PSI - Monolithic Power Systems: Curbing Our Optimism

2024-01-16 19:38:12 ET

Summary

- Monolithic Power Systems has delivered over 2x the returns of the S&P 500 over the past year, but we don't expect this to continue.

- MPWR's topline will lag the industry this year, and with an increased presence of consumer-related sales, the gross margin uplift may not be easy to facilitate.

- Earnings growth of 10% will lag topline growth and with a forward P/E of 45x that doesn't look like a great pitch.

- MPWR has delivered exceptional dividend growth for 3 years on the trot, but we highlight why this may ebb going forward.

- The risk-reward on the charts doesn't look appealing.

Introduction

The stock of Monolithic Power Systems, Inc. ( MPWR ) a 27-year-old fabless entity that specializes in analog and mixed-signal ICs (integrated circuits) has enjoyed its time in the sun. Over the past year, it has managed to generate ample returns of 46%, over 2x the returns generated by the broader markets.

{kind=link}

{kind=link}

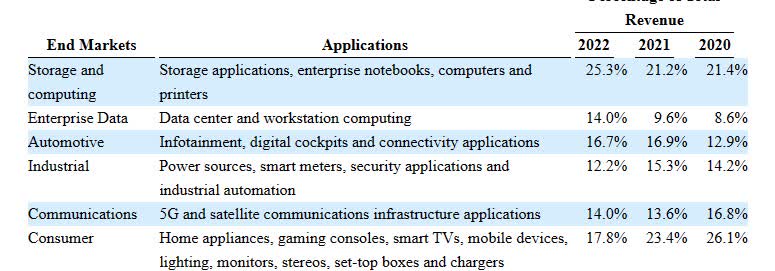

Whilst MPWR no doubt has some fundamentally impressive qualities (the small form factor of their chips which facilitates greater integration across various applications, diversified exposure to 6 end markets, sturdy dividend growth, no debt on the books, solid FCF-generation and over $1bn of liquidity on the balance sheet, etc.) that would have attracted large swathes of the investment community, we think interest was amplified with the growing clout of the enterprise data segment which is seen as an ideal proxy for AI-GPU momentum. For context, back in 2020, the enterprise segment was the lowest contributor to the top line, accounting for only 9% of the sales mix, but by Q3-23 it was the second largest contributor, accounting for 21% of group sales.

All in all, whilst MPWR's alpha generation has been admirable, we remain doubtful if that can be maintained for yet another year. Here are a few reasons why we would choose to temper our optimism on the stock.

The Financial Outlook Isn’t Outstanding And The Forward Valuations Don’t Reflect That

During difficult periods for the semiconductor market, MPWR has traditionally demonstrated useful competence in growing ahead of the market, but with fortunes poised to shift in 2024, we are not sure the stock is best placed to ride the cyclical upswing.

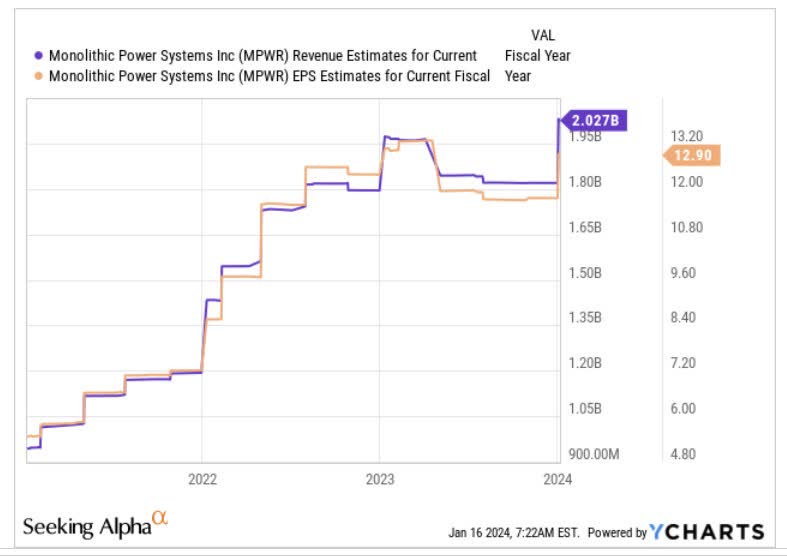

Gartner now expects the semiconductor industry to grow at a healthy pace of 17% in FY24, but with MPWR poised to generate topline of $2.03bn, you’re basically looking at a smaller pace of YoY revenue growth of only 12%. When you’re only likely to generate early double-digit topline growth, it feels a bit much to be priced at a forward price-to-sales multiple of 14x.

