through the lens of Monday's share price performance, which has been fine all things considered (with those things being the fairly noteworthy slowdown for the software industry as a whole), but rather I say this through purely the lens of business execution.

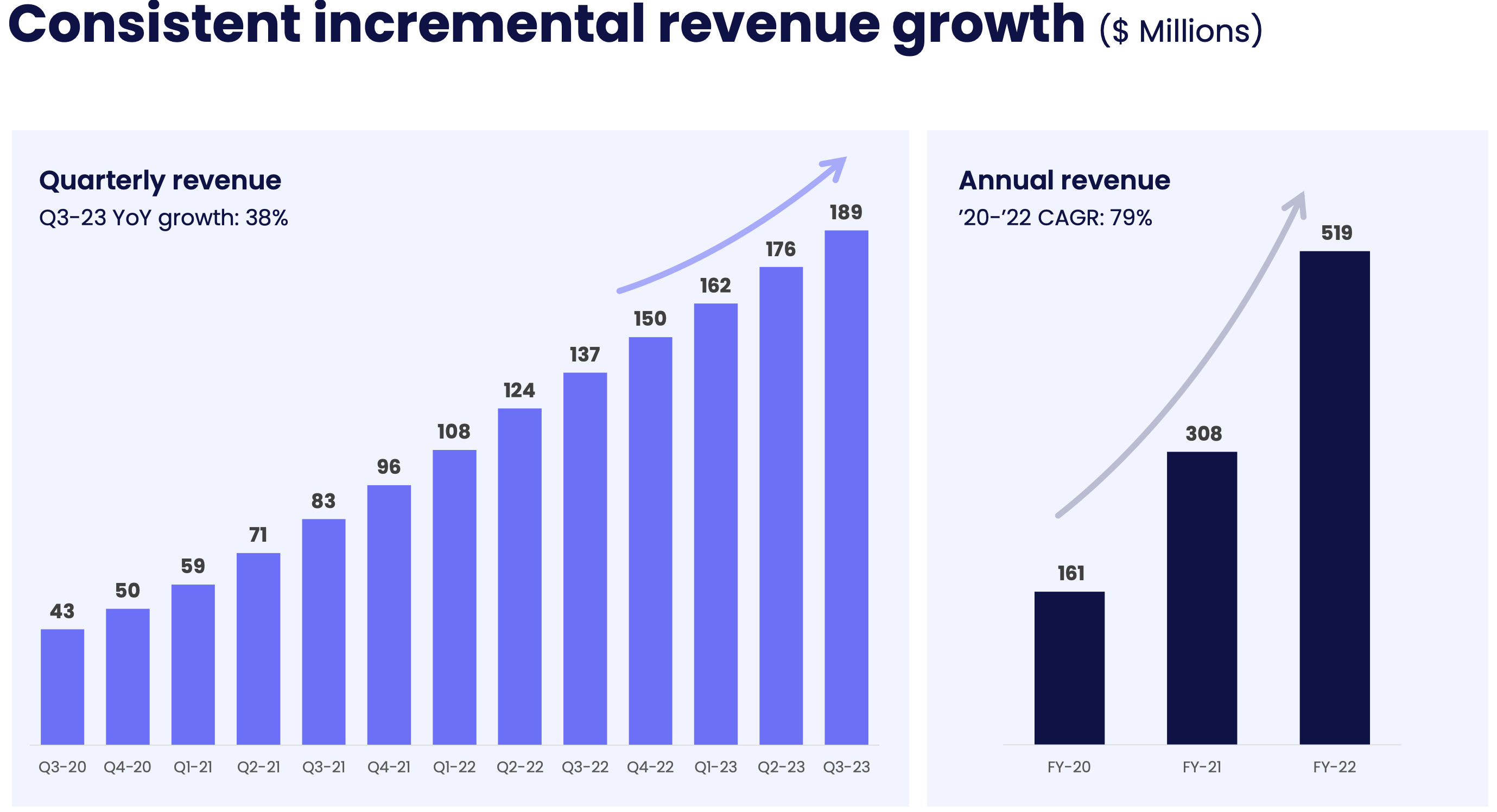

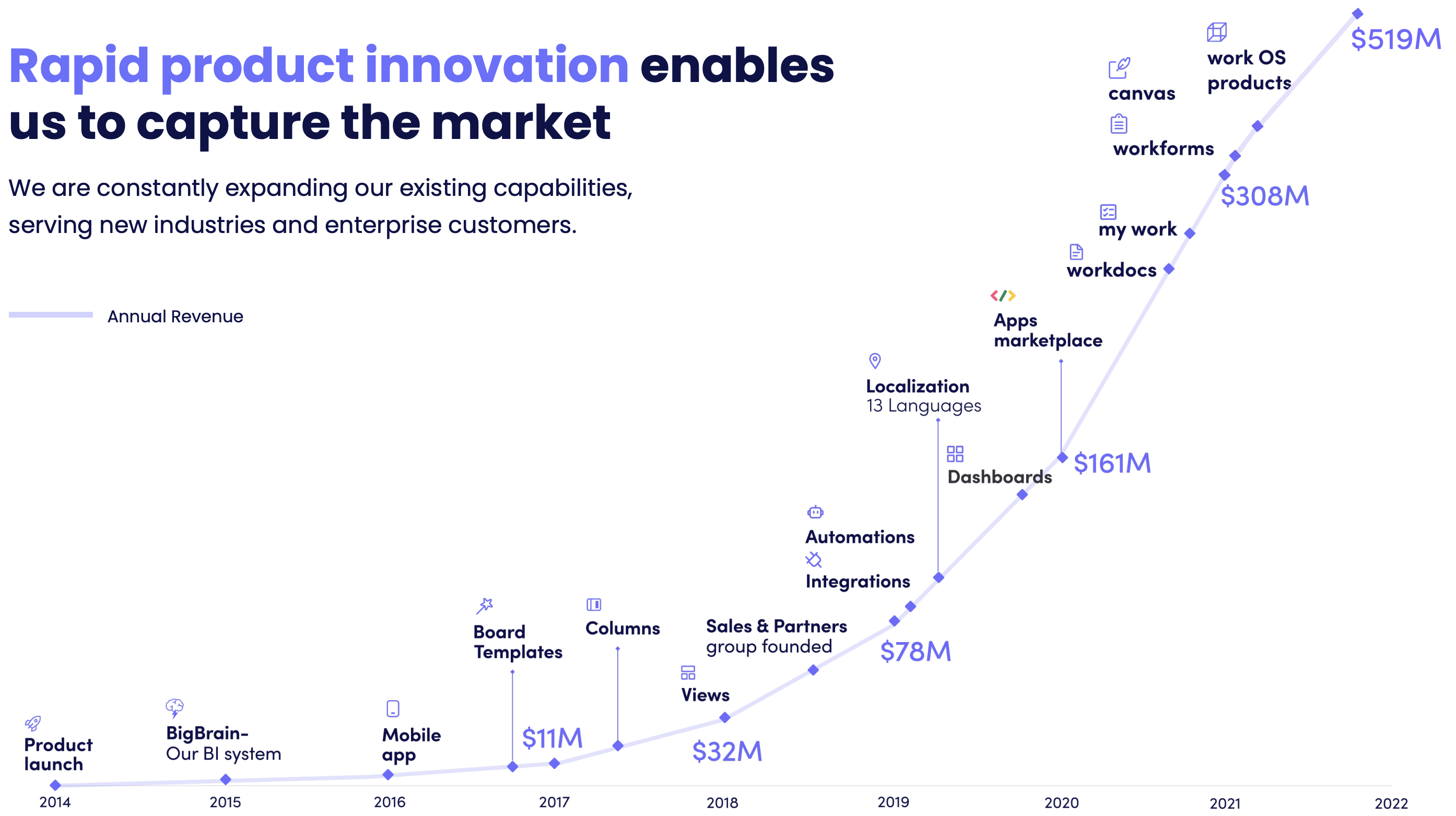

Specifically, Monday has executed its multi-product strategy to virtual perfection, which has resulted in the steady sales growth depicted just below.

Q3 2023 Monday Investor Presentation

{kind=link}

Monday has added revenue in each sequential quarter in a mechanical fashion, producing and sustaining exceptional sales growth as a result.

