MDB - MongoDB: Deceleration Incoming (Rating Downgrade)

2023-12-21 09:27:12 ET

Summary

- MongoDB's share price has jumped over 115% this year, but growth is slowing, and the valuation is quite rich.

- The stock trades at ~14x FY25 revenue.

- Meanwhile, revenue growth is decelerating due to a slowdown in Atlas customer additions, as well as macro-impacted usage levels.

- It's best to take chips off the table and lock in gains here.

And just like that, the S&P 500 is close to touching all-time highs again. Interest-rate fears, which have driven the markets for most of the past two years, subsided much more quickly than they built up - and with it, high-flying tech stocks are now everywhere in the markets as well.

MongoDB (MDB) is a chief example of this. The non-relational database software platform has seen its share price jump by more than 115% year to date, bringing the stock close to its pandemic-era highs (a level many of its peers are still yet to rebound to). The core question for investors now is: can MongoDB keep rallying in 2024, or is it time to take chips off the table?

I'm in the latter camp. I last wrote a neutral opinion on MongoDB in October when the stock was trading closer to $360 per share, after having previously been bullish on the stock earlier in the year. And while it's true that I missed out on the past two months' worth of appreciation, I hardly regret my decision to de-risk my portfolio.

The two top things for investors to keep in mind: MongoDB's growth is now slowing in a big way, not only from a tough macro environment for IT budgets, but also as a victim of its own scale. And yet despite this, expectations remain incredibly lofty for the company ( earnings results generally tend to disappoint , at least it did in the most recent Q3) - which is a given when a stock like MongoDB trades at valuation levels almost unheard of in the software sector.

Valuation, not fundamentals, is the second and the biggest concern here. Even with a ~1 point reduction in interest rates, it's hard to justify that MongoDB trades at an investible price. At current share prices near $411, the company has a market cap of $29.77 billion. And after we net off the $1.92 billion of cash and $1.14 billion of convertible debt on MongoDB's most recent balance sheet, the company's resulting enterprise value is $28.99 billion.

Meanwhile, for fiscal year 2025 (the year for MongoDB ending in January 2025), Wall Street analysts are expecting the company to generate $2.02 billion in revenue, representing 22% y/y growth (and a sharp fall from the current quarter's 30% y/y growth rate, and last quarter's 40% y/y growth rate). In spite of this, investors are apparently still assigning very high multiples for this stock - against FY25 consensus, MongoDB trades at 14.4x EV/FY25 revenue.

A mid-teens valuation multiple in the height of the pandemic for a ~20% growth stock was commonplace - but that's back when interest rates were nearly zero. Even though rate expectations for next year have come down , it's still difficult to justify a pandemic-era price for MongoDB especially when its growth rate is expected to come down to "normal" ~20% levels.

And on top of the major valuation risk, I see some performance/fundamental risks heading into next year as well, including:

- Less-than-stellar usage trends - MongoDB prices by usage and by workload, and analysts have called out that MongoDB's usage rates have not seen a bounce back like some competitors have.

- Customer growth is slowing down - Results in MongoDB Atlas have also sparked concern, especially as net-new customer additions slow relative to the pace from recent quarters.

- GAAP losses are still large - Though MongoDB has notched positive pro forma operating and net income levels, the company is still burning through large GAAP losses because of its reliance on stock-based compensation. In boom times investors may look the other way, but in this more cautious market environment MongoDB's losses may stand out.

- Competition- MongoDB may have called itself an "Oracle killer" at the time of its IPO, but Oracle (ORCL) is also making headway in autonomous and non-relational databases. Given Oracle's much broader software platform and ease of cross-selling, this may eventually cut into MongoDB's momentum.

All in all, I'm downgrading MongoDB to sell , given the confluence of an unsupportable high valuation and elevated expectations making it difficult for MongoDB to surprise to the upside in 2024. Lock in any gains you have on this stock, and move on.

