MNDY - monday.com: Recent Underperformance Has Been Unjustified

2023-11-18 00:11:20 ET

Summary

- Shares of monday.com underperformed peers since the escalation of the Israel-Hamas conflict, which seems unjustified in the light of recent Q3 earnings release.

- Current valuation suggests there is still significant room for shares to catch up to peers even after the post-earnings surge.

- Company-specific drivers, such as rapid adoption of emerging products and increased focus on enterprise customers, could lead to revenue growth reacceleration in 2024.

Introduction and Investment thesis

Since the renewed escalation of the Israel-Hamas conflict the shares of monday.com (MNDY) started to underperform against peers, as investors have been worried about potential operational disruptions to the company. Although the company’s customer base is truly global serving 200+ business industries in 200+ countries, their headquarter is still in Tel-Aviv, Israel.

The publication of 2023 Q3 earnings dispelled most of these fears in my opinion and resulted in a 10.5% increase of the share price that same day. However, I strongly believe that this post-earnings surge didn’t make up for the underperformance suffered during October, which is also supported by the significantly increased valuation discount to peers.

In the light of this, and recently published strong Q3 numbers I believe it’s a good time to invest in monday’s shares for the long run.

Unjustified underperformance

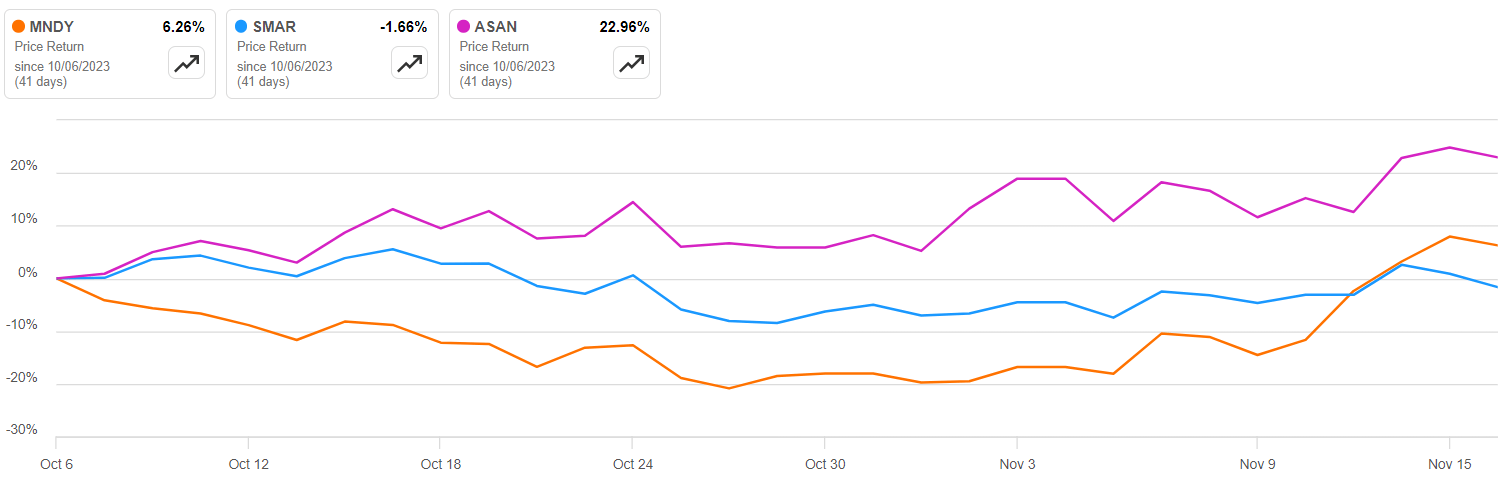

On the chart below I’ve compared the share price performance of monday with Smartsheet ( SMAR ) and Asana ( ASAN ) since the escalation of the Israel-Hamas conflict (7 th of October), representing two close competitors in the Project and Work Management Software ((PWMS)) space:

{kind=link}

Neither Smartsheet, nor Asana had their earnings published over this time horizon, so this couldn’t have impacted their share prices. If we look at the chart above, we can see, that for the end of October the share price of monday had been down almost 20% since the 6 th of October. Meanwhile, the shares of Smartsheet lost less than 10% of their value, while the shares of Asana were almost up 10%. As there have been no other significant company specific news around monday during October, I believe this underperformance can be mostly tied to the outbreak of the armed conflict.

