MPWR - Monolithic Power Systems Inc - Excellent Balance Sheet But Rich Valuation

2023-05-18 15:02:04 ET

Summary

- Monolithic Power Systems saw a slight decrease QoQ in terms of revenues, but are still expected to end 2023 higher than 2022, unique among many other companies in the sector.

- Semiconductor companies are cyclical, but Monolithic seems to prove they have a diverse enough market to cater to that their revenues stay more resilient.

- The current valuation is too high though in my opinion and I rate the company a Hold.

Interlude

Monolithic Power Systems ( MPWR ) specializes in developing and producing advanced semiconductor solutions for a broad range of industries, including automotive, consumer electronics, and industrial applications. With a focus on power management technology, the company has established itself as a leading provider of high-performance power solutions. MPS offers a comprehensive product portfolio, which includes voltage regulators, power modules, motor drivers, and other power management products.

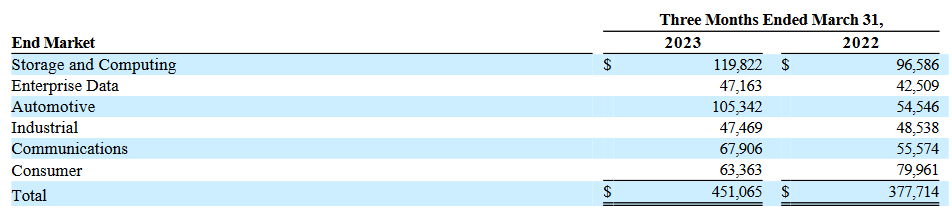

Company Revenues (Earnings Report Q1)

{kind=link}

The company has seen a quarterly decline in the last report as the market they are in has softened in terms of demand and pricing power isn't what it used to be, but this seems like a relatively short-term headwind though, even if manufacturers are warning it could go on longer. But estimates are that Monolithic will still be able to achieve a slight increase in the top line for 2023 compared to 2022. The company has managed to diversify its revenues and only 36% of revenues are generated in the United States. This puts them in a more stable position long-term in my opinion as they won't be dependent on a single market. The forward P/E though sits quite high at 34x earnings, which as far as I am concerned is too high to pay for a company that would be expected to generate around 10% CAGR for revenues in the next several years. The company is strong, however, and I don't doubt its ability to succeed in its market and rate it a hold until the valuation comes down.

Growth Opportunity

As mentioned previously, the semiconductor market as a whole has seen a loss in momentum as the market became saturated with an oversupply in certain areas and still lacking in others. Companies were finally able to fill up inventories and orders therefore declined in order to minimize the risk of overbuying and hurting margins.

