MNDY - monday.com Q4 Earnings: Witnessing History

Summary

- monday.com is a unique company in probably the most crowded segments of the SaaS space.

- Q4 earnings confirmed that monday is sticking to its transformative leader position.

- Besides a rosy sales outlook for 2023, non-GAAP operating margin reached positive territory for the first time in company history.

- Even after post-earnings surge valuation seems still compelling.

Intro

monday.com ( MNDY ) based in Tel-Aviv, Israel is a unique company in probably the most crowded segment of the SaaS space: project and work management software. In my previous article on the company (“ monday.com: Making A Difference ”) I have outlined the details from both a product and financial perspective why I think they could be long-term winners in this fiercely competitive market.

The company’s platform combines ease-of-use with low-code, no-code customization making them stand out from competition. Besides, monday is characterized by continuous innovation and flexibility, which is a must in such a competitive space in my opinion. One good example for this from the current earnings release is the company’s new partnership with Appfire, the world’s largest collaboration app provider, which helps expand the reach of Monday’s marketplace further. Another freshly announced example is the introduction of monday DB, which increases the speed and reliability of the company’s platform and infrastructure with possibly 10x faster board load times.

Until recently monday was far from making an operating profit as it invested heavily in sales and marketing. Strong topline growth showed that these investments have paid off nicely and cost per account sign up steadily decreased throughout 2022 with showing some slowdown in recent months:

monday.com 2022 Q4 shareholder letter

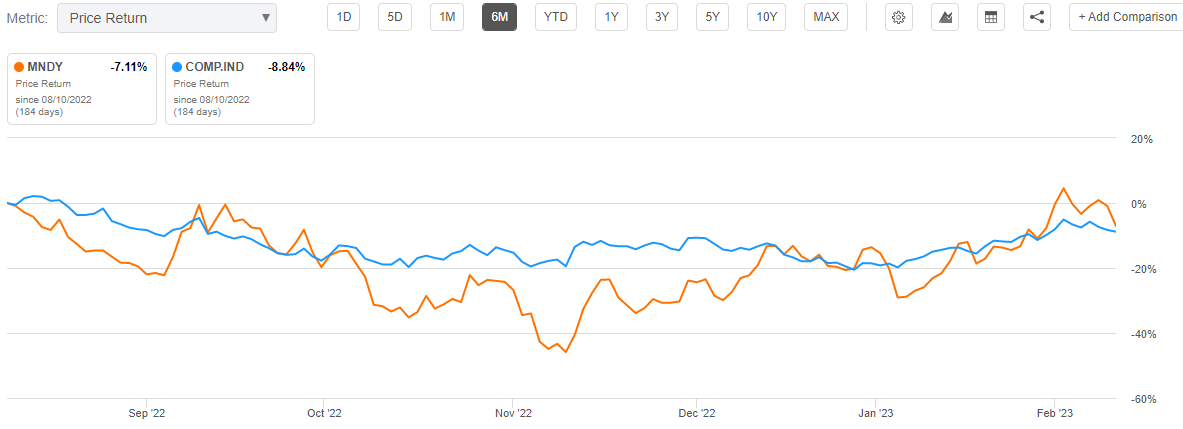

This has resulted in increasing acquisition efficiency during the year justifying aggressive investments in further growth. Although unprofitable growth stocks in general have fallen from the grace since inflation picked up in 2022, the share price performance of monday has been on par with the Nasdaq for the past 6 months (until the release of Q4 earnings):

{kind=link}

With this, shares outperformed many other SaaS companies during this volatile period confirming that something unique is going on at the company.

Finally, recent disappointing outlook from key competitor, Atlassian ( TEAM ) made monday’s upcoming earnings release even more exciting, making investors guessing whether a more pronounced slowdown could be in the box for the project and work management space in general.

Q4 earnings: Comfortable beat-and-raise on the topline

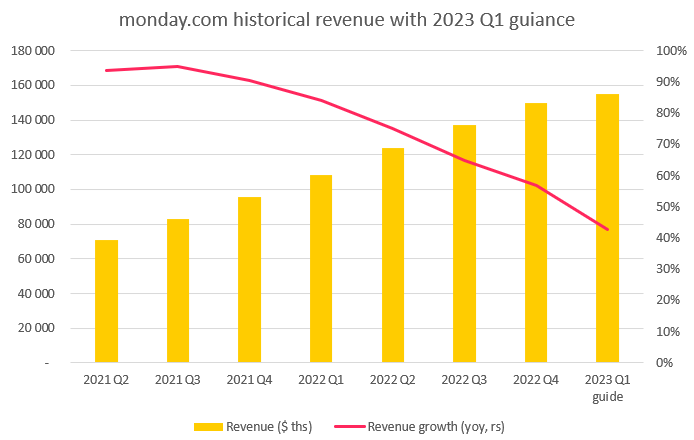

Investors could breathe a sigh relief after monday released its 2022 Q4 numbers yesterday as they showed continued strong growth momentum in the company’s business coupled with further improving margins. Revenue came in at $149.9 million growing ~57% yoy or 60% on an FX-adjusted basis. This has resulted in a ~6% beat compared to the average analyst estimate, which was also typical for the previous two quarters.

