UL - Mondelez: Still More Attractive Than Peers - I Am Buying

2023-12-05 01:41:55 ET

Summary

- Mondelez International's shares are attractive compared to peers, with potential annual returns of approximately 13%.

- The company's exposure to faster-growing verticals, regional diversification, and strong management make it a compelling investment.

- Mondelez has been able to keep volumes positive despite price increases, demonstrating its strong product portfolio and execution.

Investment thesis

I maintain my “Buy” rating on Mondelez International, Inc. ( MDLZ ) as the shares continue to look attractive when compared to peers, following the company’s remarkably strong Q3 performance and favorable long-term positioning. From a current share price of around $71, investors are poised for annual returns of approximately 13%.

While the likes of PepsiCo ( PEP ) and Coca-Cola ( KO ) are the face of the consumer staple industry and do not get me wrong, I very much like these as well and own both in my portfolio, I believe Mondelez is much more compelling today due to its exposure to faster-growing verticals, excellent regional diversification, and terrific management team. As a result, the company is poised for strong growth and should outgrow most of its consumer staples peers.

Overall, Mondelez stands out as a premier choice within the consumer staples sector. The company boasts a diverse array of globally recognized multi-billion-dollar brands alongside an extensive collection of local and regional gems that thrive in their respective markets. This dynamic collection not only affords Mondelez exceptional pricing power but also positions it strategically to navigate current inflationary challenges by leveraging price adjustments while maintaining impressive volume growth, as we have witnessed over recent quarters.

This is where the company sets itself apart from the competition. Unlike many of its peers who have seen volumes in negative territory due to the price increases, Mondelez has been able to keep volumes positive over the entire period of price increases, which is a testimony to its very strong product and brand portfolio and management’s excellent execution.

Furthermore, Mondelez has successfully implemented a forward-thinking approach, focusing on biscuits and chocolate, two high-growth product categories within the snacks industry. This strategic emphasis aligns the company favorably against competitors, ensuring sustained momentum throughout the decade.

In addition, geographical resilience is a key strength, with Mondelez's exposure extending strategically into emerging markets. This advantageous positioning is underscored by the latest earnings report, reflecting the company's ability to sustain growth rates surpassing industry standards. For a full analysis of the company, I recommend reading my initial article on the company, which can be found here .

Also, Mondelez's management exhibits a keen understanding of market dynamics, contributing to the acceleration of the company's growth trajectory in recent years. Notably, this well-crafted strategy is anticipated to yield a commendable revenue CAGR of 4-7% in the coming years.

On top of this, management is also committed to growing its dividend in line with EPS growth, which should result in very respectable dividend growth accompanied by buybacks. As a result, Mondelez presents a very compelling investment case, and I believe that from current levels, investors remain poised for market-beating returns, proving that no high-risk and storytelling technology company is needed to achieve this.

In this article, I will discuss some of the most important developments since my last article and closely examine the most recent quarterly results to update my financial projections and target price.

GLP-1 drug adoption caused downward pressure on Mondelez's stock, but the “panic” is an overreaction

I have aggressively been buying Mondelez stock in October as shares came under pressure following some temporary investor “panic” on the news of obesity drugs from the likes of Novo Nordisk ( NVO ) and others impacting consumer appetite and potentially calories consumed. However, this seems to be a complete (premature) overreaction, so let’s deal with this first off.

While I am not about to say that these drugs don’t represent a risk to Mondelez’s business, these are overstated so far. I discussed this matter in depth in my most recent Starbucks ( SBUX ) article, and this is what I said : (Starbucks-specific details have been taken out)

The GLP-1 weight loss drugs have been an important subject of discussion in recent months when it comes to food and beverage companies. There has been some slight panic in the markets as claims are circulating that these incredibly popular weight loss drugs could lead to lower calorie consumption as a result of a lower appetite, impacting demand for food and beverages.

The GLP-1 agonists that Novo’s Wegovy is based on were originally developed to treat type 2 diabetes, but in addition to controlling blood sugar levels, they affect hunger signals to the brain, resulting in users feeling full for longer, making it an excellent weight loss drug.

The drugs have seen a very positive response in recent quarters and quite strong adoption. This has led to worries about a drop in calorie consumption and food and beverage demand in general, pressuring the share prices of industry leaders. However, these claims and concerns seem to be vastly overblown as, for one, these drugs aren’t as straightforward as they sound, and we shouldn’t expect massive global adoption due to side effects. Morgan Stanley analysts are expecting 7% of the US population to use the drugs by 2035.