Q3 download

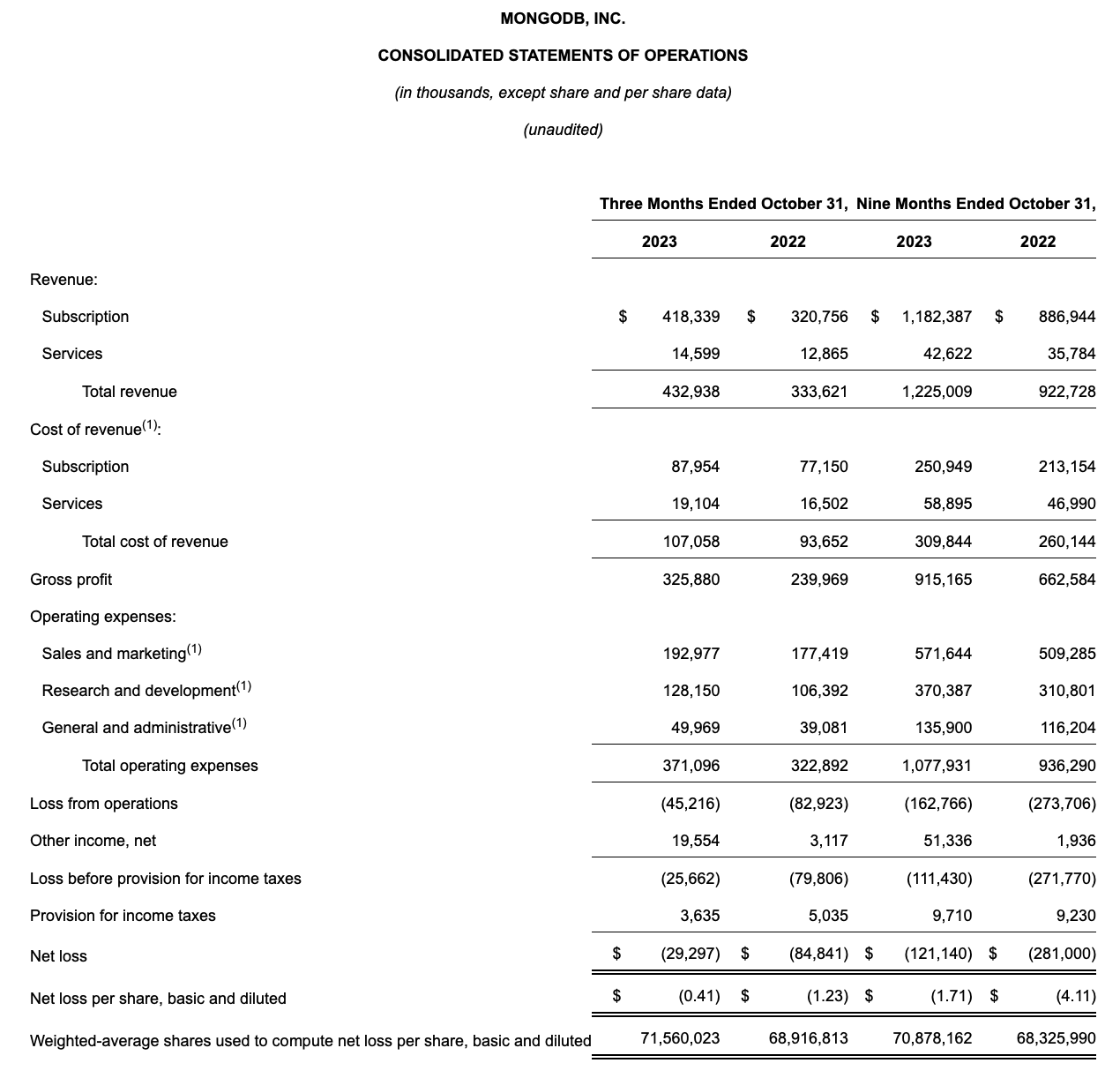

Let's now go through MongoDB's latest quarterly results in greater detail. The Q3 earnings results are shown in the snapshot below:

MongoDB Q3 results (MongoDB Q3 earnings release)

{kind=link}

MongoDB's revenue grew 30% y/y to $432.9 million. This was well ahead of Wall Street's expectations of $403.9 million (+21% y/y), but showed considerable deceleration relative to Q2's growth pace of 40% y/y.

From a product perspective, the company continued to deepen its suite of AI-related offerings. It made a new product, MongoDB Atlas Vector Search, generally available within the quarter - a platform which helps developers build real-time generative AI applications on top of the MongoDB database.

