KDP - Monster Beverage: A Good Hedge Against Coming Economic Slowdown

2023-10-22 09:18:18 ET

Summary

- In case of a recession, Monster Beverage could help investors weather the downturn in earnings and stock prices in the broader market.

- MNST stands out with its reinvestment of earnings in business growth, high ROIC, clean balance sheet, and resilient product portfolio.

- The key risk is that MNST's valuations are elevated, and the company is priced more like a high-growth tech stock than a consumer staples stock.

- Despite its high valuation, MNST has consistently outperformed the broader market and will likely remain an outperformer in the event of an economic slowdown.

The waning strength of US consumers has been an issue of growing concern for investors and other market participants all through the year. Back in June, major retailers like Macy's ( M ), Home Depot ( HD ) and Lowe's ( LOW ) warned that consumers were slowing down on spending. Signs of weaker consumer spending in the economy are now beginning to show in the banking system, with Brian Moynihan, CEO and Chairman, Bank of America ( BAC ), stating in a recent interview that median income households have lower account balances and are spending down their pandemic savings.

"Consumers' activity has slowed down ... it's slowed by half, and that means the consumer is being slowed down by the interest rate environment and all the stuff going on," said Moynihan on CNBC. He explained that, in a given year, the bank's customers spend $4 trillion. From 2021 to 2022 that spend grew by 10%. It began dropping to 9% in Q1 2023 and now that growth figure has dropped to 4.5%.

Weaker consumer spending and the possibility of a recession are signs that investors may need to start thinking about adding consumer staple stocks to their portfolios. These stocks are often considered safe bets during an economic slowdown since they sell essential items like food and personal hygiene products. One stock in this category that is worthy of consideration is Monster Beverage Corporation ( MNST ), the maker of some of the most popular energy drinks in the US and globally.

Differences and similarities with other consumer staple stocks

Most consumer staple stocks pay a solid and stable dividend. MNST, however, pays no dividend at all but reinvests its earnings into the business. This is one of its key differences from other consumer staple stocks.

Foregoing dividends makes sense for a long-term investor in MNST in view of how rapidly the company has expanded its topline and bottom line in the past 5- 10 years. MNST's historical financial statements show that the business has grown revenue in leaps and bounds over the past decade.

| TTM |

| 2020 |

| 2017 |

| 2013 |

| Revenues |

| $6.69 billion |

| $4.59 billion |

| $3.36 billion |

| $2.24 billion |

| Net income |

| $1.43 billion |

| $1.40 billion |

| $820.7 million |

| $338.7 million |

Source: Seeking Alpha

Importantly, MNST has been able to achieve this strong financial performance while keeping its balance sheet squeaky clean. The California-based company has virtually no debt, having reported cash and short-term investments of $3.28 billion vs total debt of just $40.9 million in the most recent quarter.

Monster's clean balance sheet (Seeking Alpha)

Thanks to its clean balance sheet, low cost of capital, and consistently strong commercial performance, MNST has been able to maintain an impressive average return on invested capital ((ROIC)) of 25.2% for fiscal years ending December 2018 to 2022, according to data from Finbox . ROIC is a key performance metric because it shows how efficiently management uses funds raised through debt and equity to turn a profit. Exceptionally high returns above 20% mean the underlying business has high margins and carries low level of debt, as is the case with MNST. A business with a high ROIC makes better use of its capital reinvesting profits than paying dividends.

While MNST doesn't pay a dividend like most consumer staple stocks, it has one striking similarity with every other consumer staple stock out there: that is, consumer demand for its products is resilient to multiple external shocks.

MNST's revenues and product volumes have grown healthily and steadily in recent years despite an endless series of economic, geopolitical and public health shocks. People keep buying the company's drinks no matter what's happening in the economy, in the news or the wider world. As a pointer to this, the company's revenues have grown steadily since 2019 to date, despite multiple shocks over this period such as the Covid-19 pandemic, the Russia-Ukraine war, inflation and rising interest rates, and the current economic slowdown and fears of recession.