Secondly, other sources claim these weight loss drugs aren’t causing a significantly lower calorie consumption at all, at least no more than weight loss drugs that have been around for decades. For now, the biggest problem is that not enough data is available to draw reliable conclusions, and, therefore, the market reaction about the popularity of the drugs or the impact is overblown.

Several clinical trials have found that the drug, for example, lowers alcohol consumption, while others show mixed results or no impact at all. Circana Research believes that the GLP-1 medication is not at all causing smaller shopping baskets or fewer grocery trips, but it drives strategic shifts to lower-calorie items. Therefore, this should not impact food and beverage giants as long as they continue to monitor consumer demand and stay ahead of consumer preferences.

Therefore, while the drugs might have some impact on calorie consumption in developed economies, as is pointed out by some recent studies (definitely not all), this seems to be far enough down the road that these food and beverage giants can prepare themselves, mitigating the risk.

Now, while the real impact remains to be seen and everything said so far is largely speculation, there is not any impact today, and none is expected in the near future either, according to the CEOs of food and beverage giants PepsiCo, Coca-Cola, and Mondelez. Therefore, the recent share price weakness for these giants is a pure overreaction by the market.

The most important takeaway from the research and discussion above is that I, for now, do not view these recent drug developments as a risk for any of the food and beverage giants. Mondelez, along with its peers, is seeing no direct impact today and will most likely not see one for several years. In the meantime, the company has plenty of time to act on these developing consumer preferences.

With that, I want to end this speculation and recommend not to pay too much attention to these most often deceiving headlines until more reliable research becomes available.

In the meantime, though, Mondelez stock fell to the low $60s in mid-October, meaning shares were trading at a meaningful discount with peers like Coca-Cola and PepsiCo. Shares have since recovered back to the low $70s but continue to present a compelling investment opportunity, which is why I keep buying, although less aggressively. Its most recent quarterly result perfectly highlights why this company is a top pick in the consumer staples space.

Mondelez's Q3 results highlight its high quality

As a result of the market dynamics discussed above, shares are actually down 3% since I last covered these in June, against a 7% increase for the SP500. In the meantime, though, the company has delivered incredibly strong quarterly results of the quality that giants like PepsiCo could be jealous of.

