MNDY - monday.com Stock: A Monster In The Making

2023-05-16 17:01:01 ET

Summary

- In Q1 2023, monday.com delivered a solid beat on both top and bottom lines on the back of strong demand for its Work OS platform and robust operating leverage.

- With revenues growing at a rapid clip, monday is quickly turning into a free cash flow machine. Furthermore, monday's management now expects the company to remain (non-GAAP) operationally profitable.

- While the post-ER bounce has left MNDY trading at the top end of its Stage-I base, I rate it a buy in the mid $100s with a preference for staggered accumulation.

Reviewing monday.com's Q1'23 Report

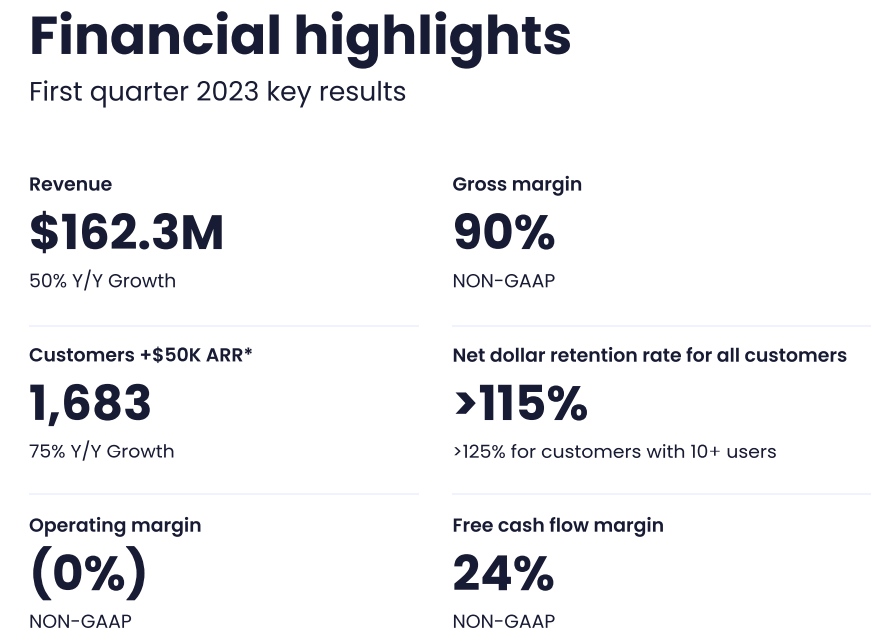

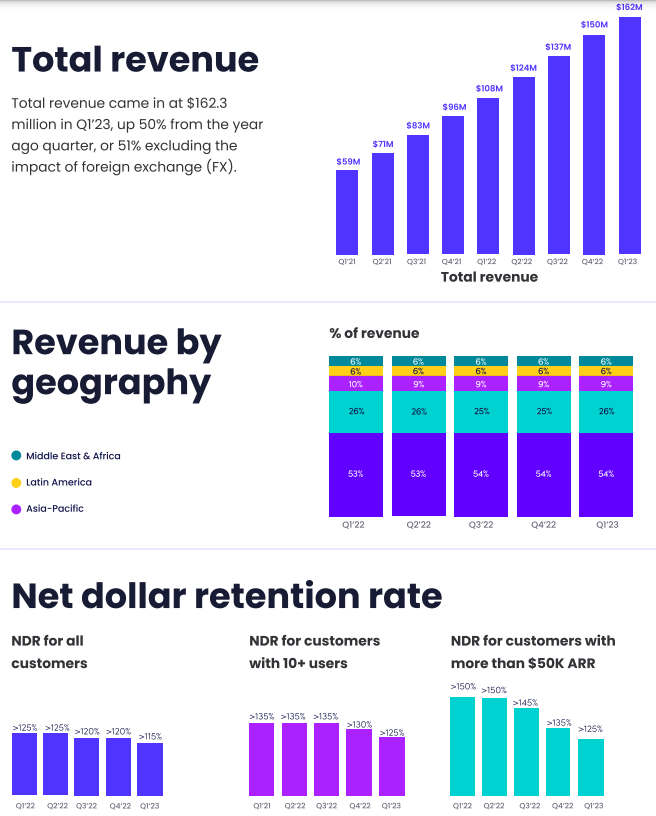

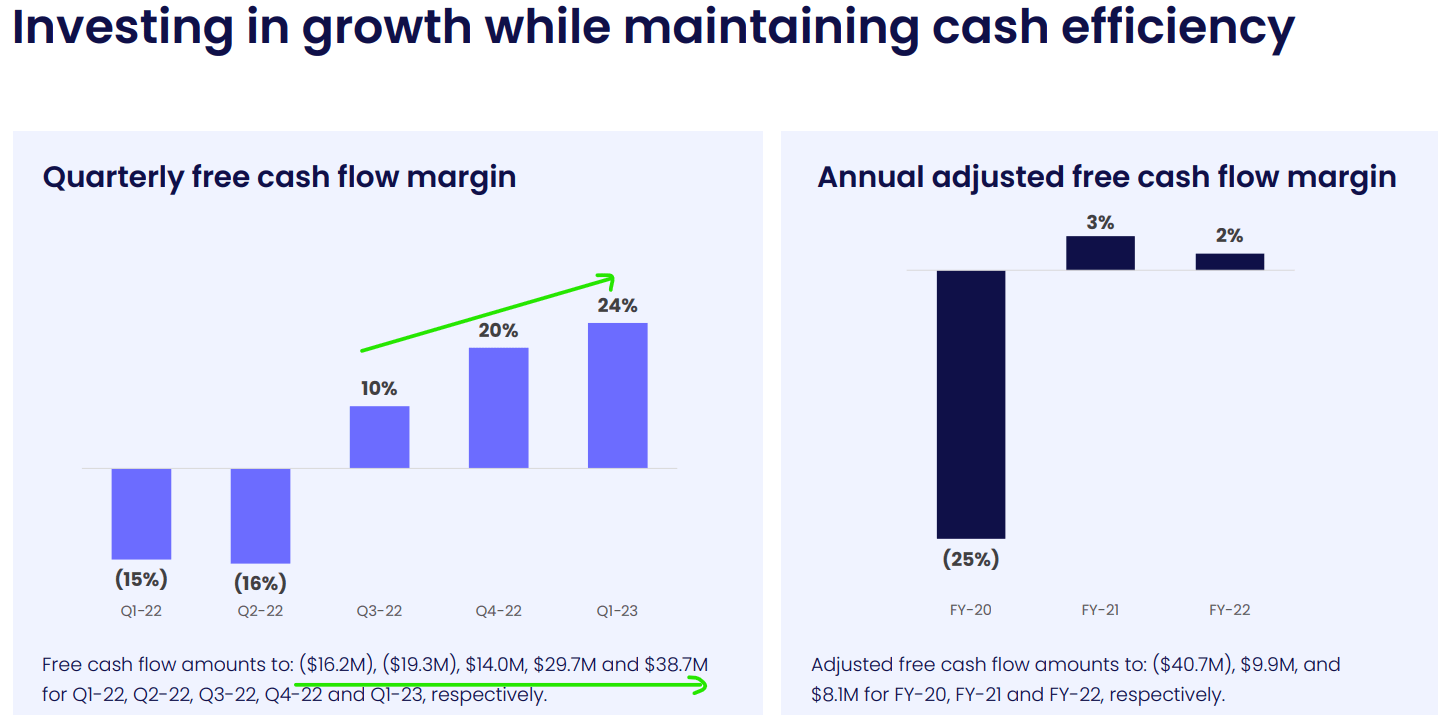

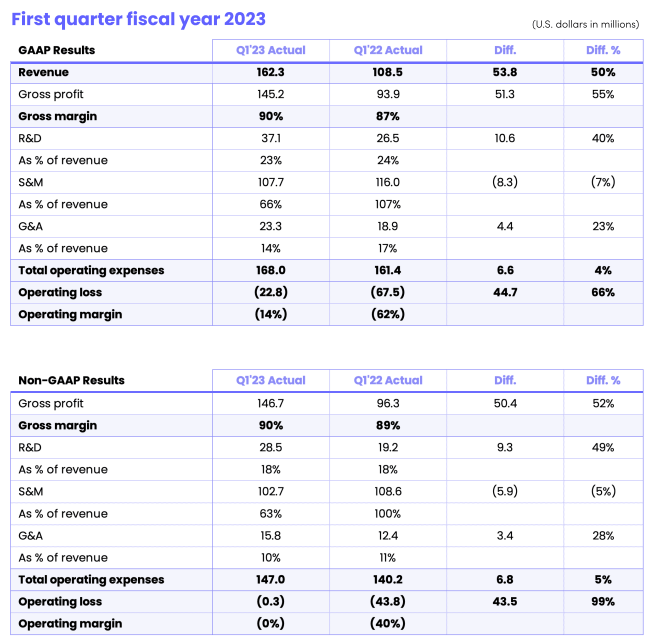

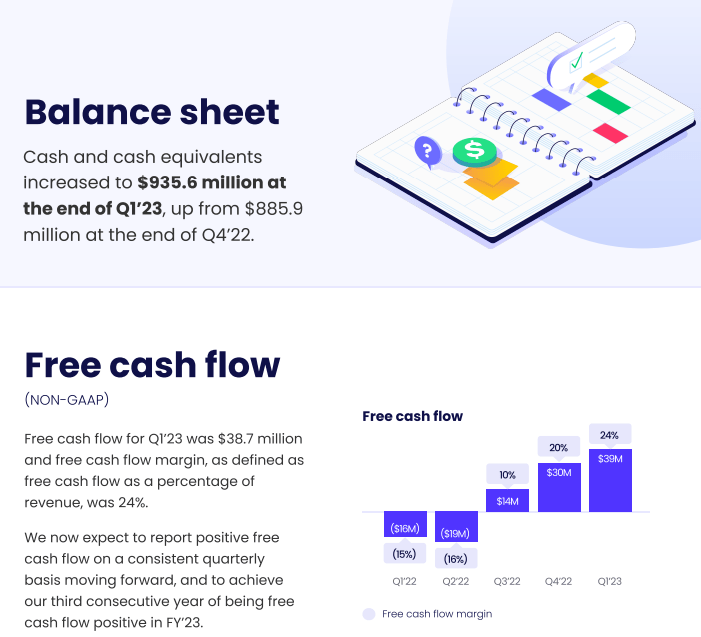

On May 15, monday ( MNDY ) reported a significant double beat for its Q1 2023 earnings, with quarterly revenues growing by 50% y/y to $162.3M and the Work OS platform company reporting a narrower-than-expected non-GAAP operating loss of -$0.3M. Furthermore, monday.com is turning into a free cash flow printing machine already, with adjusted free cash flow margin reaching +24% in Q1 2023, resulting in adjusted free cash flow of $38.7M.

