MNDY - monday.com Stock Is Receiving Serious Traction After Its Q4 Earnings Beat

Summary

- monday.com Ltd.'s Q4 earnings report could be the catalyst investors have been waiting for.

- The company's sustained hyper-growth trajectory is assisted by the successful integration of CRM tools and a synergetic marketplace.

- monday.com's hard-to-execute subscription-based business model is quite an achievement, especially if market fragmentation is considered.

- Although monday.com's income statement and price multiples might seem unfavorable, investors need to regard the business cycle and monday.com's operating cash flow.

- monday.com Ltd. is one of our top growth stock picks for this year.

monday.com Ltd. ( MNDY ) released its Q4 earnings report on Monday morning. The company's quarterly results beat analysts' estimates comprehensively, which caused MNDY stock to surge. Based on the stock's post-earnings market behavior, monday.com's latest earnings report has instilled confidence in investors who have presumably long-awaited a growth stock conducive market before recommitting to monday.com's stock.

Although monday.com's triumphant Q4 earnings report provides an indication of the company's trajectory, the question beckons: is it a good time to invest in monday.com's stock after a nearly 35% year-over-year drawdown? Well, there's only one way of finding out. Let's cover a few talking points to address our central question.

{kind=link}

Assessing monday.com's Operational Performance

Core Items Assessed

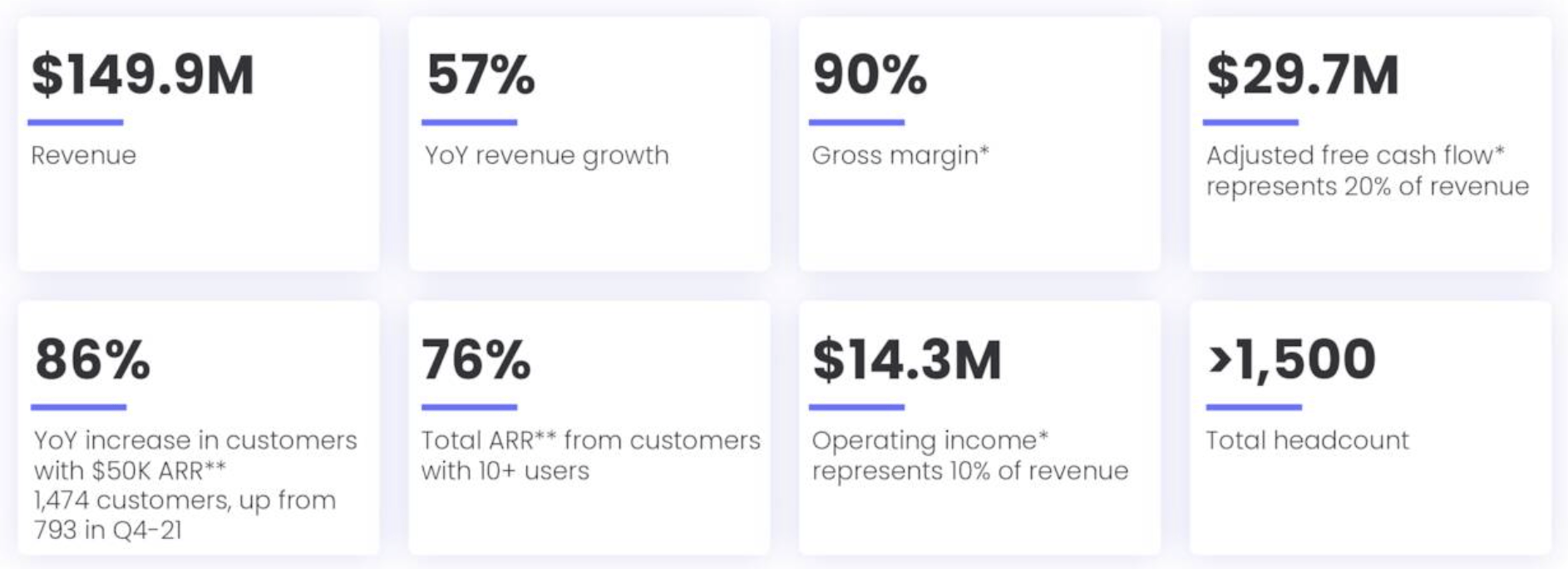

monday.com's exponential growth trajectory was reaffirmed by its Q4 results, which revealed a 57% year-over-year growth in revenue, suggesting the company's end-users outweighed the importance of monday.com's offerings over macroeconomic headwinds.