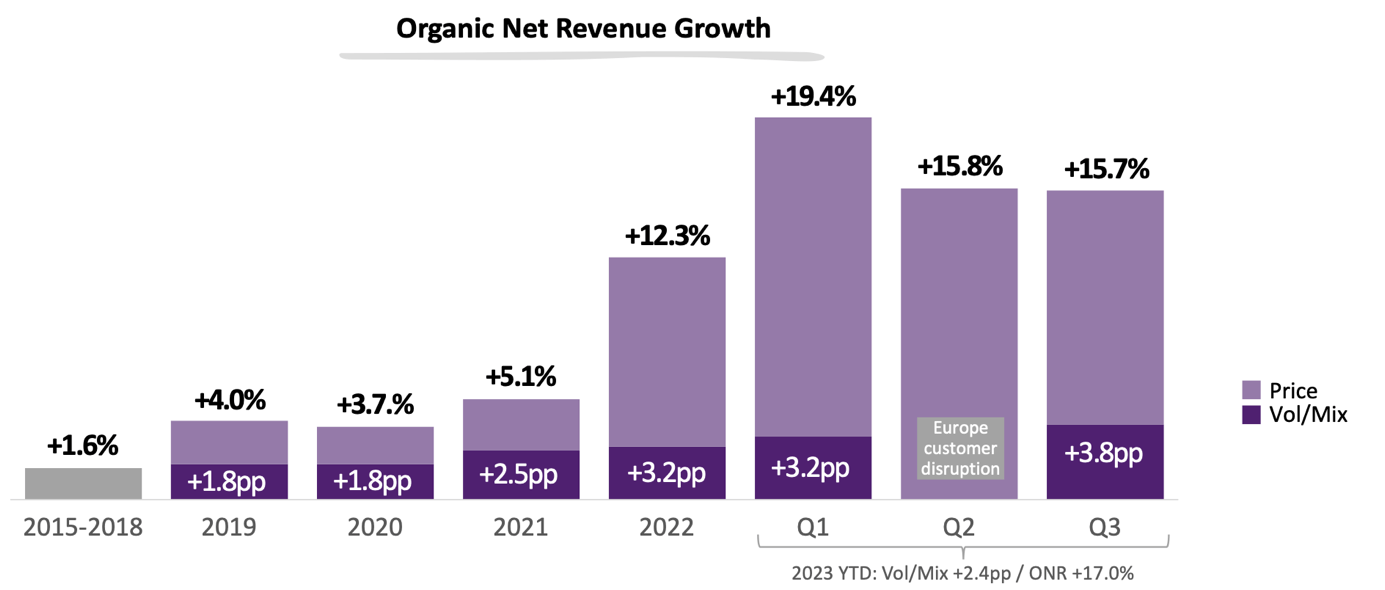

Mondelez released its Q3 earnings on the 1 st of November and reported revenue and EPS roughly in line with my expectations. Revenue beat by $110 million and came in at $9.03 billion, reflecting organic net revenue growth of 15.7% for the quarter, which is remarkable. This means that YTD revenue is now up 17% YoY or up close to $4 billion, on top of an already substantial 12.3% increase in 2022.

{kind=link}

Mondelez Q3 growth data (Mondelez)

In both instances, this increase was driven by both price and volume, which is far better than what we have seen from many peers who reported negative volume in response to the price increases. We are seeing somewhat of a shift in Mondelez’s mix, though, as volumes in Q3 contributed 3.9 percentage points to growth, up from the 2.8 percentage points YTD. This comes in response to price increases easing, with pricing contributing only 11.9 percentage points in Q3 against 14.6 YTD. According to Mondelez, most of its pricing measures are now behind it.

An important takeaway from this is that not only was Mondelez able to keep volumes positive throughout a year filled with significant price increases, but volumes are now also increasing meaningfully almost immediately following a slowdown in price growth, which is an essential indicator of strong demand for its products and a strong outlook not only driven by price increases – something consumer staple peers like PG ( PG ), KO ((KO)), and UL ( UL ) are often criticized for.

However, this is where Mondelez excels and what sets it apart from many of its peers. Mondelez's volumes today are stronger than before 2021 as Mondelez has been working hard on implementing new strategies, streamlining its product portfolio, and improving its financial profile. The strong Q3 results are evidence that management's long-term strategy continues to pay off, and I am bullish on the years ahead as I expect volume growth to remain far ahead of peers. For reference, driven by strong sales execution and brand-building investments, Mondelez held or gained market share in 65% of its revenue base YTD, up from 40% in 2022.

The strong top-line performance has translated into operating leverage across the business. Notwithstanding material marketing investment, profit growth delivery has been very strong in all regions and segments. As a result, the company was able to report margin expansion across the board, with a gross margin increase of 120 basis points YoY to 38.6% and an operating margin up 60 basis points to 16.7%. This resulted in an adjusted gross profit dollar growth of 22.3% for the quarter, which, again, is incredibly strong.