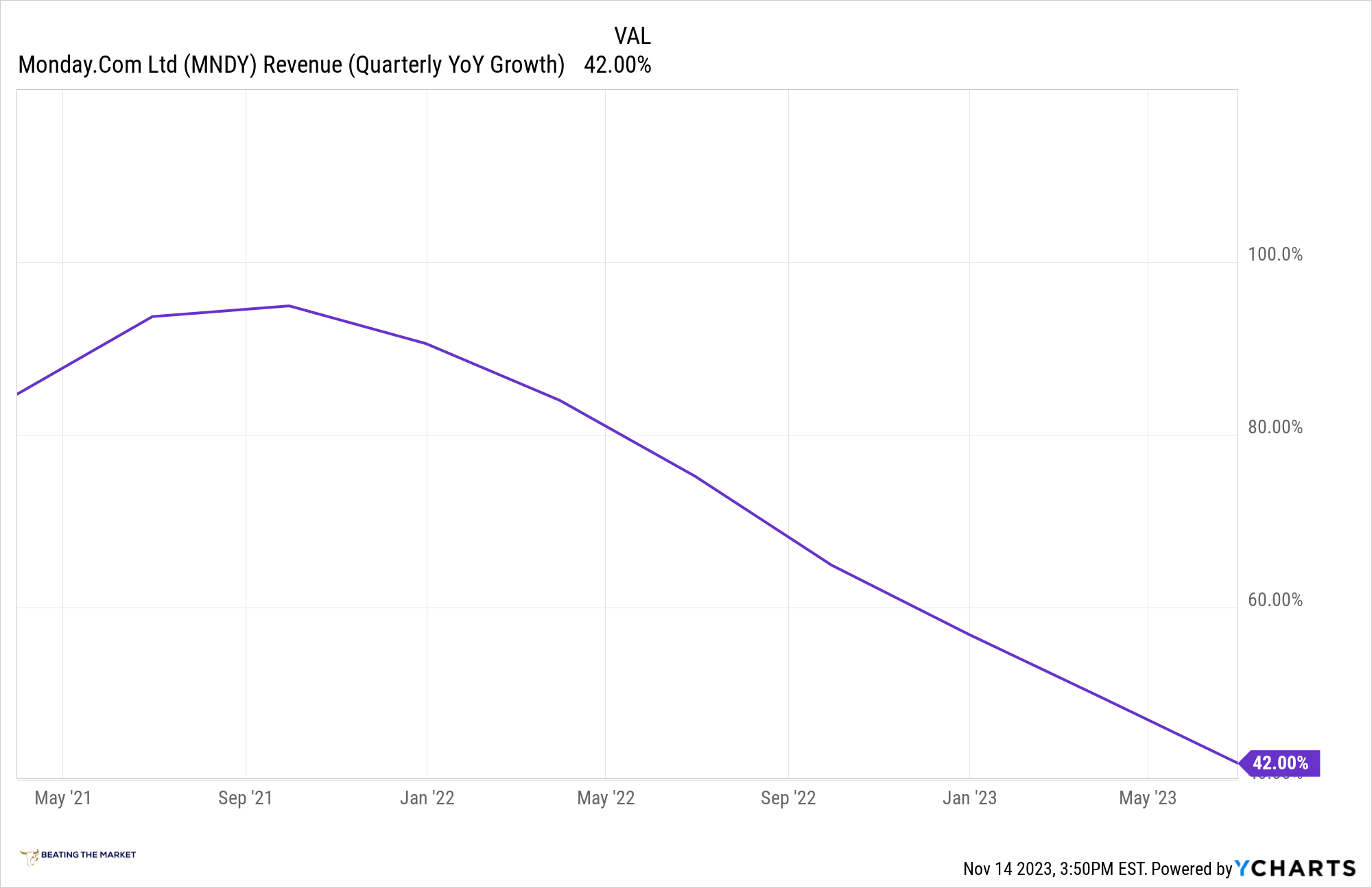

Monday Sustains 35%+ Growth Despite A Dramatic Slowdown For The Broad Software Industry