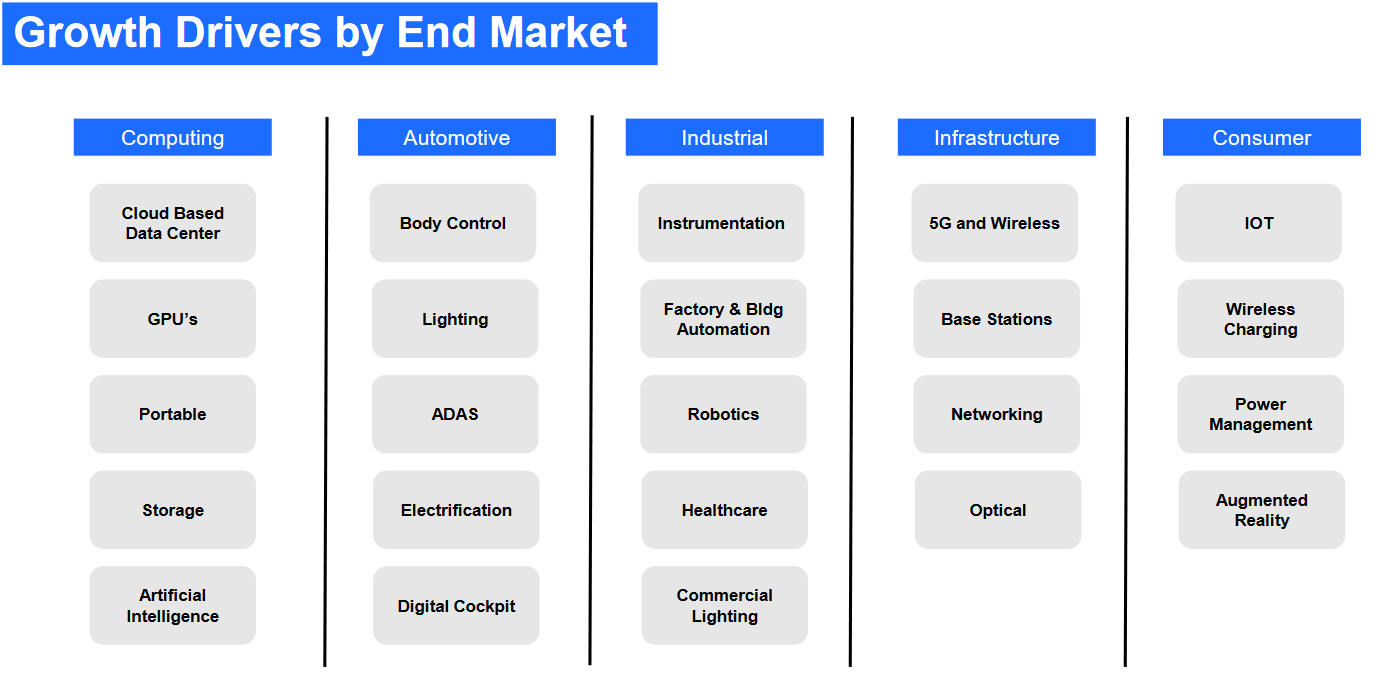

Company End Markets (Investor Presentation)

{kind=link}

I don't believe that Monolithic won't see any growth as they are both very diversified in terms of which regions they generate revenues from, but they are exposed to several end markets placing strong demand on semiconductor companies over the long term. In a report by Allied Market Research, they estimate the semiconductor industry to see a 6.21% CAGR between 2022 and 2031. Many of the drivers behind this growth will be the further advancements we are making in technology, semiconductors are these days in basically every electric appliance.

The semiconductor industry will continue increasing production and help ease the demand when inventories are running low. The industry is cyclical and often runs up when inventories shrink and companies are seeing increased demand and then placed massive orders to these semiconductor companies, causing a boom and bust cycle, much like any other commodity market. Often the tactic has been to buy when margins are horrible and valuation rich, but seeing as Monolithic isn't really expecting a slowdown in revenues, and the valuation is still high, I don't think the same tactic can be applied here. I think Monolithic is right now just a case of a company that ran up too high in valuation and needs to come down before an investment should be made. Boom and busts in their revenues are unlikely seeing as they have such a massive catalog of products to offer and can efficiently lean into certain areas when necessary to help stabilize revenues.

