MDLZ - Mondelez: Fantastic Consumer Goods Business But Expensive

Summary

- Mondelez is a consumer goods business focusing on snacks. The company operates across 160 countries, owning brands such as Oreo.

- Our view is that economic weakening will not materially impact growth, although it will continue to pressure gross margins due to supply-side issues.

- The business is positioned well competitively due to strong brand recognition and investment into ESG.

- Financials stack up well, with growth returning in recent years and continued improvement in efficiency metrics.

- Mondelez is more conservatively financed than its peers and has a better growth/profitability ratio. Based on our valuation, there is only a 3-8% upside, so we consider the stock a hold.

Company overview:

Mondelez International, Inc. (MDLZ) is a global producer, marketer and distributor of snack foods and beverages. Its product line includes biscuits (cookies, crackers, and savory snacks), chocolate, gum and candies, cheese and grocery items, and powdered beverages. The company sells its products through various distribution channels.

The company's snack brand portfolio includes Cadbury, Milka, and Toblerone chocolates; Oreo, belVita, among others.

Mondelez has grown very well since it was formed in 2012, when the initial incarnation of Kraft was split. As a consumer goods ((CG)) business, the company targets organic growth at the top end of inflation targets, supplementing this with M&A activity.

As part of prior asset realizations, Mondelez holds c.5.33% in Keurig Dr Pepper ( KDP ) (.2.4BN) and c.19% in JDE Peet's ( JDEPF ) ($2.9BN) ( Source: Tikr Terminal ). This has the opportunity to cause some degree of fluctuation in the business' results, but in aggregate has been beneficial, earning unrealized gains.

Having mentioned realizations, we should note that Mondelez has agreed to sell its Gum Brands (Including Trident) for $1.35BN, with an implied valuation of 15x EBITDA . This is based on an overarching strategy to transition their portfolio towards higher growth areas.

Mondelez's share price has performed incredibly well over the last 10 years, heading sharply in one direction. Markets have likely been attracted to the successful execution of their long-term strategy and the quality of brands in their portfolio.

With economic conditions continuing to weaken and inflation remaining high, investors are increasingly looking for a safe haven for their money. Our view (See write up on Unilever (UL)) is that consumer goods businesses can perform extremely well during such times, as demand remains sticky. The purpose of this paper is to consider the overarching attractiveness of the business in 2023 relative to other CG options and to identify if there are any unique attributes that could suggest Mondelez will outperform long-term. We will do this by considering quantitative and qualitative factors, beginning with an analysis of how economic conditions impact such businesses.

Economic consideration:

Demand for goods began to slow in 2022, partially due to a hangover from lockdown and post-lockdown spending binges. The biggest driver in our view has been the rise of inflation, which increased in 2022. A decade of aggressive monetary policy, energy price disruptions and supply chain problems have all contributed to this. Businesses have suffered with margins tightening, as their costs have increased, and employees have sought pay rises. Consumers have equally suffered with income deteriorating and a reduction in discretionary income.

Central bank policy has been to raise interest rates, with the intention of cooling demand. The problem with this is that the contributing ratio of supply and demand is weighted materially towards supply, due to energy prices (Russian invasion of Ukraine) and supply issues (Ramping up of production following lockdown), which is unusual when compared to prior inflationary periods. Our view is that this is why inflation has been slow to come down, with it only now looking to reverse.

Our outlook is that 2023 will be more of the same, with interest rates likely ticking up a further 0.25-0.5%. This will be to put the final nail in the inflationary coffin, with the view to returning to a sustainable level of inflation by Q4'23 / Q1'24. In the meantime, however, many businesses and almost every consumer will struggle to varying degrees, potentially triggering many recessions globally.

Naturally, this has caused many businesses to underperform in recent quarters, with the stock market reacting in kind. The situation with CG businesses is that they usually (but not always) sell goods which are inelastic in demand. This means that as prices go up, total income does also, even if the quantity of sales fall. The reason for this is that consumers generally cannot forego the expenditure, either because it is required, such as cleaning products, or because it is a small enough expenditure that they are willing to incur it anyway.

In the case of Mondelez, our view would be that the business specifically sells goods in that second segment. Oreo biscuits in the UK, as an example, have increased from £1 to £1.10. 10p is not a deal breaker for the average household. Therefore, Mondelez should be able to pass on costs successfully, potentially even improving margins.