On the top of that, management guidance for 2023 Q1 and FY2023 has been comfortably above analyst estimates providing evidence that topline growth isn’t falling off a cliff. For the 2023 Q1 quarter monday expects revenues in the range of $154-156 million topping even the highest analyst estimate:

{kind=link}

The same has been almost also true for 2023 total revenue guidance that fell into the $688-693 range with analyst estimates ranging from $603-690 million:

{kind=link}

If we look at revenue trends in the light of these estimates, we can see the following:

{kind=link}

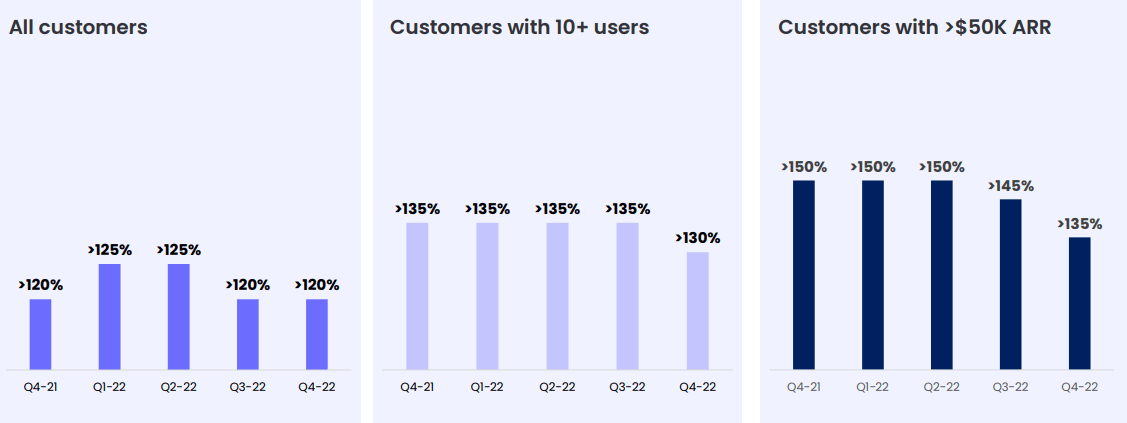

Even with the raised 2023 Q1 guide the slowdown in topline growth seems to be significant for the first sight: after growing 84% yoy in 2022 Q1 revenue is now projected to grow 43% in 2023 Q1, almost half the growth rate year one year ago. If we factor in the usual ~5% overperformance we arrive to a growth rate of 50% that sounds somewhat better. However, even in this case it is clear, that monday is also not exempt from the current macroeconomic downturn. The most obvious impact can be seen on the net dollar retention rate (NDR rate) in the enterprise customer segment (customers above $50,000 ARR) that saw conspicuous decline in recent quarters:

{kind=link}

Last quarter management blamed the slight decline on FX impact and the increasing contract size of initial customer lands. This quarter they acknowledged in their shareholder letter that seat expansion has slowed in this segment resulting from the challenging macroeconomic environment. On the Q4 earnings call management highlighted the negative effect of tech company layoffs on monday’s seat expansion as ~30% of revenues are derived from this sector. As these companies slowed headcount growth and laid off people so did the short-term potential for monday’s platform decline. As the NDR rate is a trailing four-quarter metric investors should expect further slowdown in the upcoming quarters. Nevertheless, a ~50% yoy topline growth rate for a company with annual revenues above $500 million is still quite impressive.

To sum it up, the main takeaway regarding the company’s topline is the following in my view: The general macroeconomic slowdown has a visible impact on monday, but revenue estimates have been already de-risked by management comfortably, which makes the company’s shares more investable in the current environment. This is especially true in the light that FY 2023 guidance has also seen the daylight providing a positive surprise for investors.