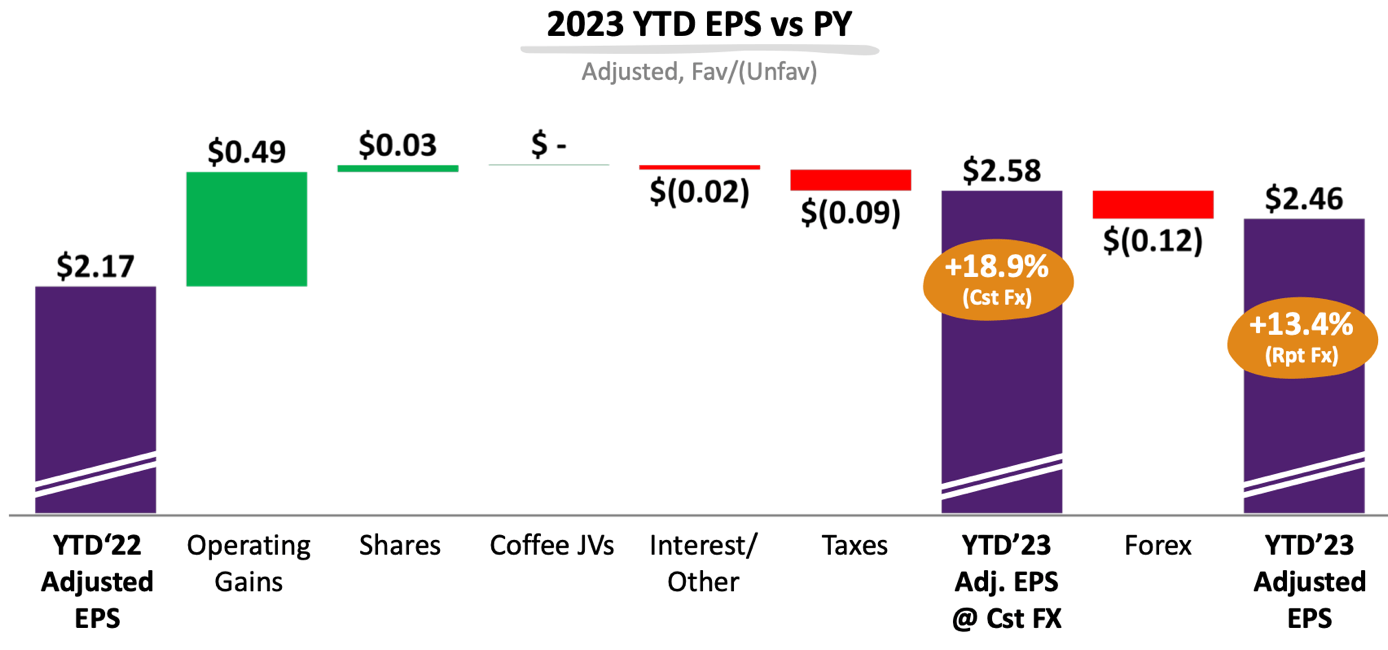

This improved profitability drove EPS up 13.9% in Q3 to $0.82, beating my estimates by $0.01. YTD, EPS is now up 13%. Furthermore, the company reported $2.4 billion in FCF YTD, up 26% YoY, and easily covered the capital returns of $2.2 billion this year, comprising $1.6 billion in dividends and $0.7 billion in repurchases. In addition, the company ended the quarter with $1.6 billion in cash and debt of $16.4 billion, which is down $3.6 billion over the last nine months and the company’s best balance sheet condition in years.

{kind=link}

Mondelez YTD EPS growth (Mondelez)