The only problem comes with substitution. Consumers could look to find areas to cut costs, which leads to buying supermarket-branded goods rather than the "branded" products. As an example, consumers can get double the chocolate vs. a Mondelez brand for a lower price.

Cadbury Chocolate (Tesco)

Supermarket-branded chocolate (Tesco)

Funnily enough, at the time of checking this the Tesco Chocolate bar was sold out.

We must also consider supply issues. With supply chain problems, businesses are experiencing greater costs in order to produce their products. This has the potential to cause margin contraction and delays in being able to realize inventory.

Our view is that being able to pass on costs is more important that supply chain issue impacts, the reason for this is that the former shows strength in the brand, whereas the latter is a short-term issue which is difficult to avoid.

When looking at Mondelez's performance, we observe an impressive 6% growth in revenue, suggest that they have been able to successfully increase prices. This said, GPM has fallen 3%, which for a business of its size, is very poor. Management have attributed a large chunk of this to a mark-to-market loss on derivatives, with adjusted GPM only being down 1.2% ( Source: Q4'22 Mgmt. Commentary ). Derivatives aside, margins have declined due to raw materials and transportation costs increasing.

Mondelez GPM snapshot (TIkr Terminal)

Overall, economic conditions display the conditions necessary for a CG business to outperform. Although growing GPM is extremely difficult, our view is that strong growth and minimizing margin contraction is a sign of a great performance. For Mondelez, this will likely be the case in FY23 should things continue in a similar vein and assuming no further one-off expenses, but FY22 feels like wasted potential to show a robust operating model.

ESG:

ESG factors are becoming increasingly important in the consumer goods industry for several reasons:

- Consumer Demand: Consumers are becoming more environmentally and socially conscious, and they are increasingly seeking products that align with their values.

- Long-term Business Performance: ESG factors can have a significant impact on a company's long-term financial performance. For example, companies that are sustainable and have strong labor practices are likely to be more efficient and have lower operational costs.

- Risk Management: ESG factors can also pose risks to companies in the consumer goods industry, such as reputational damage from environmental incidents or labor disputes.

- Investment Considerations: ESG is becoming an increasingly important factor for investors when making investment decisions. Investors are recognizing that companies with strong ESG practices are more likely to perform well over the long-term and are more attractive as investment opportunities.

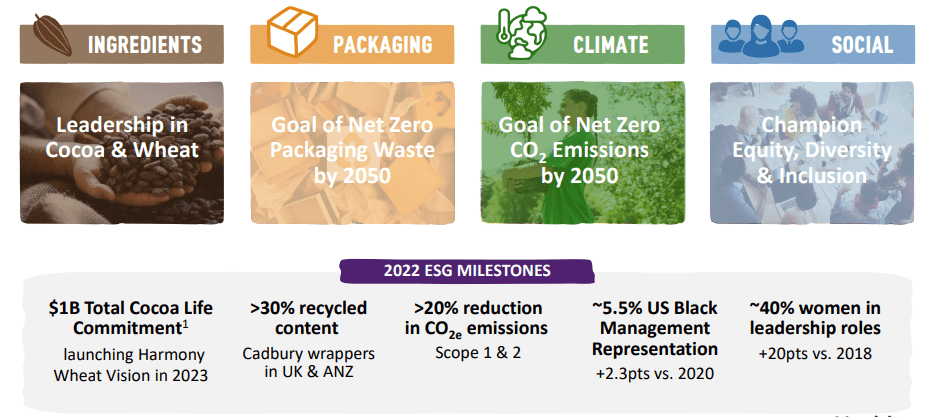

As the below shows, Mondelez is committing to a host of ESG causes across the spectrum. We are slightly disappointed by how far out they have set their goals, however.

ESG initiatives - Mondelez (Q4 Investor pack)

{kind=link}

Competitive positioning:

Mondelez operates in a highly competitive industry with major players such as Mars, Nestle ( NSRGY ), and Hershey's ( HSY ). However, the company's strong brand portfolio and geographic diversity give it a competitive advantage over its peers. Mondelez International has also been successful in expanding its product offerings to include healthier snacks, which has helped it capture a larger share of the health-conscious consumer market.

This is an important innovation as there is a growing movement towards being more health conscious and avoiding unhealthy aspects of life. We could have easily seen Mondelez avoid any actions here, as its goods are not exactly close to the healthy category, but this shows clear determination to innovate in the face of threats.