The odds greatly favor Monster

If MNST has been resilient in the past few years (even after all that has happened in terms of inflation and the cost-of-living crisis, rising interest rates, multiple wars and geopolitical shocks, and Covid), what are the odds that the coming economic slowdown will negatively impact its performance? This in my view is the central question investors need to ask when assessing MNST's prospects as an investment opportunity in a recessionary environment.

I believe that, going forward, MNST will likely keep performing as well, just like it has in recent years when it overcame the challenging macroeconomic and geopolitical backdrop and maintained its growth trajectory. The odds greatly favor the company, going by its most recent performance for Q2 2023 and H1 2023 as well as analysts' projections for 2023 and 2024.

MNST posted record performance in the second quarter of 2023. Net sales were $3.55 billion for the six-months ended June 30, 2023, an increase of approximately $380.1 million, or 12.0% higher than net sales of $3.17 billion for the six-months ended June 30,2022, according to the company's SEC filings . The company is expected to earn revenues of $7.17 billion in 2023 and $8.00 billion in 2024, according to consensus estimates from Wall Street analysts covering the stock. MNST's consensus EPS is expected to expand to $1.54 in 2023 and $1.80 in 2024, from $1.13 in 2022.

If these projections materialize, or MNST surpasses them, shareholders will likely continue enjoying high stock prices given the company's significantly high margins, which have historically contributed to strong EPS growth and share price appreciation.

Monster enjoys high margins (Seeking Alpha)