{kind=link}

It's critical to note that monday.com offers a high-quality core service with integrated features to bolster its appeal.

If we think about it anecdotally, m onday.com allows users to save an abundance of time by being able to plan their endeavors at a price starting at merely $10 per month. Moreover, m onday.com's offerings are organization-friendly. Sure, you can plan your day on Excel templates; however, integration and sharing add value to monday.com's product. As such, it is unlikely that the firm's users will void its products during turbulent macroeconomic circumstances, as the cost vs. benefit just makes sense.

Furthermore, monday.com is experiencing significant success with its CRM (client relationship management) and marketplace features. As mentioned before, "sharing" allows the company to charge a premium as it sets the tone for employee and customer relationship management. According to monday.com's Q4 results, the company's CRM segment finished 2022 with 2248 new active accounts , illustrating the domain's market potential.

Another aspect that has attached significant value to monday.com's business model of late is its marketplace. The company's marketplace accommodates third-party developers, allowing monday.com's end-users to scale their productivity according to their requirements. In the past year, monday.com has increased its total monetized apps to 61, broadening the firm's scope for cross-synergies and revenue growth.

Lastly, monday.com has achieved success with a full-on subscription-based business model, which is no easy task in a fragmented industry that hosts an abundance of free-to-use tools. Apart from Microsoft ( MSFT ) Office, most related tools are offered for free, with advertising revenue being the central goal of providers. Alternatively, templates are offered on a pay-per-download basis. Thus, we think monday.com's success with a subscription-based model in a saturated market should not be underestimated.

