MRCC - Monroe Capital: 3 Reasons To Avoid This BDC

2023-12-26 17:18:43 ET

Summary

- Monroe Capital is a small BDC and relatively unpopular one with a market cap of ~$150 million providing financing for companies in the US and Canada.

- Portfolio-wise the structure is quite conventional with ~80% located in first lien and a nice distribution among various sectors without any major focus into speculative areas.

- Yet, the fact that MRCC has one of the most indebted balance sheets and fully exhausted dividend coverage renders this investment overly speculative, even considering 14.4% yield.

- The recent dynamics on the NAV front (i.e., material write-downs) reveal some early signs of potential consequences.

Monroe Capital (NASDAQ: MRCC ) is a relatively small and unpopular BDC, which provides financing primarily to lower middle-market companies both in the U.S. and Canada.

The most preferred investment types by MRCC are primarily associated with senior, unitranche and junior secured debt. According to MRCC's investment policy , unsecured subordinated debt and equity are also possible, but the reliance on these investments is not that material.

MRCC Investor Presentation

More than 85% of the total exposure is explained by debt-like investments, which is critical to match the assets with liabilities and at the same time to accommodate stable streams of dividend payments. Compared to the BDC sector, ~80% exposure to first lien could be considered in line with the average (i.e., not too conservative and not too aggressive either).

MRCC Investor Presentation

In terms of the industry exposure, MRCC is rather diversified with a slight bias towards real estate, healthcare & pharma, and business services. Although there is a bit of concentration risk in these three industries, none of them are overly speculative with ambiguous business models. The remaining industries are rather straightforward as well without excessive volatility.

{kind=link}

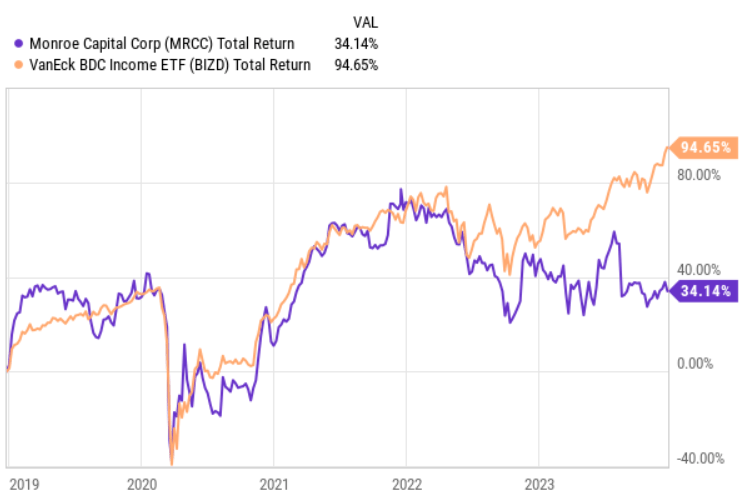

Performance-wise MRCC has historically delivered similar returns to the overall BDC market, but starting from mid 2022 when the effects from stricter monetary policy started to percolate through the system, it has significantly diverged from its peers.

Let me now elaborate on why I think that going forward, MRCC will likely continue to lag behind the index despite currently offering a massive dividend yield of 14.4%, which is roughly 350 basis points above the BDC average.

3 Reasons to avoid MRCC

Low margin of safety in the dividend coverage

For BDCs to preserve NAV base, protect dividends and have a buffer in the case of deteriorating investment performance, it is very crucial to possess a healthy dividend payout profile. Namely, it is recommended to have cash based or core NII (i.e., excluding equity gains) above the distributed dividend levels.

{kind=link}

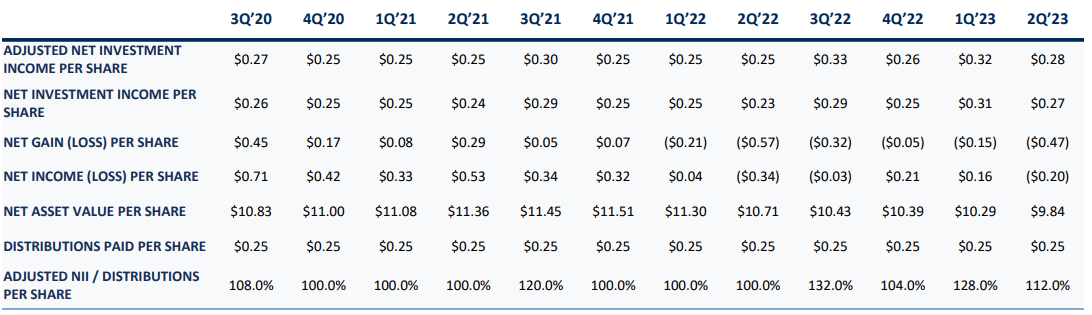

Historically, MRCC has walked on a very thin ice by just barely covering the dividend distributions with the adjusted NII results. This is even after a major drop in the DPS at the beginning of 2020.