A proven winner over time

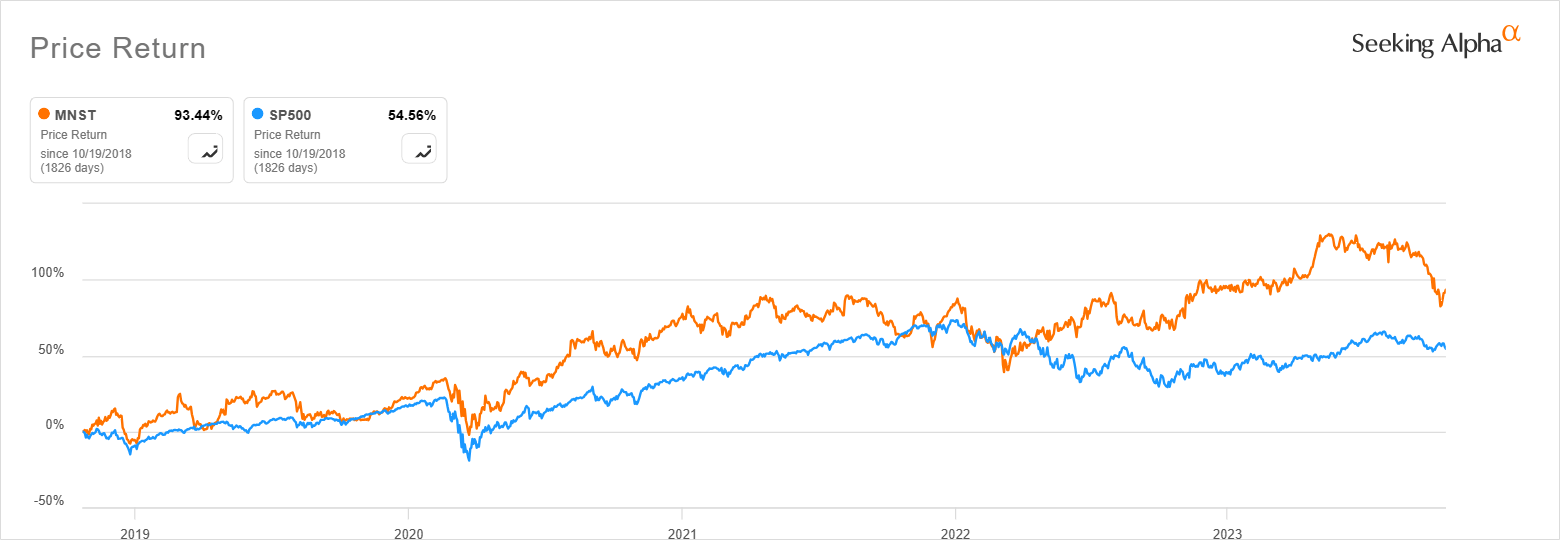

In the past five years, MNST has handily outperformed the S&P 500, delivering a return of 93% vs the S&P's 54%. Assuming predictions of a recession come true, investors will likely flock to stocks like MNST that can beat the market in times of turmoil - just like they have in the past few tumultuous years. This means that MNST's outperformance could likely accelerate in coming quarters and years as fears of an economic slowdown take hold in the market and investors flee to companies like MNST that have a proven history of growing profitably in turbulent times.

MNST has outperformed the market in the past 5 years (Seeking Alpha)

{kind=link}

MNST is a market darling that counts The Coca-Cola Company ( KO ) as one of its key shareholders and strategic partners. KO bought a stake in MNST in 2015 as part of a strategic partnership involving an equity investment and expanded distribution in the global energy drink category. In connection with the closing of this deal , KO made a net cash payment of approximately $2.15 billion to MNST.

