MONDF - Mondi: Interestingly Valued Dividend Payer In A Special Situation

2023-06-19 05:41:25 ET

Summary

- Mondi, a leading paper and packaging company, is a top choice for investors looking to tap into the industry, offering high returns on capital, low indebtedness, and a strong dividend.

- The industry is currently experiencing a slowdown, but the following quarters could provide a good entry point for leading names in the industry, including Mondi.

- Despite concerns around industry slowdown and uncertainty around Russian operations, Mondi stock is reasonably priced and offers a good dividend, making it an attractive option for risk-tolerant investors.

Mondi (MONDF)(MONDY) is a leading paper and packaging company. The company is one of the top choices for an investor considering tapping into the industry, which is a major player in the more sustainable future. Mondi has market leading positions in its businesses, high returns on capital, low indebtedness, strong cash generation and a high but relatively secure dividend.

The industry is in the midst of a slowdown and the valuations have contracted against the strong previous year. While earnings are likely to contract, the following quarters could represent a good entry to the leading names in the industry. Currently, Mondi is also in a special situation. Its rather substantial Russian operations have been for sale, but the sales process was recently put on hold or terminated. If the sales ever goes through, shareholders could be rewarded with an extra dividend.

A leading player in Europe

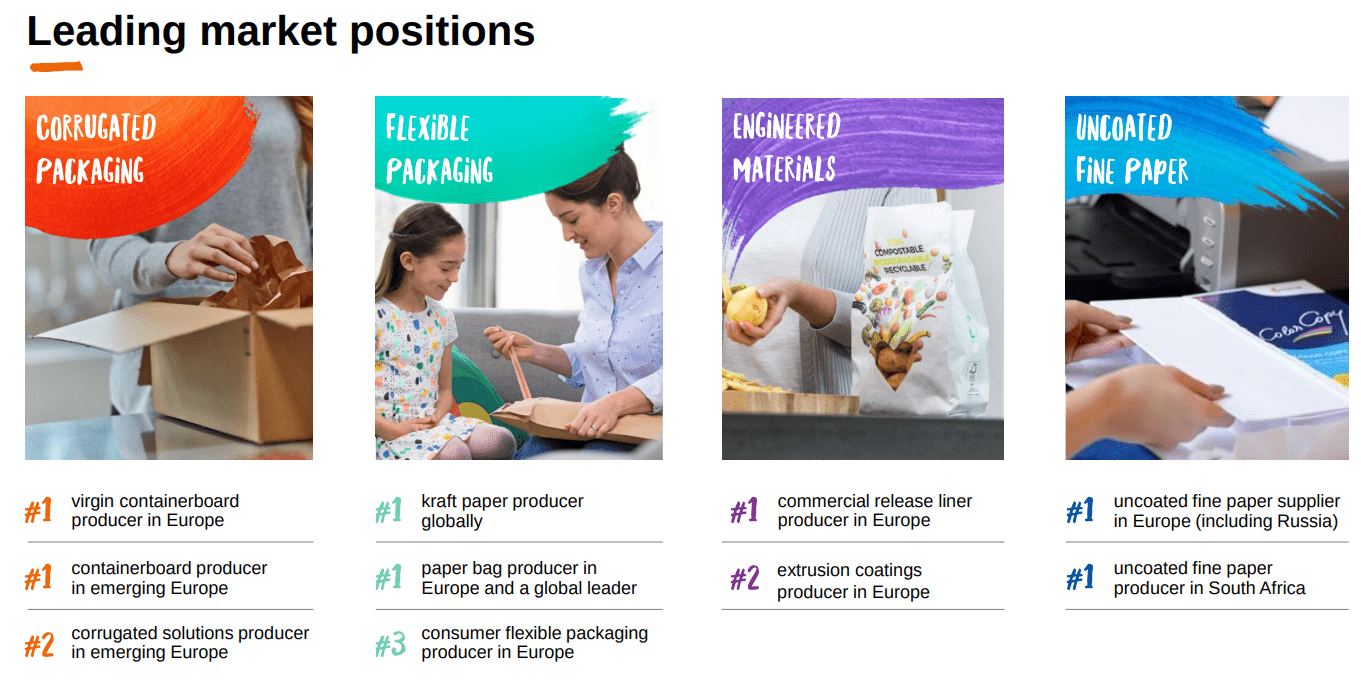

Mondi is a vertically integrated paper and packaging company. Its business is divided into three segments: corrugated packaging (35% of EBITDA), flexible packaging (43%) and uncoated fine paper (23%). It holds a market leading position in most of its sub-segments in Europe. Mondi employs 22 000 people and has 100 production facilities in over 30 countries and all continents except Asia. Mondi has a primary listing on the London Stock Exchange and a secondary listing on the JSE Limited, Johannesburg, South-Africa.

