MCO - Moody's: Dominant Business But A Little Pricey

2023-06-06 08:22:12 ET

Summary

- Moody's is a dominant market leader underpinned by a wide economic moat.

- Revenue was down by 12% in 2022 due to the backdrop in bond issuance.

- The company has a good track record of allocating capital.

- I assign a hold because I believe the company is fairly valued at its current price.

Thesis

Moody's Corporation ( MCO ) operates a duopoly with S&P Global ( SPGI ) in the credit rating industry. Moody's is a dominant market leader with a wide economic moat and a flawless track record of capital allocation. Additionally, 69% of the company's revenue is recurring, which I believe should support profitability during economic hardship. Despite Moody's great track record, I assign a hold because the company seems fairly valued at $327 per share, plus MCO isn't doing as well as its competitor, SPGI. I will explain each of the key drivers of my thesis below.

Company Description

Moody's Corporation is a global integrated risk assessment firm providing credit rating opinions, analytical solutions, and insights that empower organizations to make better, faster decisions. The company operates in two segments: Moody's Analytics and Moody's Investment Services.

Business Segments

Moody's Analytics (52% Revenue, 37% Adjusted Operating Income)

MA is a subscription model with high retention rates. This segment offers a gamut of risk-related data and analytics content, including credit research, quantitative credit scores, economics research, business intelligence, know-your-customer tools, commercial real estate data, training services, ESG, and risk management software for financial institutions. 94% of MA's revenue is recurring. Segment revenue increased by 15% YoY, while total revenue declined by 12%. I believe that this segment is set to benefit from the growing interest in ESG. The company guided for low-to-mid-teens percent growth in the medium term in its investor presentation for Q1 23 .

Moody's Investor Services (48% Revenue, 63% Adjusted Operating Income)

MIS provides investors with credit ratings, risk analysis, and research for stocks, bonds, and government entities. This segment is heavily influenced by macro conditions. MIS's revenue declined by 30% in 2022, mainly due to bond issuance. I believe that as macro conditions (interest rates and inflation) get better and GDP growth resumes, revenue should rebound. The company guided for low-to-mid-single-digit growth in the medium term in its investor presentation for Q1 23.

Economic Moat

I assign Moody's a wide economic moat because of their network effect, intangible assets, and toll moat. What do I mean by network effect"? Well, bond investors value credit ratings and credit ratings provide value to bond investors, and so forth. The more customers use Moody's services, the more valuable they become. In my opinion, it is extremely difficult for a new company to break into credit ratings. It might take them years just to establish credibility, let alone have repeated customers. Moody's has been around for more than 100 years. This means the company has established relationships with thousands of companies and investors who value their ratings. The company's brand is associated with credit ratings and credit risk. A toll moat is when a business is a supplier of something the customer needs. Bond investors and bond issuers aren't the only ones that value credit ratings. Index providers and government regulators do too. For example, the Bloomberg U.S. Aggregate Bond Index only considers ratings from either S&P, Moody's, or Fitch. This makes Moody's services a must if a company or government wants its bond to be credible. I believe that the competitive advantages listed above will help Moody's keep hold of its market position in the near future.

Capital Allocation

Moody's has done a stunning job of deploying its capital. The company has used capital for strategic acquisitions, dividends, and share repurchases. MCO has made three key acquisitions in the last six years. Bureau van Dijk, a European provider of privately held company data, for $3.5 billion in 2017, RDC, a provider of anti-money laundering and KYC tools, for $700 million in 2020, and RMS, a provider of climate analytics, for $1.9 billion in 2021. The company had a dividend payout ratio of 37% in 2022. Moody's has spent $3.4 billion on share repurchases in the last five years. This benefited EPS by decreasing average diluted shares by 5% in the past 5 years. MCO's 5-year average ROIC is 23.08%. Overall, I think the company has done a good job allocating capital and shareholders have benefited from that. I believe that capital allocation is crucial for a business because if a company is successful in reinvesting capital, it can expand its operations and return more money to shareholders through share repurchase programs and dividends, and Moody's has done just that.