{kind=link}

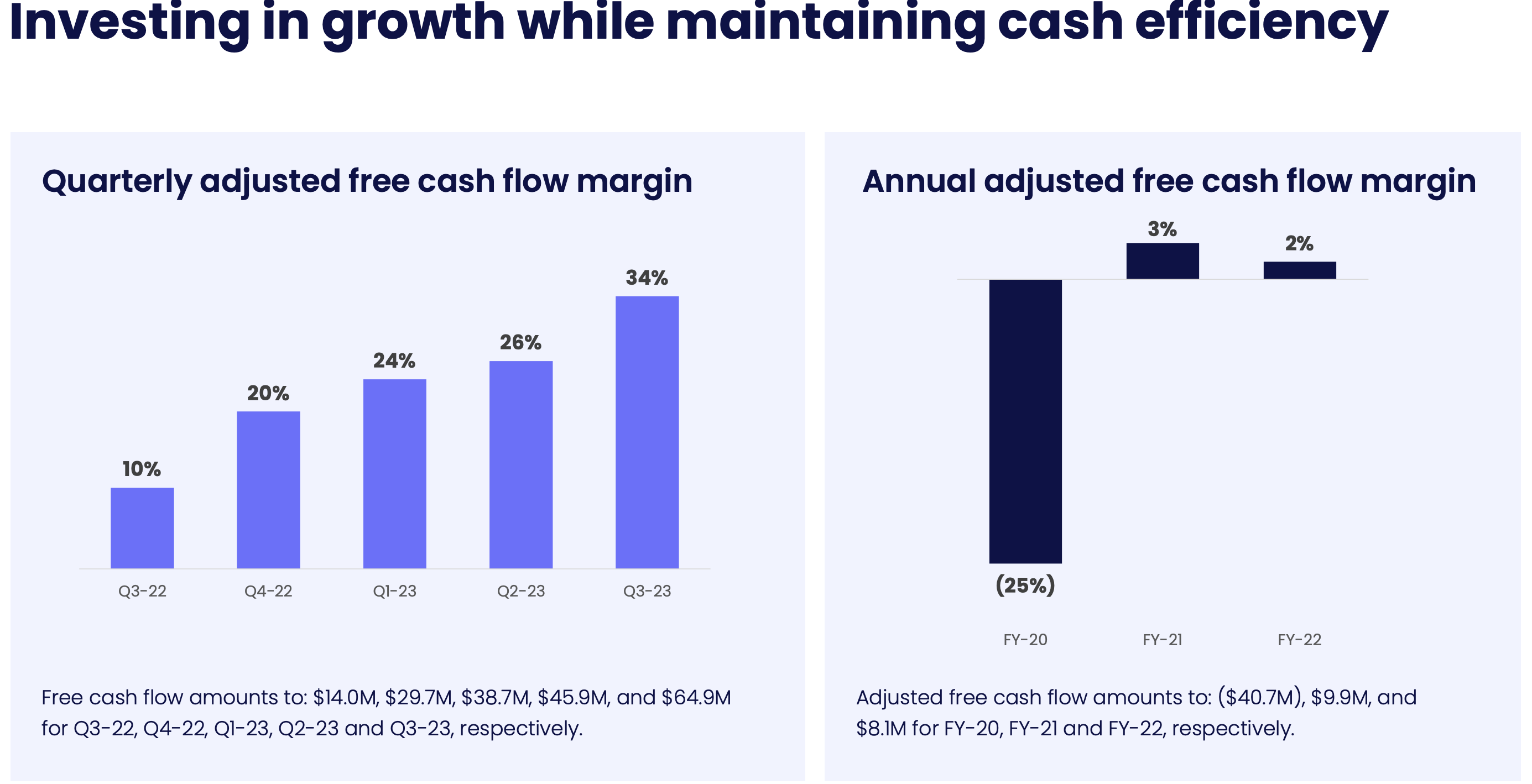

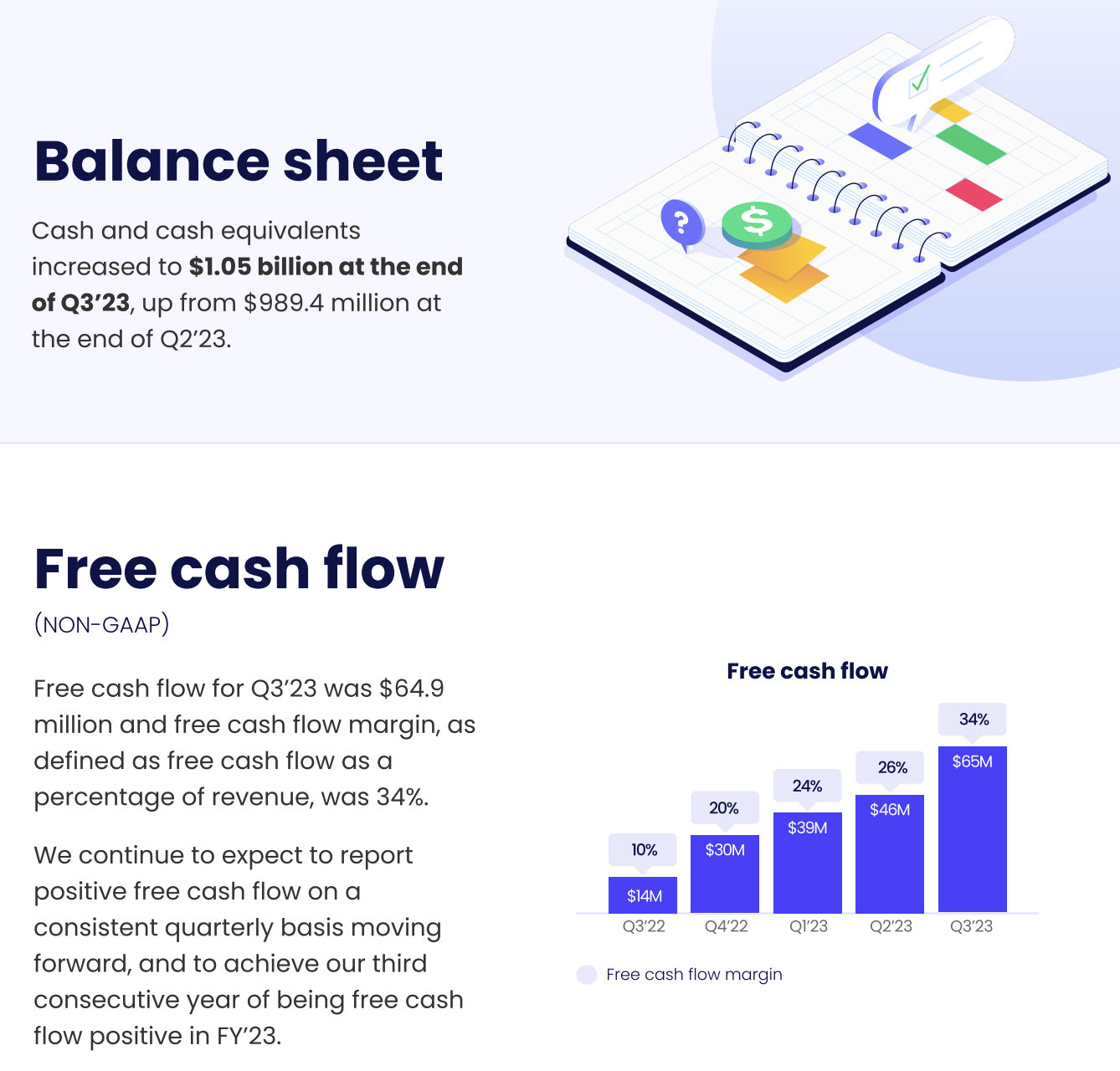

And it has maintained this growth while expanding its free cash flow margin, the expansion of which we can see below:

Q3 2023 Monday Investor Presentation

{kind=link}

It should be noted, however, that a large portion of this free cash flow has been generated by Monday's interest income that it generates from having invested its $1.05B cash hoard (it has no debt).

Monday's Free Cash Flow Margin Has Grown In Tandem With The Yield It's Generated On Its $1.05B Cash Hoard

{kind=link}

So while it's quite incredible that Monday has sustained such elevated growth, especially in light of its target market being SMBs, who usually get "blown out" first during economic turmoil, Monday has also had a great deal of help from this massive cash hoard and the yield it's generated therefrom.

- SMB = small to medium-sized business.

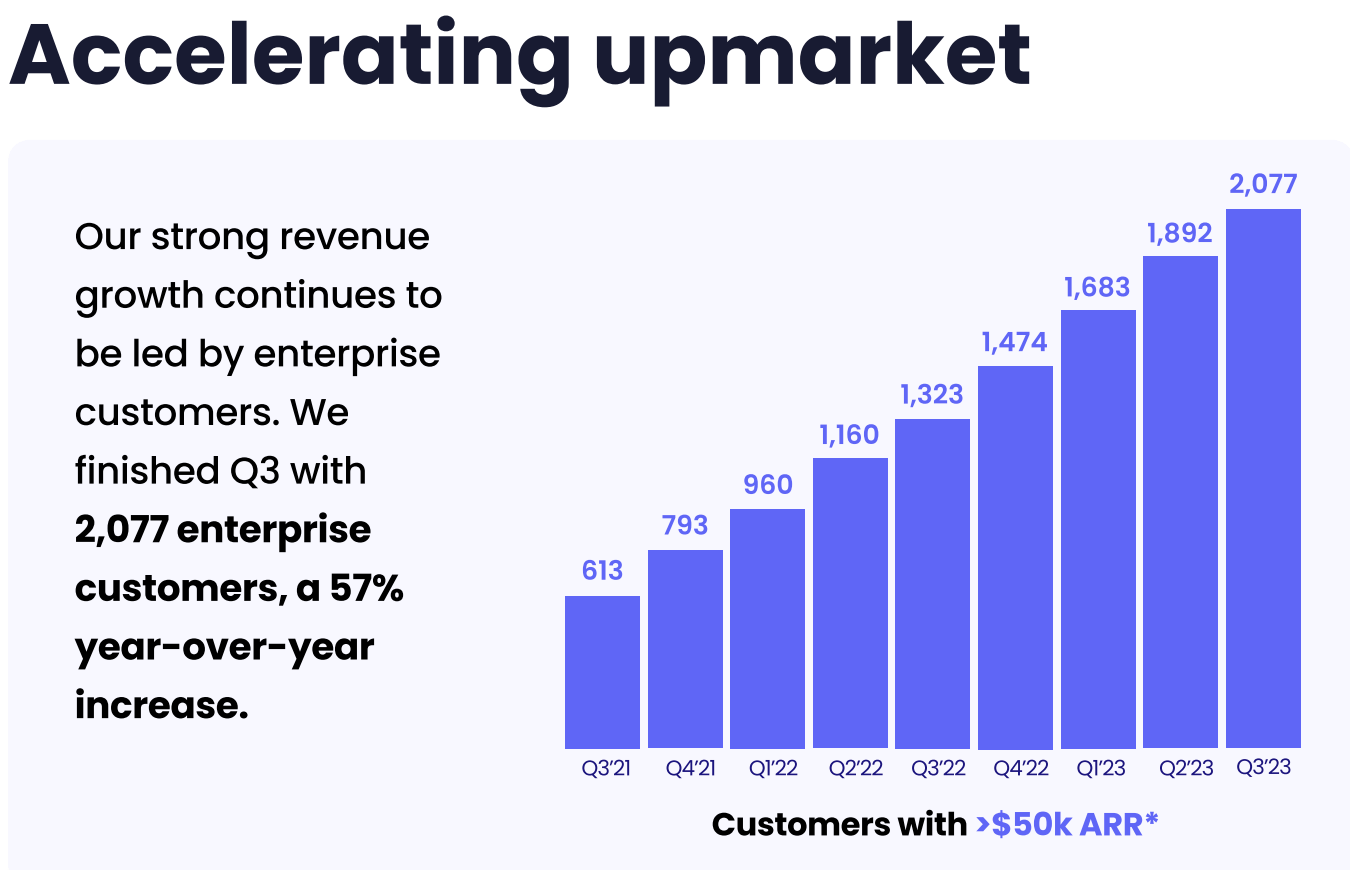

Speaking of Monday's target customers, it's done a phenomenal job of expanding upmarket, i.e., winning customers with accounts over $50k who are vastly more durable and profitable over the long run.