Market positions in different segments. (Company presentation)

{kind=link}

Year 2022 was an exceptionally strong year for Mondi. The revenue increased 28% to 8.9 billion euros. Its operating profit increased 114% to 1.7 billion euros and earnings per share grew 118%. It’s unlikely that these results will repeat this year and the share price has acknowledged that. The share price has stabilized on the level where it was last time in 2016 and briefly during the pandemic and Russian invasion of Ukraine.

Mondi doesn’t publish quarterly reports but trading updates. In the trading update for the first quarter the “underlying EBITDA” decreased by 25% compared to the year earlier but was 30% higher than in 2021. The following quarters will show if Mondi is able to maintain a higher level than in the past. In the trading update the company warned about lower selling prices and softer demand driven by destocking but balanced by lower input costs.

Quarterly EBITDA development. (Trading update of Mondi.)

Current opportunities and risks

Key trends supporting the business

Mondi is a key player in a more sustainable future. Its products help to reduce plastic materials in consumer product packaging. It’s relatively safe to say that the trend is in its early innings. CPG companies partner with companies such as Mondi to develop more sustainable packaging and logistic solutions.

Digitalisation and ecommerce are both an opportunity and a risk for Mondi. The growing share of ecommerce requires more containerboards and packaging. On the other hand, the company produces fine paper for printing which is on a secular decline. Since the share of fine paper of the company’s revenues and profits is much smaller, the net result of these trends works in Mondi’s favor.

Investing into a downturn

The industry is clearly now in a downturn demonstrated by the recent news. On the 15th of June Billerud, a Swedish competitor, released a negative profit warning, however the stock reacted to it mildly. Stora Enso, a Finnish competitor, recently announced a major reorganization, potentially leading to divestments and layoffs. The stock has reacted more negatively, probably due to the fact that it had rebounded from its lows in May.

Falling pulp prices could be a concern in the pulp and paper industry. However, Mondi’s net exposure to pulp prices is low. It sells only around 5% of its pulp production to external customers. The majority of the produced pulp is used internally for different types of products. Vertical integration has enabled Mondi to maintain good margins over the last ten years.

{kind=link}

Furthermore, Mondi has a healthy balance sheet with very little good-will and intangibles. Total debt to equity is only 33% and net debt to EBITDA deducting capital expenditures is 0.9. Due to the lower EBITDA and investments this figure will inch higher, probably to around 1.2-1.5. Despite low leverage Mondi has historically achieved high return on equity and good levels of return on assets and capital.