{kind=link}

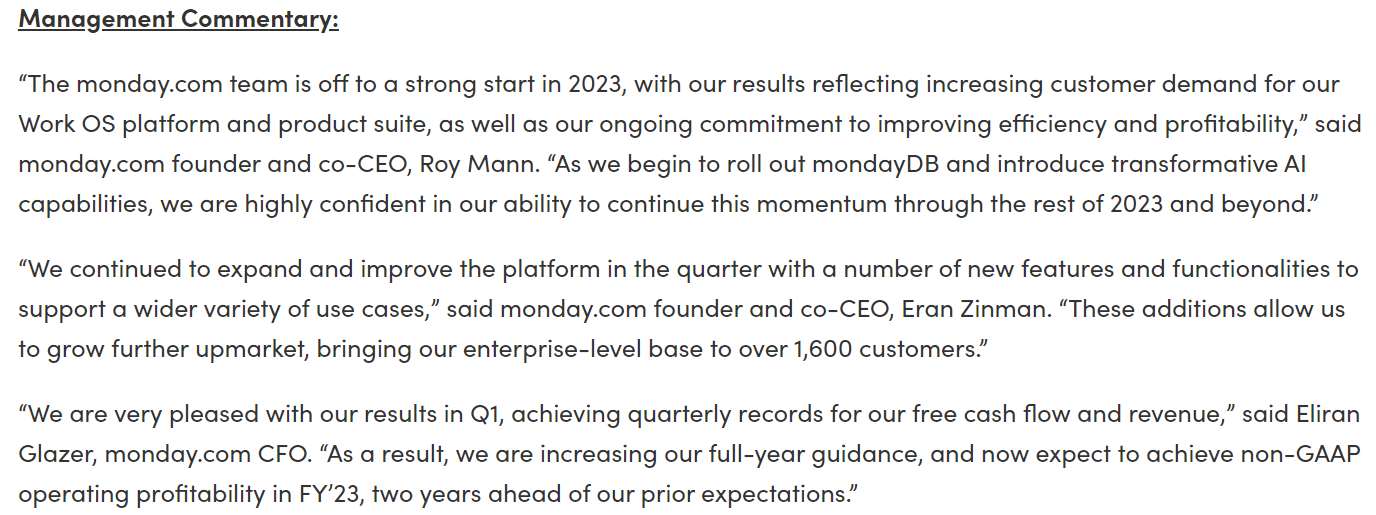

Management commentary on Q1 2023:

{kind=link}

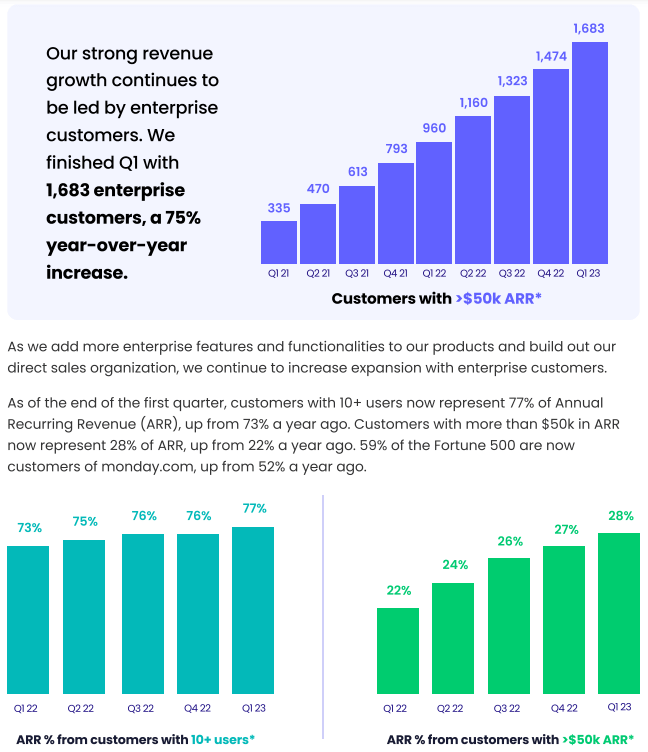

In the Q1 2023 earnings call, monday.com's management alluded to strong demand for its Work OS platform as the primary driver of these stronger-than-expected numbers. Amid persistent macro headwinds, monday's net dollar retention rates declined further in Q1'23, reflecting slower enterprise customer seat expansions. However, monday's gross retention rates remain stable, and the company is still adding new enterprise customers at a healthy clip.