With the publication of recent strong Q3 earnings the shares of monday began to outperform competitors in recent days. However, if we compare the performances since the 6 th of October, the relative share price performance of Asana is still ~10%-points better than that of monday, despite the recently published strong earnings print.

Based on this, I believe that monday’s share price has still a longer runway to catch up to peers. Looking at the shares’ valuation after the post-earnings surge confirms the same:

Created by author based on company fundamentals and analyst forecasts

On the chart above I’ve depicted the major public companies in the PWMS space based on their forward Enterprise Value/Sales ratios and their expected forward 12-month revenue growth rates. The last time I did this comparison three months ago (see my previous article on the company) it suggested that shares of monday are undervalued by 20% compared to average of the peer group. The recent update of my valuation framework shows that the valuation discount increased to 42%, which has been mostly the result of the underperformance during October.

In the light of strong Q3 numbers and the fact, that management calmed investors in the Q3 earnings call , that the effect of the armed conflict on the company’s operation is minimal, I believe this underperformance since last quarter is truly unjustified. So, I believe investors can purchase monday’s shares at current levels for a discount compared to peers, which won’t probably come back for a long time.

As an example, if we compare monday with Asana we can see quite similar valuation multiples when it comes to the forward EV/Sales ratio. Asana trades at 6x forward EV/Sales, while monday at 6.5x, which is close to 10% higher. However, the expected revenue growth rate over the upcoming 12 months is 12% for Asana, while 27% of monday, more than double . This would justify a significantly higher valuation multiple for monday, which should materialize soon in my opinion.

Q3 earnings quick take

monday managed to print the third beat-and-raise quarter out of three in 2023, which has been a rare streak among SaaS companies in the current fragile economic environment. Seat expansions from existing customers remained under slight pressure, which continued to moderate over the quarter. Meanwhile, new customer acquisition has been strong, and the penetration of recently launched products continued to increase nicely.

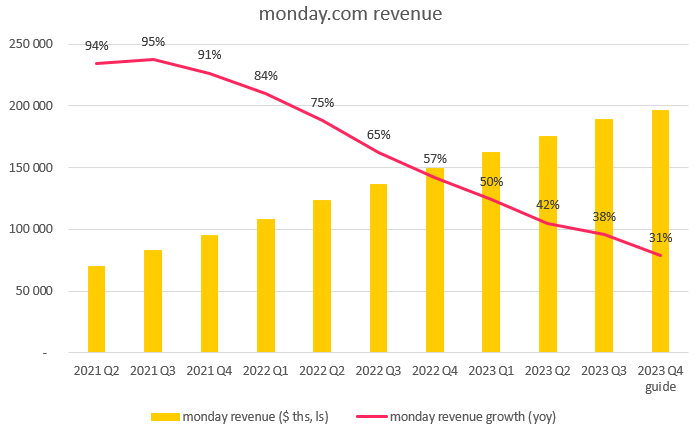

This resulted in revenues of $189.2 million over the Q3 quarter, an increase of 38% yoy. This has been a 4%-point deceleration compared to the previous quarter, which is significantly less than in the previous ones:

{kind=link}

This is a good sign in my opinion that topline growth slowdown could stabilize soon indeed. For Q4 monday guided for revenues of $197 million, which would equal a yoy increase of 31%. If the company manages to beat its guidance by ~3.5% like it did in Q2 and Q3 this would mean a yoy increase of 36% for Q4. I believe if this happens it could foreshadow a topline growth reacceleration for 2024.