Monday Continues Its Torrid Pace Of Winning Enterprise Customers

Q3 2023 Monday Shareholder Letter

{kind=link}

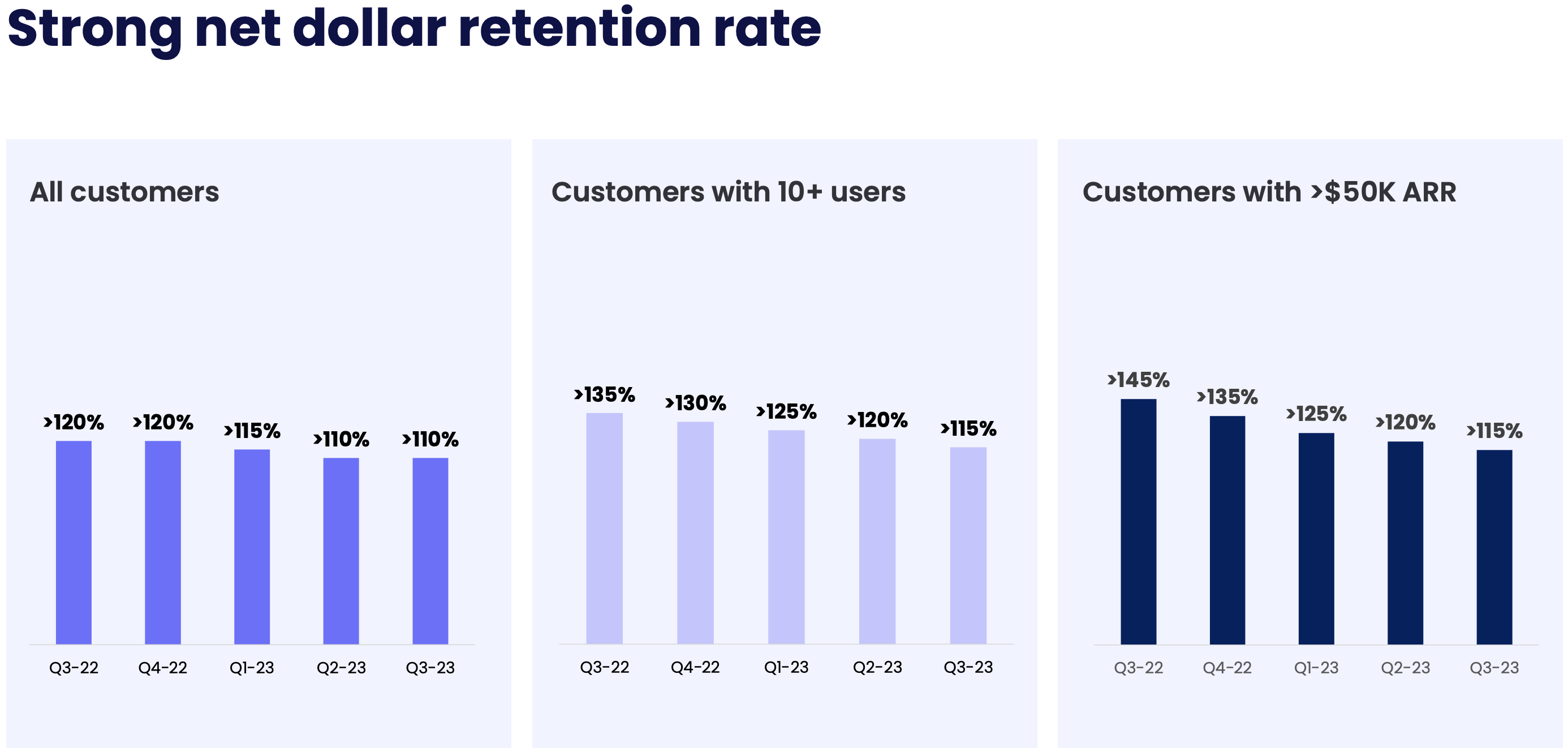

To illustrate the contention that enterprise customers are more valuable to Monday than SMBs, below, we can see that Monday's larger customers have continued to spend more money with Monday, year over year, than their much smaller peers.

Monday's Net Retention Rate

Q3 2023 Monday Shareholder Letter

{kind=link}

As we can see, on the righthand side of the chart, Monday's larger customers have, on average, spent 15%+ more money with Monday year over year.

Including Monday's smaller customers, that number falls to just 10%. I will say, though, that that 110% net retention rate is pretty incredible, all things considered.

When HubSpot ( HUBS ) was the same age as Monday, its NRR was roughly at or below 100%, so this is really incredible performance for Monday.

Lastly, let's quickly review Monday's mountainous cash hoard found on its balance sheet :

Q3 2023 Monday Shareholder Letter

{kind=link}

As I've often noted, our companies have genuinely massive cash hoards alongside little to no debt, and Monday is a gleaming example of this assertion.

As we know, Monday presently uses this cash hoard to generate yield that has served to subsidize its operations to some degree, but there's a lot Monday could do with this giant cash hoard, especially as inflation abates. In this vein, I found the following exchange insightful (emphasis added):

Jason Celino: Great. And then, Eliran, you mentioned having a lot of cash, crossing the $1 billion mark, and you're generating more. Maybe can you speak to some of your capital deployment strategy?

Eliran Glazer: Yes. So with regards to cash, obviously, it's going to be used for corporate initiative. We're going to continue to invest in investing in the business, bringing and hiring people, expanding the leadership team, the management team as well as thinking about nonorganic growth opportunities, we are going to look potentially next year at companies thinking about M&A. Again, mostly tuck-in, equity hiring, complementary products, but this is something that we definitely started to think about and to deploy it potentially in the next 12 to 18 months.

Q3 2023 Monday Earnings Call.

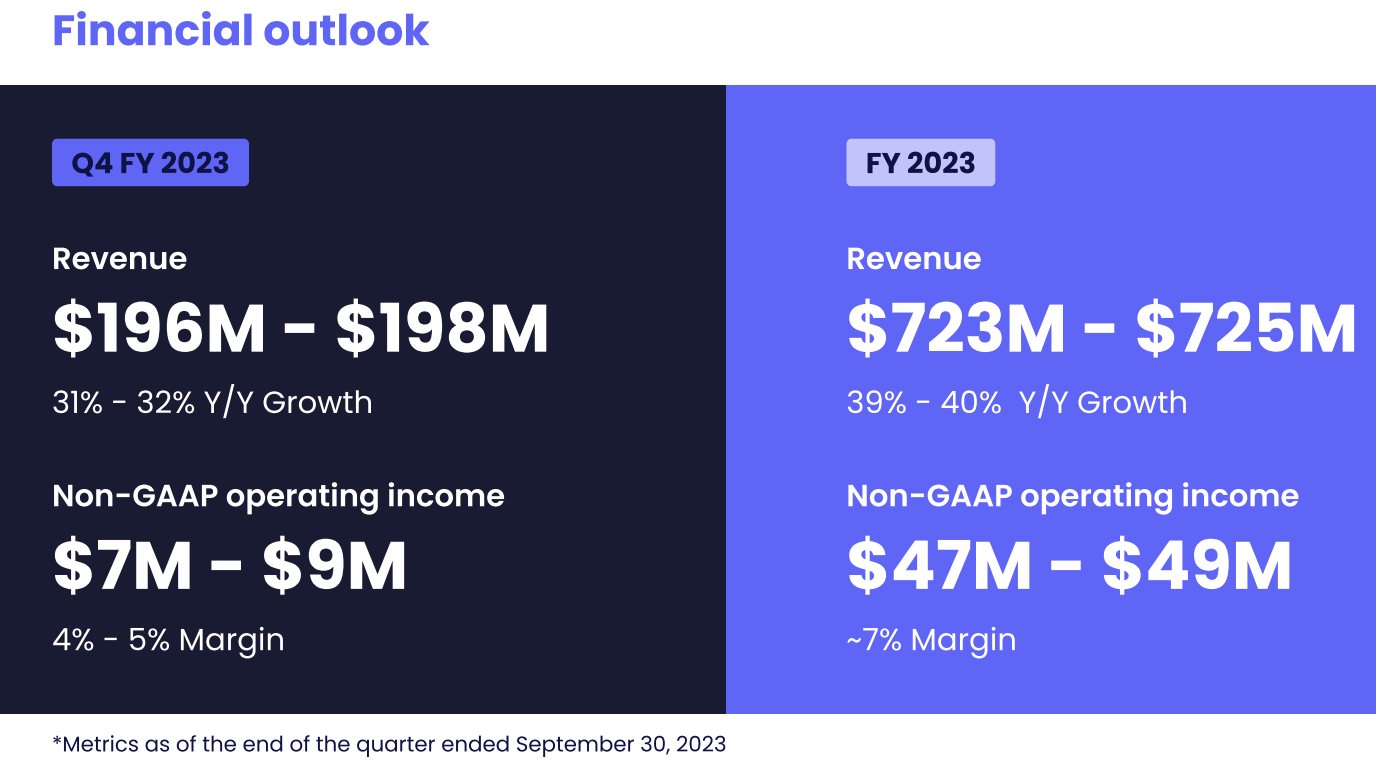

To close this section, below, we can see Monday's guidance for Q4 2023 and the full year. With a little earnings beat in mind, Monday will likely grow at 35% in Q4 2023, which far exceeds the average growth rate of all publicly listed software companies presently.