{kind=link}

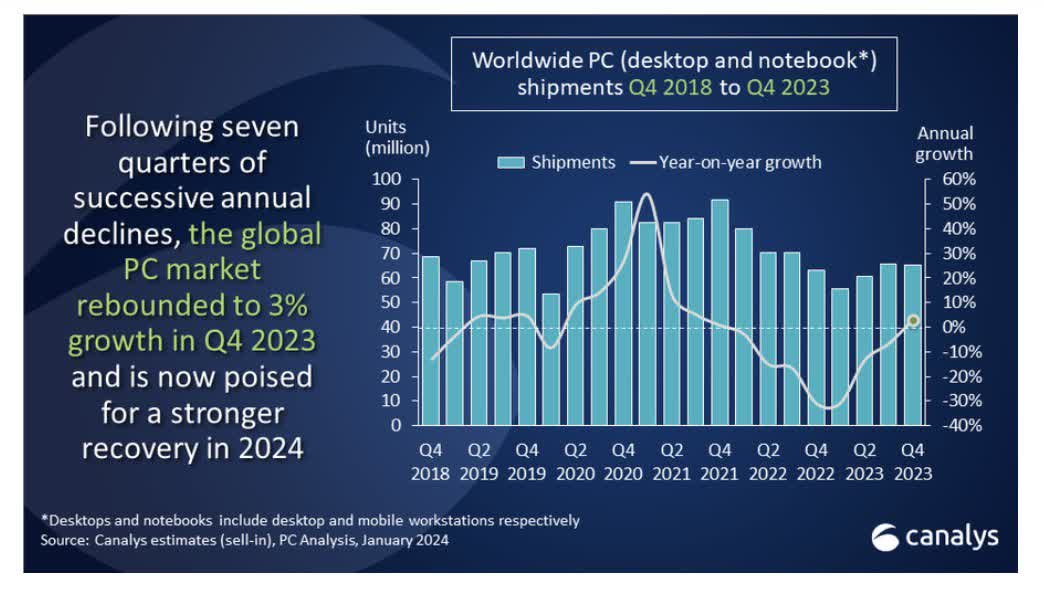

What investors also need to note is that after multiple quarters of weakness, industry-wide PC shipments witnessed some growth towards the end of the year (+3% in Q4-23), and it looks like positive momentum will only grow in FY24 with the new refresh cycle, and better consumer health.

{kind=link}

As a result of this, MPWR’s consumer division, a traditional mainstay will likely take a greater share of the overall sales mix this year, and that development could also have an inimical impact on the overall gross margins and the flow through to the bottom line.