For example, the most recent financial quarter for MRCC ended with 100% dividend coverage - i.e., adjusted net investment income per share perfectly matching the distribution level per share.

Too aggressive leverage

If we compare MRCC's debt to equity profile with that of the average BDC name, we will notice a quite unpleasant situation.

BDC WEEKLY INSIGHT INSIGHT | RAYMOND JAMES INVESTMENT BANKING

MRCC is way above the average debt to equity level of BDC peers. During the Q3, 2023, MRCC's leverage increased from 1.54x to 1.60x.

It is worth underscoring that the increase in leverage has happened during one of the most favourable times for BDCs when many peers have assumed a road of de-risking their balance sheets to shield the NAV from the looming crisis and corporate default uncertainty.

Given the already exhausted dividend coverage capacity, having one of the most aggressive external debt positions in the industry does not help and contribute to an elevated probability of dividend cut and/or sharp loss in the NAV base.

Early signs of consequences

Looking at Q3, 2023 results we can already notice some unpleasant dynamics in MRCC's books.

According to Ted Koenig - Chairman & Chief Executive Officer - the Management was forced to write off a notable chunk of the NAV due to material defaults of some portfolio constituencies; excerpt from the most recent earnings call :

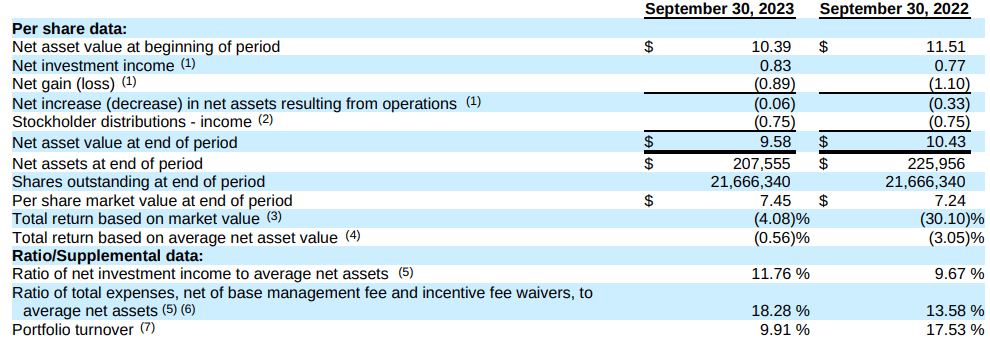

We also reported NAV of $207.6 million or $9.58 per share as of September 30, 2023 compared to $213.2 million or $9.84 per share as of June 30, 2023. The decline in NAV was primarily attributable to net unrealized losses on the portfolio attributable to a few specific portfolio companies that were affected by idiosyncratic factors as well as a decrease in value at SLF, which was driven by unrealized mark-to-market losses.

In other words, adjusted for the NII component, MRCC has recognized $0.89 NAV per share impairment this year, which has exceeded the underlying NII amount generated by the portfolio investments. Interestingly, last year under a comparable period, MRCC made similar NAV corrections, which were also higher than the relevant NII figure.

{kind=link}

Plus, it is worth mentioning that during Q3, 2023, MRCC did not incorporate incremental write-downs, which could be considered a deviation from the norm, where in most of the previous quarters (since the Fed decided to hike) MRCC actually classified loans under non-accruals.

Obviously, this is a high degree of speculation, but theoretically it could be so that MRCC has decided to back-end load some of these struggles in order to avoid even more painful results (i.e., NAV loss) in Q3'23.

The bottom line

In my opinion, MRCC is not a BDC for prudent investors, who want to count on stable streams of dividend income. The current dividend yield of 14.4% is indeed relatively high, but because it is also characterized with significant risks, it is hard to rely on these income streams going forward.

The combination of extreme leverage (one of the highest in the sector) and already exhausted dividend coverage renders this BDC overly speculative, especially against the backdrop of looming recessionary risk.

For further details see:

Monroe Capital: 3 Reasons To Avoid This BDC