Q3 2023 Monday Shareholder Letter

{kind=link}

Valuation

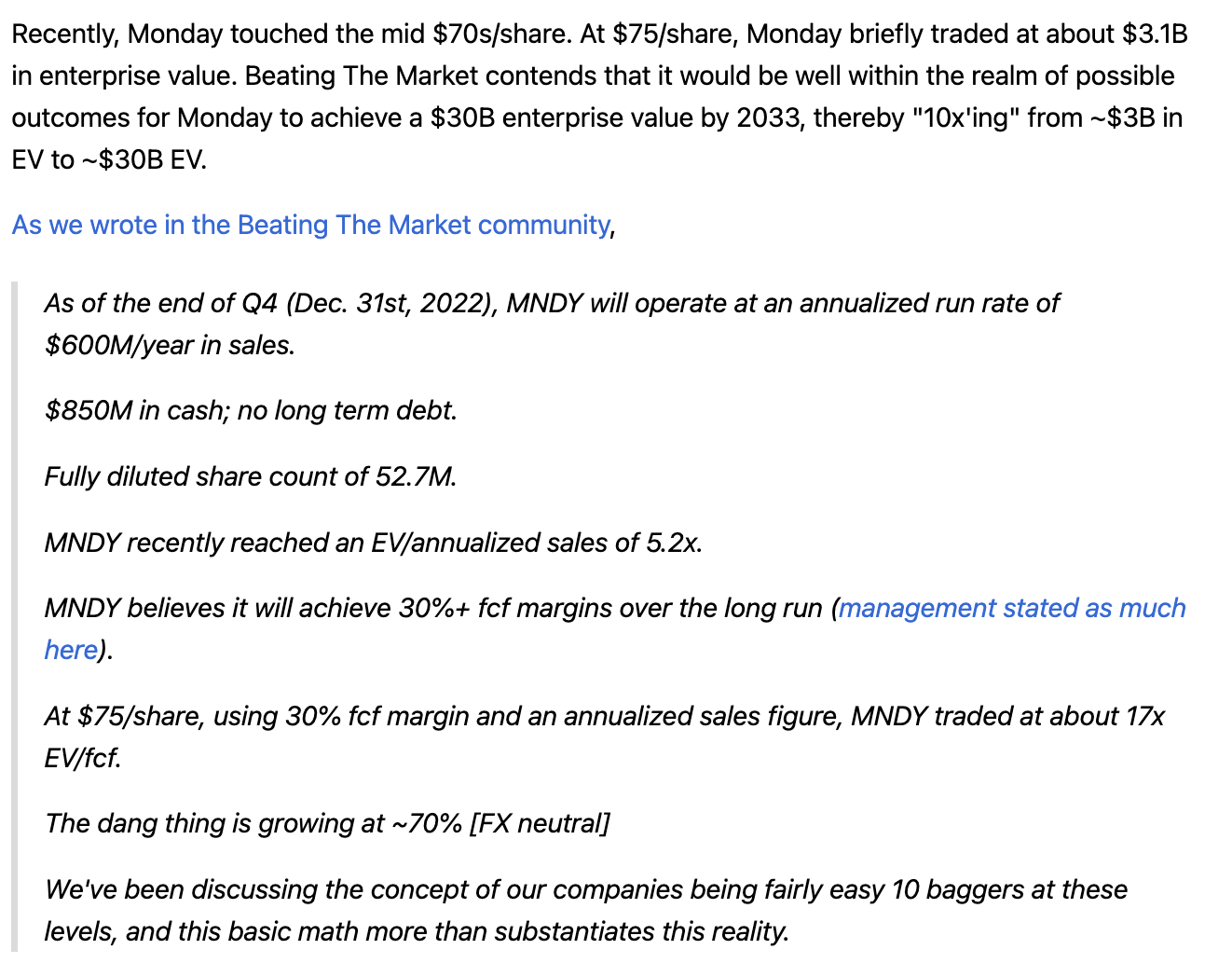

In late 2022, I'd often assert that Monday was an easy 10-bagger from the double digits.

{kind=link}

Today, Monday is up over 100% from its lows of about $80/share in late 2022; however, I still think it's quite attractive and the humble assumptions depicted below substantiate as much.

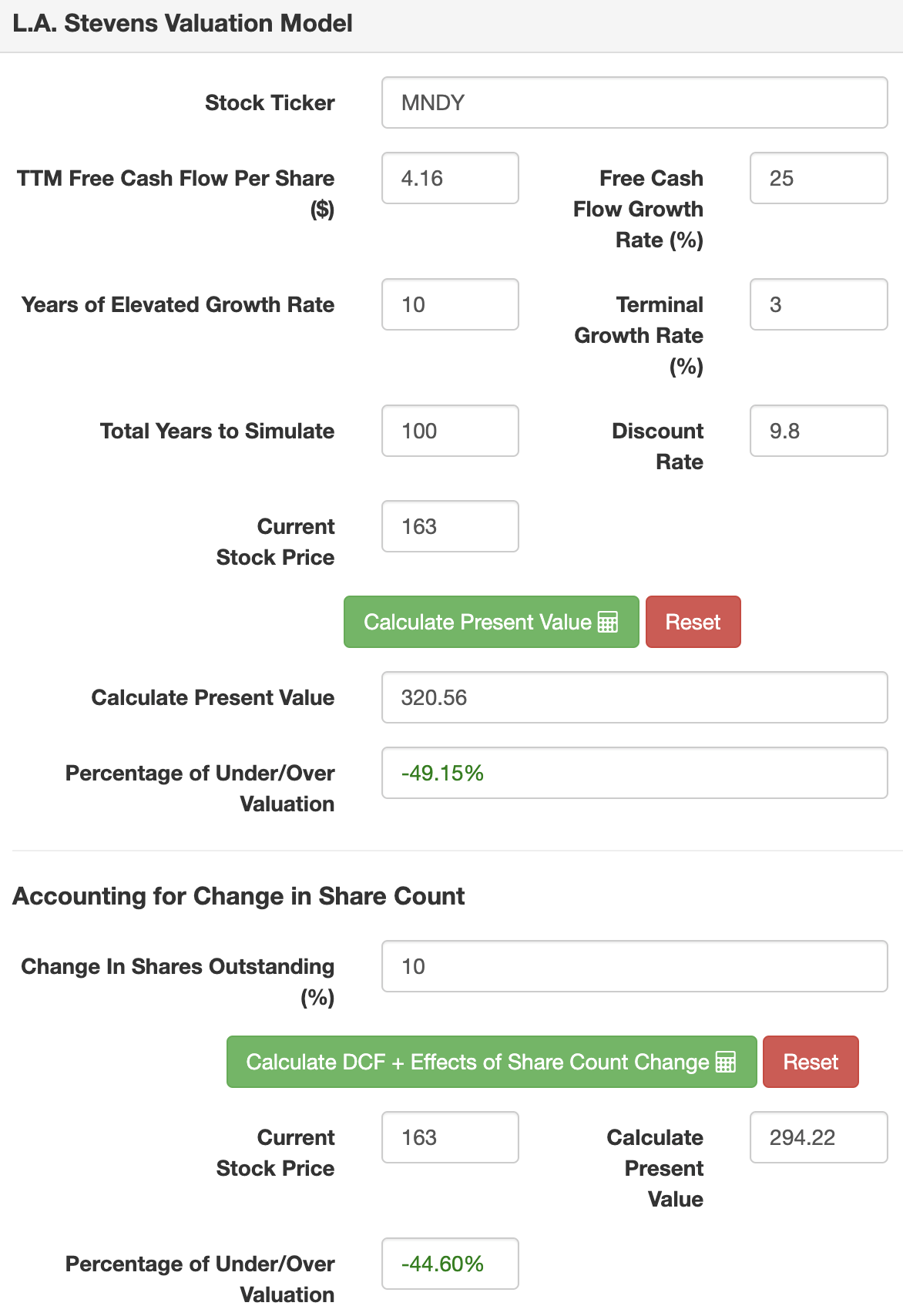

Assumptions:

| TTM Sales [A] |

| $731 million |

| Potential Free Cash Flow Margin [B] |

| 30% |

| Total diluted shares outstanding [C] |

| 52.7 million |

| Free cash flow per share [ D = (A * B) / C ] |

| $4.16 |

| Free cash flow per share growth rate (conservative) |

| 25% |

| Terminal growth rate |

| 3% |

| Years of elevated growth |

| 10 |

| Total years to stimulate |

| 100 |

| Discount Rate (Our "Next Best Alternative") |

| 9.8% |

And here are the results:

{kind=link}

In light of Monday's youth and the tendency of software companies to dilute the living daylights out of their shareholders, some may take issue with my decision to factor in only 10% dilution over 10 years.