Mondelez International operates in over 165 countries, which gives it a competitive advantage over other snacking companies that are more focused on a specific region. This geographic diversity allows the company to mitigate the impact of local market conditions and currency fluctuations, as well as take advantage of growth opportunities in new markets.

Financials:

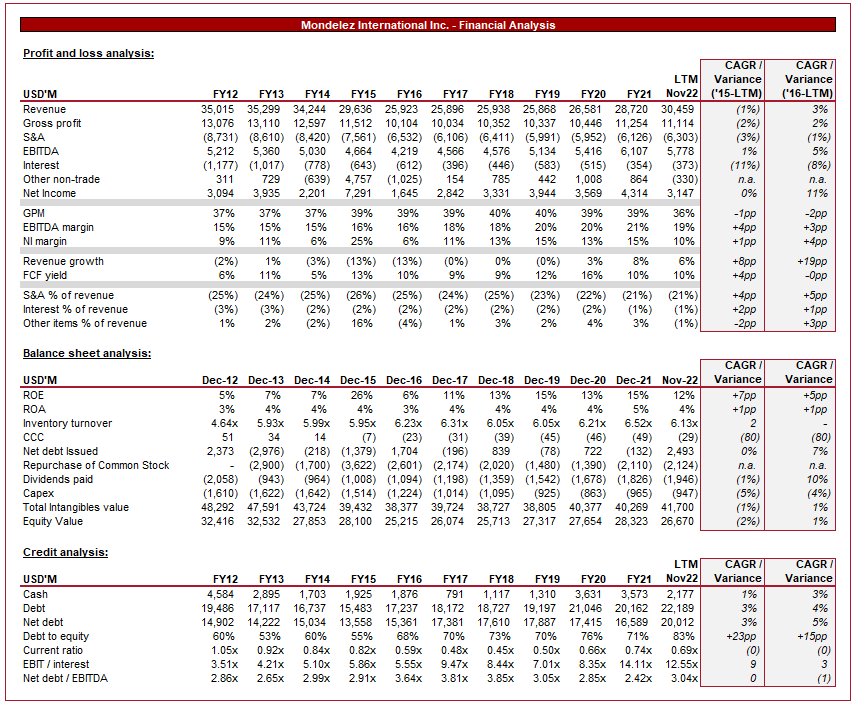

Mondelez's financials are a story of 3. We have FY12-FY16, a decline culminating in the deconsolidation and spin-off of its coffee business . FY16-FY19, the stagnation as focus is turned on margins and operational improvements. Finally, FY20 to present, the revival. Historically, the business has been able to achieve organic growth, but struggled to translate this into revenue, and importantly attractive margins. Management has systematically addressed each item, with a business now that looks to be growing, while achieving impressive profitability.

What we observe is that net income improves across the historical period (With LTM pulling back), reflecting the fruits of Management's strategic shift. This is important as investor returns from a CGs business is materially tied to its profits, which drive distributions. The stock price is probably not going to compound in the high double digits. The issue with Mondelez has always been with achieving sustainable revenue growth.

MDZL - Financials (Tikr Terminal)

{kind=link}

Revenue revitalization stems from Mondelez's shift towards growing businesses and exploiting opportunity segments. Their biscuit / chocolate segment has performed extremely well, led by Oreo, and is the core of their long-term vision for the business. We see this with the types of businesses acquired by the Group. Management believe these brands will already contribute over 1% growth alone.

M&A deals (Q4 investor pack) Growth potential (Q4 Investor pack)

Both EBITDA and NI have improved well in the second half of the decade, as Management sought to produce market competitive profitability. This involved focusing on becoming more efficient and cutting unnecessary expenses. S&A costs has fallen as a % of revenue almost consecutively since FY15, inventory turnover has increased and the business's CCC has fallen significantly.

Moving onto the balance sheet, Mondelez's overall return is very good, with a ROE of 12%. Much of the value of the balance sheet relates to goodwill, which usually means the business has no real hard "asset" value in a conservative sense. However, given the quality of the brands, supported by the sale of Trident at 15x, we are not concerned by this dwarfing equity value.

The business has maintained attractive, sustained dividends to shareholders across the last 10 years. Further, a corresponding number of shares are repurchased annually as well.

