MNDY - monday.com's Positioning For 2024: Stabilizing Growth Rates

2023-11-15 18:30:52 ET

Summary

- Analyzing monday.com's performance, I remain optimistic about its strategic positioning for future growth.

- With a robust cash reserve exceeding $1 billion, monday.com has ample resources for strategic initiatives.

- Despite consecutive quarters of decelerating revenue growth, I see potential stabilization around a 35% CAGR in 2024.

Investment Thesis

monday.com Ltd. ( MNDY ) is a work operating system that provides a collaborative platform for teams to manage projects, workflows, and tasks effectively. By offering a visual and intuitive interface, monday.com facilitates seamless communication, coordination, and organization, enhancing team productivity and project management.

monday.com reported its Q3 2023 results two days ago, and the message coming out of the company is clear: this is a growth stock. Indeed, I argue that despite several consecutive quarters of decelerating growth rates for monday.com, its growth rates should stabilize at close to 35% CAGR in 2024, which is undoubtedly attractive.

While I am optimistic about this company's prospects, it's important to note that its stock is not cheap.

Quick Recap

On the back of monday.com's Q2 2023 results, I said ,

All monday.com had to do was show that customers are still ready to use its services years after the ''digitalization'' movement began, which also happened to be the onset of the pandemic. And these outcomes unequivocally support my bull thesis.

Consequently, I continue to rate this stock a buy.

Author's work on MNDY

Since I wrote up that analysis, the stock has treaded water and ended down 3%. It's not a terrible performance, but it's not exactly what I'd expected to see.

However, despite MNDY stock's lackluster performance, I continue to believe that this stock is attractively priced.

monday.com's Near-Term Prospects

Monday.com is strategically positioned for growth through the expansion of its product portfolio, including the recent introductions of Monday Dev and Monday CRM. These additions signify a deliberate effort to broaden the platform's utility and attract a diverse user base.

The commitment to cultivating a robust marketplace is underscored by the emergence of vertical applications tailored to specific functions like CRM, work management, and development.

Notably, Monday.com exhibits a promising trajectory in the development of its Monday Dev product, positioning it as a significant player in this market segment. The encouraging growth is reminiscent of the company's earlier successes with CRM a year ago. While acknowledging the ongoing need for feature enhancements, the overall outlook for Monday Dev appears promising.

Finally, the company boasts a cash reserve exceeding $1 billion, providing ample resources for strategic initiatives. This equates to about 13% of its market cap being made up of cash with no debt.

{kind=link}

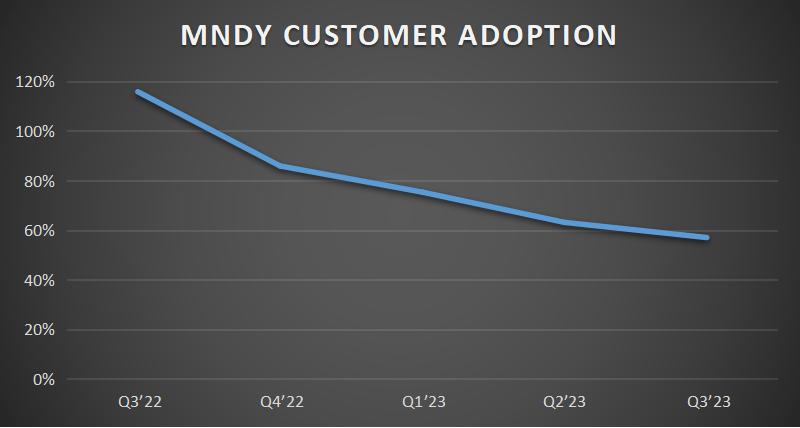

Now, let's discuss a pesky detraction from the bull case. monday.com Ltd.'s customer adoption curve is slowing down, even if for now it's still growing at a very rapid rate. This is a key indicator to remain watchful over going forward.

