MONDF - Mondi: Tougher Times But Still A Decent Business

2023-09-24 08:16:59 ET

Summary

- Mondi, a packaging and paper multinational, had a challenging first half due to downward pricing pressure in the global paper market.

- Despite the challenging business environment, Mondi remains well-positioned in an industry with high and growing demand, providing some level of protection to profitability.

- The company's interim results were underwhelming, with revenue falling and pre-tax profit more than halving, but its strong cash generation performance highlights its long-term investment potential.

Packaging and paper multinational Mondi ( OTCPK:MONDF ) had a tough first half, largely due to downward pricing pressure in the global paper market (though that underlines that to a large extent it is operating in a commodity market). At the same time, the underlying potential of the business remains strong if not compelling.

I last covered Mondi in 2020 ( Mondi: Positioned For Long-Term Growth ) with a “buy” rating, since when the total return has been -13%. I maintain my “buy” rating. I maintain my “buy” rating albeit I think this is a stock to buy and largely forget about for coming years rather than a racy growth number.

Business Environment is Challenging

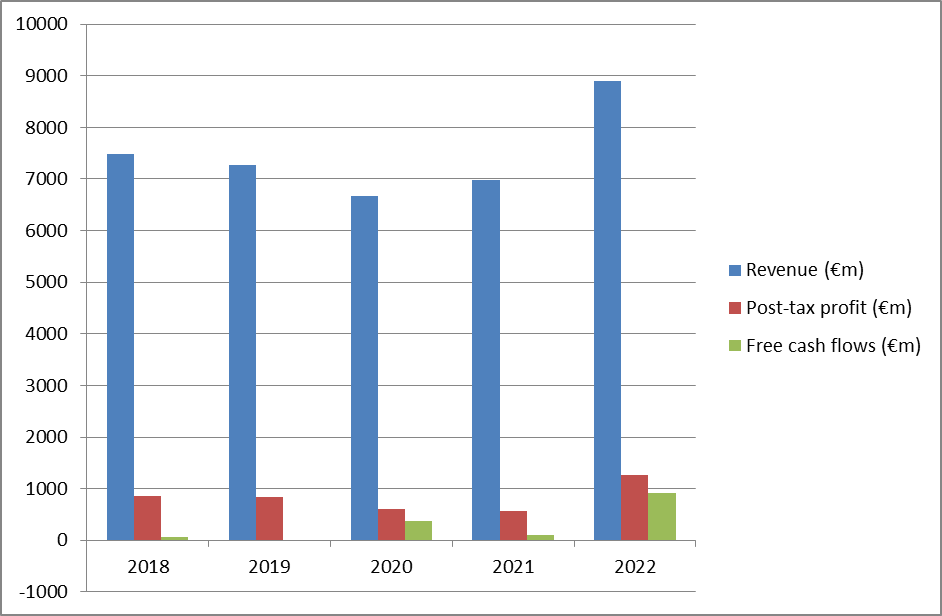

I would say that Mondi turns in a respectable though not outstanding business performance in a mature industry. In recent years it has been consistently profitable, though free cash flows have been variable and weaker than profits.

Chart calculated and compiled by author using data from company annual reports

{kind=link}

What I like about Mondi is that it is well-positioned in an industry that I expect to see high and growing demand, with relatively high barriers to entry at the global level. That ought to keep revenues buoyant, as well as providing some level of protection to profitability.

I do not see it as an exciting share or one from which I would expect dramatic returns. Rather, I see it as likely being a fairly solid performer over the long haul.

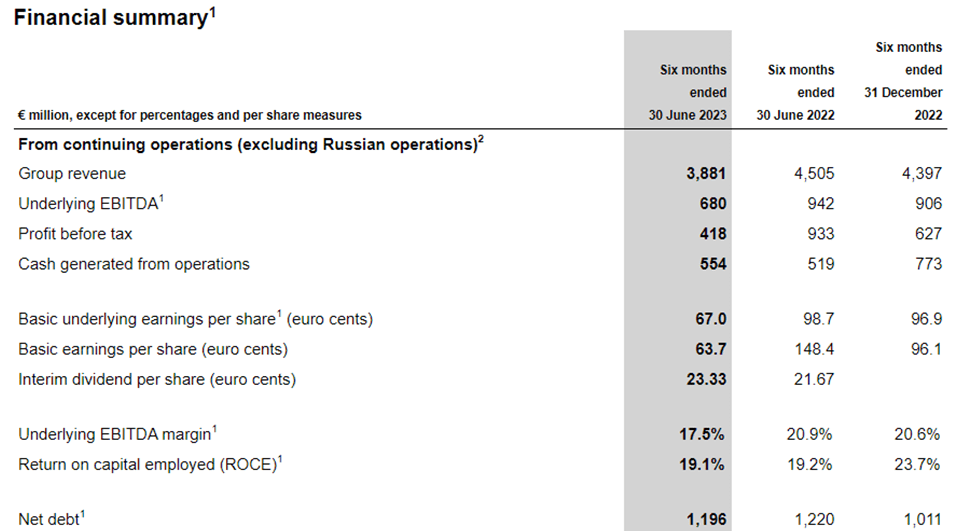

The company released its interim results last month. These were underwhelming. Revenue fell, pre-tax profit more than halved, while basic earnings per share did a little worse yet. A 7.6% increase in the interim dividend offered some solace to shareholders.