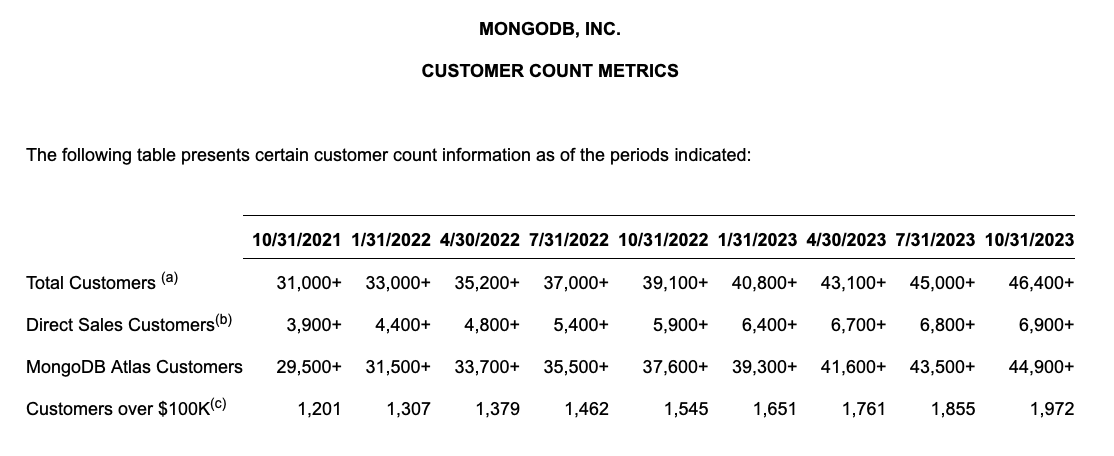

From a customer perspective: note that MongoDB's overall customer counts slowed to a net add of just 1,400 customers in the quarter, versus 1,900 in Q2.

MongoDB customer counts (MongoDB Q3 earnings release)

{kind=link}

Similar to other companies, MongoDB has faced both elongating sales cycles as well as difficulties in upselling existing customers; though management notes retention has been strong, with dollar-based net retention rates clocking in at 120% this quarter. Here is additional commentary from CFO Michael Gordon on consumption trends in Q3, taken from his prepared remarks on the Q3 earnings call :

Let me provide some context on Atlas consumption in the quarter. Week-over-week consumption growth in Q3 was in line with our expectations and stronger than Q2. As a reminder, we were expecting a seasonal uptick in consumption in Q3 compared to Q2 based on what we've experienced and shared with you last year. We had forecasted that seasonal improvement to be less pronounced this year compared to last year. Given that overall, we've seen less consumption variability this year and that is exactly how the quarter played out.

Turning to non-Atlas revenues, EA exceeded our expectations in the quarter as we continue to have success selling incremental workloads into our existing EA customer base. Ongoing EA strength speaks to the appeal and the success of our run-anywhere strategy. The EA revenue outperformance was in part a result of more multiyear deals than we had expected. As a reminder, the term license component for multiyear deals is recognized as upfront revenue at the start of the contract and therefore includes term license revenues from future years."

From a profitability standpoint, we do note that MongoDB achieved an impressive pro forma operating margin lift to 18%, 12 points better than 6% in the year-ago quarter - though management noted that Q3 was rosier than normal due to a timing shift of both new hires as well as marketing spend pushing out to Q4. In spite of this, we note that MongoDB remains a "Rule of 40" software company - so some valuation premium is certainly justified, but considering GAAP losses are still negative and the company doesn't generate enough pro forma net income or cash flow to support its valuation from a bottom-line perspective, I remain bearish on this name.

Key takeaways

MongoDB remains a classic software trade "good quality for an extremely high price." In this market environment, with the S&P 500 flirting with all-time highs again, I'd hesitate to overexpose my portfolio to high-flying software stocks like this one. My recommendation: sell what you have (perhaps in January to defer your tax bill on any gains; I don't foresee much downside in either the broader market or MongoDB in the next few weeks through the end of the year) and invest elsewhere.

For further details see:

MongoDB: Deceleration Incoming (Rating Downgrade)