MNDY - monday.com: Q2 Earnings Just Another Optimum Quarter

2023-08-15 05:57:14 ET

Summary

- monday.com reported another beat-and-raise quarter both on the top and bottom lines.

- The company's product innovation efforts continued to bear fruit with several important announcements in Q2.

- These should aid revenue growth reacceleration in 2024 coupled with further improvement in margins.

- In the light of this, valuation of shares seems still conservative leading me to affirm my Strong Buy rating.

Introduction and investment thesis

With its user-friendly, low-code/no-code project and work management ((PWM)) platform monday.com ( MNDY ) is a pioneer in the rapidly changing, competitive PWM space. The company is in the middle of a product innovation cycle, where it reached several new milestones in its most recent quarter. Partly these innovations helped them to exceed the high end of their previous Q2 targets, and enabled management to raise its 2023 revenue estimate for the third time in a row.

Meanwhile, macroeconomic pressures still exist, which continue to effect expansion from existing customers. These effects could impact the upcoming quarters as well, however, based on management’s recent guidance to a gradually decreasing extent.

Considering the company’s growth prospects and further improving margin profile valuation of shares seems still conservative, which makes me affirm my Strong Buy rating for the shares.

Growth drivers remain intact

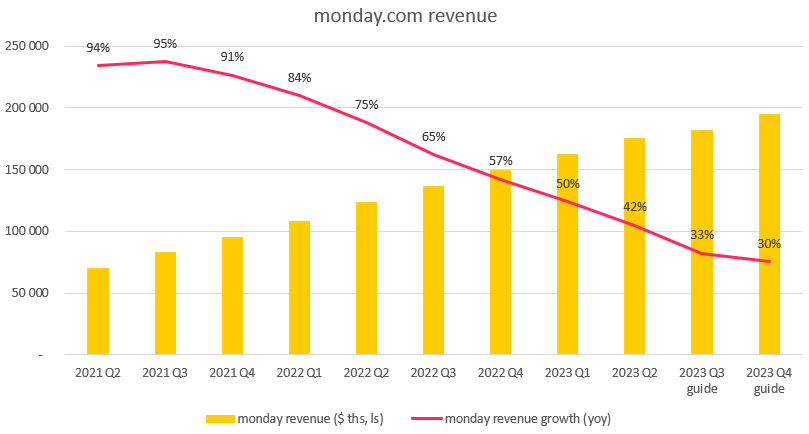

monday reported revenues of $175.7 million for the 2023 Q2 quarter, beating the high end of its previous guidance ($170 million) by 3.3%. This resulted in a yoy growth rate of 42%, a further gradual decline from previous quarter’s 50%. As macroeconomy related pressures continue to have a negative effect on seat expansions, investors should expect this trend to continue. However, there could be some light at the end of the tunnel as management guidance for Q3 and Q4 (implied from 2023 annual guidance) suggest that a turnaround could be on the corner:

Created by author based on company fundamentals

{kind=link}

For the Q3 quarter management guided for revenues of $181-183 million, a 33% increase at the midpoint. For 2023 as whole the guidance has been raised for the third time in a row, which has been quite rare among SaaS companies recently. Now it stands at $713-717 million, which would represent 37-38% yoy growth for the entire year. From the Q1/Q2 facts, and the Q3 and 2023 guide we can calculate the implied guidance for the Q4 quarter, which is $195 million at the midpoint. This would mean 30% yoy growth compared to 2022 Q4, only a slight downtick from the 33% projected for Q3. This suggests that the gradual decline in the headline growth rate - resulting mainly from the uncertain macroeconomic environment – could soon come to an end, which represents the same story hyperscalers told investors on their most recent earnings calls.

I believe it’s a sign of management confidence that the 2023 guidance has been raised by $11 million at the midpoint, approximately twice the size of the Q2 beat. The reasons behind this confidence could have been several folds.