My decision to do this stems from the fact that we've been modeling Monday using its fully diluted share count of 52.7M since it IPO'd in 2021, and it has still not breached that share count level as of today, two full years later.

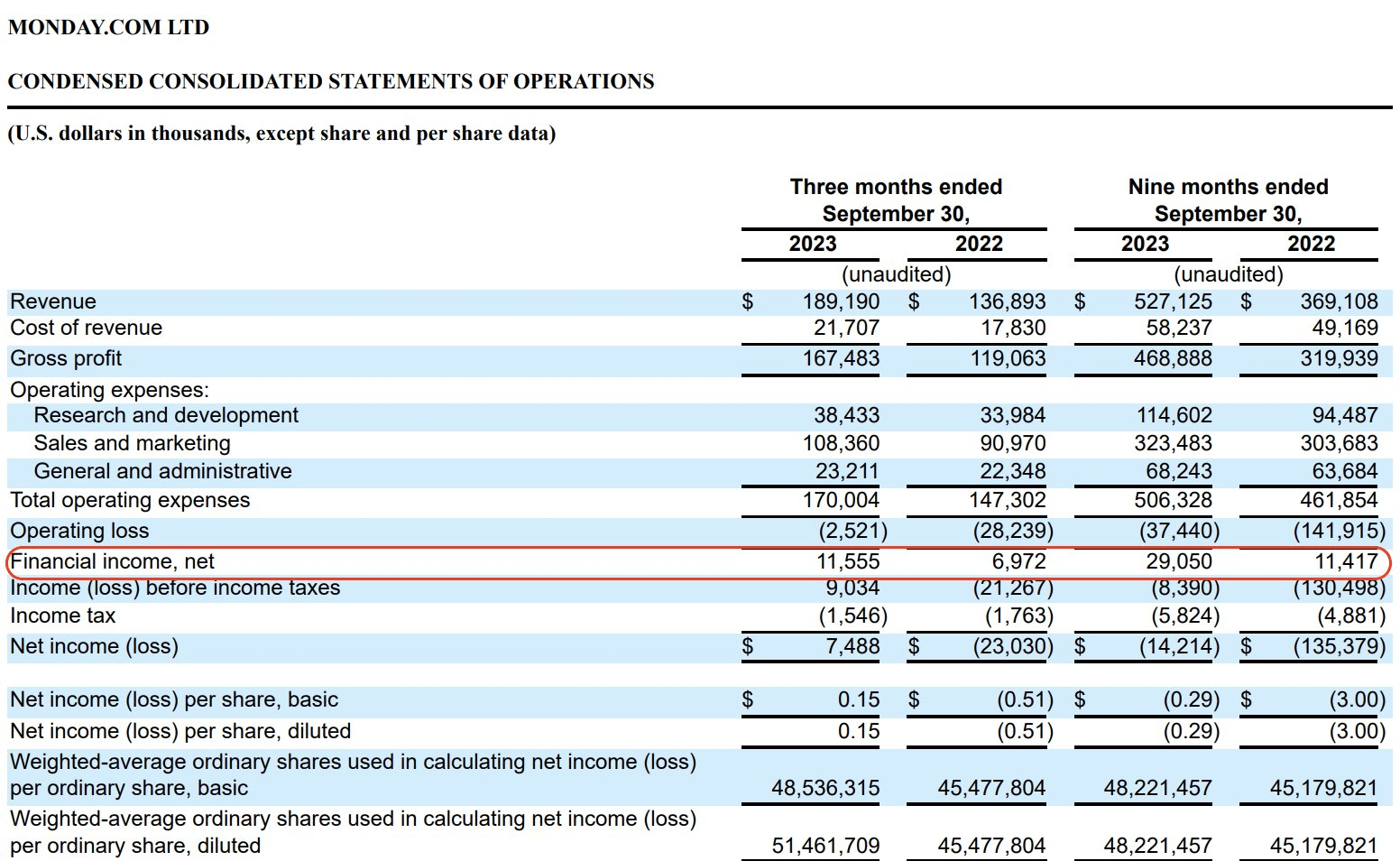

G&A expense was $15.2 million or 8% of revenue compared to 11% in Q3 2022. Net income was $32 million, up from $2.6 million in Q3 2022. Diluted net income per share was $0.64 based on 51.5 million fully diluted shares outstanding. Total employee headcount was 1,744, an increase of 98 employees since Q2 '23. We expect to continue hiring over the next year with a focus on our R&D product and sales teams as we build out our platform and product suite.

Eliran Glazer, CFO, Q3 2023 Monday Earnings Call.

I believe Monday has created a culture of disciplined execution, so, if there is further, meaningful dilution, I believe it will come in tandem with an acceleration in top line growth, making my 25% annualized growth assumption too conservative.

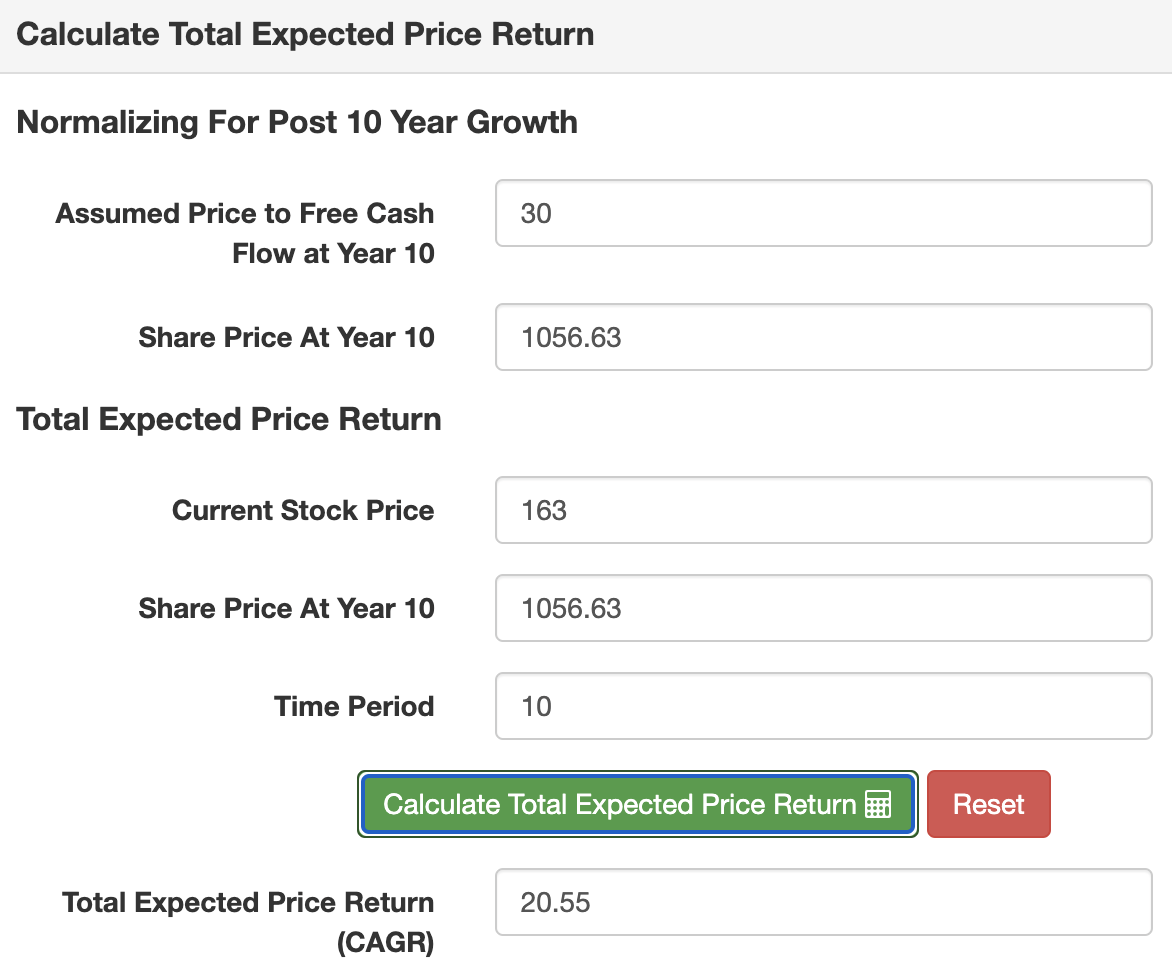

Turning to total projected returns:

{kind=link}

I chose a free cash flow yield of 3.33% (invert the 30x assumed just above) because I believe Monday will still grow at 15-30% annualized by 2034.