{kind=link}

{kind=link}

Yes, monday's growth rates are decelerating, and sales cycles have gotten longer. However, monday's platform expansion, declining customer acquisition costs, and healthy retention rates are ample reasons to consider an investment in MNDY stock.

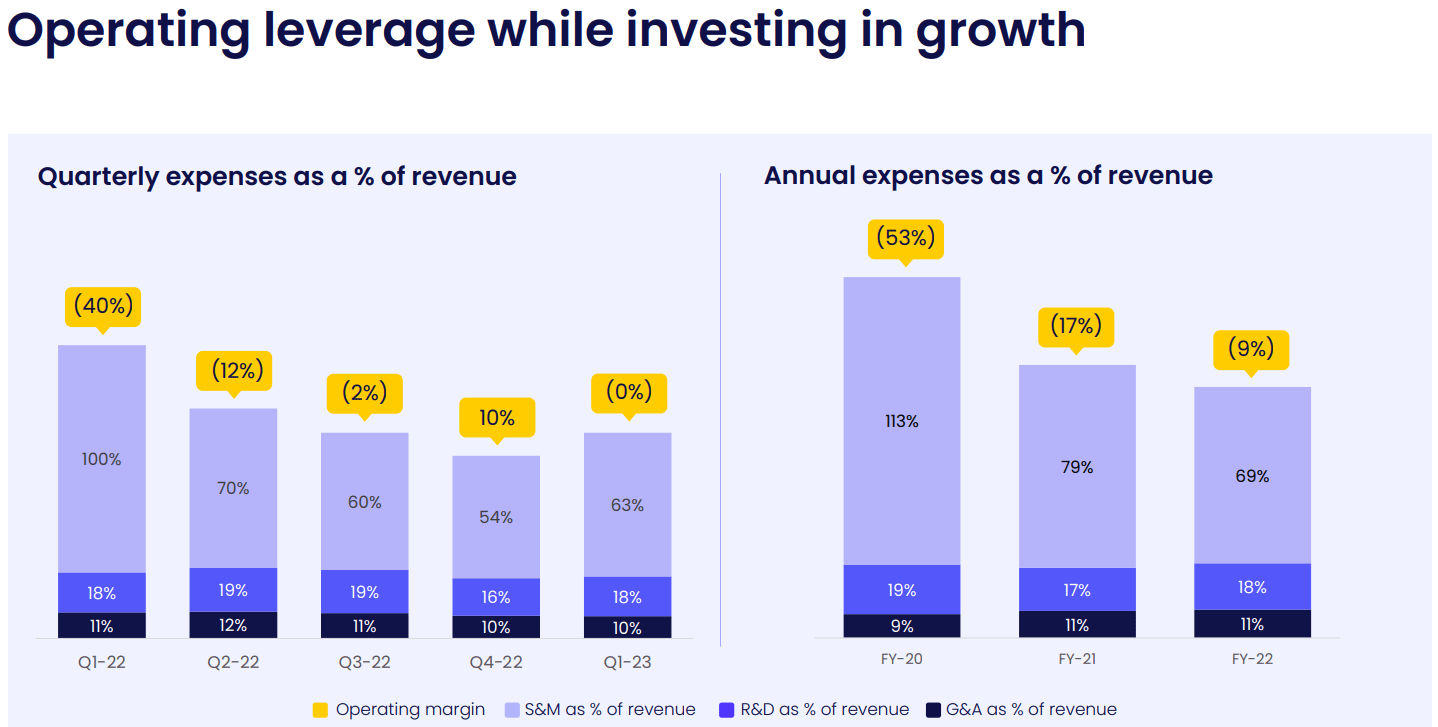

In addition to rapid revenue growth, monday is delivering robust operating leverage and quickly becoming a free cash flow generating machine. In Q1, monday's non-GAAP operating margin improved to -0% from -40% from a year ago period, with a significant drop in Sales & Marketing expenses as a percentage of revenue. Despite a drastic drop in S&M expenses as a percentage of revenues in recent quarters, monday's revenue growth numbers have remained robust, and I think this puts monday.com in rare air.