{kind=link}

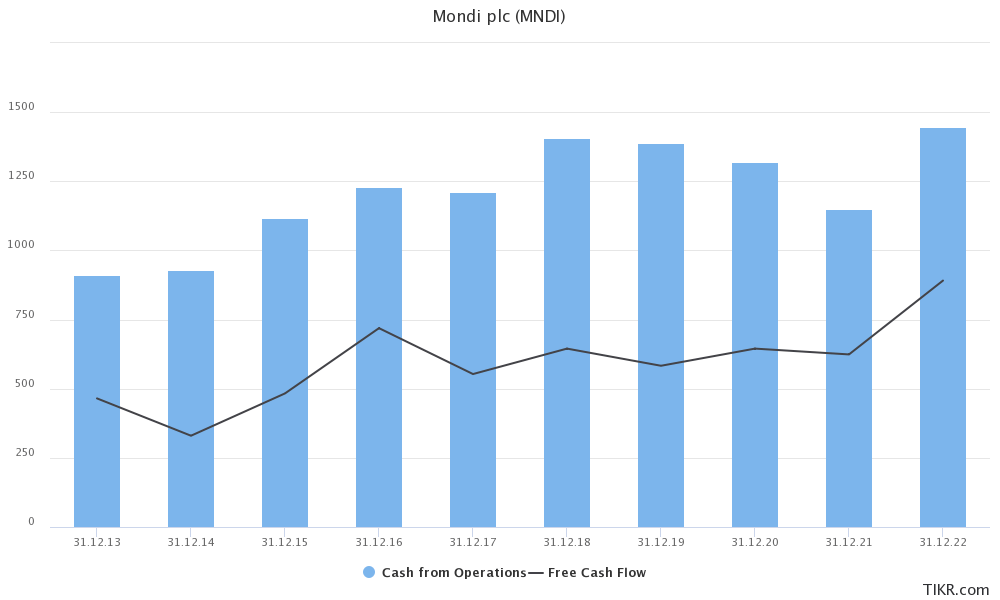

Mondi has an ongoing 1 billion euro investment program to increase its capacity. The investment is allocated to the growth segments. 22% to the production of corrugated packaging and 19% to its converting operations. 40% to the production of flexible packaging and 19% to its converting operations. The investments are split into several years and if the company is able to maintain its historically strong cash flow profile and cash position, there doesn't seem to be issues in financing the investments internally.

Cash flow from operations and free cash flow. (TIKR)

{kind=link}

The risk here is that Mondi invests and increases capacity in the midst of a recession and falling consumer demand. On the other hand the investments are required for further growth while a large chunk of its business is behind the new iron curtain.

The sale of Russian operations halted

One of the key risks for Mondi and its shareholders are the Russian operations. In 2021 the share of Russia was 10% of the revenues but 23% of the underlying EBITDA. In the first quarter of 2023 Russia’s share of the underlying EBITDA was 35%. At the end of the previous year the Russian operations were valued at €1.1 billion on the company's books, representing approximately 10% of the total assets.

In the beginning of June the company withdrew from an agreement to sell its Russian operations. Most likely the company didn't get the price it wanted. According to the news , Citibank expected “GBP0.49-GBP1.15 for each share”, which could be translated as extra dividend of 4-10 per cent. Citi maintained a target price of 1700 pence for Mondi’s stock. While the Russians pursue to purchase Western assets on the cheap, I believe it’s good that the Mondi’s management stays prudent. The company still intends to sell the business.

Price-to-book multiple in a ten year low

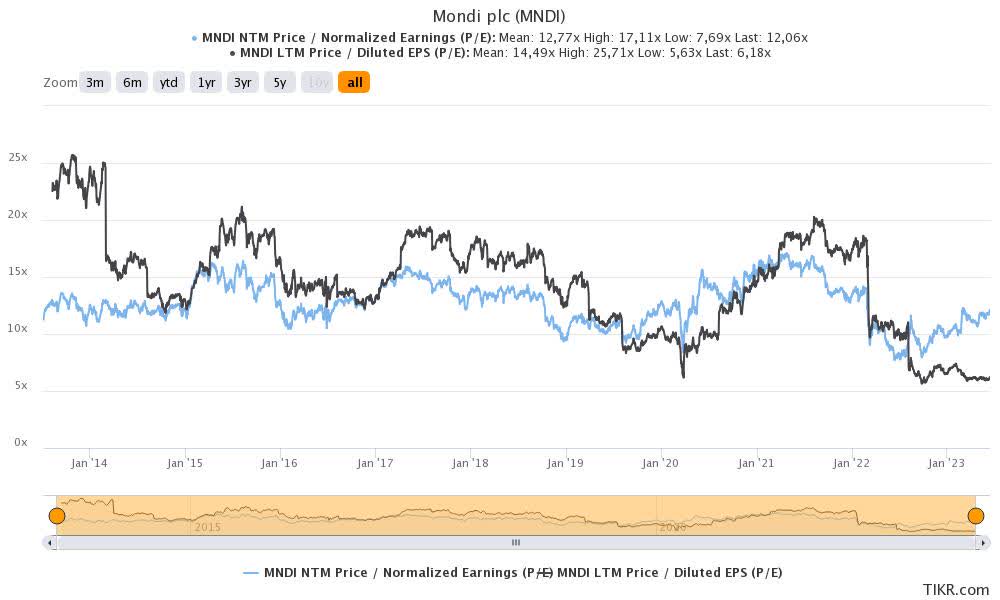

In 2022 Mondi’s earnings were unusually high. Its earnings per share were 2.44 euros, while its earnings have normally ranged between 0.8 to 1.7 euros per share for the past 10 years. Excluding the year 2022, the average EPS of the preceding nine years would be 1.14 euros. According to Tikr, the next twelve months normalized (excluding exceptional items) earnings per share is 1.24 euros. The current share price implies a P/E-multiple of 12. The last time Mondi’s EPS was below the normalized earnings was in 2021 (1.2 euros), but we need to go as far as to 2015 and before (1.09, 0.93 and 0.54 euros) to see lower EPS figures.