Mondelez reports strong growth across the board

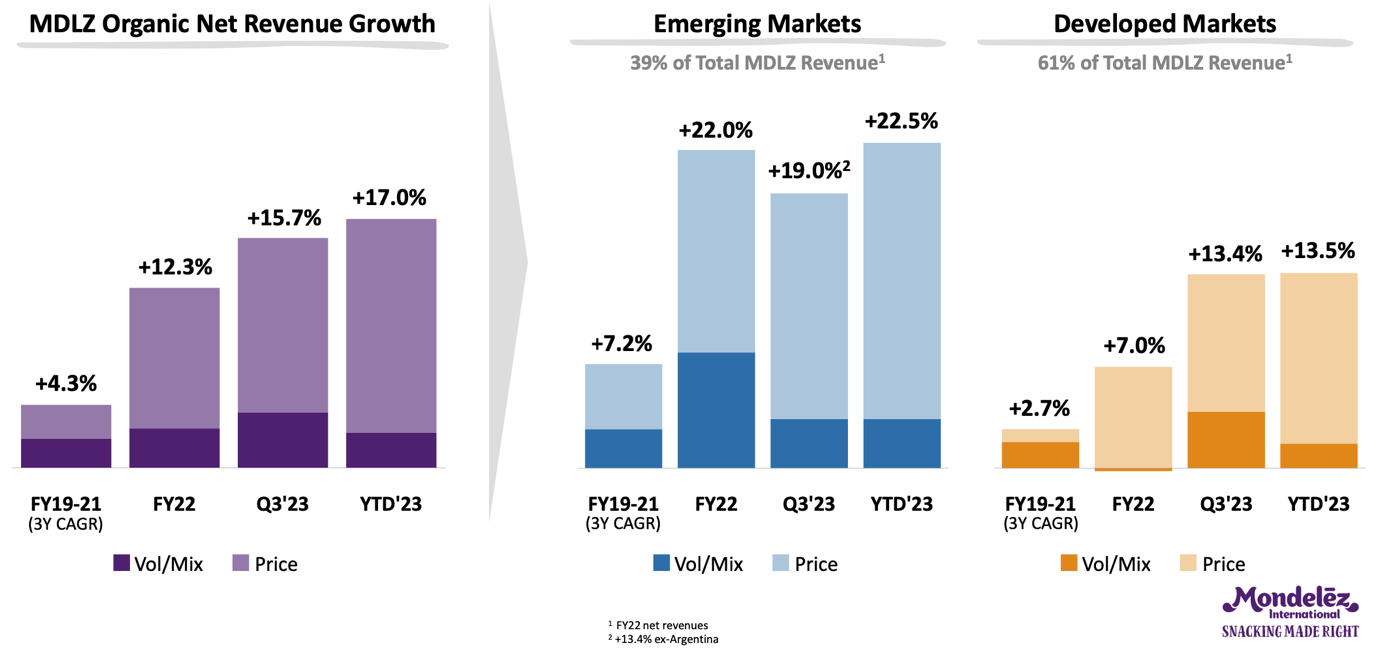

Diving deeper into the Q3 results, growth was driven by all regions, with double-digit growth in every region, driven by both pricing and volume. Europe grew 15.4% YoY, North America 11.4% with strong volume growth of 4.6%, AMEA was up 11.9%, and Latin America 35.1%.

This shows that demand remains strong globally, both in emerging and developed markets, up 19% and 13%, respectively, in Q3. Emerging markets continue to outgrow developed markets, in line with expectations. This trend will most likely persist due to the growing wealth and middle class in these regions and with the company having much greater expansion possibilities. Emerging markets now account for 39% of revenue, giving the company great exposure to these faster-growing regions, further fueling my optimistic growth expectations.

{kind=link}

Mondelez Q3 growth data (Mondelez)

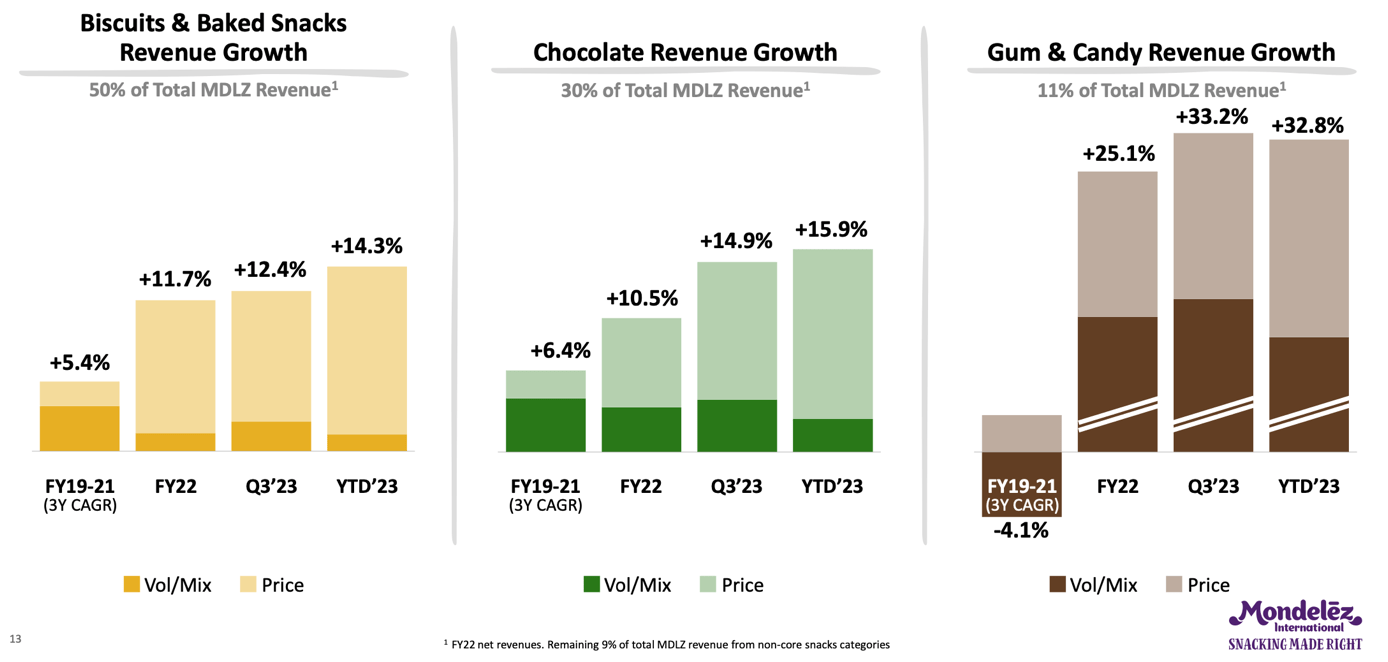

Meanwhile, organic growth for Mondelez also continues to be driven by all its product categories, with each of these posting double-digit growth in Q3. Biscuit revenue was up 12.4% in Q3, driven by a strong performance in brands like Oreo, LU, TUC, and Clif, as the company continues to benefit from healthy demand and incredible pricing power.