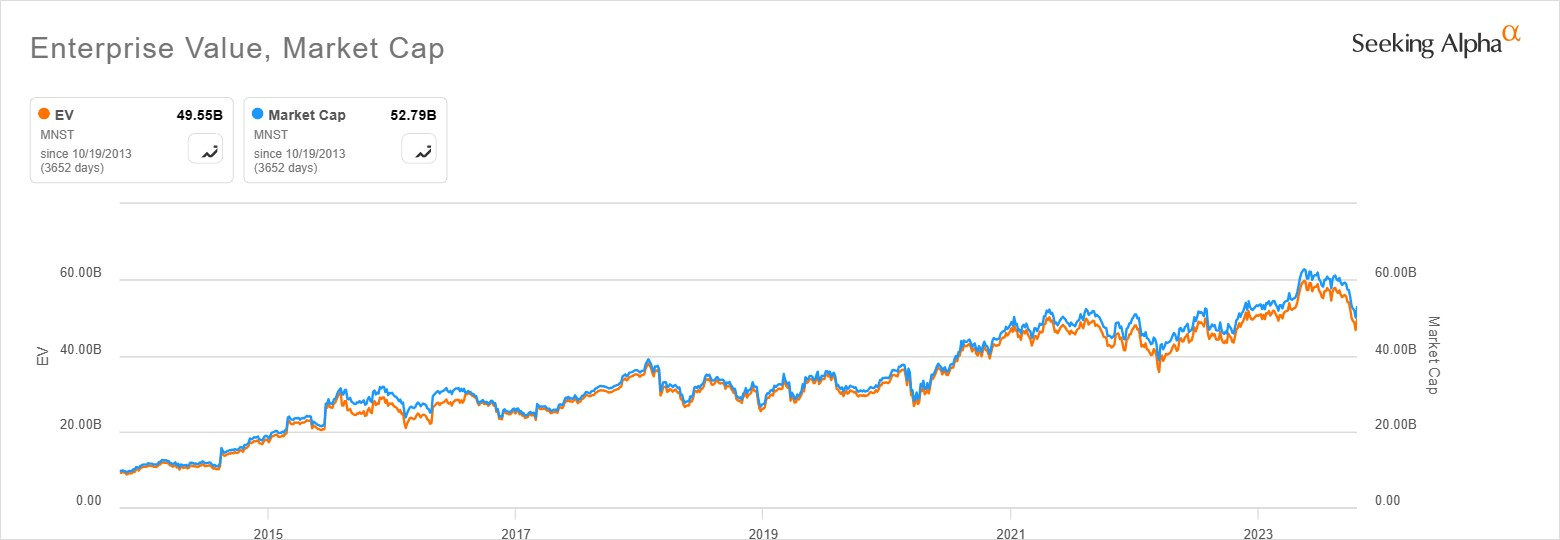

With the caveat that "past results are not an indicator of future performance", a look at MNST's historical performance shows that it's been a consistently superior performer. Not only has it outperformed the S&P by almost 100% in the past five years, but its valuation in terms of market cap and enterprise value has increased more than fivefold in the past 10 years.

Monster's valuation has increased fivefold in past decade (Seeking Alpha)

{kind=link}

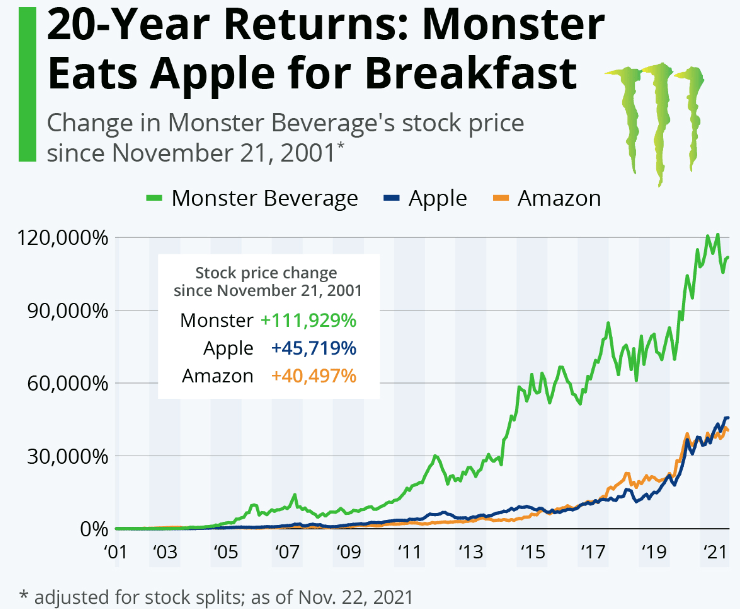

Its noteworthy that since the turn of the new millennium, MNST has delivered a significantly higher return for investors than Apple ( AAPL ) and Amazon ( AMZN ).

"When you ask people to guess the best-performing stock in the S&P 500 over the past 20 years, the answers would probably be pretty tech-heavy. Apple? Amazon? Microsoft or Google maybe? Well, it's neither," notes Statista data journalist, Felix Richter, in an insightful Nov 2021 chart and article comparing the 20-year stock performance of MNST to those of AAPL and AMZN.

MNST significantly outperformed AMZN and AAPL in the past 20 years (Statista)