EPS development and net income margin. (TIKR)

It's important to note that the cyclical stocks look the cheapest before downturn, meaning the P/E-ratio is not the best benchmark here. Nevertheless, from the earnings perspective the valuation has accommodated to the new market environment and front run the earnings decline.

Forward and trailing P/E. (TIKR)

{kind=link}

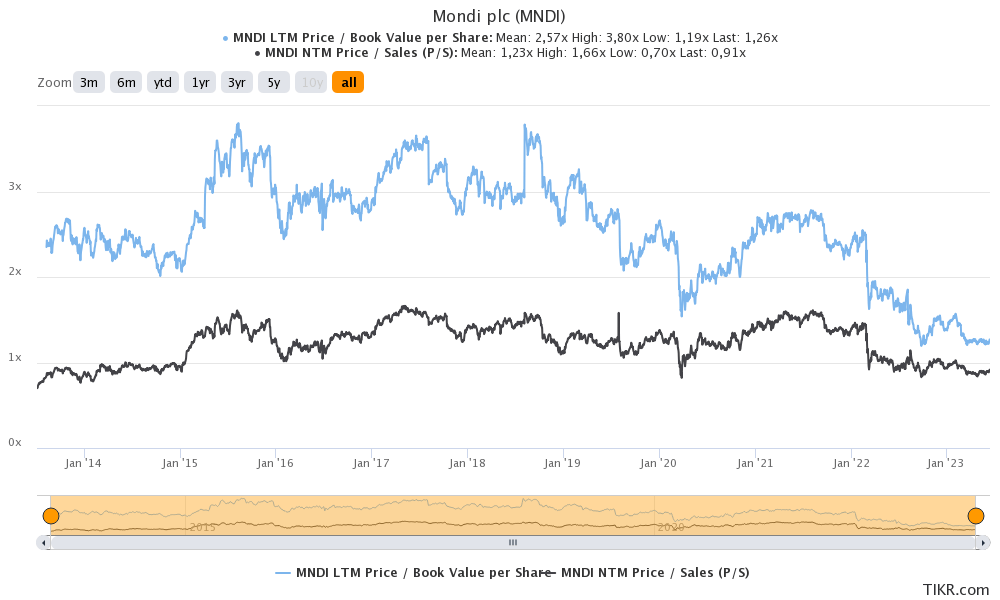

The price decline of the shares have made the stock inexpensive against its book value - the cheapest level in ten years actually. Since the balance sheet is mostly composed by real assets, an investor can now purchase the production network at historically low valuation. Although the sustainability of the current level of sales is at risk, P/S-multiple is also well below the mean. On a free cash flow basis, the next 12 months free cash flow yield stands at 6%, which is also a 10-year mean.

{kind=link}

When comparing Mondi to its key competitors Mondi is lower valued on various metrics, despite its strong financial performance. Some of the reasons for this could include the risks involved with Russian operations, high exposure to Europe and listing in the UK and South Africa.

An industry leading dividend

Mondi pays its dividend in euros. According to the 2022 annual report , the dividend has developed positively over the past four years, increasing from 57 cents in 2019 to 70 cents in 2022. In 2018 the dividend was 76 cents per share. Due to the abnormally high earnings last year the payout ratio is only 25%. Against the forward-looking normalized earnings presented above, the payout ratio is 62%.

Mondi pays the dividend semi-annually. The first payment, a final dividend from the previous year, is typically paid in May and the interim dividend, if declared, is paid in September or October. For the residents outside the UK and South Africa the dividend is paid in euros.

Conclusion

While concerns around the industry slowdown shadow all the stocks in the paper and packaging industry, one of the leading players is reasonably priced based on forward looking earnings and is on sale based on the price to book. The uncertainty around the fate of the Russian operations can pressure the stock but provide an opportunity to a risk tolerant investor. Meanwhile the company pays a good dividend.

Considering the industry, Mondi has characteristics of a good business with good capital returns and margins. There are important trends supporting the business. As the downturn could be in its early innings, a cautious investor should wait for the half-year results to be announced on 3rd of August.

For further details see:

Mondi: Interestingly Valued Dividend Payer In A Special Situation