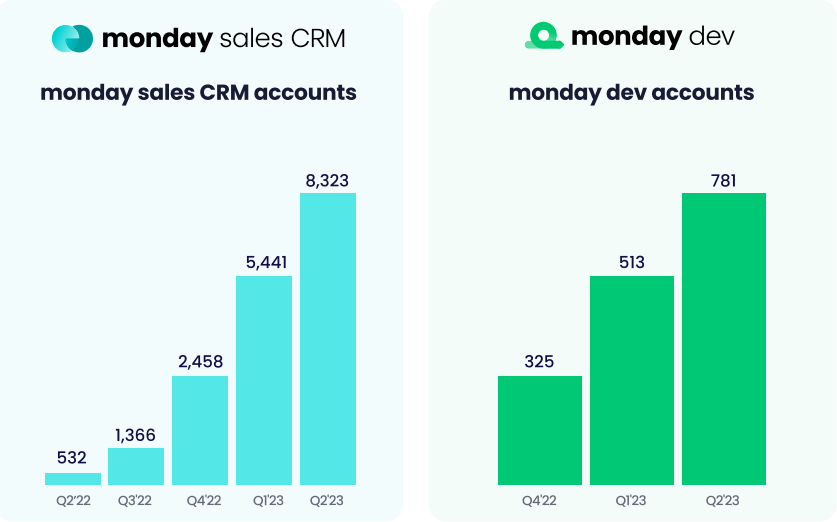

First and foremost, the company’s redesigned product strategy continued to gain traction as the number of monday sales CRM and monday dev accounts continued to rise significantly in Q2:

monday.com Q2 shareholder letter

{kind=link}

monday introduced these two distinguishable products last year as an extension to its core work management platform. Both products are currently available to approximately half of monday’s customers, monday dev has gotten out of beta only recently. Looking at the chart above we can see that the number of customers using these products continued to increase rapidly in Q2, by more than 50% qoq in both cases. This represents strong cross-sell opportunities going forward and could be a major competitive advantage in the crowded PWM space.

Besides the main platform, the company’s marketplace continued its growth trajectory counting 301 apps of which 136 have been monetized. This shows that not only the number of total apps has increased significantly over the quarter, but also the ratio of monetized apps continued to tick higher:

Created by author based on company fundamentals

Although the revenues derived from the marketplace are representing only a tiny fraction of total revenues currently, they could be important growth drivers in the future if these trends persist.

Another important catalyst of future revenue growth could be the integration of AI into the work OS platform. The first steps have been taken in the Q2 quarter and a handful of AI-based apps have been released by the company based on their AI Assistant infrastructure. Among others these include AI-assisted automated task and content generation, formula building or email composition.

On the top of that monday decided to open up its platform for 3 rd party developers to build AI apps, which has been also a great success. The AI show will go on in the upcoming quarters as well, as already in Q3 a new AI solution builder will be rolled out based on OpenAI’s technology. These efforts are a good proof in my opinion that monday is a truly innovative company and is quick to adopt to changing customer needs.

Based on these continuous innovations it’s no wonder that more and more enterprises decide to start using monday’s platform or make larger commitments, if they are already customers. The company closed Q2 with 1,892 enterprise accounts (defined by customers with >$50,000 ARR), a yoy growth of 63%. This means a net addition of 209 such customers in Q2, the same number just one quarter before:

Created by author based on company fundamentals

Comparing with the numbers of previous quarters Q1 and Q2 in 2023 seem to be quite encouraging, especially in the light of the fact that macroeconomic pressures didn’t cease to exist. Based on this it’s no wonder that these customers make up a constantly increasing portion of monday’s revenues, reaching 29% of total ARR in Q2:

monday.com Q2 shareholder letter

It’s important to note that the general macroeconomic slowdown and the resulting IT budget cuts have an impact on the growth of this segment as well, which can be evidenced by net dollar retention rate ((NDRR)):

monday.com Q2 shareholder letter

After printing more than 150% just one year ago it has declined to somewhere between 120% and 125% for Q2. However, compared with the company’s total NDRR, which stands somewhere between 110% and 115%, this is still superior, showing that these customers are the ones who really drive topline growth. Management expects some further slight decrease in this metric this year, but based on the Q2 earnings call they are already seeing some signs of stabilization.