Competition

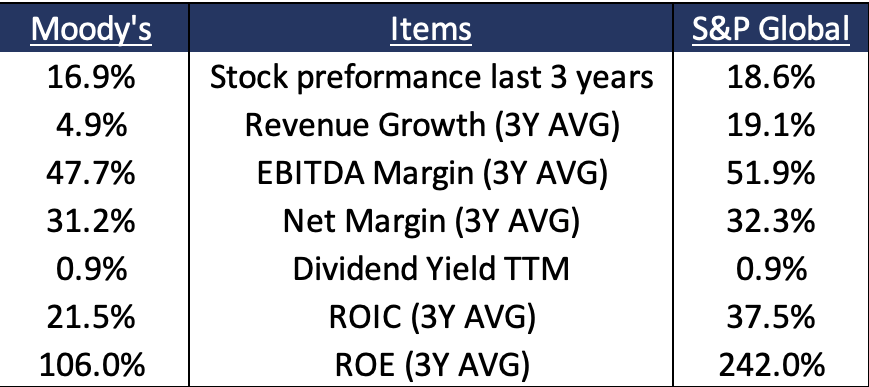

Moody's has multiple competitors, including Bloomberg, Morningstar, and Fitch. But perhaps their biggest competitor is S&P Global. Below is a table comparing both companies in some key items.

{kind=link}

Despite SPGI's better performance, both companies' stocks have performed fairly well in the past 3 years. Moody's stock has outperformed SPGI's in the past 5 years by 2%. It is worth mentioning that SPGI's revenue is more diversified beyond ratings and analytics. Plus, Moody's is more exposed to macro conditions. In 2022, Moody's revenue declined by 12% due to the backdrop in the bond market, while SPGI's increased by 22%. In 2020, SPGI completed its merger with IHS Markit to expand its analytics segment and diversify the business even more.