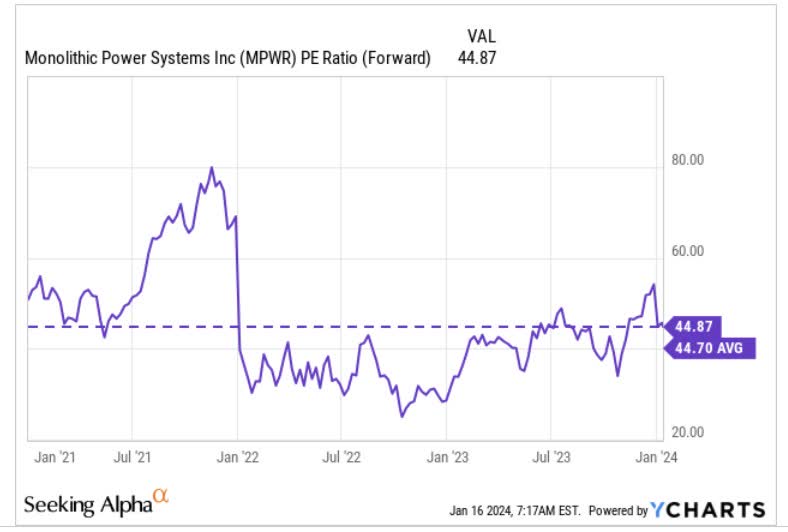

Consensus points to an EPS figure of $12.9, which would translate to EPS growth of only 10% (a lower pace than the topline growth of 12%). For a business offering 10% earnings growth this year, it is asking for a lot to shed out a forward P/E of nearly 45x, which is also slightly higher than the stock’s rolling 5-year average multiple.

{kind=link}

MPWR’s Sturdy Dividend Growth Trajectory May Ebb

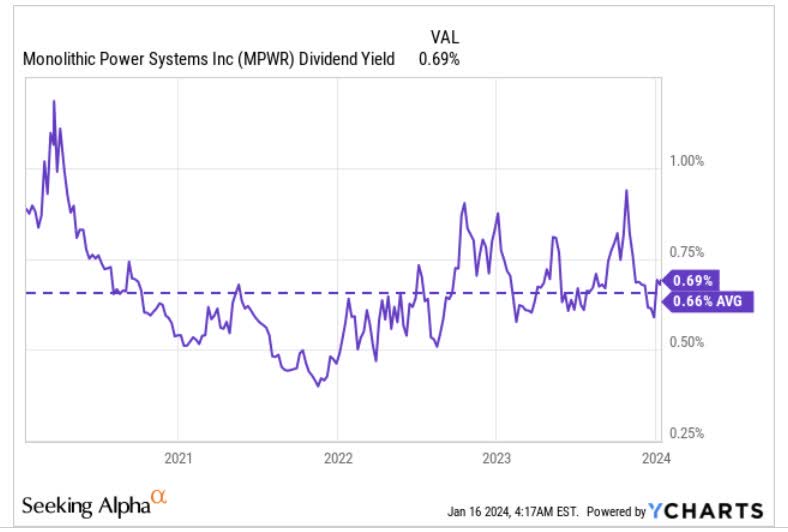

Prima facie, MPWR’s current dividend yield of 0.69% may not lighten up your eyes, but that figure doesn’t do justice to the impressive pace of dividend growth seen in recent years. To get a sense of this, note that even though the MPWR stock has witnessed price appreciation to the tune of over 220% over the last four years, the current dividend yield figure has not been hampered by the expanding denominator effect, and is still marginally better than the 4-year average of 0.66% .

{kind=link}

This speaks to the impressive dividend growth that MPWR has facilitated year in year out. For context, over the last three years, the annual hike in dividends has only continued to expand every successive year and the most recent hike was to the tune of 33%.

Seeking Alpha

Given this recent track record and with a record of over $1bn of cash &liquid investments sitting on the balance sheet, investors may be inclined to think that the pace of dividend growth may well expand by an even larger pace for the fourth year running. Whilst we are not ruling that thesis out entirely, we think it is more likely that one sees a step down in the pace of dividend growth.