Monday's CEOs are still just in their early to mid-40s and will really be hitting their stride by early next decade.

As you can see, we're getting about 20% annualized returns from these levels.

I do not believe this to be an extraordinary return profile, as I thought was the case for Monday's return profile when it traded in the double digits.

I do not believe this to be insufficient either.

I think we're getting a fair appraisal of risk with this return profile (remember that risk = return).

Concluding Thoughts: Multi-Product Strategy

{kind=link}

In the interest of brevity, I will not make this an academic course on business development, employing our four foundational investment frameworks (Monday fits within three of them at present) to delve into the process by which Monday has grown at incredible rates and will likely continue to do so.

That said, I did want to spend just a little bit of time illustrating Monday's success in its multi-product strategy.

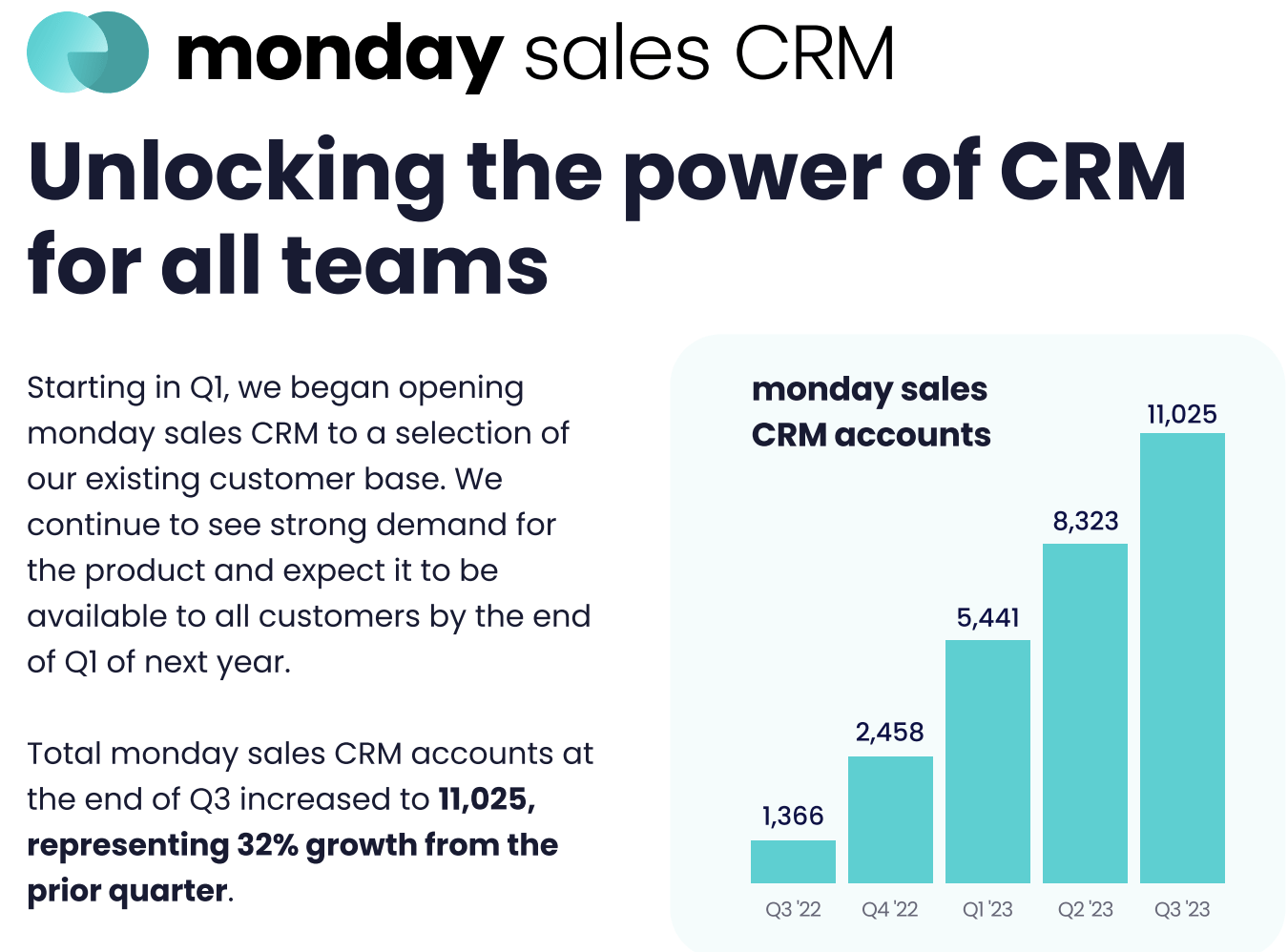

We remain focused on our multiproduct strategy and ensuring that our products can successfully scale cross functional collaboration for our customers. Our new products continue to show a remarkable cross-sell opportunity with 2,534 initial work management accounts adopting one of our new products. We are dedicated to providing exceptional solutions that meet the evolving needs of our customers, and we believe that our new products will play a pivotal role in achieving this.

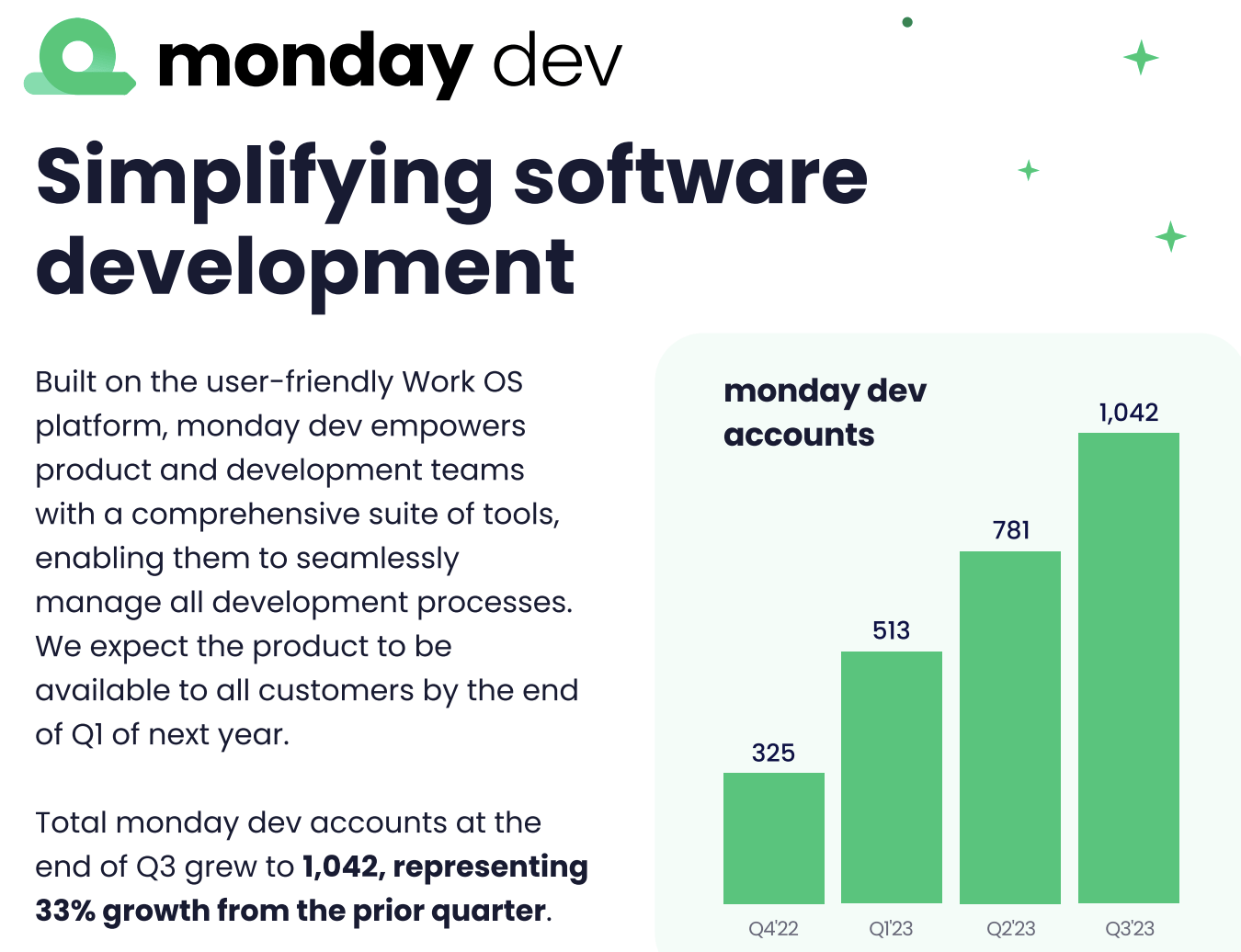

Our target is to open access to our new monday sales CRM and mondayDev products to all customers by the end of Q1 of next year. In Q2, we've successfully completed mondayDB 1.0. With the completion of that phase, all monday customers have been transitioned to our new cutting-edge infrastructure and initial feedback has been amazing. Users are noticing a meaningful boost in performance and capabilities of the Work OS platform.