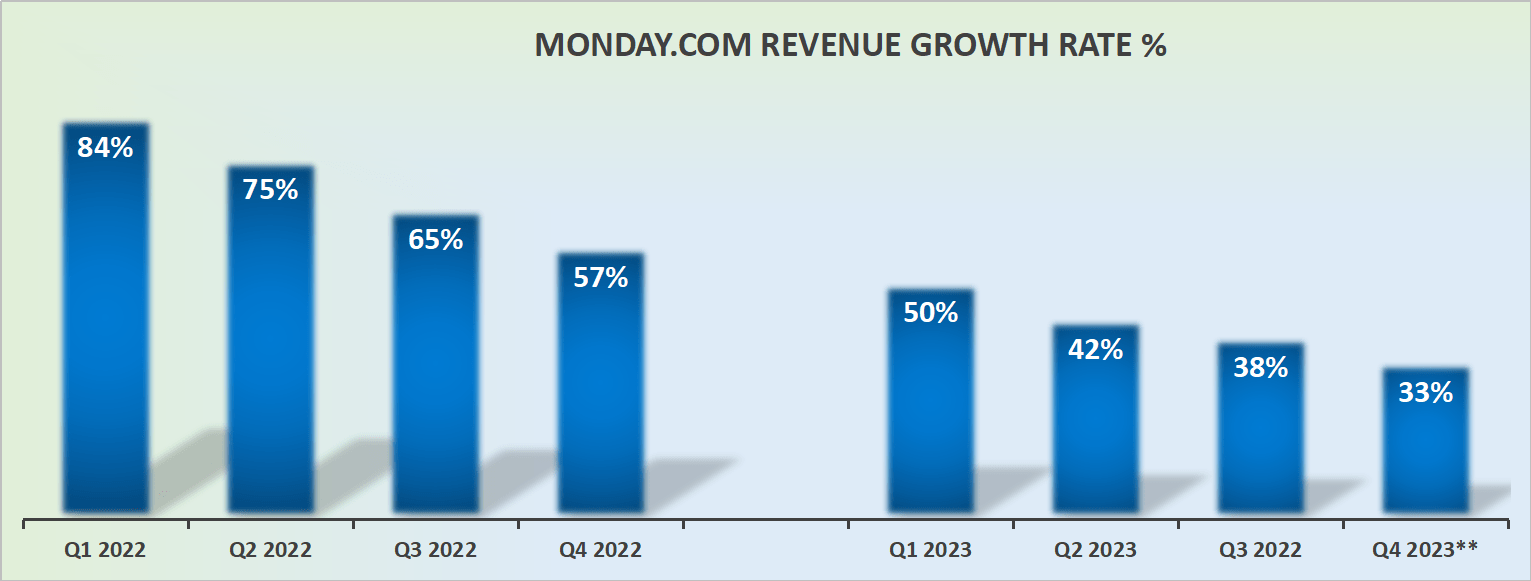

Revenue Growth Rates Rapidly Decelerating, With a "But"

{kind=link}

During monday.com's recent Q3 2023 earnings call , we heard about monday.com challenges that warrant consideration in assessing its future prospects.

One notable concern is the impact of macroeconomic conditions, introducing a level of unpredictability and potential pressure on net revenue retention. While the company anticipates retention trends to stabilize by the end of the year, the ongoing economic climate adds an element of uncertainty.

Additionally, there is a need to address the competitive landscape, especially in the realm of collaborative work management.

Also, the introduction of AI features, while promising, brings the challenge of staying ahead in a rapidly evolving technological landscape where AI capabilities are becoming increasingly common.

Now to get more specific, monday.com is a growth story. But, for now, it's facing numerous consecutive quarters of decelerating revenue growth rates.

However, I believe that as monday.com enters 2024, its comparables will meaningfully improve, allowing its revenue growth rates to stabilize as it probably grows in the 30% to mid-30s% CAGR range.

MNDY Stock Valuation -- Far From Cheap

monday.com's latest results guide to finish 2023 with approximately $50 million of operating profits. If we make a generous assumption that in 2024 its operating profits will grow by 30% y/y, this would imply that in 2024, monday.com would see about $65 million in operating profits. This would leave the stock priced at about 120x next year's operating profits.

One may argue that 30% CAGR is too pedestrian, that monday.com could, in fact, increase its underlying profitability by closer to 50% CAGR. This would still leave the stock priced at north of 100x next year's non-GAAP operating profits.

What's more, consider this: last year in Q4, monday.com reported $14 million of non-GAAP operating profits, whereas this year monday.com is guiding for about $9 million at the high end. Even if this figure comes in around $11 or $12 million, this would still be a decrease from the prior year.

Therefore, reinforcing that my estimate for 30% CAGR next year isn't perhaps as pedestrian as it appeared at first glance.

The Bottom Line

My analysis of monday.com leads me to maintain a positive outlook on the company's future, despite facing challenges such as decelerating revenue growth rates and competitive pressures.

The introduction of innovative products like Monday Dev and Monday CRM, coupled with a substantial cash reserve exceeding $1 billion, positions monday.com for strategic growth.

While acknowledging the need for vigilance regarding customer adoption and evolving technological landscapes, I believe the company's commitment to expansion and its potential for stabilized growth rates in 2024 make it an attractive investment.

Though stock valuation considerations underscore the importance of caution, the overall trajectory and strategic initiatives indicate that monday.com remains a compelling player in the collaborative work management space.

For further details see:

monday.com's Positioning For 2024: Stabilizing Growth Rates