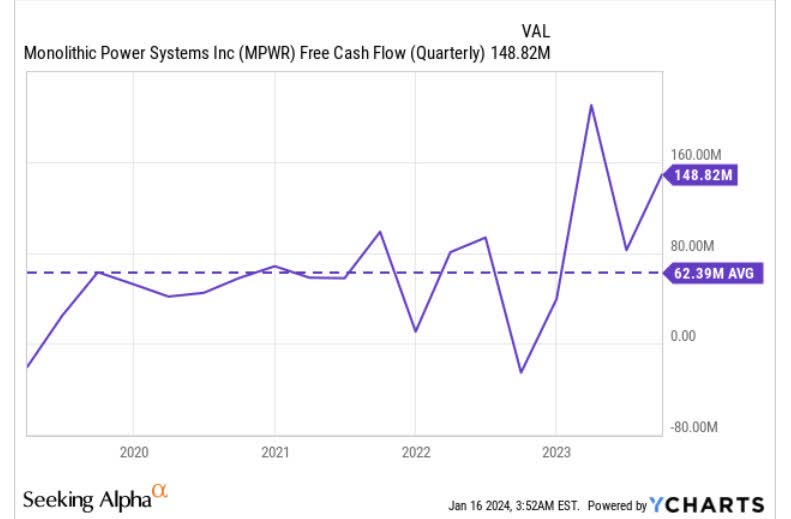

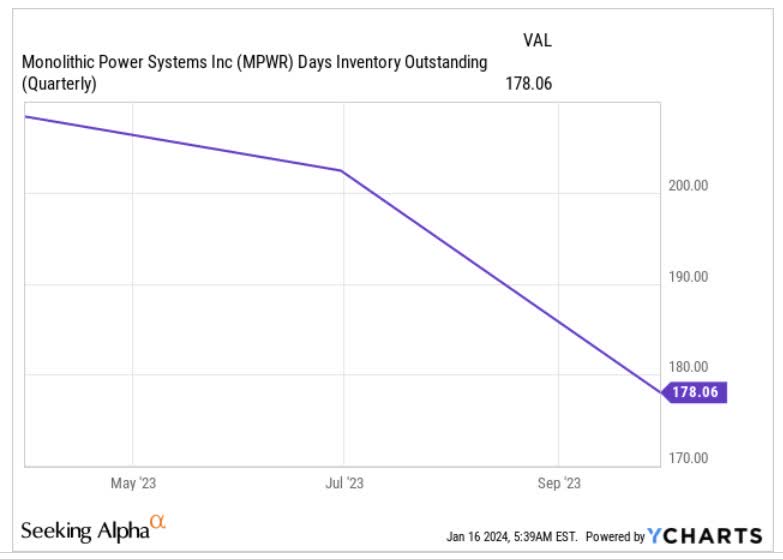

Our reasoning is primarily driven by what’s happening on the inventory front. Since Q1-23, MPWR has curtailed production and has been drawing down its inventory resources which have been dropped by around 15%. As a result, inventory changes have boosted the 9m-23 operating cash flow by +$50m as opposed to a -$138m drag in the previous period. However, on the Q3 earnings call , management did confirm that there would be a shift in the strategy over the next couple of quarters, as they seek to ramp up inventory in anticipation of the pickup in demand. As a result, expect inventory to start weighing adversely on the operating cash flow position again.

{kind=link}

Even otherwise, also consider that the FCF generation per quarter is already at quite steep levels of nearly $150m per quarter, and at some point, one has to be mindful of the ceiling effect. To get some perspective note that over the last 5 years, FCF generation per quarter has typically averaged only a little over $60m, so there are clearly downside risks here.

Even if the FCF doesn’t drop closer to historically average levels, investors should also note that MPWR will now have to divert over $210m per annum or around $52m of cash towards buying back its shares as part of the new $640m share buyback program that will run through the end of Oct 2026.