Considering Profitability

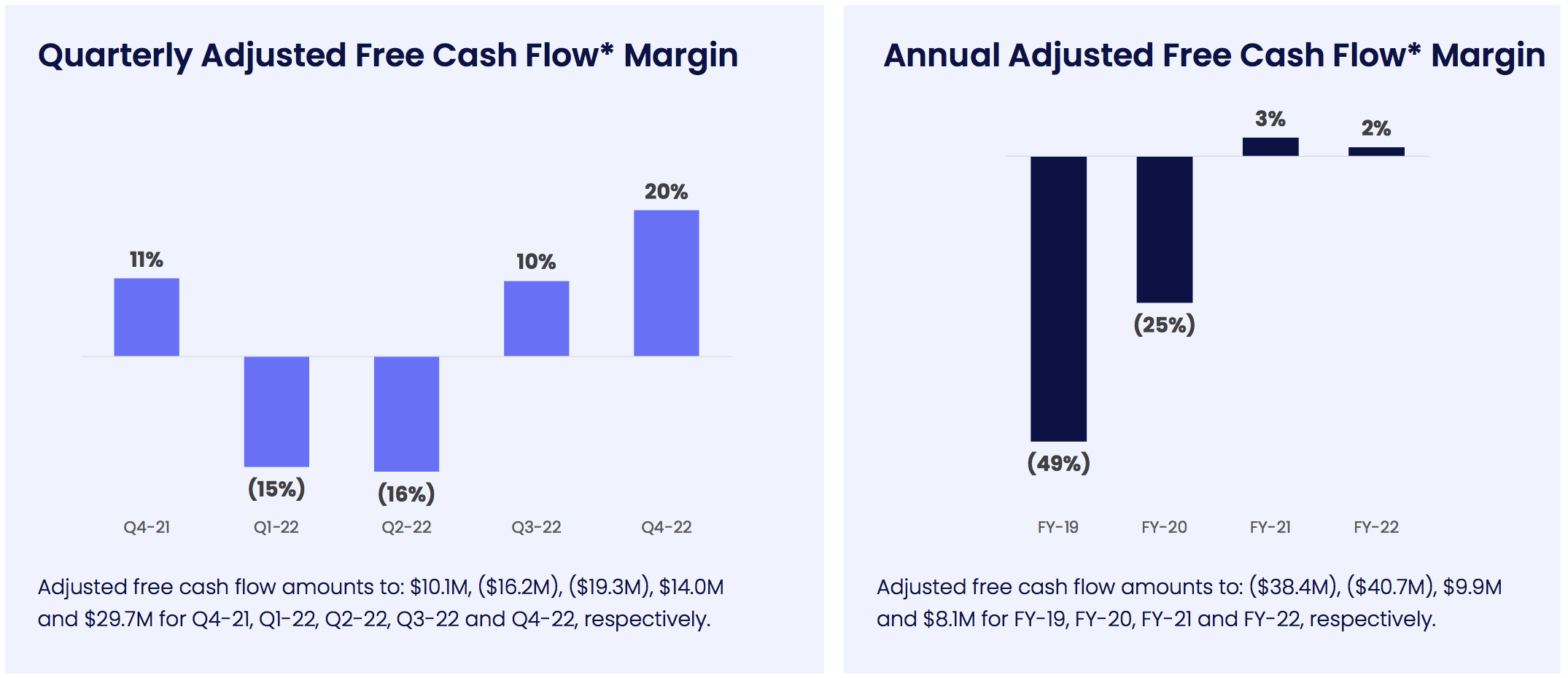

monday.com is an early-stage company that is arguably in its embryonic stage. Therefore, its $47,095 annual operating loss in 2022 should come as no surprise. In our opinion, investors should look past the firm's interim losses and toward its cash flow.

The Israeli technology company's operating cash flow speaks volumes, with two successive years of positive numbers conveying the monetary potential of monday.com's business model. Investors must consider that an income statement hosts various non-cash costs, which diminishes a growth-stage companies' profit & loss statements as they generally invest aggressively in research & development.

monday.com's 47.88% year-over-year CapEx growth suggests the company is on a heavy reinvestment spree to ensure it consolidates itself as an industry leader. Furthermore, a current ratio of 3.10 indicates the firm's balance sheet is robust, leading us to believe that monday.com will use its dry powder effectively and pass through value to its shareholders when the time is right.

{kind=link}

Critical Risks To Consider

monday.com possesses two identifiable risks that could alter the stock's year-to-date momentum.

Firstly, the firm's recent financial success has onboarded a severe operational risk. monday.com's robust earnings will probably encourage competition, resulting in an abundance of new market entrants. Moreover, the company operates in an industry with low barriers to entry, meaning it needs to spend aggressively to stay ahead of the eight ball, which could diminish its profit and loss statement for an extended period.

Furthermore, as a non-profitable company that hosts a stock with significantly elevated price multiples , it's safe to say that monday.com can be classified as a growth stock. Growth stocks have started the year sharply as inflation has moderated, and 2023's global economic outlook has arguably settled better than most anticipated. However, growth stocks are extremely sensitive to a wobbly economy; therefore, monday.com's stock could sink into the abyss if the primary economic themes experienced in 2022 had to reoccur.

{kind=link}

Final Word

Although market-related risks remain, monday.com's Q4 earnings beat could send its stock into the stratosphere. The company is scaling at a rate of knots with the successful integration of its CRM and marketplace offerings providing additional embedded growth.

Monday.com operates in a low-barrier-to-entry industry. Nonetheless, its managerial value additivity and aggressive reinvestment strategy allowed it to achieve positive operating cash flows with a hard-to-execute subscription-based business model.

The company's lack of profitability and its stock's elevated valuation multiples poses risks. However, a risk-on stock market might reward investors for onboarding excess risk.

- Buy rating for monday.com Ltd. assigned with an indefinite horizon.

For further details see:

monday.com Stock Is Receiving Serious Traction After Its Q4 Earnings Beat