Furthermore, the company has a very well-diversified brand portfolio as well. The company has the ability to lean and invest in proven brands with great strength and popularity globally like Oreo but also to invest in upcoming brands like BelVita, which increased its share by close to 100 bps YTD. This mix of brands gives the company plenty of growth levers.

Meanwhile, management also shows a remarkable ability to spot and successfully act on upcoming consumer trends. For example, the company is seeing great progress in its snack bar business – a snack packaging category that is seeing great momentum – with this expected to hit $1.2 billion net revenue this year due to the company’s favorable positioning with its Clif bars, Grenade, and Perfect Snacks brands. The company has seen 19% growth YTD in consumption dollars of its Clif brand and is quickly gaining market share with its Grenade snack bars, driving growth in Biscuits.

{kind=link}

Mondelez Q3 growth by product segment (Mondelez)

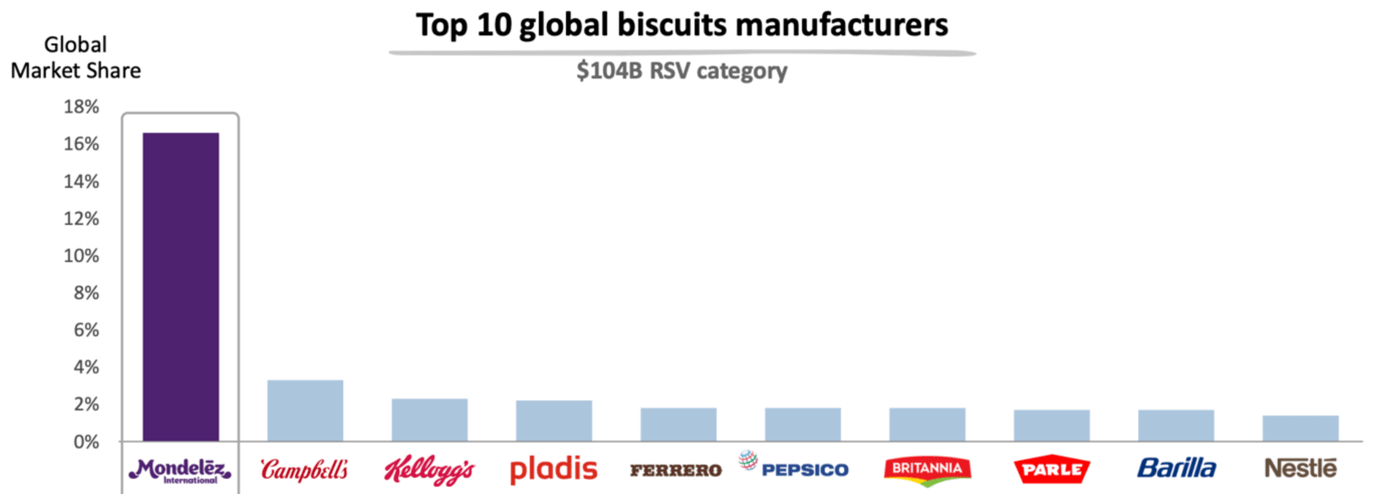

This segment now accounts for 50% of Mondelez's revenues. The biscuits industry is projected to keep outgrowing the overall snacks industry at a 5% projected CAGR through 2029 . Meanwhile, Mondelez remains the undisputed #1 in the industry with a market share of over 16%, compared to just around 3% for second place Campbell’s. Furthermore, Mondelez has shown over recent years that it has consistently captured more market share by focusing on faster-growing market verticals and strategic investments and acquisitions. Therefore, I firmly believe management should be able to keep outgrowing this industry by taking market share, most likely resulting in its largest segment growing at a 4-6% CAGR.

{kind=link}

Mondelez biscuits market share (Mondelez)

The chocolate segment is the second largest for Mondelez, accounting for 30% of revenue, and this one also performed strongly in Q3, with revenue up 14.9%, with key brands like Milka and Toblerone performing well.