{kind=link}

Somewhat disingenuously, the results were entitled “"Delivering in challenging markets. Investing for future growth." The report emphasised what was seen as strong company performance (as seen in the above chart, operating cash generation grew by 7% year-on-year) in what was characterised as a challenging set of market conditions. I note, however, that pre-tax profit at rival Smurfit Kappa ( OTCPK:SMFTF ) declined by only 14% in the equivalent period).

The first half saw the industry experiencing a downtrend both in demand and pricing, outside containerboard. Input costs fell, but clearly that was insufficient to save profitability levels at Mondi.

The company had little to say about its full-year outlook. The paper market continues to face a difficult environment and weak pricing. I expect that to show through in Mondi’s second half results and therefore across the year as a whole. The downbeat note struck by Mondi in its interim results led to a 6% fall in its share price on the day of their release. They have since recovered from that (and more) and are 4% down so far this year.

In the short term I see the paper market pricing as unsettling. However, it is essentially a cyclical market and I expect demand and supply to rebalance over time, bringing pricing up again. Meanwhile, even in the current depressed market, Mondi powered through and generated substantial cash in its first half. While the swings are large (as is common in cyclical markets), in itself the first half cash generation performance helps to underline the long-term investment case in my view.

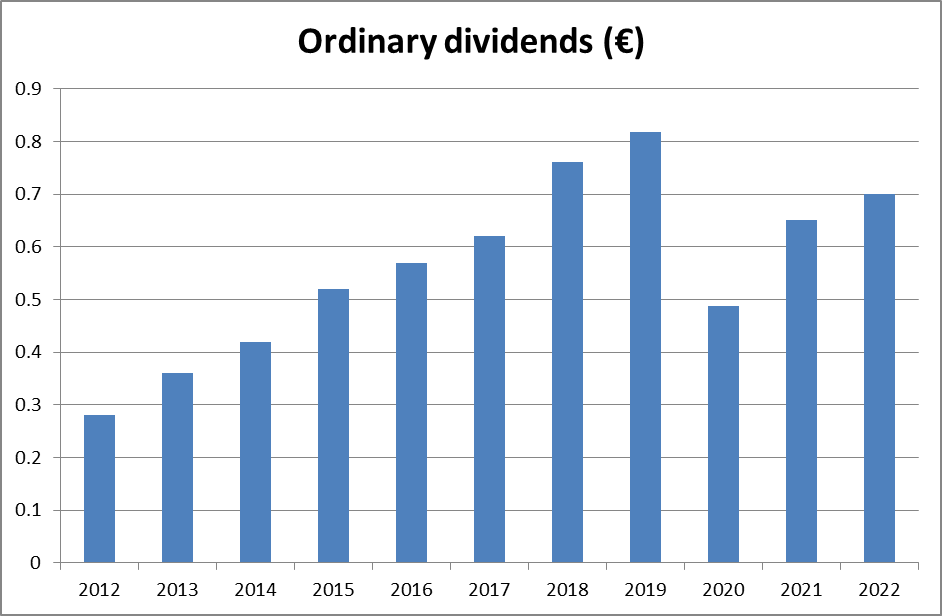

Dividends have Room to Rise Further

With a yield of 4.6%, Mondi is fairly attractive from a dividend perspective.

The dividend last year was covered 2.8 times by earnings.

The company generated €892m of free cash flows even after paying €321m of dividends, which I regard as comfortably ample coverage. Indeed that provides sufficient flexibility for the company to continue raising its dividend even if financial performance slips, as we saw at the interim stage.

That said, the past few years have seen an inconsistent dividend level (driven in part by the company’s response to the pandemic). So, even after the 7% rise, the latest interim dividend is just 9% above the level seen five years previously. That is fine but not exactly the stuff of investor dreams.

Chart compiled by author using data from company annual reports

{kind=link}

Risks

As the first half demonstrated, pricing moves in the wider market pose a significant risk to revenue and particularly to profitability at Mondi. The demand surge and fallback during the pandemic years continue to work their way through the system and I see this as an ongoing risk for some years to come.

“Risk” is mentioned 631 times in the most recent annual report (!) In reality, though, I see this as a mature, stable and conservative business with a risk profile to match.

Valuation

At the moment, Mondi has a market cap of £6.1bn. Its net debt at yearend stood at €1.0bn (sharply lower than the prior year’s €1.7bn). That suggests an enterprise value of approximately £7bn.

It currently trades on a price-to-earnings ratio of just 8, which makes it sound like a potential bargain. As the above chart showed, though, earnings can move around a fair bit and last year’s performance was the best for years albeit this year has begun (and looks set to end) far less lucratively. Still, even using the far smaller 2021 number, the P/E ratio only comes in at around 11, which seems reasonable to me.

Rivals are even cheaper: Smurfit trades on a P/E ratio of 7, for example. But I see that as an example of deep value in this cyclical sector rather than of Mondi offering poor value. I therefore maintain my “buy” rating.

For further details see:

Mondi: Tougher Times But Still A Decent Business