{kind=link}

{kind=link}

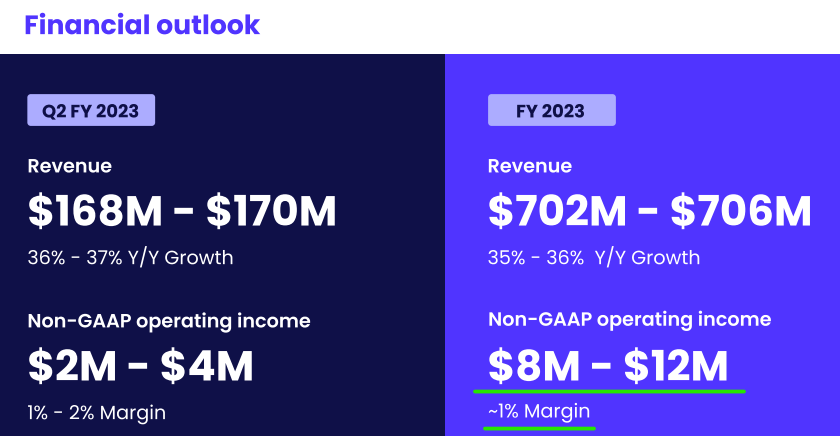

For Q1 2023, monday is projected to deliver revenues of $168-170M (growth of 36-37% y/y) and a non-GAAP operating income of $2-4M (1-2% margin). While this guide points to further growth deceleration, monday's management raising full-year revenue guidance to $702-706M (growth of 35-36% y/y) was quite positive (especially in the current macroeconomic environment). Furthermore, monday is now expected to maintain non-GAAP operating profitability going forward.

{kind=link}

That said, monday is far from being a consistently profitable business on a GAAP basis, as you can see below:

{kind=link}

However, with a cash position of $935.6M and no debt, monday's balance sheet is in great shape, and I see no liquidity problems brewing at the company. With monday set to add tons of cash to its balance sheet in upcoming quarters, it will be interesting to see what the management does with capital allocation.

{kind=link}

On the Q1 2023 earnings call, monday's management shared that the company's capital allocation policy is focused on internal product development (R&D). However, we may get some strategic acquisitions in the future that could accelerate monday's platform expansion (nothing in the pipeline).

{kind=link}

{kind=link}

Last year, monday launched several products atop its Work OS platform, including monday sales CRM, monday projects, monday dev, monday marketer, and mondayDB. While most of these products are still in the development phase or just getting into the hands of customers, the early adoption trends for monday sales CRM look impressive.

{kind=link}

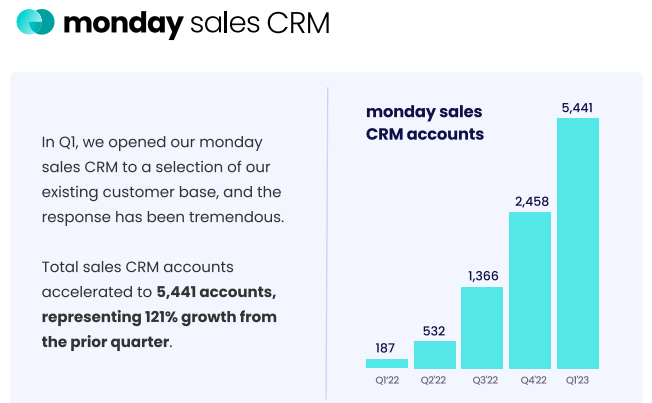

In Q1 2023, total sales CRM accounts soared to 5,441 accounts (+121% q/q growth) on the back of monday sales CRM becoming available to a select portion of its existing customer base during the quarter.

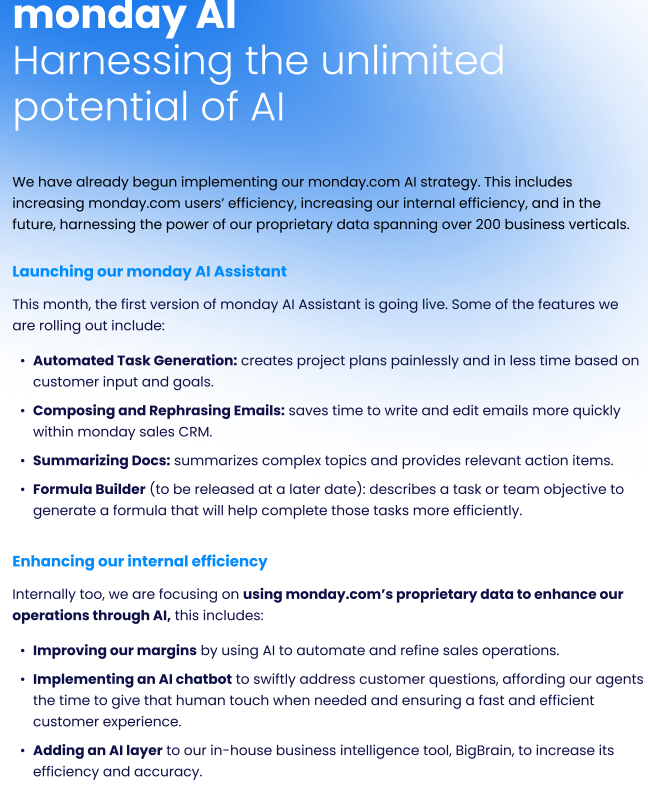

Considering its solid track record for innovation and massive customer base, I believe monday.com's Work OS platform expansion is a compelling cross-sell growth story. And monday's innovative DNA was once again on full display in Q1, with the company announcing monday AI :

{kind=link}

With the introduction of monday AI Assistant, I think monday has gotten itself ahead of the competition and poured cold water on the "AI will disrupt monday.com" argument.