Looking from a credit perspective, we are not concerned by debt ticking up across the historical period. The reason for this is that it has remained flat as a ratio of EBITDA, at around 3x. In conjunction with a debt-to-equity ratio of 83%, the business is in a healthy place. Importantly, the business should be able to finance further expansion without taking on expensive debt.

Overall, we are very impressed with Mondelez's financials, especially in recent years. Margin contraction is certainly not good, but our view would be that this is only short term and could bounce back to the c.38% level by '23/'24. Based on our qualitative analysis of the business, our view is that the business can grow at mid-single digits in the medium term, with the optionality for large M&A activity.

Outlook:

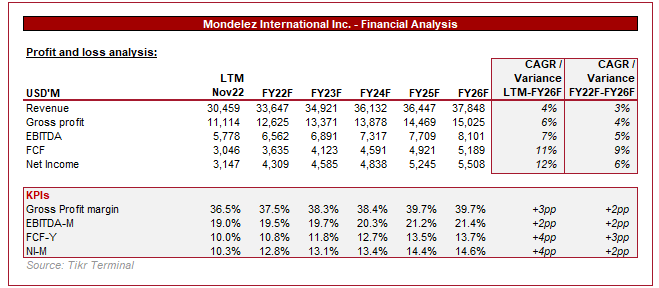

MDLZ - Analyst consensus forecast (Tikr Terminal)

{kind=link}

Analyst forecasts support our view of the business, which is continued growth at a rate above the sustainable inflation level. Analysts see margins continuing to improve by several percent across the board. This will have to be driven my high margin products as the business can only gain so much from efficiency.

Peer comparison:

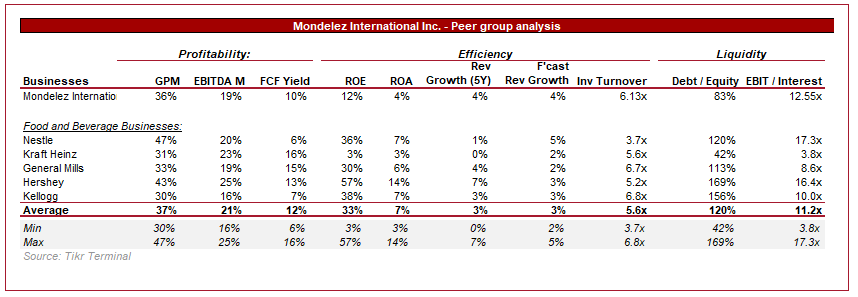

Peer group analysis (Tikr Terminal)

{kind=link}

When compared to the average of our chosen peer group, Mondelez appears to be an average performer in the food and beverage industry, although slightly more efficient.

What is more important for us is the split between profitability and growth. Those with growth >3% forecast, such as Nestle and Kellogg ( K ), lack the profitability of peers (<10% FCF-Y). Conversely, those with >12% FCF-Y, Kraft ( KHC ) and General Mills ( GIS ), have <3% growth forecast. Therefore, investors looking for a balance of both, while being conservatively financed and efficient, will find value with Mondelez.

The only exception is Hershey, which looks incredibly attractive and outperforms Mondelez, although has used far more debt to achieve this.

Valuation:

Peer group valuation (Tikr Terminal)

Presented above is the valuation of the businesses mentioned prior. Straight off the bat, Hershey is valued at a market-leading premium, reflecting the superiority identified previously.

Our view is that Mondelez should trade at a premium to its peer average due to the healthy mix between profitability and growth. It should also trade at a premium to its historical average as the business now has improved growth. This suggests a minimum valuation of c.17x, with our calculation suggesting 20-21x is a fair valuation. The EBITDA multiple is based on an average of the high performing peers and the DCF is based on the assumption of growth in the region of 3-5% and GPM returning to 38%.

This suggests minimal upside, in the region of 3-8%. Given the current level of market weakness and margin for error, this is not a substantial enough upside to attribute a buy rating.

Conclusion:

Mondelez is a fantastic business, with a strong portfolio of brands. The business has focused on transitioning the portfolio towards growth and has earned fruits for its labor. Our view is that current economic conditions will not have a material impact on the business, only short-term headwinds through marginal GPM contraction. Our assessment of growth is that Management has made the necessary decisions to ensure this is far more sustainable going forward. Our only issue currently is that the stock is slightly expensive and so we rate the stock a hold.

For further details see:

Mondelez: Fantastic Consumer Goods Business But Expensive