{kind=link}

The main risks and key catalysts

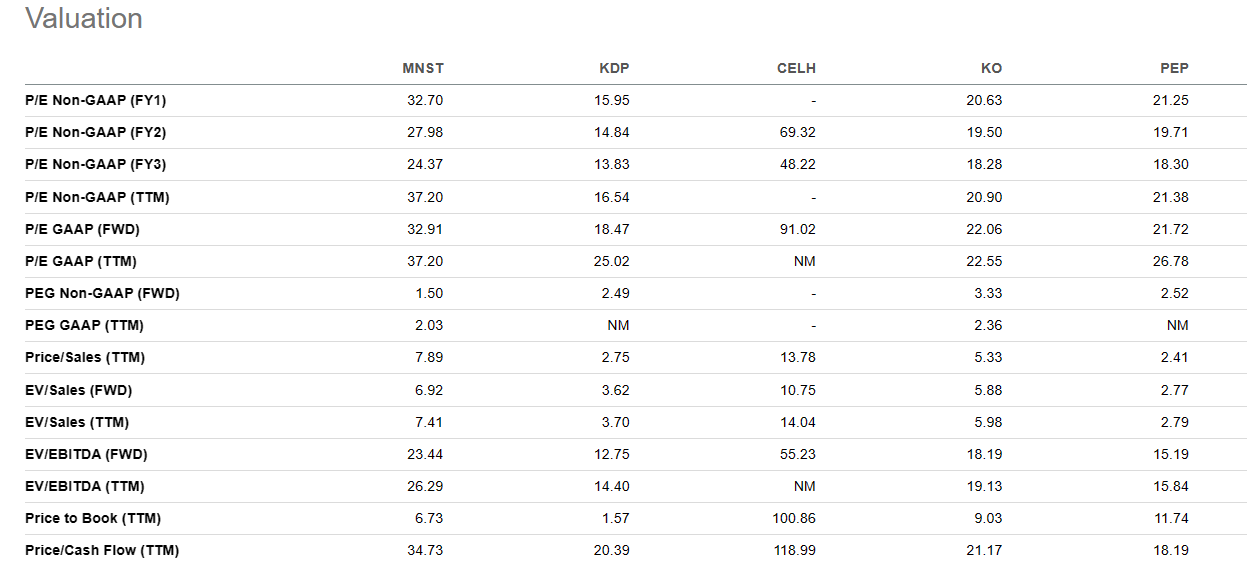

While buying MNST to weather a possible coming economic slowdown doesn't seem like a bad idea. I'm cautious about the stock's valuation . It has a P/E ((FWD)) of 32.91 and an EV/EBITDA ((FWD)) of 23.44 vs the consumer staples sector's median P/E ((FWD)) of 17.63 and median EV/EBITDA ((FWD)) of 10.60.

In comparison to other leading beverage makers, MNST is also priced at a premium. The chart below, comparing MNST vs KO, PepsiCo ( PEP ) Keurig Dr Pepper ( KDP )and Celsius Holdings ( CELH ), shows that, with the exception of CELH, Monster is expensive when compared to peers.

{kind=link}

MNST's high valuation metrics could be a sign that the stock has limited future returns, so investors need to proceed cautiously. I don't, however, hold this to be the case and instead believe the company will keep growing profitably and enjoying high margins. MNST is in my view priced more like a high growth tech stock than a consumer staples stock, hence the high P/E. Its noteworthy that large tech companies like AAPL and AMZN, both of which MNST has outperformed in the past 2 decades, have valuation metrics as high or higher than MNST. AAPL has a P/E ((FWD)) of 28.98 while AMZN has a P/E ((FWD)) of 59.70.

In terms of the main positive catalysts for investors to keep an eye on, the two main ones are MNST's ability to continue driving growth with zero debt, and the strong brand equity that the company has built with consumers.

One of the most reliable indicators of a brand's strength with consumers is the ability for a company to increase prices and still report improved volumes. Due to continued cost pressures, MNST implemented price increases in 2022 and the first half of 2023.

"We will continue to review further opportunities for pricing actions in order to mitigate inflationary pressures," noted Chairman and Co-CEO Rodney Sacks in the Q2 2023 earnings call . Its noteworthy that, despite these price increases, SEC filings show that MNST case sales for MNST's energy drink products, in 192-ounce case equivalents, were 380.8 million cases in H1 2023, an increase of approximately 27.8 million cases or 7.9% higher than case sales of 353.0 million cases in H1 2022. The company's volumes have grown robustly even after prices went up, underlining its strong brand among consumers.

Conclusion

MNST's popularity with consumers, its high-growth, high margin underlying business, and its clean balance sheet have given it the freedom to experiment in new areas like alcoholic beverages. The company's efforts in the alcohol drinks segment could help sustain long-term growth even further. While MNST's valuation looks rich today, it could still deliver a strong return over the long-term and act as a good hedge against the potential recession coming our way.

For further details see:

Monster Beverage: A Good Hedge Against Coming Economic Slowdown