Going into a potential economic recession (hard landing), monday's platform expansion looks very promising as organizations (small and large) are likely to look for bundled offerings to save on costs (consolidation). Despite facing macro headwinds, monday continues growing like a weed, and it's doing so while improving margins.

While monday is not yet profitable on a GAAP basis, it has turned operationally profitable on a non-GAAP basis, and it's looking like a robust FCF machine in the making. Having a cash cushion of ~$935M and no debt should allow management to remain aggressive during the impending downturn, i.e., capture more market share. Overall, I'm impressed with monday's financial performance in Q1 2023, and I'm already looking forward to Q2.

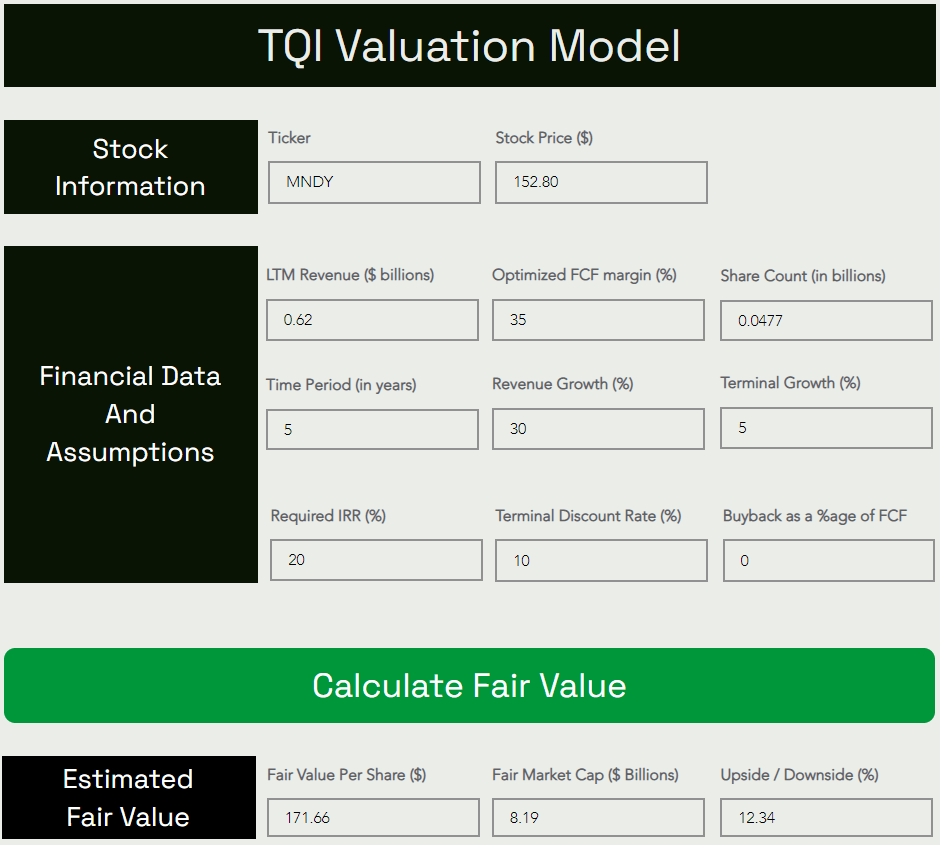

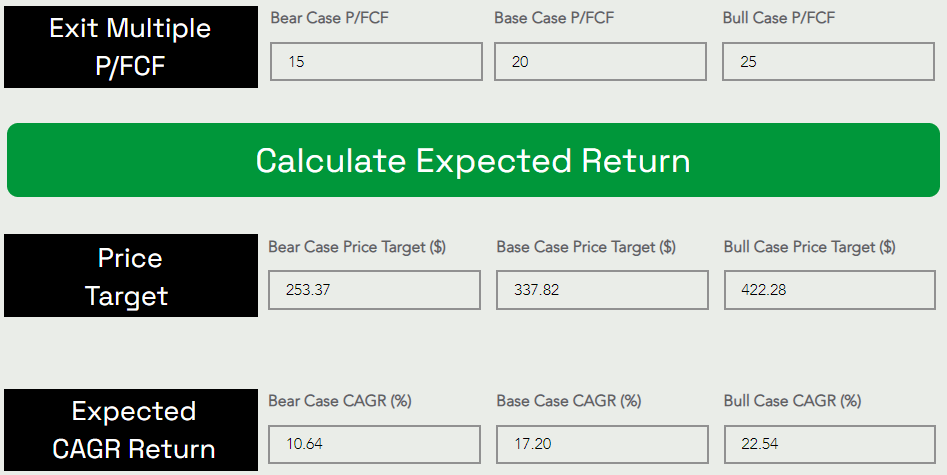

Here's my updated valuation for monday.com

{kind=link}

{kind=link}

A significant update here:

- Old FV estimate: $135.18, New FV estimate: $171.66

- Old Base case PT (5-yr): $323.99, New Base case PT (5-yr): $337.82

This upgrade is driven by the stronger-than-expected top and bottom line performance from monday.com in Q1 2023 and robust guidance for Q2 and the rest of 2023.