The Financial State

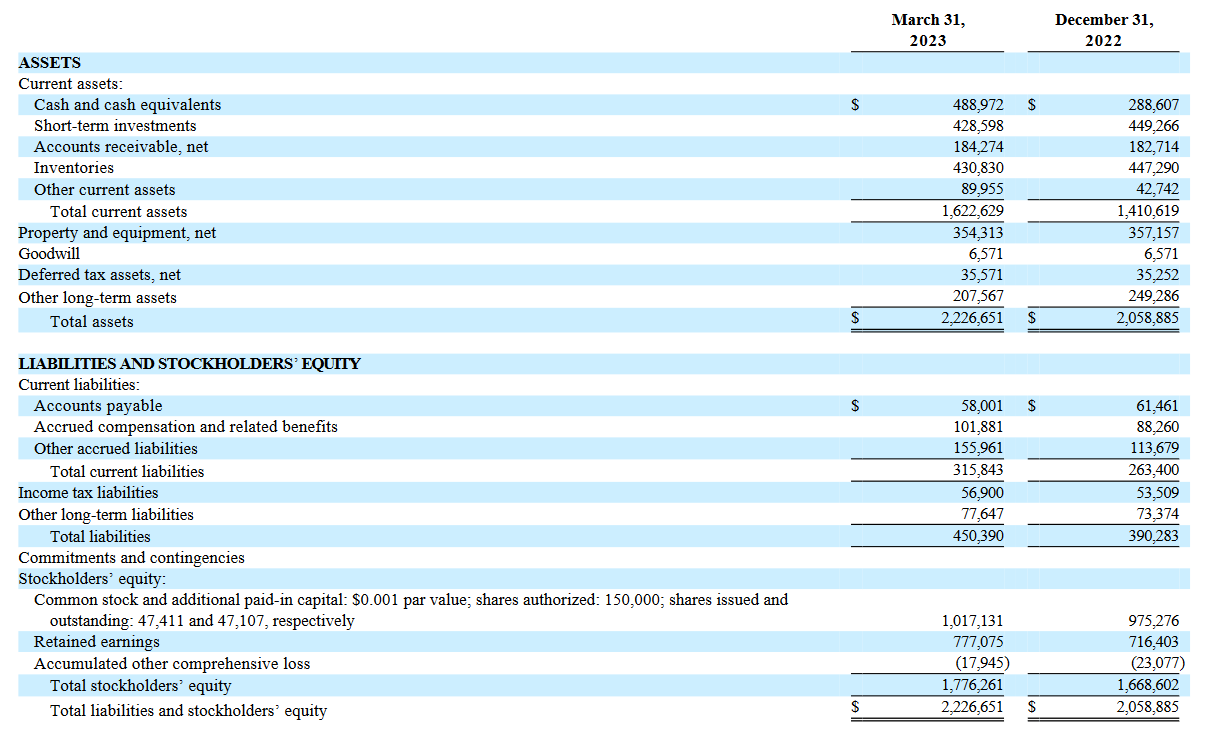

Looking at how the financials are for Monolithic, I think they are in fantastic shape. The cash position has seen an increase YoY, and by no small amount either, $200 million to be exact. I typically compare a company's cash position to the amount of debt outstanding, but Monolithic doesn't have any long-term debts right now. The $488 million cash position can in my opinion be quite heavily used to fund expansion .

Balance Sheet (Earnings Report Q1)

{kind=link}

This cash position will make it easier for the company to also continue distributing a dividend, which right now sits near a 1% yield. With no long-term debts, the net debt for the company sits negative at $1.1 billion right now. I think there is a clear case to be made that Monolithic can afford to take on more debt to grow their business, and do it faster than competitors. They don't hold a massive market share, but in my opinion, there's a possibility to take more. Especially with a 17% FCF margin, the need to dilute shares as they have done should no longer be necessary. They are in a strong financial state; raising capital this way is not the route to go when you have nearly $500 million in cash. Monolithic will need to keep up, at least if the current valuation could ever be justified.

Company Risks

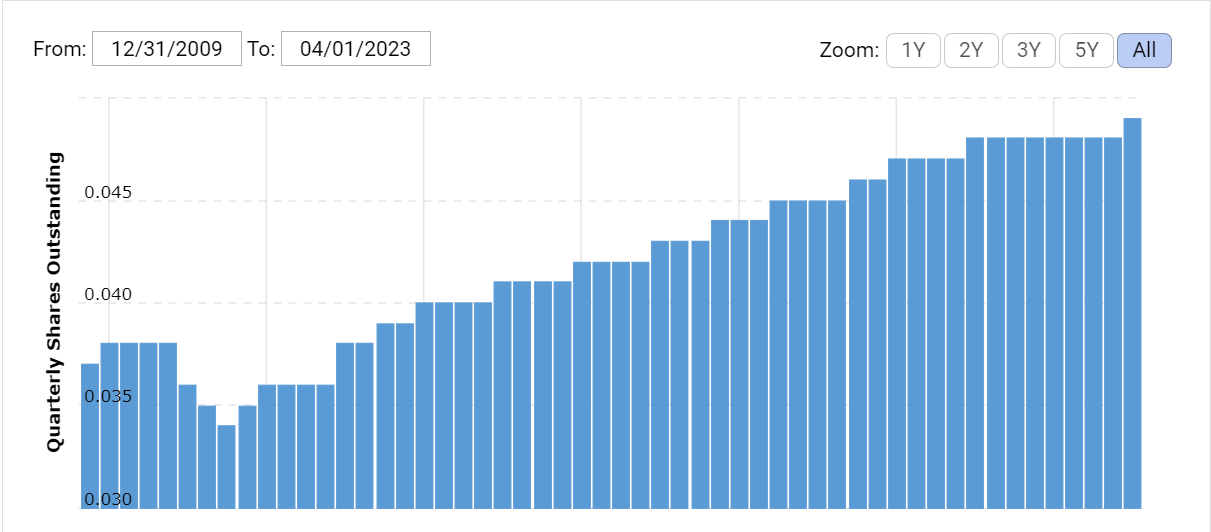

One of the main shortcomings has been Monolithic's share dilution over the last few years. Steadily increasing share count by around 1% each year, it does hurt investors quite significantly over the long term. Most of it is coming from stock-based competition, which came in at $160 million in 2022.

Shares Outstanding (Macrotrends)

{kind=link}

What I would prefer to help make the long-term case for the company more appealing is the introduction of a buyback program. With strong FCF margins and no debt on the balance sheet, they are in a fantastic position to start giving back to shareholders. Their revenues are diversified, with a massive catalog of revenues and no single dependence on a market or region. With over $300 million in levered FCF, they can at least keep up the dividend. Where I can see the argument for not introducing a buyback program is that the current valuation might not scream a buy, with the forward P/E at 34.