{kind=link}

Closing Thoughts - Unappealing Positioning On The Charts

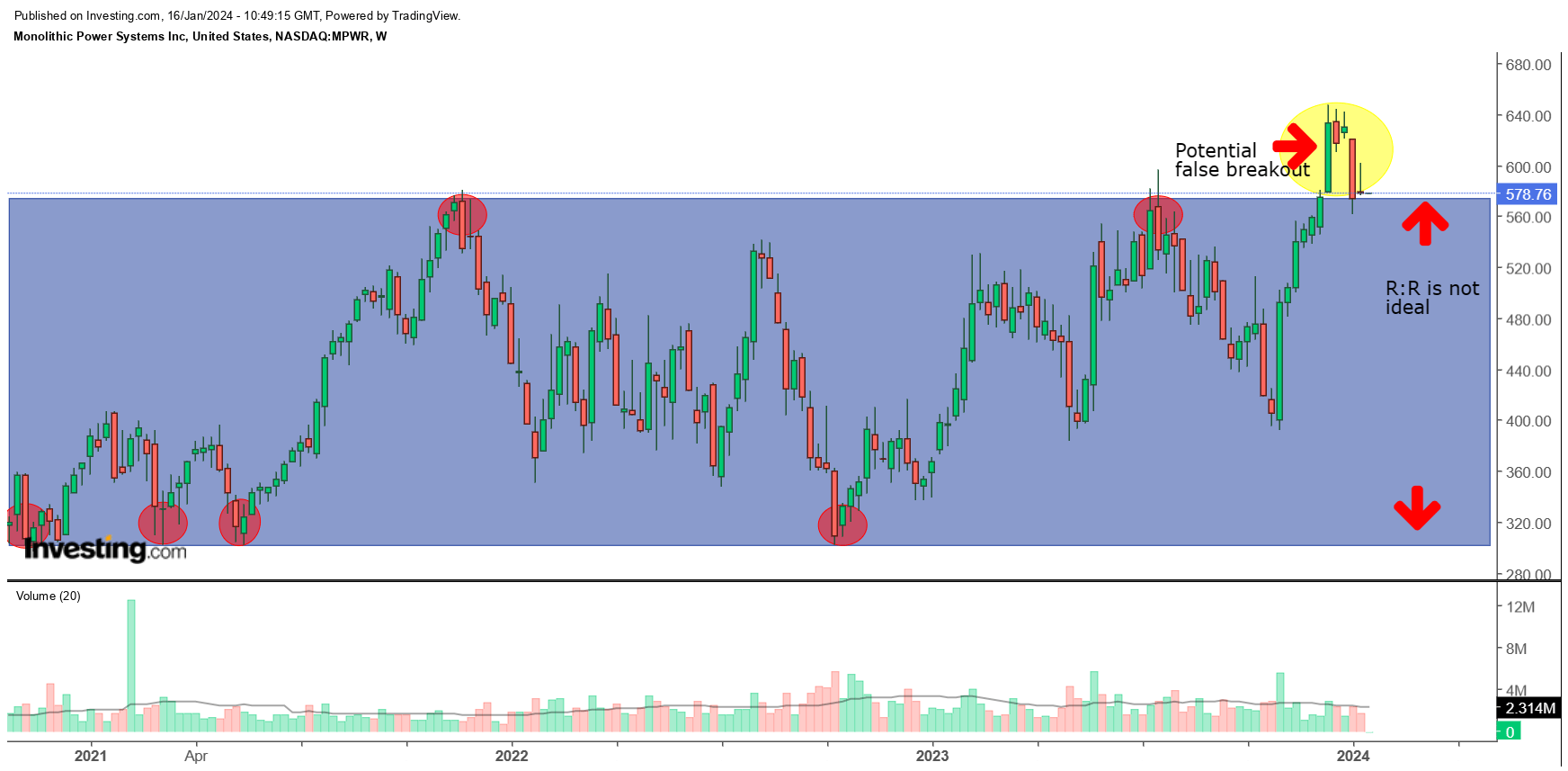

The underlying narrative on the charts suggests that MPWR won't make a great buy at this stage.

On MPWR's standalone weekly chart, we can see that the stock has formed an approximate trading range within the $300 to $600 levels. Whenever the price touches the boundaries of this range, we can see that it has recoiled from there (those points have been highlighted in red). That’s why we felt that when the stock broke out of this range in December last month, there was the risk of a sell-off. Well, in the ensuing weeks, it looks like what we have is a false breakout.

Given how steep the share price looks relative to the broad range, we don’t think the risk-reward is ideal for a long position.

{kind=link}

The long case is further dampened by how elevated the MPWR stock looks relative to its peers from the semiconductor space. The chart below shows how the relative strength ratio is now trading around 65% higher than the mid-point of the long-term range. Even if you think that ratio may not mean-revert, it’s also worth noting that this ratio has been trending up within a certain channel over the last two decades, and even within the channel the ratio looks quite overbought.

{kind=link}

For further details see:

Monolithic Power Systems: Curbing Our Optimism