Chocolate presents a strong growth opportunity for Mondelez, with its brands holding a strong position in the market, which is expected to grow at a CAGR of close to 6% through 2028 . The company holds a meaningful 12% market share in this $112 billion industry, making it the second largest only behind MARS, which has a market share of close to 13%. Yet, Mondelez has been rapidly gaining on MARS over recent years and is poised to overtake it to become the industry’s #1 in the next few years. Again, I expect Mondelez to keep gaining market share in this industry as well, driven by excellent execution and a very strong and well-positioned brand portfolio. Therefore, I project this segment to grow at a CAGR of 5.5% to 6.5%.

Finally, gum and candy grew more than 30% in Q3, with particular strength coming from emerging markets. This segment only represents 11% of revenue, but growth is expected to remain strong due to the company primarily focusing on emerging markets within these snack categories.

In October, Mondelez completed the sale of its developed markets gum business to Perfetti Van Melle. As a result, the company is now pretty much entirely focused on emerging markets within the gum and candy segment. The candy industry is projected to grow at a CAGR of just below 4% and gum at a CAGR of 4.4% . However, due to the focus on emerging markets, I expect growth for this segment to remain in the mid to high-single-digit range for Mondelez.

Taking all of this into consideration, I believe Mondelez should be able to grow revenues organically at a CAGR of 4-7% for the foreseeable future, slightly higher than management’s target of achieving 3-5% revenue growth. However, historically, management has been very conservative in its estimates, and I don’t expect this to be different today. Therefore, I see quite some room for financial outperformance and remain bullish.

Outlook & Valuation – Is MDLZ stock a Buy, Sell, Or Hold?

Following the impressive Q3 results, management once more upgraded its FY23 guidance and now expects top-line growth of 14% to 15%, against a start-of-the-year outlook of 5% to 7%, indicating that management has been very conservative in its guidance and demand has been far stronger than anticipated. In addition, management also expects EPS to come in higher than expected and now guides for a 16% YoY increase (organically).

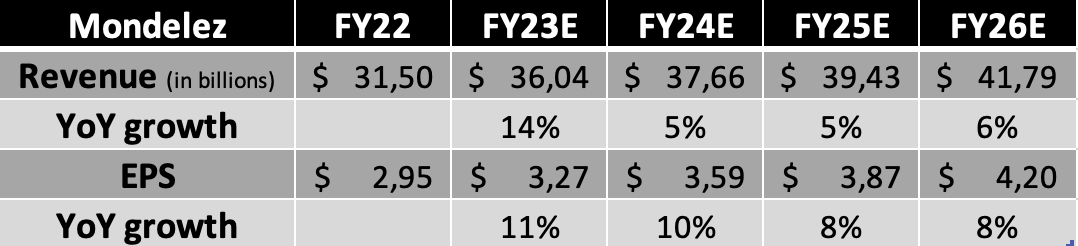

Following these recent developments, management’s upgraded guidance, and the very impressive Q3 results, I upgraded my near-term financial estimates and now expect the following financial results through FY26.

{kind=link}

Financial projections (Author)

Based on these financial projections, shares are now valued at approximately 21.5x this year’s earnings, which means these trade at a slight 3% premium to their 5-year average but are discounted to similar high-quality peers like PEP, PG, CL ( CL ), and KO.

Considering the company’s incredibly high quality, which should have become quite obvious throughout this article, I strongly believe the company deserves to trade at a valuation similar to that of these peers, which is why I view a 23x multiple as fair. Based on this view and my FY25 EPS projection, I calculate a target price of $89 per share. From a current share price of just below $71 per share, this should leave investors with annual returns exceeding 10%.

Meanwhile, the company also pays a very attractive dividend that should bring total returns to close to 13% annually, which should easily beat global indices through the end of the decade. Shares currently yield 2.4%, in line with peers PG and CL. However, Mondelez has shown very impressive dividend growth over the last few years, growing the dividend at an average of 11% over the past five years, with the most recent increase of 10% in July of this year. Also, this is based on a conservative payout ratio of below 50%, much better than most of its peers and leaving the company with plenty of room to continue growing the dividend strongly, making this an interesting pick for dividend growth investors as well.

All things considered, I continue to be extremely bullish on Mondelez’s long-term prospects and strongly believe this to be one of the most attractive opportunities in the consumer staples industry today, following some share price weakness. From a current share price of $71 per share, I expect investors to reap returns of around 13% annually, which is more than enough to rate shares a “Buy.”

For further details see:

Mondelez: Still More Attractive Than Peers - I Am Buying