Company Takeaway

As mentioned before, I don't think the company is a buy right now when the valuation sits this high. If the estimated top line was near 20 - 30% YoY, then I could see the valuation being justified. But that doesn't seem to be the case with Monolithic. There is no shortage of companies in the semiconductor industry, and I think there are better opportunities out there than Monolithic right now.

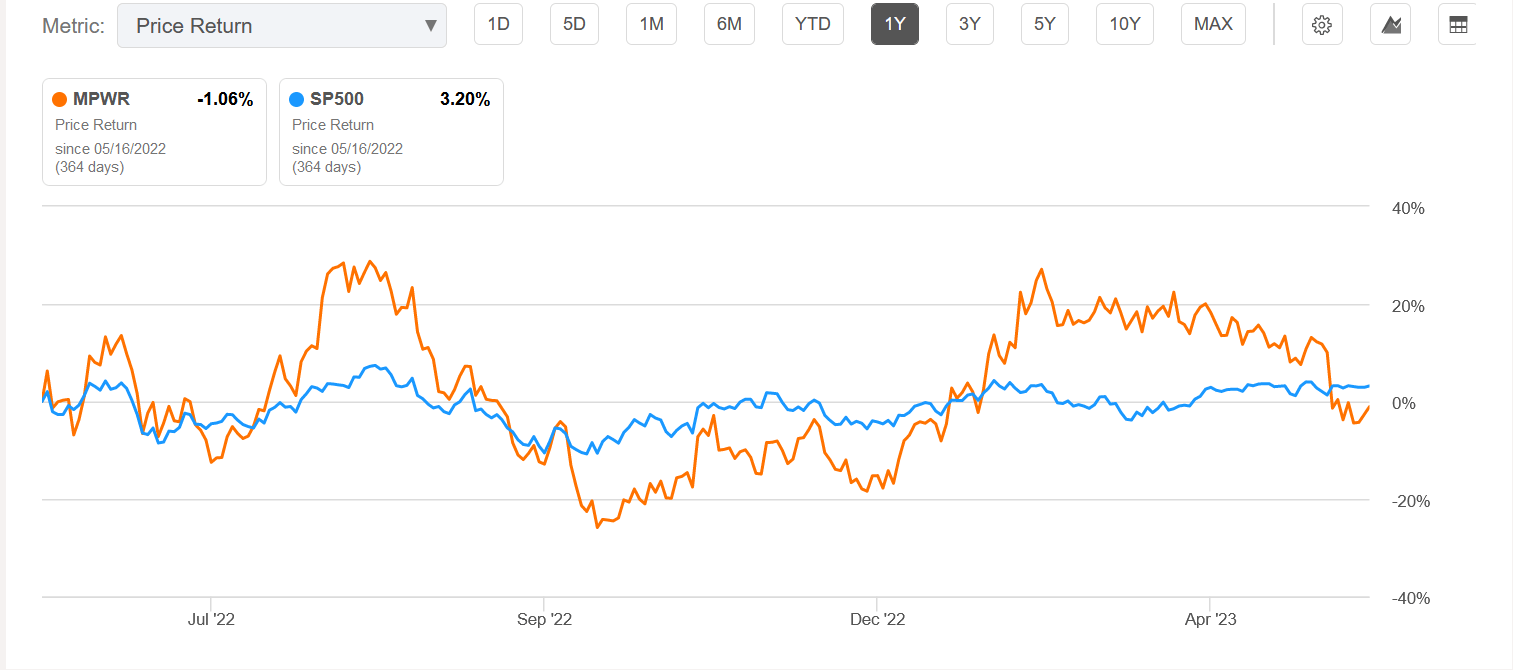

MPWR vs S&P 500 (Seeking Alpha)

{kind=link}

A company like Microchip Technology Incorporated ( MCHP ) has a phenomenal balance sheet too and good growth prospects which should mimic the same as the industry. But perhaps most importantly, you wouldn't be buying MCHP at the same premium as Monolithic. MCHP has a forward P/E of only 12x, which presents a better opportunity to any investor seeking broad exposure to the semiconductor market, in my opinion. To conclude, I think Monolithic Power Systems is a hold for now until there is a compression in the valuation. Paying 34x forward earnings is too much, and I am happy to wait on the sidelines a little if it means getting a better deal.

For further details see:

Monolithic Power Systems Inc - Excellent Balance Sheet But Rich Valuation