Concluding Thoughts

In my previous update on monday, I rated the company a buy in the low $100s with a preference for staggered accumulation. Here's what I said about MNDY's technical setup in December 2022:

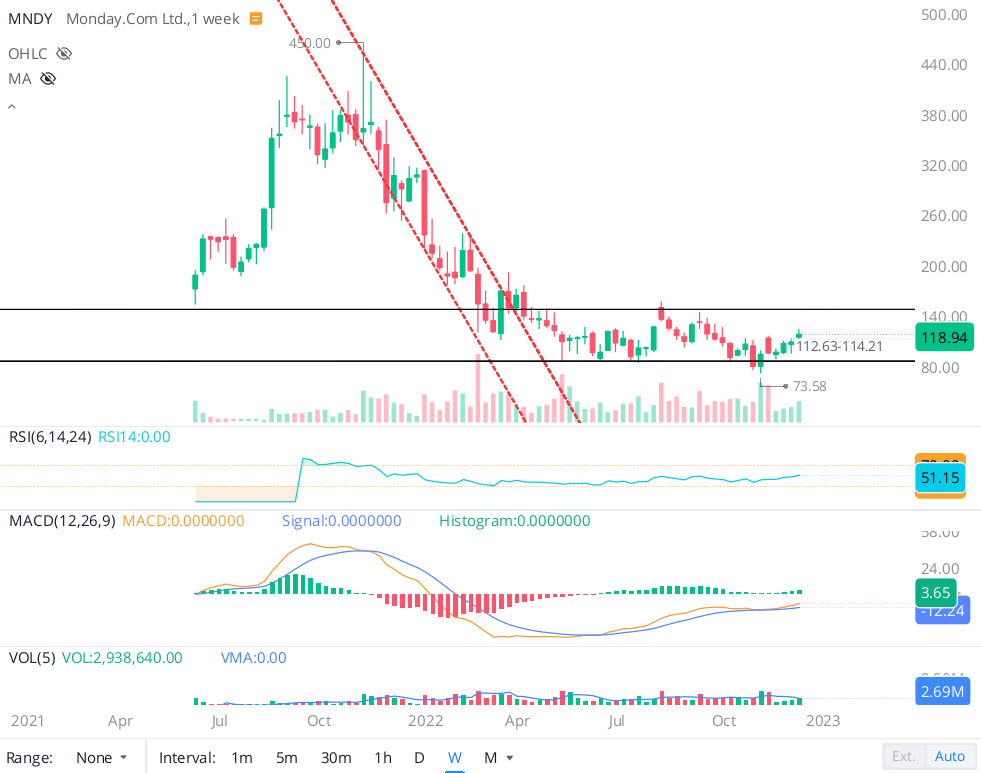

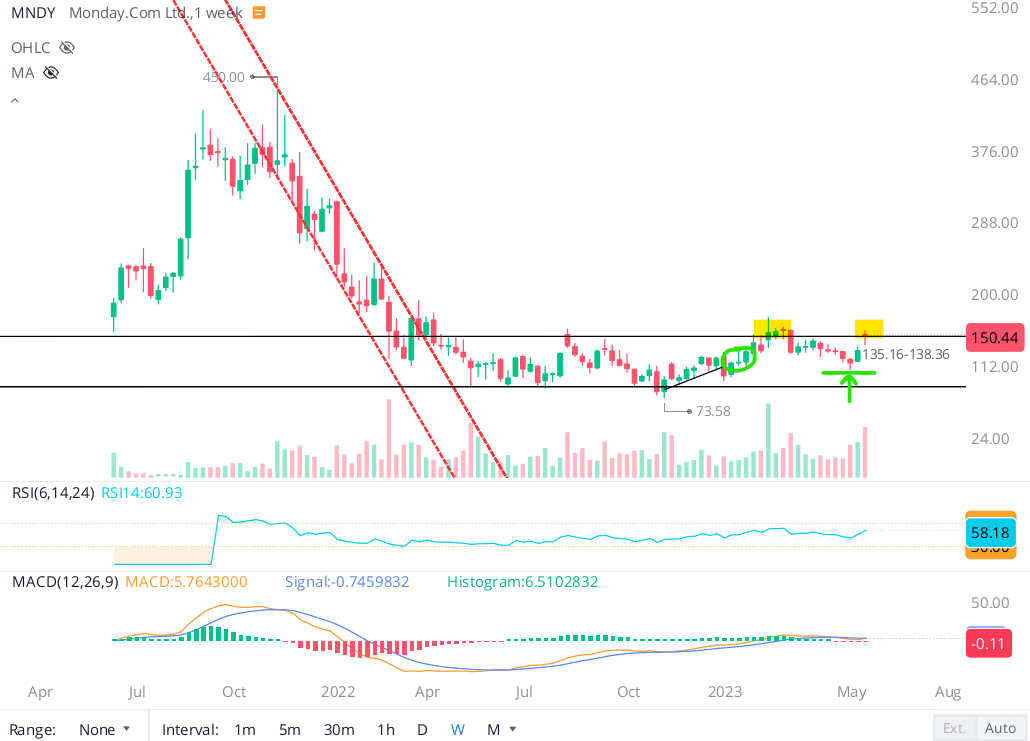

monday's relatively-short history as a publicly-traded company has been quite volatile, with the stock climbing from an IPO price of $155 to $450 in a matter of months during mid to late 2021, only to suffer a significant drawdown in 2022. From a technical perspective, monday's stock finds itself in a Stage-1 base formation.

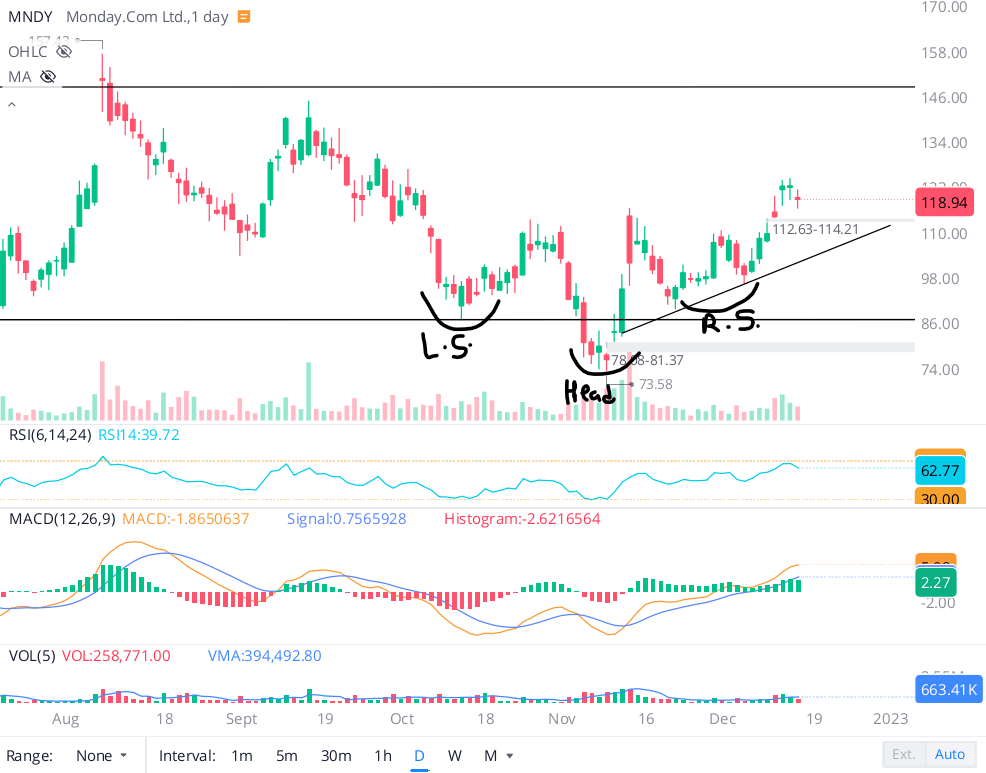

After hitting a new 52-week low of $73.58 per share in mid-October, MNDY has been rallying higher. On the technical chart, I see an inverse head and shoulders pattern, which could result in a move up to $150 in the near to medium term.

However, given the current macroeconomic backdrop, equities could come under pressure in the first half of next year. monday's stock is unlikely to be immune to the broad market conditions, and hence, we could very well see a move back down to the lower end of this base at the $80-85 range.

From a technical perspective, monday's stock is in a no trade zone. However, a long-term investment makes sense here due to strong fundamentals and a reasonable valuation. Hence, I like the idea of accumulating shares in this counter for the long run via DCA plans.

Source: monday.com Stock Is No Dot Bomb

{kind=link}

{kind=link}

And MNDY's price action has played out to toe with my previous expectations. After getting a rally up to $171 (higher than my $150 target), we got a pullback to $110 (low $100s) in recent months. And now, MNDY has rallied back up to $150.

{kind=link}

With the stock sitting at the top end of its Stage-I base, I'm somewhat cautious about the near-term price action here. My fair value estimate for MNDY now stands at $160 per share, and hence, I wouldn't be surprised if we were to get a breakout to the upside. Considering the risk/reward, I continue to remain bullish on MNDY stock in the mid $100s with a strong preference for staggered accumulation.

Key Takeaway: I continue to rate monday.com a buy in the mid $100s, with a preference for staggered accumulation.

Thanks for reading, and happy investing. Please share your thoughts, questions, or concerns in the comments section below.

For further details see:

monday.com Stock: A Monster In The Making