The main company specific drivers, which could support this turnaround are the following:

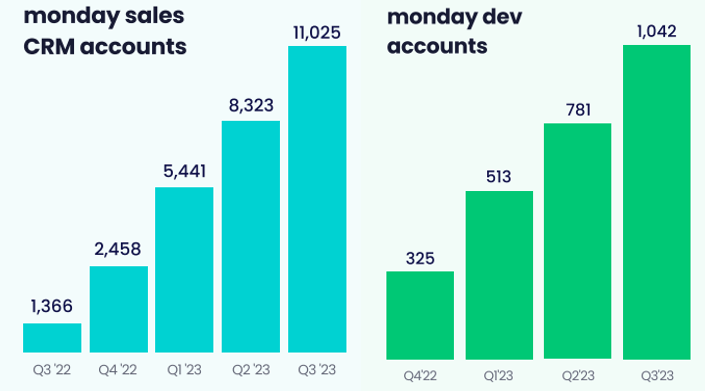

- Continued success of monday’s targeted PWMS products in sales CRM and software development. Both products are expected to be made available for all customers for the end of Q1 2024, which could build a strong base for revenue growth reacceleration next year. The number of these accounts continued to grow nicely in the Q3 quarter suggesting strong interest from existing customers:

{kind=link}

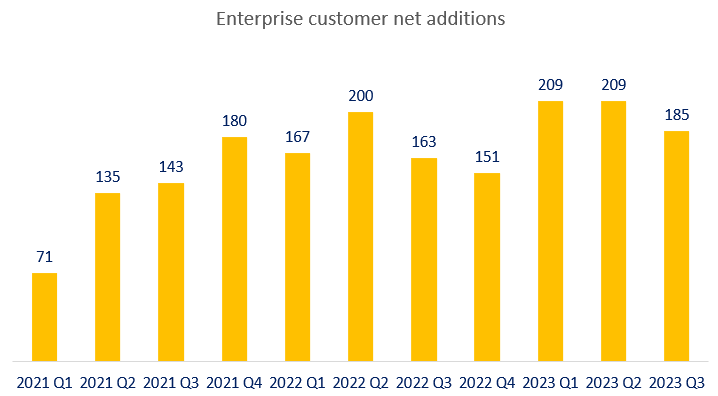

- Increased focus on enterprise customers . The number of enterprise customers (defined by >$50.000 ARR) increased by 57% yoy in Q3 reaching a total of 2,077 customers. This equaled a net addition of 185 customers over Q3, which has been down slightly from previous quarters (seasonally weaker quarter), but still up 13.5% yoy:

{kind=link}

The release of mondayDB 1.0 to all customers last quarter could be a great step towards winning more enterprise customers, as it helps significantly reduce board load times, which mostly matters with increasing scale. Currently, the company is already working on version 1.1 and 1.2, which will improve load times for larger boards even further.

- Increasing number of monetized Apps on Marketplace . The number of monetized Apps on monday’s Apps Marketplace continued to grow further in the Q3 quarter, which has been partly fueled by the company’s strategic partnerships with leading collaboration app providers like Appfire or Adaptivist:

Created by author based on company fundamentals

Over the last few quarters management emphasized that the contribution of the Apps Marketplace to total ARR is negligible, but his has changed in Q3 based on Eran Zinman’s comment on the earnings call: “We're starting to see more and more kind of more significant ARR coming from our marketplace.” Seeing the encouraging trends in total number of Marketplace apps and the share of monetized apps I believe this could be also an important driver of topline growth reacceleration in 2024.

Based on the trends above I see several company specific growth levers for the upcoming year. Looking at the macro level IT spending optimization is still headwind for the company, and the strong competition in the PWMS space is also a challenge. However, I believe the company specific drivers will more than compensate for these risks.

Finally, looking at margins they reached another record level in Q3. Non-GAAP operating margin came in at 13%, a 4%-point improvement sequentially:

monday Q3 shareholder letter

The main driver has been the further reduction in S&M expenses as % of revenues, which can be mostly explained by increasing economies of scale.

Free cash flow margin also set a record with 34% in Q3, but this can be rather regarded as a one-off based on management’s comments. With this, cash and cash equivalents crossed the $1 billion mark, which could be used for potential acquisitions over the next 12-18 months according to Eliran Glazer, CFO. So, this can be regarded as a further potential catalyst for accelerating topline growth.

Conclusion

Following the armed escalation of the Israel-Hamas conflict the shares of monday significantly underperformed the peer group during October. With the publication of Q3 earnings it seems there have been no significant disruptions to the company’s operations, although the increased valuation discount still exists. In the light of strong fundamental trends the increased valuation discount is not justified in my opinion, which should result in overperformance of monday’s shares over 2023.

For further details see:

monday.com: Recent Underperformance Has Been Unjustified