Valuation

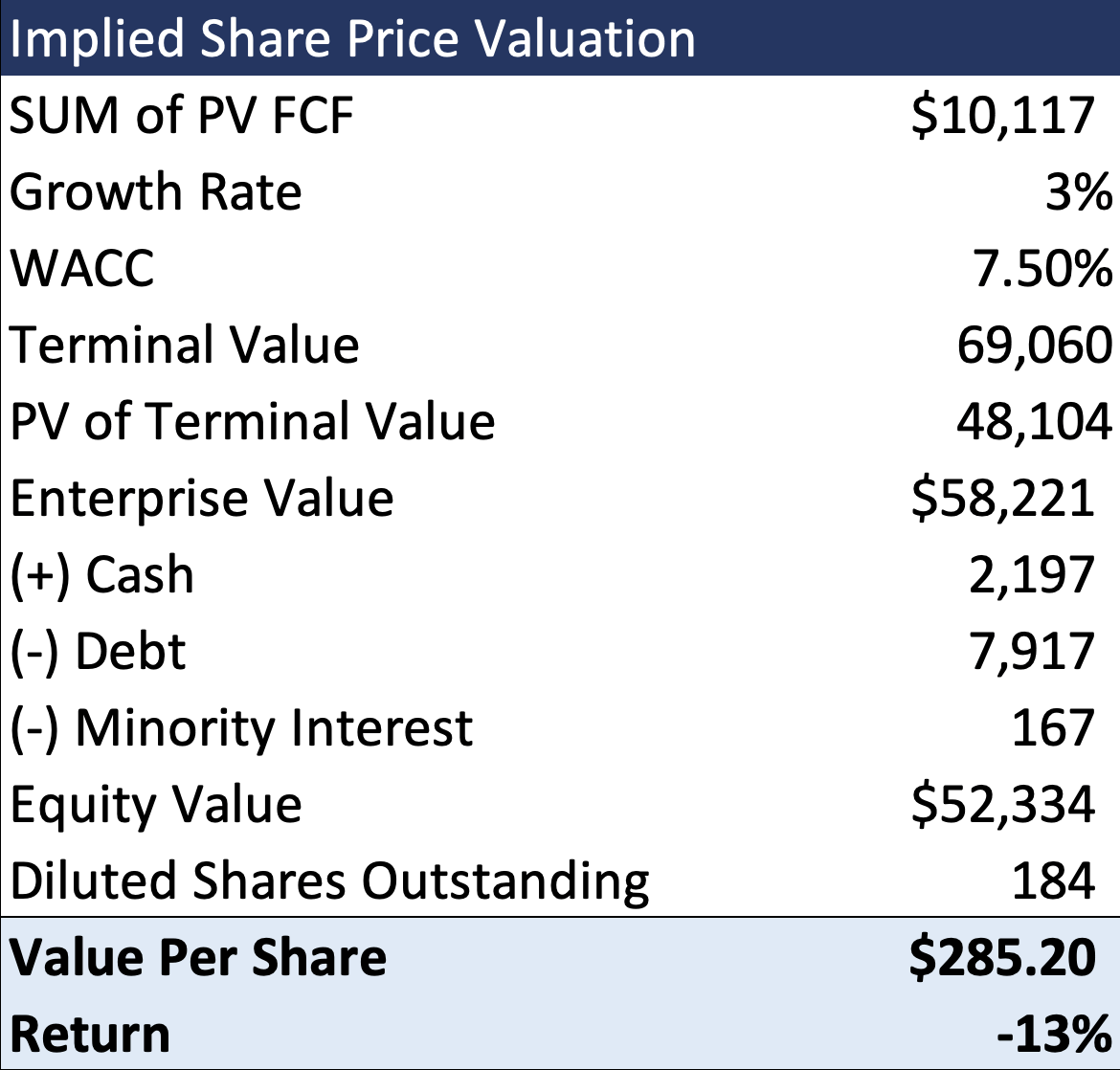

Moody's stock is currently trading at a P/E ratio of 37x and an EV/EBITDA ratio of 29x . Both ratios are trading above their 5-year average. Moody's projected at least 10% revenue growth for the next 5 years in their Q1-22 investor presentation, but revenue declined by 12% in 2023. The company kept the same guidance in their Q1-23 investor presentation, which tells me they are pretty confident about growth despite the revenue slowdown. My assumptions are that MA's revenue will grow at a CAGR of 10% in the next 5 years and MIS's by 8%, which translates into total revenue growing at 9.5%. Given those assumptions, I was able to forecast the company's financials five years into the future. Using a discount rate of 7.5%, I discounted the cash flows and terminal value back into the future. Given that, I got an equity value of ~$52 billion, or $285 per share, which represents a downside of 13% from the current price of $327.

{kind=link}

Why Hold?

Some of you might be wondering why I assigned a hold if there is a 13% downside and not a sell. Well, let me explain. A 13% downside for me doesn't necessarily mean one has to sell the stock; it means that now isn't a good time to buy in. Plus stocks, such as Moody's, have been great compounders for years. In my opinion, the current price doesn't look very attractive since the stock is trading close to its 52-week high, and based on its trading history (P/E and EV/EBITDA), it looks overvalued.

Risks

1) From time to time, you see a story in the press criticizing Moody's ratings. In January 2017, Moody's entered into an $864 million settlement with the U.S. Department of Justice and attorneys general from various states relating to civil claims on structured finance ratings. The company also gave SVB Bank a credit rating of A before it collapsed back in March.

2) Moody's exposure to bond issuance is no joke and should be taken seriously. Bond issuance can be influenced by macroeconomic variables such as interest rates, inflation, and credit spreads. 31% of Moody's revenue comes from transaction-based sources. The primary driver of transaction-based revenue is new issuance. As new issuances decline, so does Moody's revenue.

Conclusion

The bottom line is that Moody's has a good business model underpinned by a wide economic moat. MA still has more room for growth. I believe that high recurring revenue from MA should help offset some losses in the MIS segment. I expect the MIS segment to recover as macro conditions get better. Management has done a good job of returning cash to shareholders through dividends and share buybacks. I assign a hold on the company due to its current price (fairly valued), and trading multiples. As always I will leave you with a quote.

"The stock market is a device to transfer money from the impatient to the patient." - Warren Buffet

For further details see:

Moody's: Dominant Business But A Little Pricey