A historical milestone in profitability

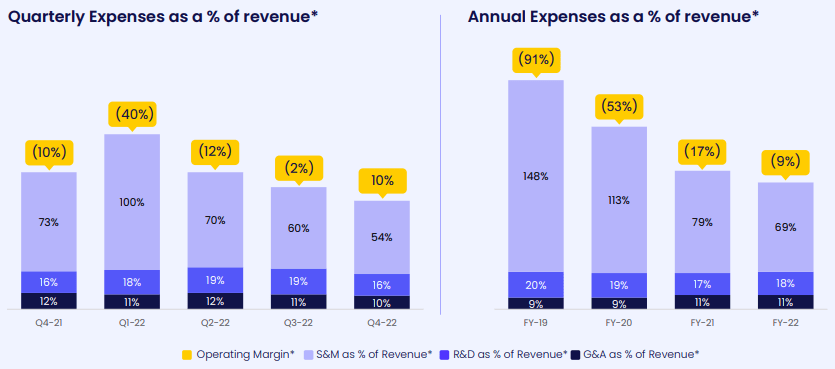

Although management guided for a Q4 non-GAAP operating margin of negative 14-15% last quarter monday reported its first ever positive number for this metric with 10%. This has been a huge beat, which didn’t only result from the beat on the topline but the significant cost control monday exercised during quarter.

After steadily growing for several quarters the headcount at the company has been flat in Q4:

monday.com 2022 Q4 shareholder letter

Along with other things this has resulted in proportionally decreasing operating expenses that has been the most pronounced in Sales and Marketing (S&M):

{kind=link}

Both when looking at quarterly and annual figures we can see a clearly declining tendency. Regarding 2023 management outlined the following plans on the Q4 earnings call: In S&M they currently don’t have plans to increase headcount further, although they plan to increase spending on performance marketing (e.g.: ads) to some extent as they see increased returns on these investments. As this category makes up ~30% of S&M spending it won’t result in a meaningful increase in overall spending. On the R&D front monday plans to increase headcount in 2023 as they continue their path on innovation. Based on management comments R&D spend could equal around 20% of revenue in 2023 a slight increase compared to 18% in 2022.

With this, I believe monday will be able to remain cash flow positive in the upcoming quarters and perhaps positively surprise investors on the operating margin side again. Management guided for a negative 12-13% non-GAAP operating margin for 2023 Q1 setting the bar quite low in my opinion.

Finally, looking at FCF margin at the company it jumped to 20% in Q4 that resulted in an increasing cash balance to $886 million for the end of the quarter from $853 million in Q3. From this point on I believe the question won’t be whether a given quarter is FCF positive or negative rather how positive it is.

All in all, monday has closed 2022 as a Rule of 77 company when adding Q4 revenue growth and FCF margin or as a Rule of 70 if we look at the year of 2022 as a whole. I believe this demonstrates the continued strength of the company’s business model well.

In the top of that there are further significant growth levers to pull in 2023 like the rollout of the company’s rebranded and extended product offering (monday Sales CRM, monday Marketer, monday Devs) for existing customers, which was only available to new customers throughout 2022. Looking at the success of monday Sales CRM among new customers in 2022 I believe this will resonate well among the existing ones:

monday.com 2022 Q4 shareholder letter

Valuation update

After post-earnings surge the market capitalization of monday has reached ~$6.6 billion. For 2023 management guided for revenue of ~$690 million manifesting in a forward Price/Sales multiple of ~9.5. Fitting this into the sales-based valuation matrix of project and work management companies results in the following picture:

Created by author based on company data

After taking the differentials in expected revenue growth rates into account we can see that monday can be regarded as slightly undervalued in the space. In the light of the fact, that usually the highest growers have the highest valuation premium I regard this as an attractive relative valuation signaling further room for outperformance within the sector.

Finally, I want to put the current forward P/S multiple of 9.5 into perspective. If we suppose that monday grows revenues at a CAGR of 25% in the upcoming 5 years, reaches a net margin of 20% (based on current strong gross margin profile), while shareholders suffer 5% annual dilution from stock-based compensation, shares would trade at a forward P/E of 16.3 in 5 years’ time. Compared to the average forward P/E of 17.2 for the S&P500 during the past 10 years I believe this wouldn’t be realistic if competitive dynamics won’t change too drastically in the space. Based on this, I believe there is further room for multiple expansion in the form of continued share price appreciation, especially in the light of the strong fundamental trends presented earlier.

Conclusion

monday.com is navigating the current challenging macroeconomic environment very well by combining continuous innovation with cost control. I believe the company has the ability to stay on the gas while others begin to hit the brakes resulting in market share gains.

As the project and work management space is quite competitive it is worth to monitor investments in this space regularly as thing can change quickly. I believe that until the beat goes on for monday possessing shares of the company is an investment that pays off well.

For further details see:

monday.com Q4 Earnings: Witnessing History