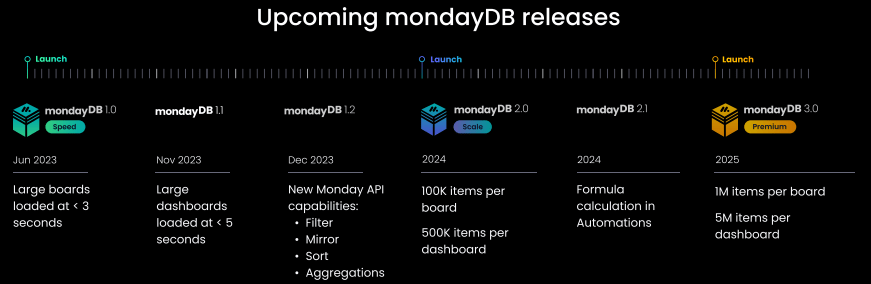

An important innovation of the company, which could further strengthen their appeal to enterprise customers is their freshly developed database architecture for the work OS platform, mondayDB 1.0 . It enables up to 5x faster load times for larger, more complex boards, so it’s well-suited for more data-intensive workflows typically pursued by enterprise customers. And this is just the beginning, there are several upcoming releases in the pipeline for mondayDB over the upcoming years:

monday.com Q2 shareholder letter

{kind=link}

Based on the trends described above I believe that monday has several growth catalysts in the quarters/years to come, which puts them in a strong competitive position within the PWM space. Furthermore, based on management comments on the Q2 earnings call in 70% of the cases new customer lands doesn’t experience any competition. This suggests there are still a lot of greenfield opportunities out there, despite the significant number of competitors in the space.

Further improvement in margins

After the seasonally higher S&M spending in Q1 non-GAAP operating margin returned to the ~10% levels it has reached for the end of 2022:

monday.com Q2 shareholder letter

Based on management comments R&D expenses should continue to track around the high teens as % of revenues as the company continues its innovative push in different product categories. Further improvement in margins could rather come from proportionally decreasing S&M expenses resulting from increasing economies of scale as the company matures.

After Q2’s beat on the bottom line as well (non-GAAP op. income of $16.6 million vs $2-4 million guidance) management raised its 2023 guidance from ~1% non-GAAP operating margin to 3-4%, which is still conservative in my opinion.

Looking at free cashflow, monday had another record quarter by generating $45.9 million, equaling an FCF margin of 26%:

monday.com Q2 shareholder letter

With this, cash and cash equivalents reached almost $1 billion for the end of Q2, a comfortable amount for financing liquidity needs and possible smaller acquisitions. However, management noted recently that they are not considering meaningful acquisitions currently as the company rather focuses its efforts on in-house innovations. Up to this point this strategy seems to pay off.

Valuation

Even after the post-earnings surge of 8.5% shares of monday still trade at conservative valuation multiples. This is especially true in the light of the company’s strong growth prospects and improving margin profile. I updated my relative valuation framework for the public PWM space, which shows that monday and Smartsheet ( SMAR ) are still those companies who are underappreciated by the market:

Created by author based on company data and analyst estimates

Based solely on this relative valuation framework shares of monday should trade 20% higher in order to trade at their fair forward EV/Sales multiple.

Risk factors

I believe the most important risk factor for investing in the company’s shares is the strong competition in the PWM space. There are larger, well-established companies like Atlassian ( TEAM ) or ServiceNow (NOW), but also smaller, innovative, private companies like Airtable or ClickUp. These and many other competitors offer a wide array of solutions, which directly compete with the offering of monday. This limits the pricing power of the company, and when greenfield opportunities cease to exist it could significantly impact revenue growth.

Another important risk factor to consider is the global macroeconomic slowdown, which impacts the company’s fundamentals now for more than a year. If this would be more prolonged than currently expected, it would further limit seat expansions of existing customers. I believe after recent positive comments from hyperscalers the market began to price in a gradual turnaround in the software space in 2023 H2. If this would fail to materialize it could lead to a material correction in share prices in my opinion.

Conclusion

monday.com continued to fire on all cylinders in Q2 printing another beat-and-raise quarter. The company’s product innovation cycle continued to evolve, with several important announcements, which could contribute to revenue growth reacceleration in 2024. I believe monday’s fundamental strength isn’t properly reflected in the current valuation of shares, which should call for continued outperformance within the PWM sector.

For further details see:

monday.com: Q2 Earnings, Just Another Optimum Quarter