Eran Zinman, co-CEO, Q3 2023 Monday Earnings Call (emphasis added).

{kind=link}

Monday has quite masterfully executed within the parameters of both our first and third foundational investment frameworks, in that it has launched a series of new products thoughtfully, each of which has found commercial success to an almost surprising degree; each of which vertically and seamlessly integrates into one highly customizable platform.

This has resulted, at least in part, in the incredible revenue growth and financial metrics we observed earlier and which can be seen below.

As Monday's Platform Has Rapidly Evolved, Its Scale Has Likewise Increased

{kind=link}

Specifically, Monday's CRM product has been a huge success, as can be seen below.

Monday's CRM Product Scales Rapidly

{kind=link}

And its dev product has seen similar success following its launch:

Monday's CRM Product Scales Rapidly

{kind=link}

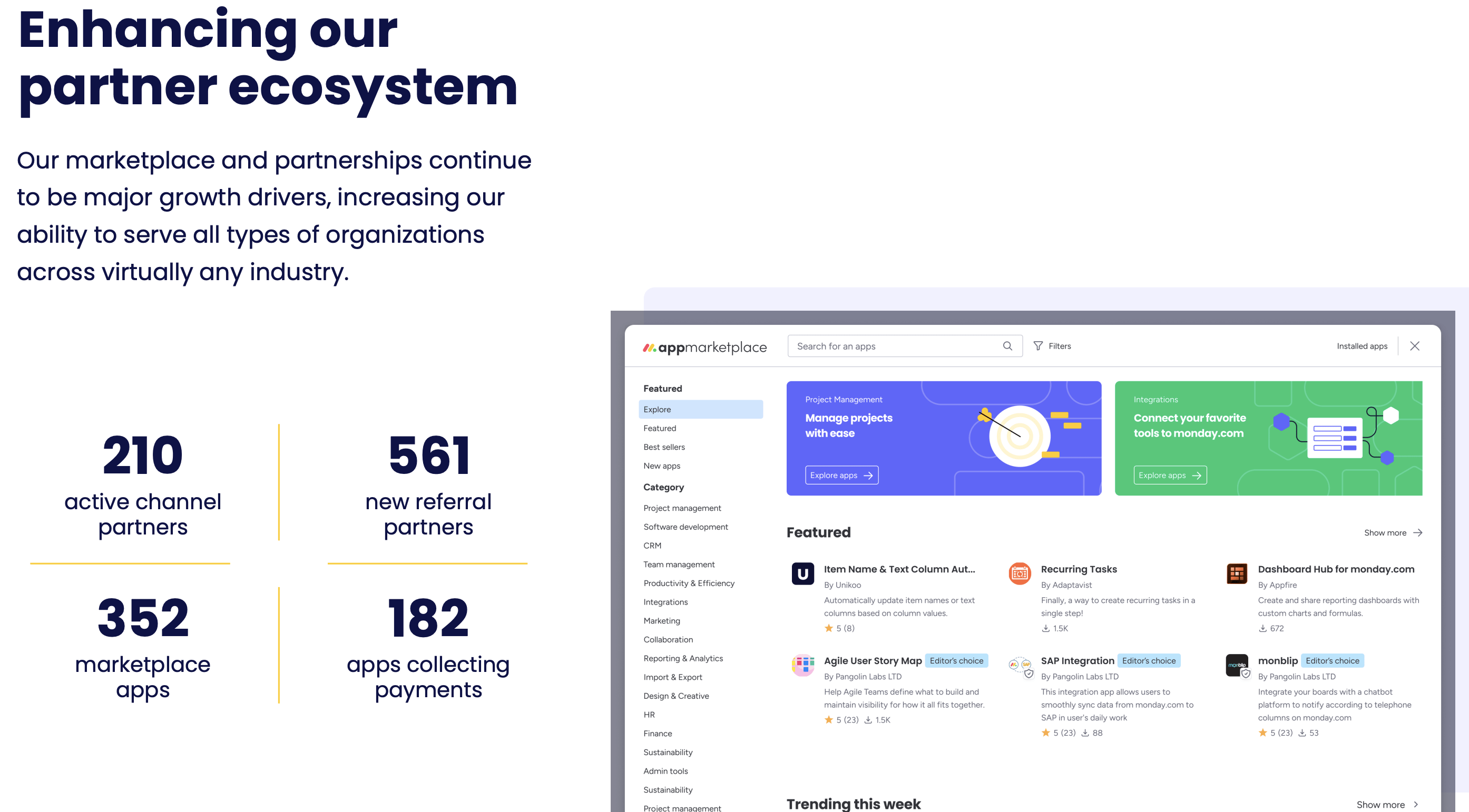

In addition to these new products, which should create large revenue streams for Monday over time, the company has continued to scale its app marketplace, which is essential for satisfying the nuanced, idiosyncratic needs of its ~200k customers.

{kind=link}

Thinking of Monday through the lens of economic moats, this app marketplace aids in creating an embedding, or switching costs, moat in that, because Monday users build out their workflows on Monday and incorporate apps from the Monday marketplace, they will be less inclined to switch off the platform.

On the subject of Monday's app marketplace, I found the following thoughts to be insightful (emphasis added):

David Hynes: I'm curious what you're seeing in terms of activity and engagement in the marketplace ecosystem. It seems like, as you make improvements in scalability and continue to roll out new product, there's just that much more surface area for partners to build around. So curious, if you're seeing any signs of that, playing out and what it could mean, for the model over time?

Eran Zinman: So definitely, we see good momentum there. We're starting to see more and more - kind of more significant ARR coming from our marketplace .

The partnership with both Upfire and Adaptivist are growing really nicely. It takes time, but currently, those two partners have some of the most popular apps in our marketplace. So definitely, we see the momentum that they bring and their experience, it's definitely helpful.

So, we're very encouraged with everything we see. We see some vertical applications built not just for the platform, but for each one of our apps for CRM, for work management, for dev. So definitely, this really enriches the marketplace and the opportunity for each one of them.

And in addition to the bigger partners, we continue to see large momentum of smaller and indie developers that build in the marketplace. So all in all, like we're very encouraged with the development and the type of applications that are being built.

Q3 2023 Monday Earnings Call.

Monday's evolution and execution over the last few years has been second to none.

It has demonstrated that it should be seen among the likes of Atlassian ( TEAM ) (who Monday has said they admire and emulate), Salesforce ( CRM ), and HubSpot.

And, finally, to close my thoughts on Monday's multi-product strategy, I found the following exchange insightful:

Kash Rangan: I'm curious to hear you further expand the thoughts on the stabilization you saw in the expansion rate in the quarter. And also as you take a step back with the broadening out of the platform and the capabilities, and the different buying centers and the personas that you can go after, such as Dev, CRM and who knows what it turns in the future, how is the go-to-market approach of the company changing? You're good entrepreneurs, you've been through multiple businesses before and you can understand the nuances of how go-to-market might have to evolve given the broadening of the product?

Eran Zinman: So regarding the new products, our product ecosystem and how it helps in terms of our go-to-market, so definitely having multiple personas and multiple verticals really helps in two ways, really. One is our ability to do both performance marketing across multiple verticals just makes our customer acquisition much more efficient. And this goes all the way to events and exhibitions, and we have different personas that can buy the software.

But more than that, it allows us to be more aggressive because our LTV for each customer is much greater. We don't just compete in one vertical, but a customer might start with a CRM and then expand into work management or vice versa. So the total LTV of each customer is much greater, which allow us to be potentially more aggressive going forward in how we acquire customers. So it definitely opened up our ability to acquire customers and expand them over time.

Q3 2023 Monday Earnings Call.

In short, I continue to like Monday a lot at these levels and higher and lower.

For further details see:

monday.com: Interminable Strength In A Challenging Time